Good results were due to inventory gain. Needs to be adjusted to see operational performance, which has not improved to that extent.

Does that mean its owe money, shouldn’t it be mentioned as borrowing, whats negative profit ? A loss as reserve. Please clarify if you can !

See the balance sheet has to be balanced by the equation Assets = Liabilities + Equity.

When a company takes on debt, the liabilities side of the equation increases, as is the case here. Depending on the use of debt, either the CWIP, Fixed Assets or Cash increases on the Assets side of the equation to balance it.

Now when a company reports losses, if the company is cash starved it takes on debt to pay off its obligations, in such a case liabilities side of the equation increases, to balance that no assets have been created. So reserves and surplus account is debited, the equity portion of the equation to balance the balance sheet.

So to answer your question, “does that mean it owes money?” Just check the increase in debt in balance sheet with increasing reported losses.

Hope this clears your doubt.

3 Likes

one way of looking at negative book value is - if the company sells all its assets and starts to repay its liabilties it will fall short .

1 Like

It mean that in accumulated loss over life of company is higher than accumulated profit. when company would report profit (assuming no dividend payment and share premium issue), the net profit would be added to reserve and surplus and then Reserve would become positive.

Also I looked at FY10 balance sheet. The net worth was nearly eroded during FY10 if one does not include revaluation reserve of Rs 99.48 Lakhs.

What did Mody have to say about the cyclicality of the business? Almost all of the company’s raw material imports are commodity chemicals, and I would imagine that tobias acid outputs also depend on global demand/supply.

Also how do you rate this company vs. local peers like Kiri Industries and Shree Ram Chemicals?

Stock has corrected almost 18% from 52 WK high of 70. What are we missing here.

Disc: invested from 37 levels

The salary of top level management looks ridiculous. For example I think CFO is paid Rs1.35 lakhs. Even a basic entry level worker would be paid more than that amount. I wonder what kind of talent such salary attracts and what would the actual bottom line be if they are paid proper salaries. On this basis the wafer this profit of Rs2cr all seems optical and it would probably be zero if the top level management is paid the proper amounts.

1 Like

Anyone still following this stock, I am keen to know about their expanded production line? Looks like a good price point to enter for long term…

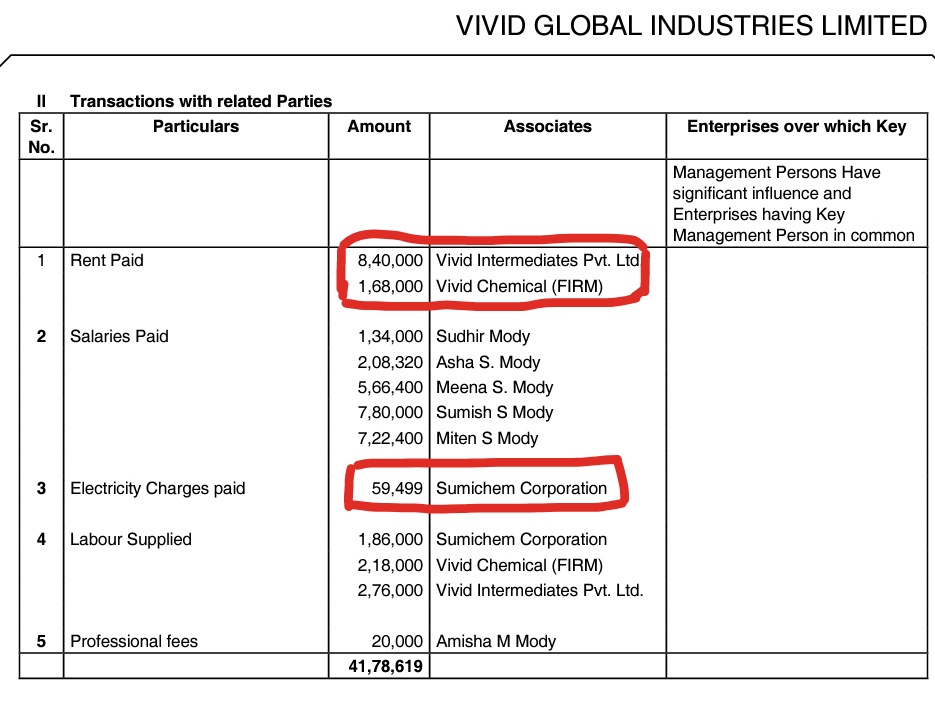

In my limited understanding, they would have taken premises on rent from group company/promoter. Normally electricity bill could be directly paid by the company, however there might only one meter and hence reimbursement of electricity charge to the associate. Please note that I have not even read annual report and this is purely on my understanding which has no objective rationale. Kindly do more due diligence at your end.

Discl: No interest in the company

Look at their results and comment again

Tracking from level of 39, Good result strong fundamentals but some issue with Liquidity of stock and volume.

Discl. Invested little for keep tracking.

Earlier I had exited this as it was more of short term bet. Added 2% PF again with average buy price of 39.80. Recent fall, I believe due to too much expectation on quarterly results. The profit and sales increased though only marginally. Still the journey is forward.

Today I could see this stock appeared in magic formula of screener too. I am still not convinced of long road for this company. But i believe Vivid should continue to grow for few quarters. The stock finds support at around 37 for the last 2 years.

Dividend Payout Ratio: 17.04 % also very good.

Being a small company, very tough to get detailed answers for questions. Only Annual reports and quarterly results are there for a people like me to form a view and see if it sustains and claims materialising or not

As per annual report, future prospects are bright from next year.

Q2 results here

Hi

Although the ratios look good for the company I am a tad worried because of the long term aspects. Essentially its a one trick pony kind of company specializing in dyes and dye intermediates. I was reading the credit report and this is called out differently by saying operations scale will be modest in medium term.

Its main input raw material J acid which is a dye intermediate. If anyone is aware whether the J Acid production which was planned for FY19 has materialized because that could have a significant impact.

Aside J Acid import rates were almost at peak in Oct and Nov in 2018 at 74% YoY & 63% YoY respectively. So if that is the case then YoY numbers in Q3 could take a beating.

Lets see how it turns out.

Rgds

2 Likes

Thank you @deevee for caution and on J Acid import rates. They are much appreciated!

Would you be able to post the charts or import rates for this dye intermediary for last few months, in case you have it.

1 Like

I had talk with company’s employee.According to him,they are going to start j acid within 3 to 6 months at tarapur plant.

3 Likes

Do you have any more information about future expansion.

Hi James

Apologies for the delayed reply. I get this data from screener itself. The HS code is 29222150.

Rgds

1 Like

Vivid global declared good result