I’ve been long time learner on ValuePickr. Fully attribute gains of last few years to generous contributors and teachers like Ayush, Donald, Hitesh and many others.

I recently shuffled my portfolio over the last 4 months. Had an earlier portfolio of Feb 2020 vintage which i felt 4 months ago had become richly valued (cos like APL Apollo, RACL Geartech, Laurus, Neuland, Solara) or where my thesis/understanding of the business went wrong (KSCL, MOSL, OCCL).

I’ve finished all the allocations over the last week. My philosophy is fairy simple:

Must have

Intelligent fanatic promoter - sometimes make exceptions like ITC or SAIL

High current or incremental RoCEs - Again some exceptions like realty or banking if I see an amazing promoter or very long runway

Double down if

3. Clear visibility (mine) on reinvestment of earnings

4. Industry has tailwinds

5. Exceptionally low valuations

Sell if

6. Valuations cross 2.5x my estimate of fair value

7. Business performance deviates from thesis and my understanding

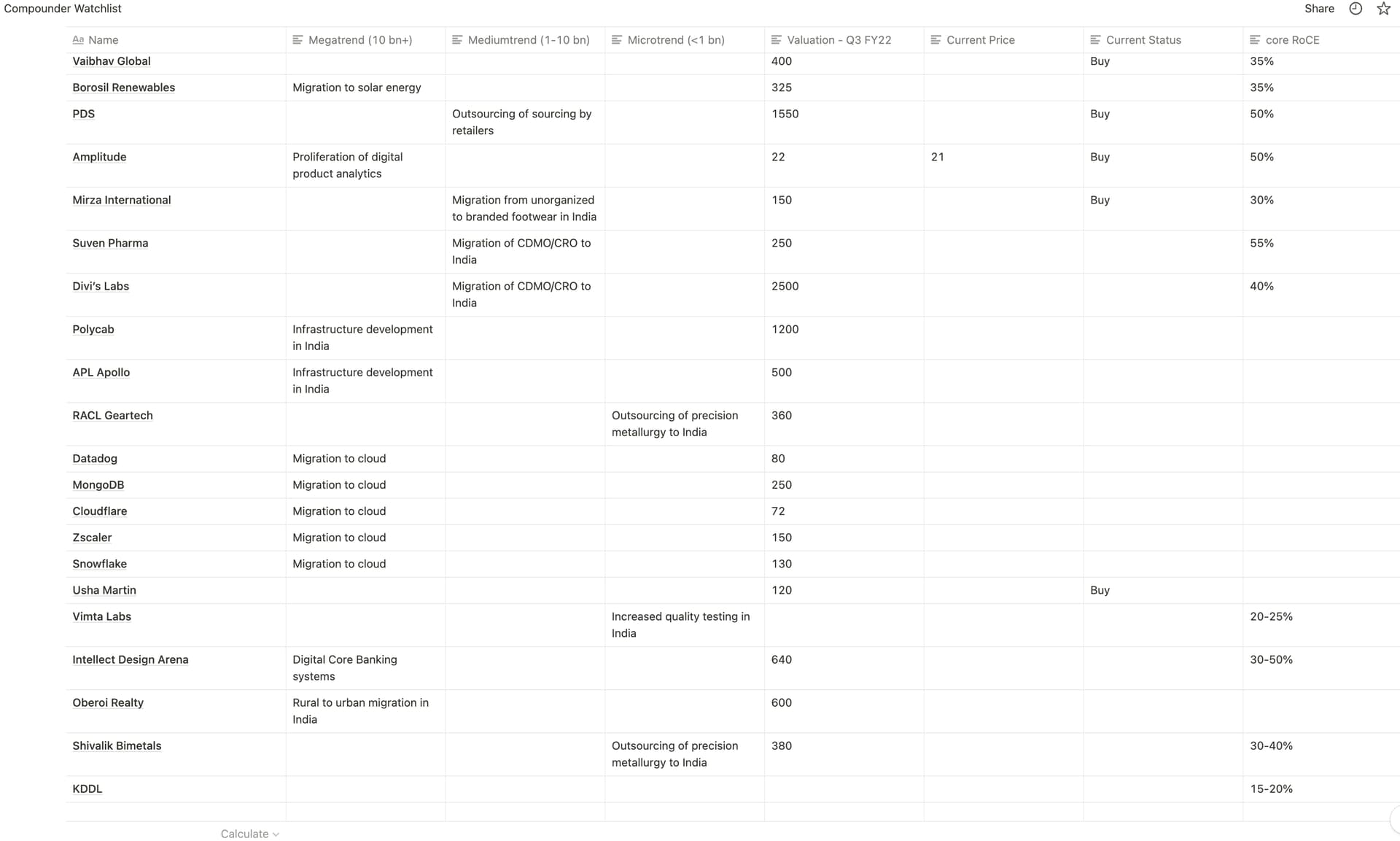

I maintain a watchlist of around 100 cos and the prices that I would buy them at if they fall.

For the last few months, I’ve been focusing on SaaS cos in the US especially category best-in-class like Datadog, Snowflake, Amplitude, Zscaler. Still not within my buying range but have set aside money for these opportunities.

Thanks for sharing. Really like your watchlist framework.

It’s nice to see more people that have invested in PDSL. Curious to know what assumptions went into pricing it at 1550. Could you please share your thoughts?

The core business of sourcing for UK and US retailers is an extraordinary business with current RoCE of 100% +. Add to this the incredible team they have assembled headed by Sanjay Jain and one could justify even a 3 x valuation higher than what I have assigned to it.

However, I have assigned a valuation of INR 4000 cr (INR 1550 stock price at a 1 year forward PE of 15) simply to have a big margin of safety for a business in transition

with a short track record

in a highly inflationary macro environment

with a newly installed management team

If PDS continues to execute for the next 2-3 years as it has for the past 3 years, I have no doubt that it will get rerated to a 30-40x PE company at the least. In each of my investments I try to ensure that if I go wrong in my thesis, the valuation is so comfortable that I don’t lose more than 33% of my invested capital.

the fair values that I assign is more a reflection of my understanding of the business than anything else. For businesses where my understanding is not very deep, I require a fair value in the range of 10-15 PE to invest. In businesses where I have more confidence in reinvestment capabilities and future earnings, I am willing to pay upto even 30 PE (as in the case of Borosil Renewables).

How’d you arrive at this figure? They’ve explained that the RoCE profile for the core business is around 60%, dragged down by the losses in Bangladesh and the venture fund. I estimate FY22 consolidated RoCE to be ~40%.

Thanks I think they’ll deliver 240-250 Cr. of PAT in FY22 itself, so you’ve been very conservative with pricing, and I understand you wanting a margin of safety. If RoCE improves to 40% and they continue to execute, I agree that this business deserves higher multiples.

If you’d like to share more of what you know, and potential anti thesis pointers you’ve studied, come join us at the PDS thread, it’ll be nice to hear from more investors.

Amplitude sells analytics software which enables companies to deep dive on the behavior of their users once integrated into their own technology applications. Amplitude provides this software via SaaS (software as a service) model, charging their subscribers an annual fee. Market perception on AMPL has turned deeply negative in the last 3 months with their stock price crashing 80% from the top. This is due to lower revenue guidance provided by the management for the coming quarter and year - they are expecting to grow at 40% y-o-y rather than the 65% they grew this year. Spenser Skates, the CEO, is a young technologist who has failed to make a favorable impression on wall street analysts.

Amplitude has superb retention metrics - Dollar Based Net Retention Rate (DBNRR) of 125%. Simply put, each cohort of customers spends 25% more the following year (the SaaS equivalent of same store sales growth). G2 is a leading platform for ranking SaaS products. Not only have they ranked amplitude as the top product analytics platform but are themselves Amplitude customers.

Amplitude is also executing the “Land and expand” strategy executed so well by Salesforce and Datadog. It has launched two new products - Amplitude Recommend and AMplitude Experiment in addtion to its core Analytics product. While they do not currently contribute significantly to revenue, they provide an excellent optionality for future growth. Amplitude has also become a Select Technology Partner for Snowflake which I believe should make it easier for Snowflake customers to deploy Amplitude.

My variant perception is that Amplitude has emerged as and will continue to be the category dominator for product analytics the way that Datadog now dominates observability and Salesforce dominates CRM and sales. AMPL cutomers include 26 of the Fortune 100 including most recently Toyota. Amplitude differentiates itself from its competitors (Heap, Mixpanel) by keep a singular focus on user behavior tracking and developing a powerful customizable platform that takes longer to implement but empowers the data science team far more - competitors provide easier to implement platforms with more features but lack the depth of Amplitude’s core offering. Amplitude therefore is suitable for very large and capable data science teams with upwards of 50 data scientists/engineers which I see as a far more lucrative market than the SMB market which I believe competitors will dominate.

After the recent fall, Amplitude now trades at 8x 1 year fwd revenue. Given its gross margins of 80%, huge runway and leadership position, I feel there is not much more downside possible.

Risks

I think the major risk to my thesis is that I may have overestimated their competitive strength vis a vis their competitors. The only way to mitigate that will be to track the feature developments and deal wins on an annual basis. I see absolutely no market risk whatsoever. Product analytics through customized event tracking is in its infancy and should grow at 40% per annum for the next 10-20 years. We have seen repeatedly that category specialists like Snowflake in persistent databases and Datadog in Observability are easily able to out engineer even the tech giants like Amazon, Google and Oracle and emerge as the platform of choice.

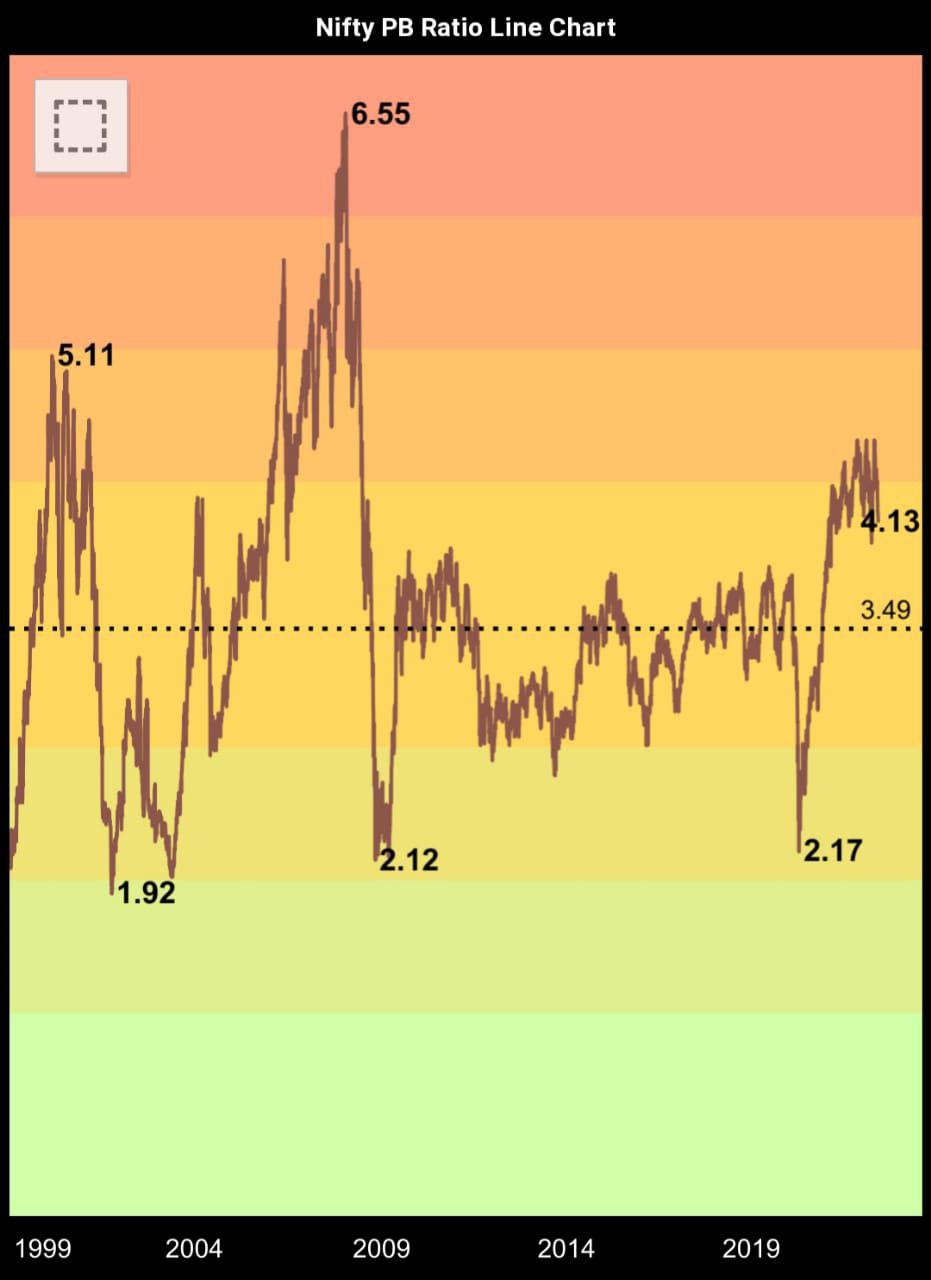

Since 2014, Nifty has only spent less than 30 days below 20 PE. It bottomed at 19 during demonetization and 17 in March 2020 - although it stayed at that level for just 1 day. Between 2011 and 2014, Nifty did spend a significant period of time between 15 and 20 PE. However, there were several factors that warrant a premium PE today than 2011 -

NIFTY RoE was 16% vs 20% today

NIFTY constituents like HDFC Bank, TCS, Infosys and others were not the behemoths they are today with proven track records and massive moats. HDFC bank book value as well as earnings were < 1/10 of today

India GDP growth in 2011 was anemic at 5 percent vs IMF forecast of 8 percent for 2022

Prior to that, NIFTY PE has even fallen to 10 during the GFC. However, nothing in the current environment remotely suggests anything comparable to the global financial contagion of 2008. Even the massive uncertainty of COVID could not drive down NIFTY PE below 20 for more than a week or two.

India non-financial debt to GDP is at a 7 year low because of the deleveraging undertaken over the last 3 years. Bank balance sheets are stress free. Household balance sheets in any case are strong for India relative to other countries.

At an individual company level, there are now several companies available at attractive valuations compared to 6 months ago. The vast majority of companies I track have compounded their earnings in this period while their stock prices have fallen.

Based on the above, I’m now fully invested with no cash whatsoever.

One thing we should consider here is that NSE has change methodology of calculating PE from last year. Previously they used to calculated it on standalone earnings and now they have started to use consolidate earning which have given a boost to earning and hence reducing the PE ~18%. So on standalone bases NIFTY PE has gone below 20.

Good point. However, it does not really change the analysis because subsidiary earnings were not meaningful for NIFTY till 2019. For example, reliance subsidiary earnings were close to nil in 2012 while now they are 33 percent of consolidated earnings. Therefore 20 PE 10 years ago on standalone is comparable to 20 PE today on consolidated.

Some increase in PB can be attributed to increasing weightage of IT stocks (TCS, Wipro, Infosys, HCL Tech) and rerating of Reliance due to Jio which commands better valuations as compared to the O2C buisness.

Book value has increased by just 12,000 cr in 6 years even though profits generated are in excess of 100,000 cr. The rest of the money has been paid out in dividends and buybacks. This causes P/B to skyrocket from 3x in 2016 to 8x today. This is why PE is a better metric to assess the general state of valuation of stocks.

Finally, it is definitely possible that the valuation pendulum swings to the other extreme and NIFTY falls even from here. My point is that, based on the general valuation of NIFTY as well as specific stocks that I track, I feel confident of a good long term return from here on out

This is perhaps the facet of investing that I find the hardest and also the one that results in the most number of mistakes by me.

Being an admirer of Buffett and Munger, I’ve always wanted to run a highly concentrated portfolio of 4-6 companies. But over time Ive also reconciled that their approach does not match my personality.

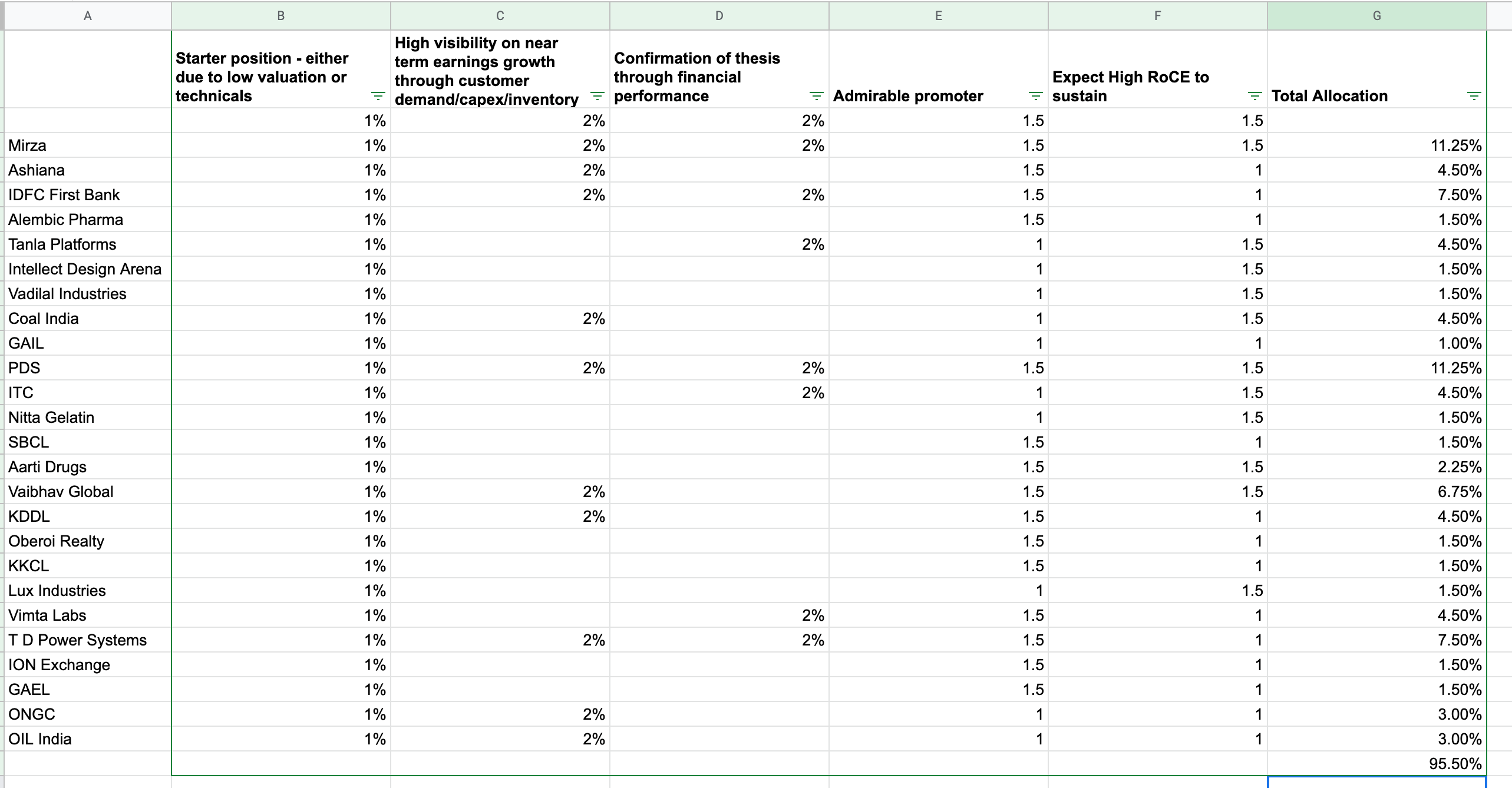

I begin every position as a 1% starter position. My ideas come from 3 sources - this forum, stock reco sites (Stalwart advisory, Katalyst Wealth) and screeners

If upon studying the company, I’m able to make a high confidence forecast of earnings for the next 2 -3 years, I add 2%. Example: ION exchange on every concall used to disclose their engineering order book. Between the Sri lanka order and the cairn India order wins in 2016-17, their order book ran up massively. I used that visibility to increase my position.

If over the next few quarters the company performs as per my thesis. I add another 2%. This oftentimes failed (especially in the bull run of the last 2 years) because the stock would run up out of my buying zone much before results. Earlier, I would buy out of FOMO. Now I’m just learning to live with it.

If I admire the promoter, I apply a multiplier of 1.5x. This is not to say that I don’t admire Uday Reddy of Tanla or Arun Jain of Polaris - I just havent tracked them as I have a Shuja Mirza or a Vaidyanathan.

If the company is likely to achieve or sustain RoCE% > 30% over the next 3 years, I apply another 1.5x multiplier. I feel that high RoCE companies offer much greater upside on valuations than lower RoCE companies which often have to dilute equity or pile debt to take advantage of their growth runway.

Therefore, my maximum exposure to a company can be - 1%+2%+2%=5% x1.5 x 1.5=11.25%

Hi @vivek423 I noticed KDDL in your portfolio and having good amount of sizing.

I was tracking KDDL but dropped when I was not able to come on any conclusion.

Can you share any recent views and thesis of yours?

Thanks!

KDDL is in my opinion one of the best placed retailers in India. In my experience, once Networth crosses 5 cr and one has purchased the first home and car, the next desirable purchase becomes a luxury watch. I believe India should see exponential boom in luxury watch purchases in next 10 years.

KDDL has built out their business beautifully. They have an excellent portfolio of brands - many of which are exclusive to them. They have especially done a great job of including several mid tier niche brands like Nomos, Junghans, Zeppelin and many others. Their website is a pleasure to browse. Ive spent several hours curating my dream watch list on their website.

Their business model is built on multiple mutually reinforcing pillars -

Offline stores - this creates the trust and brand pull

Online presence - this enables users to browse the entire inventory and make their choice before going to the store

Used watch purchase and sale - one of the biggest issues in India is the difficulty in resale of luxury watches. If i know that a 3 lakh watch can be resold for 2 lakhs after 4 years then my cost of ownership goes from 3 lakhs to 25,000 per annum. Their used watch website secondmovement.com has several high quality watches listed including several Rolexes and even an Audemars Piguet. One can sell their watch back to ethos at a reasonable price.

EBOs - Ethos has the rights to build and operate EBOs for several brands including Omega. These are highly profitable stores with much highers RoCEs that the MBOs.

Extension to other categories - Ethos has taken the India master franchisee of Rimowa - a luxury luggage retailer owned by LVMH. In the long run, Ethos can become an omnichannel luxury retail platform for multiple other categories like fine jewellery

In summary, they are driving up the availability of brands in India while driving down the cost of ownership. The moats they have built are enormous. Tomorrow if Patek or AP wants to enter India in a big way, there is only one credible choice of partner available to them.

The best part is that they have no competitor. There are a few watch retailers but they are localized with limited inventory and few brands. They largely sell to their legacy clientele with whom they have established relationships. The sales teams at these stores do not have the sophistication of an Ethos sales person.

Thanks @vivek423 really appreciate your views.

Product vise I was comfortable with reviews but the concern for me was few factors like:

continuous dilution in capital and there is no sign of borrowings getting low

Inventory and capital days are at peak

retailers holding 24% (can be ignored but do play significant role)

lastly the sales growth of past 3 and 5 years ( covid can be one of the reason but I still don’t see people coming out and focusing on luxury items in current situation of inflation)

Lets see how it plays out but I do have keep this in my watchlist.

Dislclaimer: No buy/sell recommendation