What is your asset allocation like. Do you invest in equity other than this portfolio.

Thanks

I do have some investments in rural plots.

Would make it 70:30 mix between real estate and equities.

Only have 1 pf which is the above one.

I do not invest in Mutual funds - Debt or Equity.

2 Likes

Since you gave 20% allocation to Balaji Amines, please go through this twitter link;

1 Like

Yup. And i have retweeted it as well. Though amt is trivial it adds to the perception of poor corp governance due to hotel diversification.

FY18 and FY19 AR and not before that.

Never focused on the cash flow statement in the AR since I depended on the values from screener. A point for the future to re-confirm numbers with the actual stated figures in the AR.

2 Likes

Hello Vishnu,

Your average buy price for auro, Tejas, and Balaji has come down substantially. Does that mean you invested a lump sum recently. If yes, to me this reinforces the point that only when one has studied a company deeply can one have the conviction to buy more as price goes down.

Thanks

No lump sum investments.

Some of the factors which led to drastic reduction in Average Buy Price:

- Invested the 18% cash allocation from July and invested in each of the stocks.

- Also did some tax loss harvesting to carry forward short term capital losses.

- Reallocation from tail portion to the core stocks.

Yes. Deep conviction is required to at least hold on, if not buy during draw-downs. However to be honest, I would rather be in a position of averaging upwards.

Caveat: Conviction should be bounded by humility about the possibility of going wrong due to non-consideration of some factor in the investment rationale. On the other hand if conviction borders on arrogance of having factored in all the info, then Mr. Market is bound to humiliate me.

5 Likes

Hello Vishnu,

Do companies generally publish transcript of AGM. I could only come across for Tejas Networks.

Would that count as a positive for Tejas Networks considering the farce that most AGMs turn out to be.

Thanks

1 Like

There was a SEBI circular for top 100 companies to webcast the AGM proceedings.

Though it is a positive, in the overall scheme of things I would not give it much weightage.

2 Likes

Hello Vishnu,

I have a question regarding Auro Labs. In the latest annual report, Auro Labs proposed to increase remuneration of Mr. Sharat Deorah and Mr. Siddhartha Deorah to Rs 1.68 Cr. each. This totals to 3.36 Cr. and is more than 69% of TTM net profit of 4.86 Cr. from screener. Isn’t that excessive. I have seen similar proposals in quite a few small caps recently (eg RACL geartech, Mangalam Organics). How do I interpret this, reminds me of TBZ (one of my worst investments). I agree that management deserves credit if a company is doing well, but wouldn’t you prefer them to get benefited through increase in value of their holding rather than salary increases. Please guide me.

Thanks

1 Like

What they have done is they have proposed the max ceiling of their remuneration for the next 3 years. It does not mean that the promoter will increase their remuneration from current 60 lac p.a. to 1.68 crore p.a. from next year itself.

I have tabulated the Ceiling revisions from the various AR and captured them below.

This needs to be considered with the below snapshot I had put up in Auro Labs thread. U can see that the promoters did not take any salary from FY07 to FY13 though they did take loans from FY07 to FY10.

Based on the above data, here are my observations:

- Even if we consider the Promoter Salary/PAT ratio would be around 25% going forward, then the PAT has to 13.44 cr by FY22 (3x from here) if they have to justify taking entire 3.36 cr remuneration by then. (Possibly a proxy to mgmt’s confidence on making that number)

- Considering they were taking negligible salary prior to FY14, one may think that they wanted to start showing white money sources, assuming that they previously had black money sources (a big assumption with no justification as of now). Additionally they have started taking secured loans from Banks and reducing the unsecured loans from Related parties. Also, they started paying taxes in the last 2 FY which was non-existent prior to that.

- I personally am ok with the remuneration considering the significant increase in quality of the numbers across multiple parameters in Balance Sheet and cash flow statements. I would reconsider my stance if there is any deviation in the current trend.

- Assuming they continue to deliver the numbers and PAT growth is sustainable, then I expect them to increase their salary somewhere between 90 to 96 lacs p.a. in FY20

- Playing devil’s advocate, this linear increase in promoter’s salary YoY may sound too good to be true. It could either mean over-confidence or some sort of manipulation of the numbers.

- On the other hand it can also be considered as normalization of the remuneration relative to peers ( for ex: Smruthi Organics where they have revised the actual salary - not ceiling - from 84 lacs p.a. to 1.44 cr. p.a. when PAT is around 7 cr which is not far from Auro Labs)

Either ways, I continue to watch their performances cautiously to observe any anomalies that negates the investment rationale.

On a side note, RACL Geartech is part of my tail portion of the pf and am still researching on it. Maybe u can do similar exercise as above for RACL to see if it is truly anomalous.

4 Likes

Hello Vishnu,

Just wanted to check if there is any update to your portfolio. Also, your thoughts on Tejas result. I heard the concall and it seems international business will take longer to make meaningful contribution.

Thanks

Been busy with job/location change.

Pf update: reduced shivalik bimetal, nocil and tejas to the tail portion. Added new position in Racl Geartech (15%) and Gokaldas exports (10%).

Overall pf up by 12% due to balaji, banswara and racl geartech.

Re: tejas. I too am bit disappointed with the lower contribution from international segment. May need to wait for q4 before taking further decision.

2 Likes

I’d love to learn from you how to ruthlessly get rid of a stock once you change your mind. I keep waiting for a better exit price and keep cluttering my portfolio and thinking with stocks I have given up on otherwise. Any suggestions on how to develop the ability to let go of a stock once I realise that I was wrong or that things have changed.

Thanks

I am still learning. Might seem ruthless but it is still sub optimal as i am working with constraints of limited additional cash which might be a positive as well since it forces me to really think hard about opportunity costs.

The best thing u can do is it internalize the vp capital allocation thread and force rank ur ideas on conviction and undervaluation matrix. (Expected return)

Every change to the pf needs to be evaluated against the above framework.

That is just my 2 cents. U may be better off seeking advice from seniors who have been through multiple market cycles and faced the scenarios u have highlighted.

4 Likes

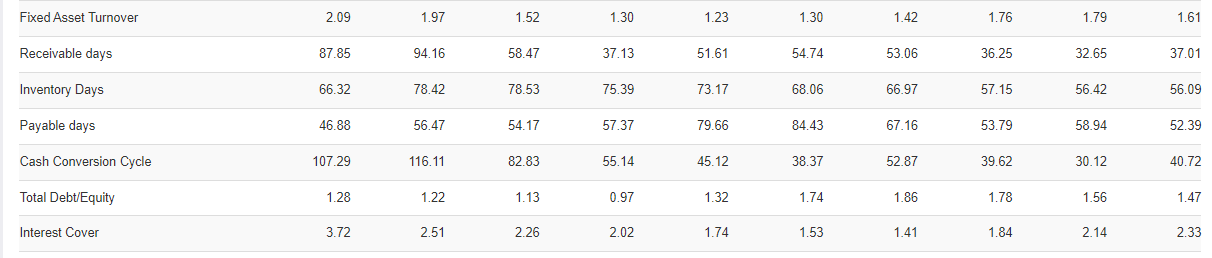

Hi Vishnu, Can you please tell the rationale for investing in RACL Geartech, The working capital seems to really worsen, the receivable days has increased in the last few years and payable days has reduced and the effect of that is shown in the increased short term borrowings and Long term borrowing also increasing.

Good thing is sales and margins are growing.

Pls provide your views on the business

1 Like

For me the increase in debtor days can be explained by the fact that the proportion of exports as a %age of overall revenue has steadily increased. Moreover as the relationship with new customers matures i expect the debtor days to come down.

Lt borrowings are for the capex in progress.

Rationale is it being a proxy for kubota market share gain in the long term and supported by a resurgent luxury 2w segment.

I have put up a post with my findings on racl thread.

4 Likes

Hi Vishnu, Can you please tell the rationale for investing in Gokaldas Exports please.

Got interested after coming across the below slide deck from alpha ideas 2020 meet by Pathik Gandotra.

https://drive.google.com/file/d/1Ro4WCgO95BTDkjEIeoh8Mg3et7jWN221/view?usp=drivesdk

Despite the aphorism that turnarounds seldom turnaround, and accentuated further by the fact that there were 2 failed attempts in gokaldas I am taking a bet that 3rd time is a charm.

Listening to the concalls and mgmt interviews there is evidence of them following through. Business wise it is another proxy play on fast fashion (zara, h&m, gap) but from the cotton side.

7 Likes

I understand that few reactions in various companies producing Metformin were seen by known guys in last 2-3 days. I saw a proactive clarification from other company (Granules) stating that their preliminary tests have confirmed against news flowing and their product is safe although they continue to do detailed investigation. I know that no company will accept it till FDA / EU health authorities take any action based on their internal findings. Let us see how it unfolds & impact will be keenly monitored by Indian pharma industries.