They came up further with result of detailed tests & happily informed that they are safe. They have confirmed same to EU authorities as well. I am missing similar aggression from other producers.

@sarthakkumar19_ @mrai74

Don’t think it is a major risk for Auro from 3 aspects:

- They do not supply to US but to few countries in Europe (not sure how much of that is regulated by EMA).

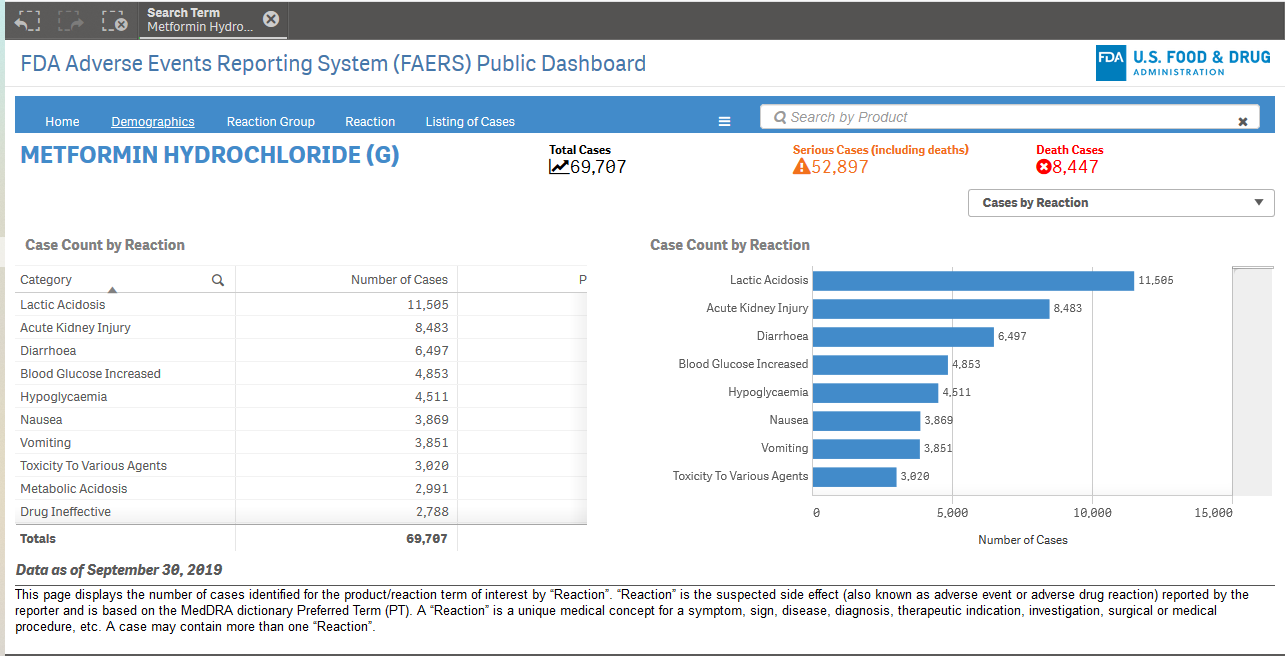

- Lindy Effect of Metformin which has been in use for more than 50 years. Based on the below snapshot from US FDA AERS, cancer does not come in the top hits.

Apart from the above there are other angles which we need to consider.

Above podcast is an useful reference to understand the NDMA issue and the difference between Sartans and Ranitidine.

Sartans: Reaction between the solvent (DMF - Dimethyl Formamide) and Nitroso intermediate compounds to form NDMA. Presence of the solvent itself. Change in mfg process.

Ranitidine: Inherently unstable molecule. Potential interaction with DDAH1 enzyme which cleaves off the DMA that then reacts with the nitrates circulating in the body. Implies the issue is not specific to generics but with the branded drug as well.

- Valisure essentially found that biological link

- They identified an enzyme, DDAH1, which grabs on to a molecule and it breaks off this DMA group

- Once you break off a DMA group, it’s very easy to form the NDMA in the body with nitrate that circles in your body

- Valisure looked at this enzyme and did computational modeling to find that it seems that the ranitidine molecule fits extremely snugly in this enzyme

- and that at least gives a potential biological mechanism for forming millions of nanograms throughout the body, even outside of the stomach

Where does Metformin come in? For me intuitively it is more likely that it falls in the bucket of sartans rather than ranitidine.

So far have not come across any research where there is an interaction between DDAH1 and Metformin (since Metformin is made from DMA HCL and DCDA)

What about Valisure? It is fair to assume that it is in their interest to highlight these issues and differentiate themselves from other pharmacies especially in a high burden healthcare market like US. So far they deserve the benefit of doubt that they are genuine and do not have any ulterior motives. Would like to see them highlighting issues from branded drugs of the innovators as well and not just generics.

Big Pharma trying to replace Metformin with SGLT2 inhibitors & GLP-1 RAs as first-line treatment for Type 2 Diabetes: https://www.mdedge.com/internalmedicine/article/203896/cardiology/costs-and-benefits-sglt2-inhibitors-glp-1-ras

Creating a scare around Metformin will nudge patients to consider alternatives.

From EU: EMA update on metformin diabetes medicines | European Medicines Agency

The levels of NDMA in the affected non-EU metformin medicines are very low and appear to be within or even below the range that people can be exposed to from other sources, including certain foods and water.

From UK MHRA: Metformin diabetes medicines – MHRA Update - GOV.UK

Patients in the UK are advised to continue taking their metformin medicines as usual. The risks from not having adequate diabetes treatment far outweigh any possible effects of the low levels of NDMA seen in metformin medicines outside the UK.

Given the above advisory and the ongoing clinical research of the anti-cancer benefits of metformin through multiple mechanism of action, I personally think the anti-cancer effects would override any potential damage caused by presence of NDMA which are present in low levels.

5 Likes

PF update

| Buy Average | Allocation | |

|---|---|---|

| Banswara Syntex | 66 | 20% |

| Balaji Amines | 245 | 17% |

| RACL Geartech | 68 | 16% |

| Gokaldas Exports | 79 | 11% |

| Auro Labs | 52 | 10% |

| Stock X | 25 | 10% |

| NOCIL | 108 | 5% |

| Tail | - | 11% |

Sold off Shivalik Bimetal from the tail portion for now (reallocated to RACL Geartech). Tejas continues to be part of the tail portion.

Added Marico to the tail.

Pretty significant deviation given that it is not overlooked and a large cap.

Rationale:

- Natural hedge against the black swan of a ban on high omega 6/linoleic acid based vegetable oils through their Coco soul product range (Cold pressed virgin coconut oils and spreads).

- Though contribution is pretty low currently, they are better placed given the competition is mainly from unlisted space and negligible from their listed peers/MNCs.

- Alignment with my LCHF/Keto bias.

- Consistent culture of tinkering and experimentation.

Peers:

Price is on the cheaper side (obviously with discounts)

PF up by 20%. Considering the majority of the returns are from the top 3, I would be happy even if this reduces to 15% by the end of year.

Been lucky so far with the concentration strategy. Goal is to trim excess allocations/add fresh capital to NOCIL and Tail portion.

Happy New Year to all and a prosperous & healthy decade ahead!

Health is Wealth after all.

12 Likes

Hello Vishnu,

How should I go about understanding the impact of corona virus on Auro Labs. My guess is that shortage of APIs might work in their favour. Looking for your guidance on how to properly assess the impact.

Thanks

Hello Vishnu,

Hope you are doing well. Saw you on the forum after a gap so just wanted to check on your health.

Wanted to know your view on latest results of Auro labs and Gokaldas. Results seemed average and but the stocks have corrected substantially. Maybe it’s just the general market uncertainty wrt corona virus. Also, any update on your portfolio.

Thanks

Hi Sarthak,

There may not be a major impact on Auro Labs since majority of Metformin API is being manufactured in India.

However the key intermediate DCDA (Dicyandiamide) is primarily manufactured in China and imported to India.

My understanding of the MFG process: Since DCDA is manufactured through the carbide route (NCN), it is energy intensive as well as highly polluting. Hence China has dominated this compound.

Only other major manufactured outside China is AlzChem which is Germany based with 1 Million TPA capacity.

I suspect there would be a RM impact but not sure how much would be the quantum of it.

Below is snippet from Alzchem site:

In 1950, SKW Trostberg, as the forerunner to AlzChem, started production of Dicyandimide (DCD). The production plant has been in continuous operation ever since, and constantly improved so that in the current day it respresents one of the most efficient, technically advanced and pollution-free DCD processes in the world. Furthermore, with a capacity of 20,000 to per annum it still represents one of the largest DCD facilities worldwide, and one of the only remaining DCD facilities located outside of China. In 2016 we are very proud to be able to announce that our total DCD manufacturing quantity will exceed the 1,000,000 to mark.

The big advantage of DCD is that it is extremely reactive but nevertheless non-hazardous, and because of this it is used in a wide variety of applications. The largest application field is as a synthetic component for the production of active pharmaceutical ingredients (API’s), inter alia for the manufacture of the type II anti-diabetes drug Metformin. Another major application field is the hot-curing of epoxy resins for industrial applications, and in recent years Dicyandiamide has a growing importance as a nitrogen stabiliser for agicultural fertilisers. Internally Alzchem also use DCD as a raw material in forward-integrated intermediate products for the production of a diverse range of guanadine salts, guanamines and DCD based condensation products; used in air bags, water treatment, flame retardants, textiles, leather tanning and finishing, and pulp and paper finishing auxiliaries.

Source: Dicyandiamide | Alzchem Group

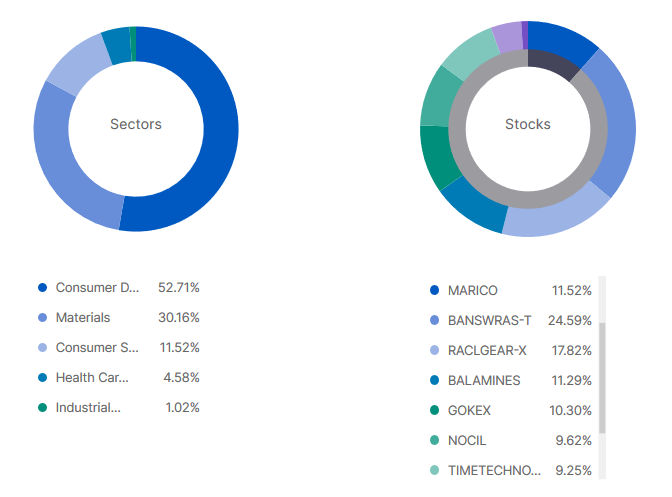

Coming to the Portfolio Update:

Above portfolio is MINUS Stock-X (which still has 9% allocation in overall pf)

Auro Labs is at 4% and hence now part of the Tail.

Reduced my holdings after the price fall.

New Position: Time Technoplast

Rationale for Investing:

- Technocrat Management: https://www.youtube.com/watch?v=ACb_JASS4OY

- Global Leader and among top 3 players in some of the Industrial Packaging segments.

- Proxy to Chemical logistics: No presence in China or South Korea. However the leader in ASEAN countries such as Thailand, Malaysia and Vietnam which are expected to get benefit of MNC’s diversifying away from China.

- Competing with Supreme Industries in Composite cylinders and MOX Films

- Prudent use of debt. Mgmt has committed to not overextend beyond 2x Debt to EBITDA

- RM tailwinds with PE oversupply and Reduction in PP and HDPE prices.

- Lot of value added products in pipeline/R&D: Composite Leaf springs, CNG tanks, Polyurethane based cylinders and many more.

[https://www.bseindia.com/xml-data/corpfiling/AttachLive/e7c47922-a57f-4441-a83a-e268b51e1bd9.pdf](Feb 20 Analyst Meet Presentation)

Auro Labs:

Personally the results were not that bad. Not sure why the fall was drastic. Maybe coronavirus related due to DCDA shortage? or Additional delays in capex approval? Either ways from an opportunity cost felt it is better to move it to Marico and Nocil instead.

Gokaldas:

Biggest positive is the revenue growth at 20% plus YoY. There was the overhang of MEIS disclosure before the results which made the stock go below the book value (INR 59). Not too much bothered about the price levels. Would wait for the annual results and see if there is an incremental improvement in the RoCE and working capital cycle.

5 Likes