![]() Vishnu prakash R Punglia LTD(VPRPL)-“Steering India’s Water Management Future”

Vishnu prakash R Punglia LTD(VPRPL)-“Steering India’s Water Management Future” ![]()

INTRODUCTION

Established in the year 1986, Vishnu Prakash R Pungalia Limited (VPRPL) is an integrated engineering, procurement and construction (“EPC”) company with experience in design and construction of infrastructure projects. VPRPL is engaged in the business of designing and constructing infrastructure projects for the Central and State Governments, autonomous bodies, and private bodies

- Market Cap : ₹2,945 Cr

- Current Price : ₹ 236

- Stock P/E : 24.1

- ROCE : 24.7 %

- ROE : 23.6 %

- Intrinsic Value : ₹ 283

- Promoter holding : 67.8 %

- Debt to equity : 0.55

Overview

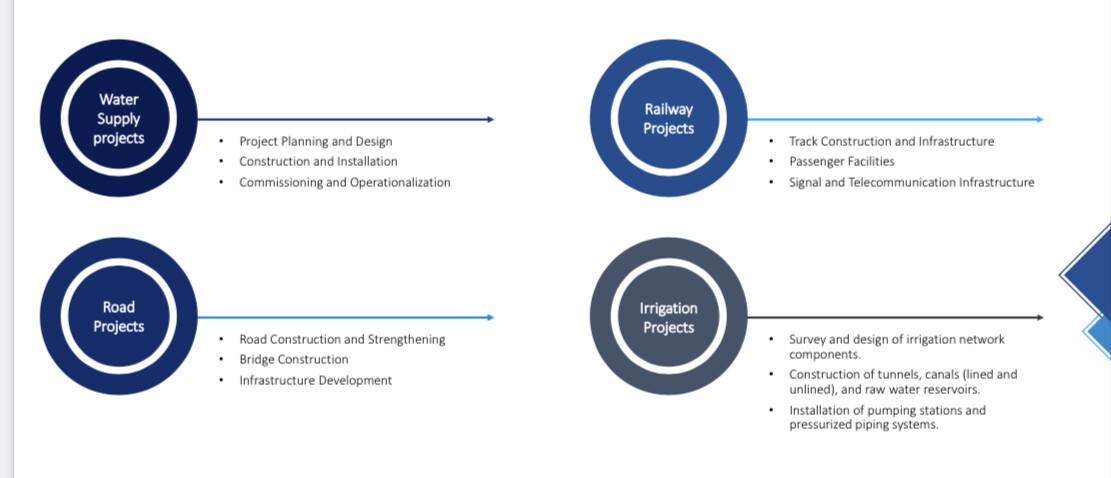

1. BUSINESS OPERATIONS

Key Operations Areas

![]() Water Supply Project: Revenue Share ~85%

Water Supply Project: Revenue Share ~85%

![]() Railway Projects: Revenue Share ~7%

Railway Projects: Revenue Share ~7%

![]() Road Projects: Revenue Share ~6%

Road Projects: Revenue Share ~6%

![]() Irrigation Network: Revenue Share ~1%

Irrigation Network: Revenue Share ~1%

![]() Other Projects: Revenue Share ~1%

Other Projects: Revenue Share ~1%

i) Water Supply Projects (WSP) -

The company has 36 years experience in executing WSPs comprising of construction and development of pipelines, water tanks, reservoirs, tunnels, overhead tanks, water treatment plants, and irrigation projects. It has executed 75+ WSPs and is one of the prominent cos in Rajasthan in water supply projects.

ii) Railway Projects -

earthwork, construction of bridges and supply of materials and track linking, railway station platforms, administrative buildings, rail over-bridges, and station quarters.

iii) Road Projects -

construction of highways, bridges, culverts, flyovers, and subways; projects related to irrigation like dams, canals, tunnels, pressured pipe systems, etc.

iv) Irrigation Network Projects -

sewerage, industrial effluent treatment plants on an EPC basis.

2.SECTOR DETAILS

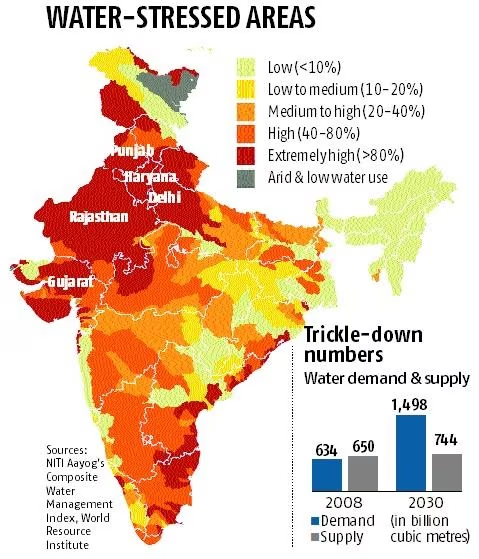

The water management sector holds critical importance in India’s path to sustainable development. As urbanization and industrialization continue to surge, the need for effective water management solutions has reached unprecedented levels. For ensuring the continued growth and prosperity of the nation."

India is facing a water scarcity problem, and ensuring efficient water usage and supply will be the government’s focus moving forward. The company’s stronghold in key states (chart 1) will prove beneficial

Sources: NITI Aayog, Mint

3. GOVERNMENT BACKED

- The Indian government has launched several initiatives like the Jal Jeevan Mission and AMRUT to ensure water supply to every household

- The Jal Shakti Ministry allocated Rs 98,418 crore in the interim budget for 2024-25 with its flagship Jal Jeevan Mission

- Jal Jeevan Yojana: The govt.'s mission to supply tap water to every rural home in India.

Rajasthan still has a long way to go, and the company has strong focus here

Stats: ~25% of households across India still to get tap water, and thus a significant opportunity

4. PROMOTER DRIVEN

*The company is promoted by the Pungalia family(68.7%) who are in the EPC business for last 4 decades. The leadership team is driven by Mr. Vishnu Prakash Punglia, Mr. Manohar Lal Punglia, Mr. Sanjay Kumar Punglia, Mr. Kamal Kishor Pungalia and Mr. Ajay Pungalia.

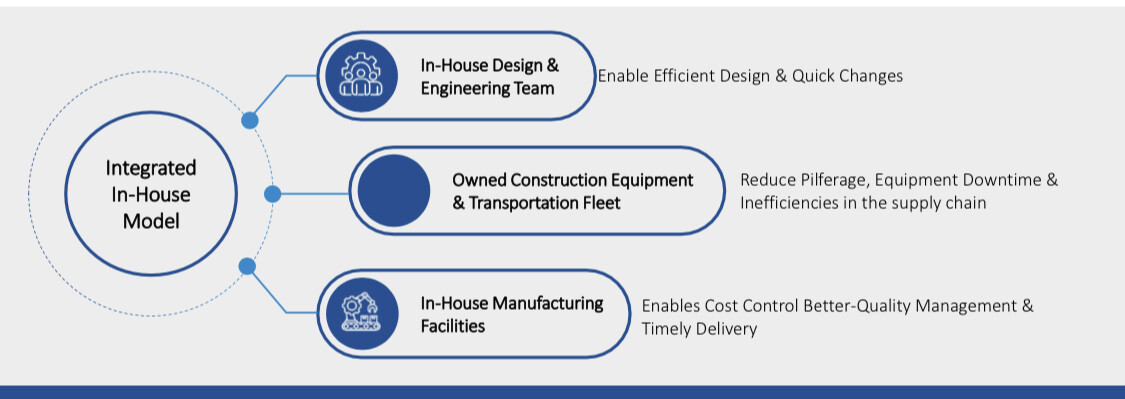

5.BUSINESS MODEL

• The company has an integrated business model with in-house execution team and a fleet of more than 500+ construction equipments which helps in reducing its dependence on third-party for key materials and services required for project execution.

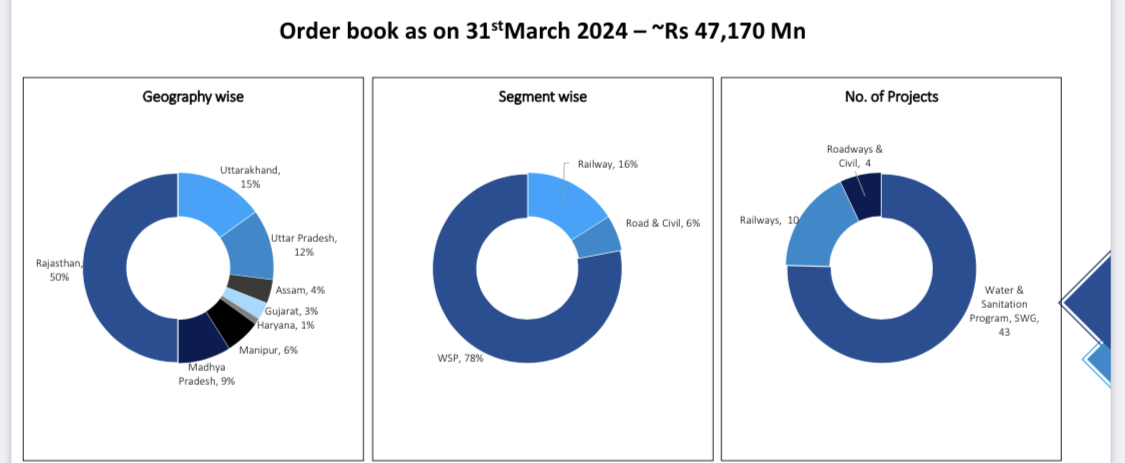

6.ORDER BOOK:SCALABLE BUSINESS

Order book as of March 31, 2024, stands at ₹4,717 crores to be executed over the next 24-36 months.

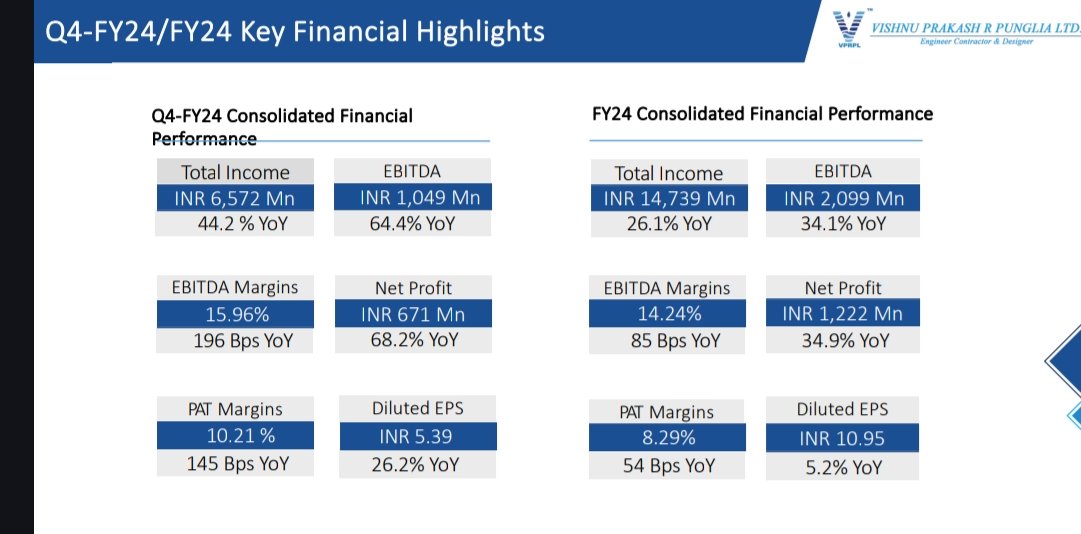

7.FINANCIAL PERFORMANCE FY24:

Orderbook at 3x of FY24 revenue

Q4FY24:

Rev⏫44% at 657cr

EBITDA ![]() 64% at 205cr

64% at 205cr

OPM at 15.96%![]() 196bps

196bps

PAT⏫68% at 67cr

FY24:

Rev⏫26% at 1473cr

EBITDA ![]() 34% at 210cr

34% at 210cr

OPM at 14.24%

PAT ![]() 35% at 122cr

35% at 122cr

GROWTH DRIVERS ![]()

-

Company aims to maintain order book turnover ratio around 3 times.

-

Strong growth in revenues driven by successful execution of ongoing projects across segments.

-

Margin expansion due to cost control, operational efficiency, and timely project execution.

-

Robust bid pipeline with hopes of new opportunities materializing in the coming months.

-

EPC only contracts Focus only on EPC projects, with or without O&M. No HAM or BOT projects.

-

Diversify into other segments while not losing focus on core business

-

Make investments in latest equipments and Focus on high value contracts

-

Further strengthen foothold in the state of Rajasthan. Selective Geographical diversification

POSITIVES

-

Company has competencies to bid for large value projects and successfully secured projects in Uttarakhand, Uttar Pradesh, and Madhya Pradesh.

Company has competencies to bid for large value projects and successfully secured projects in Uttarakhand, Uttar Pradesh, and Madhya Pradesh. -

Active participation in the Jal Jeevan Mission and AMRUT 2.0 scheme projects.

-

No immediate need for additional Capex as current equipment is adequate for upcoming projects.

-

VPRPL’s strong market position and expertise in water management make them a preferred partner for government projects. Their competitive edge lies in their execution capabilities

-

Strong pipeline of government tenders and projects in the water supply, roads and railways segments with focus on infrastructure development by central and state governments provides a good industry tailwinds.

RISKS

-

Working capital requirements are on the higher side, common in infrastructure companies.

Working capital requirements are on the higher side, common in infrastructure companies. -

Rajasthan is the highest revenue contributor, not unusual for smaller regional infrastructure firms.

-

85% revenues solely from water supply projects.

-

Order book fluctuation possible; dealing with govt (99%) carries risks of project delays and potential scams.

-

No aggressive debt funding planned, with a focus on maintaining debt equity ratio under one.

Screener link:

(Vishnu Prakash R Punglia Ltd share price | About Vishnu Prakash R | Key Insights - Screener)

Website link: https://www.vprp.co.in/

![]() Disclaimer: Invested and biased

Disclaimer: Invested and biased