A Small Cap that is performing consistantly

As per investment mantras of accomplished investment gurus like Basanth Maheshwari (The Thoughtful Investor), investors should focus on small capitalized companies that are leaders in their sectors and growing their revenues at fast clip, preferably with growing dividend yield.

One small cap company I noticed fulfilling this criteria is Vivid Global Ind Ltd.

It is in a sector where most of the companies are making new 52 week highs i.e Specialty Chemicals

In case of a small cap stock, the first thing we want to be assured is the quality of Management.

For ensuring this we generally do not have much information except the historical figures

of its earnings and return ratios.

As per the experts (The Thoughtful Investor), a company that has grown revenues at a steady rate for a long periods of time without taking too much debt while generating a high degree of ROE and by keeping a reasonable payment rate will essentially have a honest and effective Management.

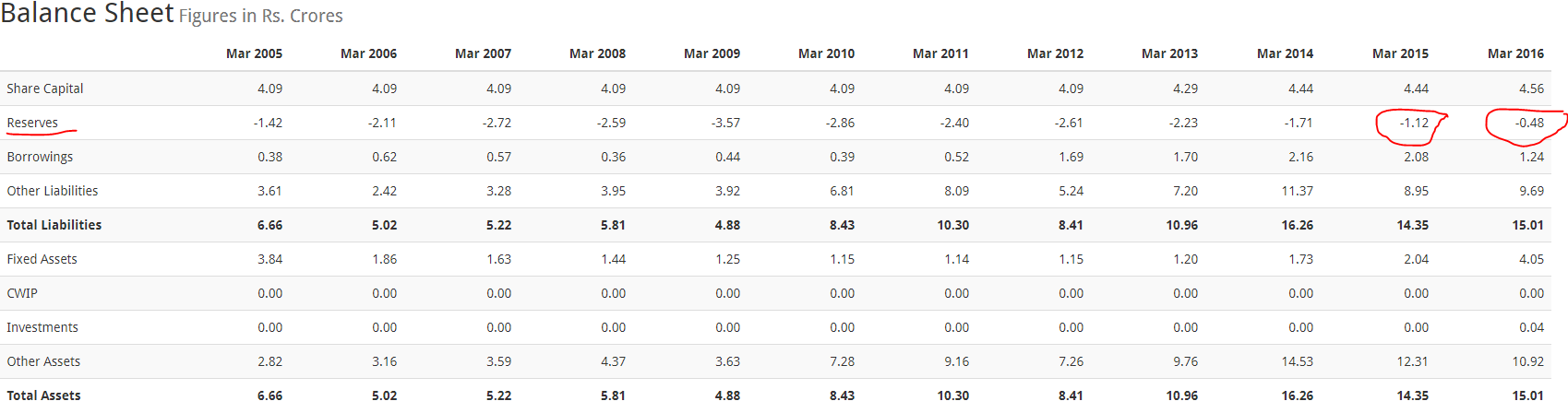

The return ratios of the company during the last 10 years are

Compounded Sales Growth

10 Years: 21.84%

5 Years: 15.5%

3 Years: 20.11%

TTM:12.35%

Compounded Profit Growth

5 Years:16.84%

3 Years:40.94%

TTM:78.79%

Return on Equity

10 Years:22.37%

5 Years:23.18%

3 Years:29.1%

TTM:26.49%

A business that generates high ROE consistently for long periods is most likely a good business.

Few more thing that gives confidence about the Management are

Negligible equity dilution over a period of ten years.

Consistent increase in promoters stake over the years

Coming to the specifics, 2012-13 was the turn around year for the company. The company has concentrated on few products and almost 90% of the India’s export of Phenyl J.Acid is being done by the Company.

The Company has established facilities for various grades of Tobias Acids and commenced production of Tobias Acid and Sulpho Tobias Acid at its Boisar Plant. The company claims that it is 1st plant of Tobias acid in India.

The return on assets of the company has increased consistently from (-) 2.5% in 2012 to 9.93% in 2016. Concentration on few customer specific products may be the reason behind such a performance.

The company recently announced establishment of facilities for commercial production of additional capacity of Tobias Acid 98% from March 2017.

Exports constitutes about 43 % of Sales

With capacity expansion, the margins are likely to be expanded as the company is the only manufacturer in India and benefits of volume expansion kicks in. Again as per experts (The Thoughtful Investor), once a company experiences margin expansion with above average revenue growth, the price earning ratio expands resulting in a disproportionately high gain for initial investors.

The negative side of the company that I noticed are as follows

- Low liquidity and entry and exit at fair prices may be difficult.

- Buying a stock at a time when the company in cyclical industry is doing well may be a risk as the end of cycle may be near.

- Volatility in currency and Crude prices may be another risk

4 Paying high PE for a small cap may be a risk.

But trying to find the best business at the lowest valuation is an exercise that remains unfulfilled almost all the time (The Thoughtful Investor)

The figures are taken from company website, annual reports and Screener.in

It is not a recommendation to invest. Further inputs and analysis by the experts on the board will give a 360 degree view of the company, the industry and will greatly help in understanding the investment worthiness or otherwise of the company.

The Company is listed only in BSE, the price on 01.02.2017 is Rs.43.30 and the market cap is Rs.39.53 crore.

In the budget corporate tax was reduced to 25% for the companies with less than Rs. 50 crore turnover. Since the turnover of the company is less than Rs. 50 crore it will benefit the company, I guess.

Things to watch out for: Company to declare the quarterly results on 03.02.2017.

Disclosure: Invested and my views may be biased. The stock forms 5% of the portfolio.