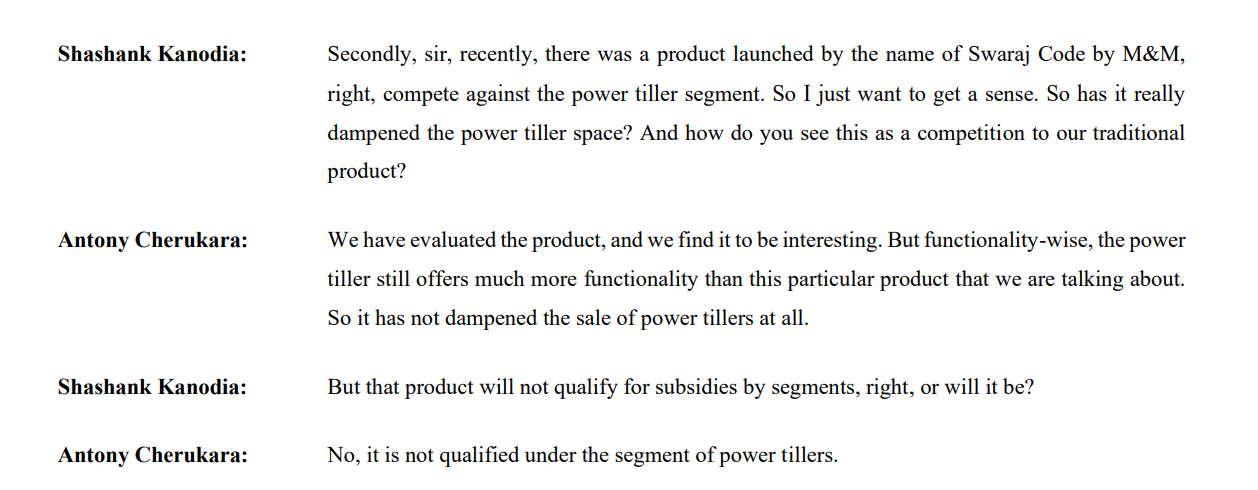

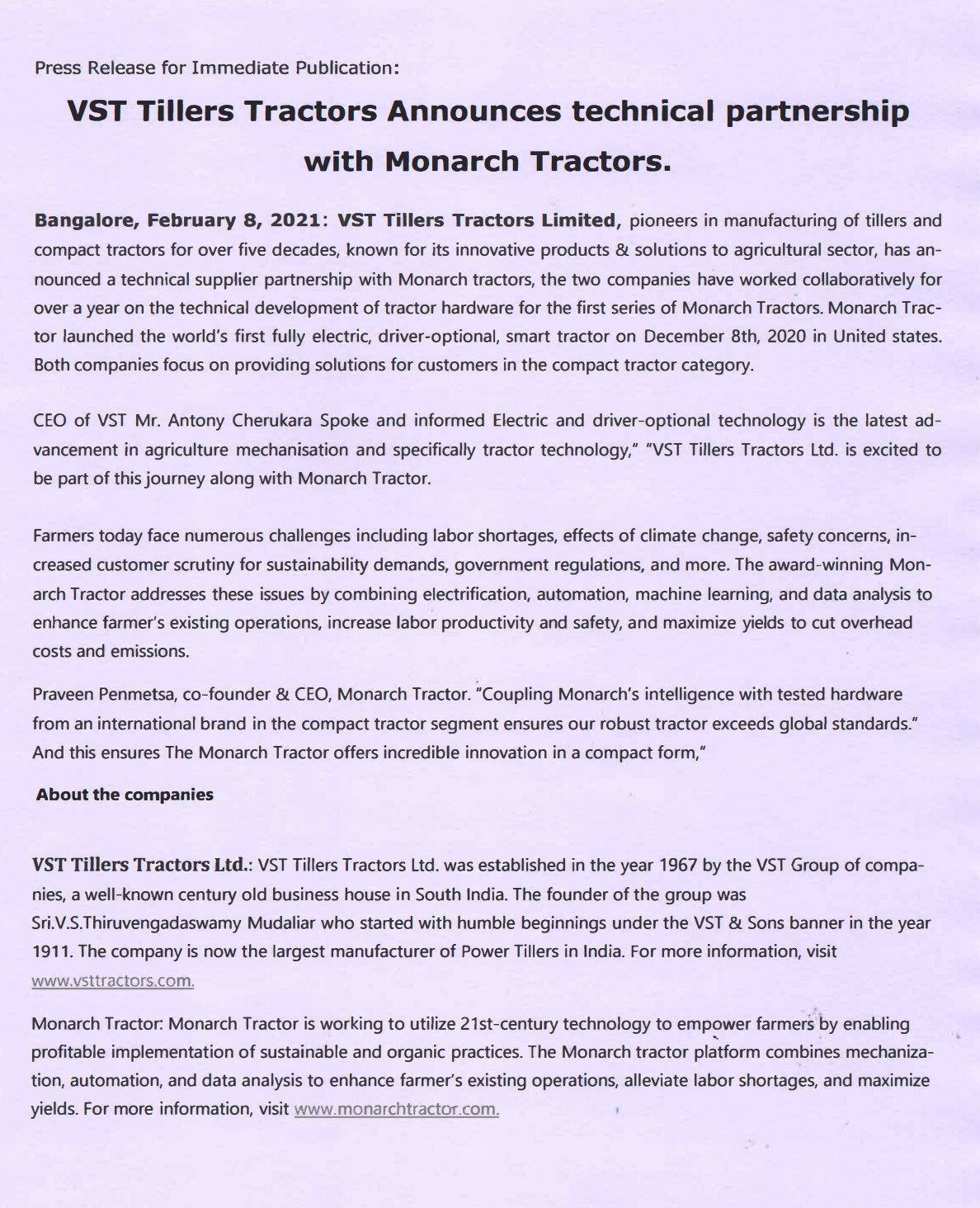

Came across new CEO, very dynamic, ex Mahindra with lot of fire in the belly. New CFO an ex CIPLA guy with very strong pedigree and culturally very strong besides strong competencies and experience. Good governance with very strong management team at the top and with razor sharp focus on the execution. The team knows the market, has a good connect with farmers and strong brand recall. They are eyeing for 3000 cr topline by next 3 to 4 years, even if they end up achieving 70% of this, this will generate very strong cagr. Balance sheet is strong and clean with no debt and and strong cashflows (company is generating free cash flows). Dividend payout regular. Company has been growing all through internal accruals with no dilution and negligible debt over last decade. Product is strong and they are near market leader in the tiller segment. Recent push in the marketing, branding is also visible.

The stock shows multiple triggers.

Have invested in 2008 and stayed with it till 2010 and made good money. Exited because of other priorities.

Disclosure: Currently invested.

I first looked at vst tillers in mid 2019 and decided to wait n watch (I used to run a concentrated portfolio back then and one Can’t afford too many mistakes in a 10 stock portfolio). Capital allocation, industry headwinds, employee fraud, ceo resignation were among reasons that deterred me from investing back then. However as they say everything is good at a price.Vst may not get re- rated but earnings growth alone can make this a good bet and we have good reason to believe that is possible. The new ceo over the last 2 years has done a lot to inspire confidence and at this point one can only hope that the same continues. It’s just that I am not comfortable betting big on anything that’s linked to the agrarian economy Hence a 3% allocation here

I first looked at vst tillers in mid 2019 and decided to wait n watch (I used to run a concentrated portfolio back then and one Can’t afford too many mistakes in a 10 stock portfolio). Capital allocation, industry headwinds, employee fraud, ceo resignation were among reasons that deterred me from investing back then. However as they say everything is good at a price.Vst may not get re- rated but earnings growth alone can make this a good bet and we have good reason to believe that is possible. The new ceo over the last 2 years has done a lot to inspire confidence and at this point one can only hope that the same continues. It’s just that I am not comfortable betting big on anything that’s linked to the agrarian economy Hence a 3% allocation here