Q4FY23

VST Tillers Concall_LT.pdf (248.5 KB)

Concall Notes

[Discl: Not invested]

Recently started to track this company with a token investment. Guidance from the management looks a little on the unrealistic side which was 3000 crores in FY25 but later updated to FY26 citing Covid. The numbers from December sales do not look very promising.

Nippon India Mutual Fund buys 1,22,000 shares from open market. The notification was posted by VST TILLER too.

Their ownership increased from 6.92% to 8.33%.

Source:

9195E97B_FAFF_4DC3_831A_15035FA07F3F_102451.pdf (288.8 KB)

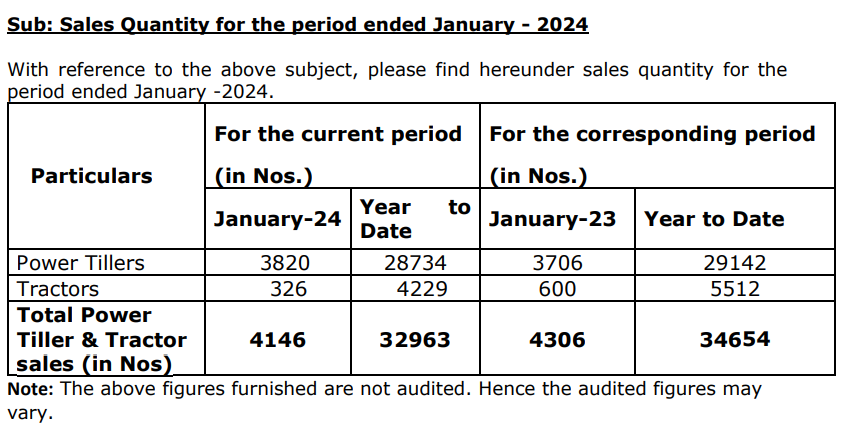

Jan 2024 monthly updated posted by the company.

Power Tillers: 3820 (3706 in Jan 2023)

Tractors: 326 (600 in Jan 2023)

Tractors sales are down 45% YoY. Power Tillers sales up 3.23% YoY.

Company in a media release announced that "The joint venture entity, VST Zetor Pvt Ltd., between the company and HTC Investemnts a.s (owner of brand “Zetor”) commenced operations in the quarter. "

Extremely poor results from the company. There seems to be a deep cyclical element to this company similar to agro chemicals since they are heavily dependent on agriculture which depends on monsoons. Would be interesting to see if the management is still firm on the guidance of 3000 crore by 2026.

Agreed! The guidance shared by the management seems so far fetched at this point!

Disclosure: Tracking it since I read about the revenue guidance but now seeming pointless

One should now read the FY2026 target as FY2027 target, which is still impressive if achieved (30% CAGR revenue growth). They believe, that focusing on small farm mechanization themes, getting into new segments with joint ventures, getting into the production of new products, and getting into new markets will get them to the target.

Best Regards

Shobhit

Tech, innovation initiative. Article also talks about the 2 subsidiaries in US.

Company walking the talk atleast w.r.t to initiatives and efforts?

What do you think?

I think the business is at a inflection point , they struggled to cross 1000 cr sales since last 2 years but now with this quarter results looks like the momentum is back in sales . The growth targets are impressive and rupee depreciating will add to bottom line . The stock chart is also speaking volumes when its just isn’t falling at all in this kind of markets . with 3000 cr sales and 12 to 13% profit , the co can do 400 cr odd profit in 2027 and with a 22x historical PE it converts to a mcap of 8000 cr . current mcap is 4200 cr. converting into 2x candidate in 2 years which isn’t bad in such volatile markets .

It was a good monsoon season in India. Rural spending might rise. Expecting good sales of tractors and other farm equipments. Company posted good growth in power tillers sale in last monthly update.

Back till 2022 also, sales target of 3000 crores is mentioned in this thread. Sometimes for FY25, now for FY27. In the meantime, actual sales for FY25 is flattish at 1000 crores. Q1FY26 was high growth due to lower base effect.

Is the mgmt. of this company trustworthy when it comes to guidance or what is the story for non achievement of longer term revenue target??