Hi All

So this is my portfolio which I’ve wanted to share for very long now, What worried me was that my friends here would bang me for having such a concentrated one. But now I am just worried sometimes looking at it if is really that bad, You’ll understand why when you complete reading this

Let’s go into the den, Weightage wise:

Laurus Labs 25%: This might be by far the most discussed share here at VP. I bought this share just when the market started to realize the story. The main reason for buying it was the exceptional management by dr. Chava and their adaptability to the changes in the market. When they knew that the main cash cow of the company might turn obsolete in the times to come, They just work on towards moving to more juicy streams of revenue. I shall be holding this one for long.

Deepak Nitrite 21% Integrated chem player moving towards specialty chemicals. Every Qtr one of their verticals is saving the show. But with the great team at the helm, The time for firing on all cylinders is coming up. Could not build a position early on, Managed to build one later. I absolutely love their ARs which are vaults of knowledge and their transparency to the investors.

Reliance 18% Bought this share to reduce the volatility of my portfolio since it was entirely made of small-caps and midcaps. Bought it when Ambani told about their plan to go on to zero debt. What was initially bought as a stabilizer, Once they came open about their green plans I bought some more and am waiting to see how this one shapes up.

Jubliant Ingreiva 12% Was worried about the way in which they were dealing with the pollution issues coming up at their plants, A bit of deep-dive revealed that they were trying to improve on this front. The company is now diversifying into the diktene and acetlyl chain streams. Still nervous about the pollution issues, But am gradually accumulating it.

Strides 11% unofficially the company with the highest bad luck in the market right now. Bought it when Arun started buying, I Will continue to buy. Looking for the stellis opp and at this price, I suppose the remaining business of strides is a no-brainer. I for one strongly believed that Arun would jump ship to stellis after it was strong enough to support itself, But with the downturn in the market, and the sputnik issue I hope it is still times away. His return to the executive positions is an extra positive.

Tata Motors 13% Bought it at the bottom, Always been fascinated by the company and the path they are now traveling on. I am interested in the PV and its EV subdivision. On their range of products, They are trying to hear to users and rectify the issues and improve them in the next iterations (facelifts). There is also a considerable change in their dealer attitude (as far as I have interacted with). Hope they don’t start to lose steam midway.

So if you’ve managed to see the name, You would know that if the chem and pharma are removed out of my PF it will cease to exist. I also understand this but I feel that only Ch & P are my areas of competence and hence feel comfortable investing in them which means it will be killed when something bad sector-specific happens.Also, I invest based on the stories, the management, and their transparency rather than going the textbook financial names. I am always looking for new names and stories to invest in. I have learned a lot from here and it was @Malkd who inspired me to concentrate on my PF (Thanks Bro). Sorry if this post is not as polished as it should be, I just wanted to bring it out first somehow. I will add up my progress as we go on. Let me know your thoughts about the PF.

Concentration risk in portfolio is taken by someone who have very strong conviction about business & its fundamentals. It can give you great returns, if your bet holds correct with time. But we have to always remember that at the end of the day you are not the promoter of company, so you are not running the day to day show of company and hence likely to cause errors in predicting the future trends of business.

Disclosure: Holding Ghcl which is 37.5% of my portfolio at avg. price of 176.

I hold 58% of your portfolio and you rightly following the stories. As Warren baffett says, the business should be seen as an evolving movie. All your holdings have an interesting story evolving and at an interesting juncture.

Stellis story is very promising but, it is still some time away right! And how would stellis will be an entity separating from strides is a questionable part.

Strides has not been consistent in terms delivery.

Will the concentrated portfolio deserve strides at this moment is the only dilemma, otherwise portfolio looks solid.

Let’s hope so. On your second point, True that We only know what those who run want us to know and we are bound to make errors. Learning more to sense the trends might guard us a bit, but in the end if it is bound to happen it will.

Brother

Why not? I somehow like that character and decided to make it my pen name

Good to know that there is a similarity. Yeah I too feel the same, They all are great stories but there is a lot of Work in progress for them to go on happily.

Regarding stellis and strides, On everything in my portfolio I had a hunch when they were at their baddest .I decided to ignore them, Only to pay much more later. Even though the separation is quite some time away I decided to take a plunge now to grab the share at its weakest. Now can It backfire? Yes, it could but I am prepared for it and just wanted to see it through (until there is a CG issue). I do hope that stellis is demerged rather than IPO, But I wouldn’t worry much. It is either the cash for the debt or the shares (either good for the company or for me).

So even though there was a dilemma, I just wanted to catch it before a turnaround and am monitoring it for the same. Hope it does

Good luck to you too

Leverage Buying:

Working in finance myself, I always knew that leverage buying would land me in deep trouble. But there was always an intent to take extreme risks for faster capital growth. Normal browsing in Twitter/Reddit will always have a story of how many issues leverage buying causes. But for once, Me earning just past half a lakh per month my journey would be very long to the day when I cross a crore (my target for now) even with all the compounding.

So just past the dip in march 2020, I went to Kotak LAS asking them for their approved list. Got a PL. Sold the unapproved securities (1) in my existing PF, invested it in large caps, pledged them to buy midcaps, and further pledged them to get small caps (unapproved which I sold in the first place) which are typically not in their approved lists .

If I had 10 L in the first place, I would get 5 L for midcaps and 2.5 L for small-caps on leverage all on a mere interest of 8.5 %.

This was/is/will be the worst idea ever devised by anyone, But I always knew that the market will fly for some time after the dip giving me time to sort it out. I just ensured that I could comfortably service my debt (interest) using my normal job. With the money in hand, I just made myself understand that I would not worry even if my complete investment becomes zero. I caused multiple botches on entry prices, ticket sizes, and allocation of sectors, But the bull market helped in minimal punishment.

Once the Shares started rising and I started to build a concentrated long-term portfolio by selling some positions as they entered their exit prices. The final portfolio in my profile was built in this way. After all these days, I am near to closing the original loan. Now looking back I just understand how lucky I have been, But the reward at the end makes it worth it. But yes if you take risks under your caliber (understanding the negative aspects and accepting them if they happen) in any aspect of life, There might be a reward that will make the risk worth it.

I would only say about this strategy as you are just plain lucky. What if the downside of March 2020 would have lingered for more than 3 years? You might end up losing your original capital faster. This strategy is a sureshot way of losing capital and violates the Buffet Principle of

Never Lose the money.

in Nassim Taleb words…You are just a lucky idiot…sorry for the word…but its what it is…your views?

It takes real gut to execute what you just said, may be luck favours the brave.

Do hope you have not got BP!

I too had some similar encounter in 2020 with idea stock, and lost considerable amount before correcting my course immediately to more stable approach.

It’s not worth to take that risk anymore, but you have that approach which is exposed to very high risk, may be, time & reward only should justify.

I had factored that in by providing for 10 % further down from the entry point through an FD (once LTV breaches I would have used it) and that if the PF lingered flat my job would be enough to service the debt. Thankfully never had to use the FD but yeah the earlier structure had multiple issues which would have held my neck if the PF reversed its direction.

No offense taken, It is true in its context. But yeah it worked for me and I was a bit extra lucky. But capital loss (actual not notional) is not possible as far as I have enough money to bring in for LTV and for interest. Whatever might have happened, It has brought me to a number I never imagined I would achieve so soon.

Hope it continues

My day job as a credit risk analyst is very very stressful to the extent that I cannot stress how stressful it is at times. Stresses apart, I went in after completely understanding the risks that had helped to a greater extent which helped in sitting through it.

My only moments of sadness were that I would ignore my gut feeling in entries, convictions, and things of that sort. When I had built enough conviction, It would be way off in prices.

Mine might be a one-off good experience which is what tells me not to test it too often.

In my humble opinion, I always feel that there is an element of risk-taking if we look for it. I have started to build a multi-tiered model implementing all those things that I have learned, what to limit the risks, and trying to decide btw blue-chips and dividend funds (regular payouts might help in interest service). This time I plan to backtest it and devise various outcomes post which will deploy it. Hopefully will document it.

Portfolio update: Risks of leveraged buying

If you have read my thread, You would have come to know that I am a plainly lucky guy who has taken risks out of my reach.

But everything that goes up should come down, right?

When the market started dipping, I started getting a few margin calls in my overdraft (LAS) account. I could manage the same with my savings. Suddenly the market started to just fall down, Now I could not manage margins owing to the sheer scale of my leveraged buying (W r t my finances). I was faced with two options. One is to sell my holdings as required and pay off the margin calls (Since all my largecaps were pledged for LAS, I had only small caps free which again were battered by that time), While the other option was to get money. Hence went with G Loans, Paid enough to prevent margin calls and when the markets are rising now I am repaying the loans and further increasing positions. This was a great experience and has further taught me to multi-collateralize my leveraged positions.

Updates to the PF: Natural Capsules Bought - The company looks good Increased sales Y-o-Y owing to the machinery upgrades. Wanted to capture the opportunity in the steroid API sales. Diamines and chemicals - Ultra conservative and secretive management, Looks like they don’t know that any other company except theirs exists in the world. However, they exist in a less crowded industry and are doing a 10X CAPEX which is to come on line starting FY end in stages. PEL Added as the special situation (demerger)

Looking to add more natural capsules, Chemcon, Diamines & Grasim (B2B & Paint)

Very sorry if the wordings are not polished, Wanted to share an update

Update after a year - Was active on the forum but never could find time to update this page:

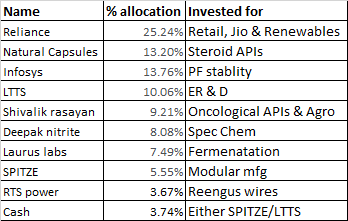

Jul 23 :

Current portfolio holdings:

Infosys - Added in the dip - Consistent performer - Free cash company

LTTS - Added for the ER&D opportunity- Expect plant engineering & transportation to contribute more to the pie hereon - Waiting for chances to add it on dips to increase overall allocation.

SPITZE - maruti interior products - a modular kitchen wardrobe and railings mfg company - Has two brands every day and Spitze - I got introduced to the company while making over my kitchen - found it reliable to use – Found the management hungry for growth and hence bought in the opp.

RTS Power - Have started buying into the company pinning hopes on The RDSS scheme of the government involves revamp of the discom infra to improve power quality. It is a fully-fledged electrical supplier from transformers to wires .its subsidiary “Reengus Wires” which is involved in electrical conductor production has also become operational. Co has reduced receivables and is promising exit in low /No profit segments. More money is to be poured into the subsidiary which turned profitable recently. Extremely low valued - net debt-free company.

Overall, I have added more money to my large caps.

Constants:

Laurus labs

Deepak nitrite

Additions:

Shivalik rasayan

Natural Capsules

Exits:

TaMo

Ingreiva

Strides

PEL/PPL

I’ve forgotten what I thought for the exits but no money was taken out - Hence, Consider all additions have been funded by the exits.

Will update the thread regularly- It reminds me of how the thesis changes with market cycles.

Having only attended very few AGMs, This time i wanted to make sure that i attended the Natural capsules AGM at any cost. I had a review with my management at my workplace at 12, The AGM was at 11. Could not attend to the questions properly as was anxious.

So, Here goes the 30th AGM of Natural capsules Ltd:

Mr Chairman called the meeting to order after having sufficient quorum. As usual, The chairman was being actively guided by someone from his side to help with his speech. It went as usual about the company and about the management.

Next came, Mr Sunil Mundra the MD - He started running us through the facts:

The revenue and profit were up 28 & 29 % YoY - increase in the capsules business.

3 new hard capsule machinery to be installed in this quarter - Company sees sufficient demand for the capacity too.

3 New HPMC machines will be installed this year - Plant based capsules predominantly used for nutraceuticals - Company finds better margins here when compared to the regular capsules.

Exports - Company reports a 72% increase in exports taking the total share of exports in revenue to 22% - MD congratulated the export marketing team

Regarding the API business, They have diluted equity to help them with the capital funds and WC.

They plan not to commit on the entire capital machinery at one go - Company will add capacity as the commercial utilization increases until they hit the planned capacity - Which will help in reducing capital requirement and fixed costs during the beginning.

The sampling data for API offtake customers will depend on their profile. Some will be okay with the sample data they have, Some will require 6 months data and so on depending on the increasing profile.

Company has started to give discounts basis volume for capsule orders. There are some bad payments (3.2 crore I think) that are stuck on various levels of litigation. Company has fully provided for them.

Company expects the Kilo lab of biogenex to go live the next quarter. Commercial and large quantity lab should go live on the final quarter.

30-40% API capacity utilization will come in the current year and 60% the upcoming year.

Overall, The company is very positive on their plans and are confident on achieving it. I was initially hesitant on the management. But after seeing Mr.Mundra - i feel that he is a hands on person, Who could answer questions on the fly at ease. He was happy to explain.

I was actually feeling happy with the management and started typing my questions too - Only to be rudely awakened that my review was preponed.

The theme seems to continue positive, I have requested the CS for a plant visit and if things go well - I will continue buying this

Disc: Invested, Second largest alloc

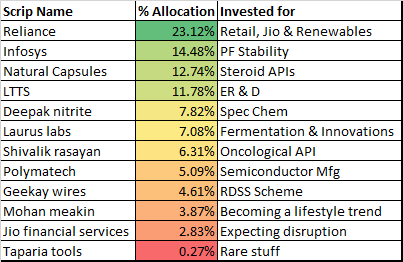

I worked - Got my salary 2X which opened a lot new opportunities of investment. PF

Laurus labs - I find the current situation to be a weakness in the stock / business. I still find the company to be highly innovative except for the concern whether they are getting into too much stuff parallelly. Adding them constantly hoping to make a higher allocation after RIL.

Polymatech - I had already burnt my hands on paytm, However this was an opportunity i did not want to miss. It is the only semiconductor related share i could get on sane PE. Company is reporting YoY sales improvements and is planning to invest on equipment’s from the IPO proceeds as well. Ultra low number of employees is a red flag, Will wait and decide on holding it.

Mohan Meakin - For long wanted to get a alcohol share which is cheaply valued, Has a track record of people actually liking their stuff. But all those shares are having bizarre PEs. Hence, Looked and picked this one up.

Jio Financial - Got it during demerger - Expecting a disruption from them. Was adding this but there has been a high price bump which has hindered it.

Exits - RTS power (Swapped for Geekay) , SPITZE - Exited post bonus Shopping for : JFS, Laurus, Deepak chemtex

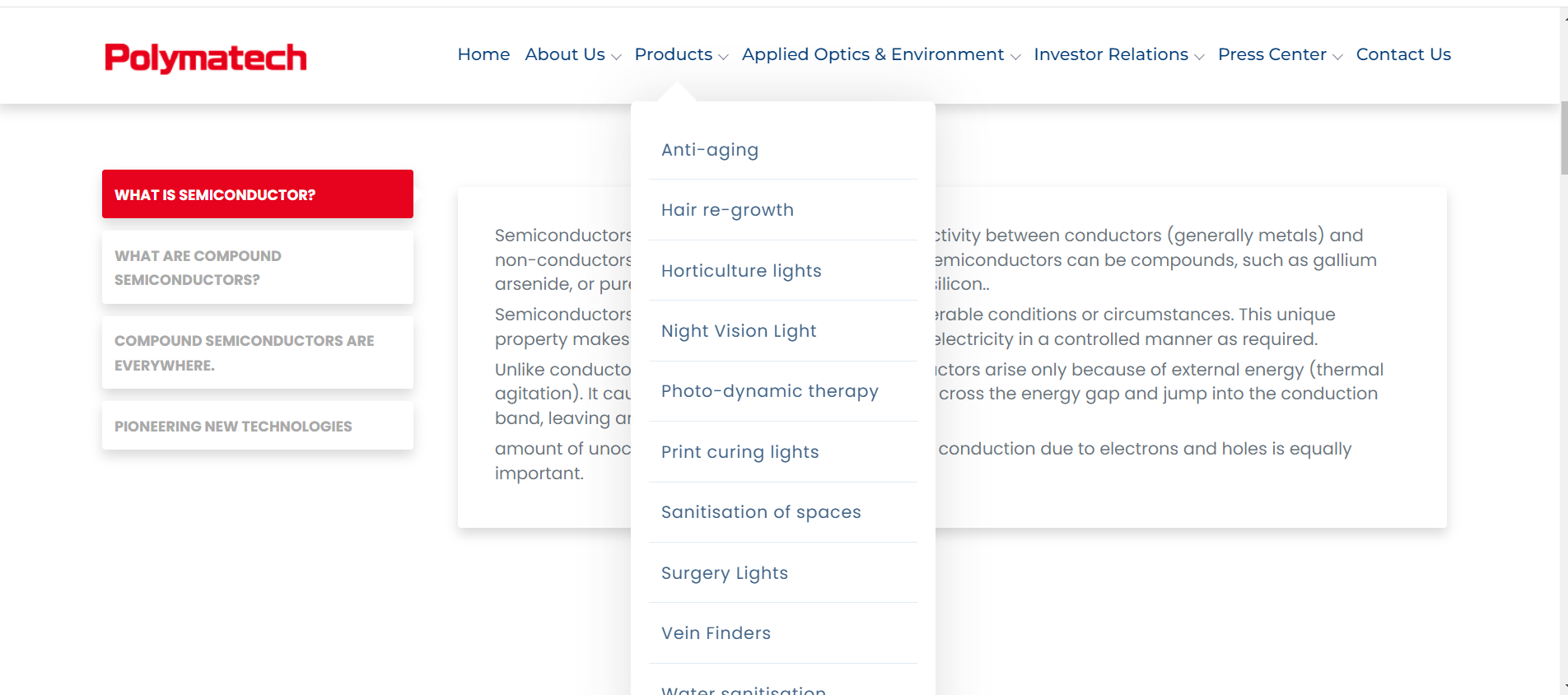

What is the logic behind investing in Polymatech. It’s not even remotely close to semiconductor fabrication - I am from this industry and involved in a few live fabrication deals. Their website confirms they are either scamsters or at best dishonest. Look at the products they mention - Hair re-growth lol.

Please do not put your hard earned money into scammy companies, open a vested account and buy world-class companies like Nvidia, ASML, Applied Materials.

Did not buy polymatech expecting them to be a Nvidia competitor

I understand from my limited knowledge that opto-semiconductors work with the absorption and emission of light, such as LED diodes.

In this context, the hair regrowth lights produced by the company might be devices that emit low-level laser light at specific wavelengths, typically in the red or near-infrared spectrum. This light is thought to penetrate the scalp and stimulate cellular activity within the hair follicles.

Whether this treatment is effective or not is a separate matter. (there were studies in both ways).

I do find too much good floating about the company which is making me jittery. But until we have some quantifiable flags, i find the company to be doing extremely good and will continue holding

I am only pointing out that they are marketing themselves as India’s first semiconductor chip manufacturer and you mentioned you wanted a semiconductor play.

Looking at the products they mention in opto, the technology is 40-50 years old. There’s no moat. So this is not a semicon play more an EMS play.

A lot of people on twitter have also pointed out that they have been using stock footage and passing it of as their own factory. Given this much dishonesty in a middle of bull market, I am just trying to understand why you would like to risk 5% of your portfolio when there are far far better options available through Vested?