Great results.

Revenue 10.88 Crore vs 15.89 crore

PBT 86 L Vs 1.47 Crore

PAT 62 L vs 1.06 C

EPS 0.68 vs 1.17

Link to results https://www.bseindia.com/xml-data/corpfiling/AttachLive/5674d7e2-59b3-4329-b883-424e7baea59c.pdf

disc: 4% of PF

Great results.

Revenue 10.88 Crore vs 15.89 crore

PBT 86 L Vs 1.47 Crore

PAT 62 L vs 1.06 C

EPS 0.68 vs 1.17

Link to results https://www.bseindia.com/xml-data/corpfiling/AttachLive/5674d7e2-59b3-4329-b883-424e7baea59c.pdf

disc: 4% of PF

So it looks like they were able to pass on higher import rates at a higher margin. So demand of finished products remained high.

In the last time when they had import rates, I couldn’t see much impact of revenue/profits. Hope they would be able to maintain margins when they start production of J Acid.

Hey James

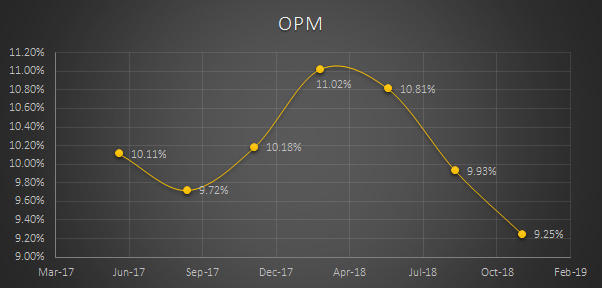

Good topline numbers by the company but actually the operating margin is low in the last 2 odd years.

Also COGS as a % of operating revenue is ~75% compared to QoQ and YoY of ~72%.

I am assuming as J acid production takes effect we should see better margins.

Rgds

As per telephonic talk with sumish mody, j acid will start within 3 months.Once j acid started,margins will improve.

Disc…invested …9% of portfolio

Great results with around 70% qoq growth and J acid is still to come. Great return on equity at so low a price. Only manufacturer in India for certain chemicals and also only manufacturer in the world for another. The stock should logically be priced higher at 30 PE or more, if not for the overhang of related party transactions which the management could settle by merging the group company. Also by retaining the earnings and using the retained earnings for further expansion the stock should boom

Disclosure: Invested 14% of portfolio.

I would like to offer the following observations. I am still learning, so please do correct me where I am wrong.

IMHO this company could at the most, be a short-term bet, as also mentioned above. However, I feel that it is currently overpriced.

I welcome your comments on my observations, so that I can improve my knowledge.

Thanks

Sandeep

Let me try and tackle few of these

1.All the other employers could be Contractual or Casual Labourers that don’t show up in the company’s wage payroll.

2. Even most big chemical companies in india don’t do any R&D its only for names sake. Its a lot about getting a guy who knows a product having worked in some other company who basically is responsible for new products.

3. will have to check

4. You would have to check the bifurcation b/w imports/ exports in volumes terms to get a better idea about this.

5. I would not read too much into this. all businesses are cyclical given long enough time.

6. Debtors are quite reasonable and intact good, given its a B to B business. Chinese firms offer credit of almost 6 months to their customers.

7. inventory turnover could be low because they might be holding certain raw materials against booked orders to save themselves against price volatility.

8. Remuneration : this could actually be a good sign as well.

9.Thats what most small companies plants look like, it a lot about functionality rather than looks in small companies. they have to sweat all their assets. A lot of these companies also buy second hand process equipments that are discarded by pharma companies.

10.I look a illiquidity as a good thing.

11Agree J acid internal production could be a good thing.

Not invested but interested nonetheless

Q4 results announced.

Sales grew by 20% Q-Q and 26% Y-Y, However profit is flat Q-Q and degrew by 30% Y-o-Y

EPS is flat at 0.79 for the quarter.

In FY19, sales grew by 27% compared to FY18 and profit by 26%.

Results.

Dividend: 0.50 per share.

Disc: Invested 2.5% of PF

I was away for some time so lost track. Any word on production of J acid? Could not find this info. Also the quantity traded has increased recently. Perhaps a good sign???

Regards

Sandeep

Disc: Not invested but watching.

What concern do you see for which the stock is dragging down lower?

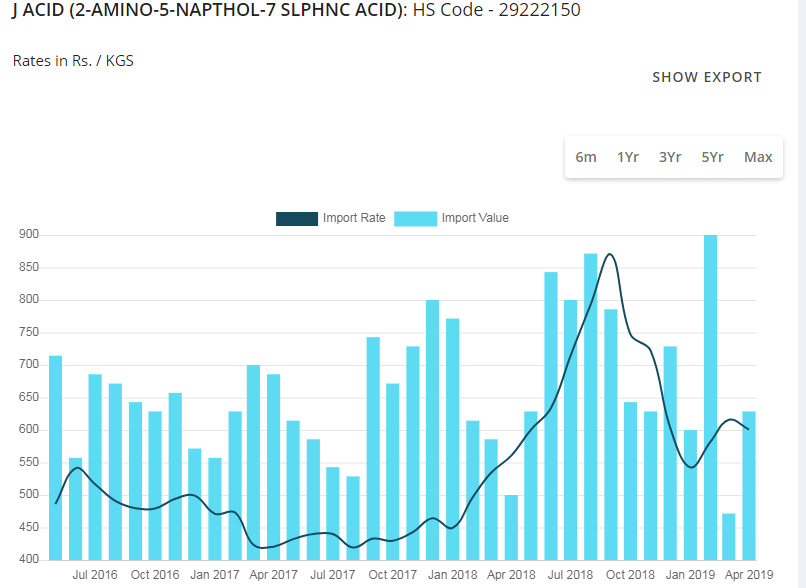

It could be J Acid import rate concerns. I don’t have recent data. Can someone post import rate graph of J Acid (HS code is 29222150) from screener. I would wait for annual report to see guidance for coming year.

What is going here, continuously going down?

J acid import rates started going up in Feb 2018, peaked in Sept 2018, then it came down to May 2018 levels in April 2019 (until we have data). I think if Q4 production used the highest raw material price in Sept-Nov 2018, now this quarter results should be better. There was good import to india in Feb 2019. So I do not see big concern for price correction to the current levels here. I am holding on to my investments and not adding any more. Will wait until annual report and quarterly report.

Thanks for your response this. Appreciate it. Do you see any concern with the company itself as this is run by family members?

This is a nano cap and comes with its associated risks. This is in cyclical industry and can get impacted. I am writing to company to understand progress of J acid in-house production and if already started or not.

Okay, please do share the information. ![]()

J-acid is produced in low volumes for one plant’s internal requirement now. OPM may suffer as company is facing head winds and tries to reduce the inventories and sells the products with low margins due to bleak global outlook and stricter rules for pollution control in India. With this I mean products do not have high pricing power.

Now let us wait for Annual report and quarterly results to understand more. Please see J-acid important rate and quantity trends over last 3 years

Source: screener.in

This is a great insight. Thanks. How do I see this J Acid-related info on Screener.in ? Please guide.

You need to pay and take screener premium. Then you can see import export figures through HS codes.

I paid and subscribed screener premium recently and posted graph by permission from screener team.

Thank you James for your prompt response. I truly appreciate.