Attended Q2FY25 Concall:

Some key points:

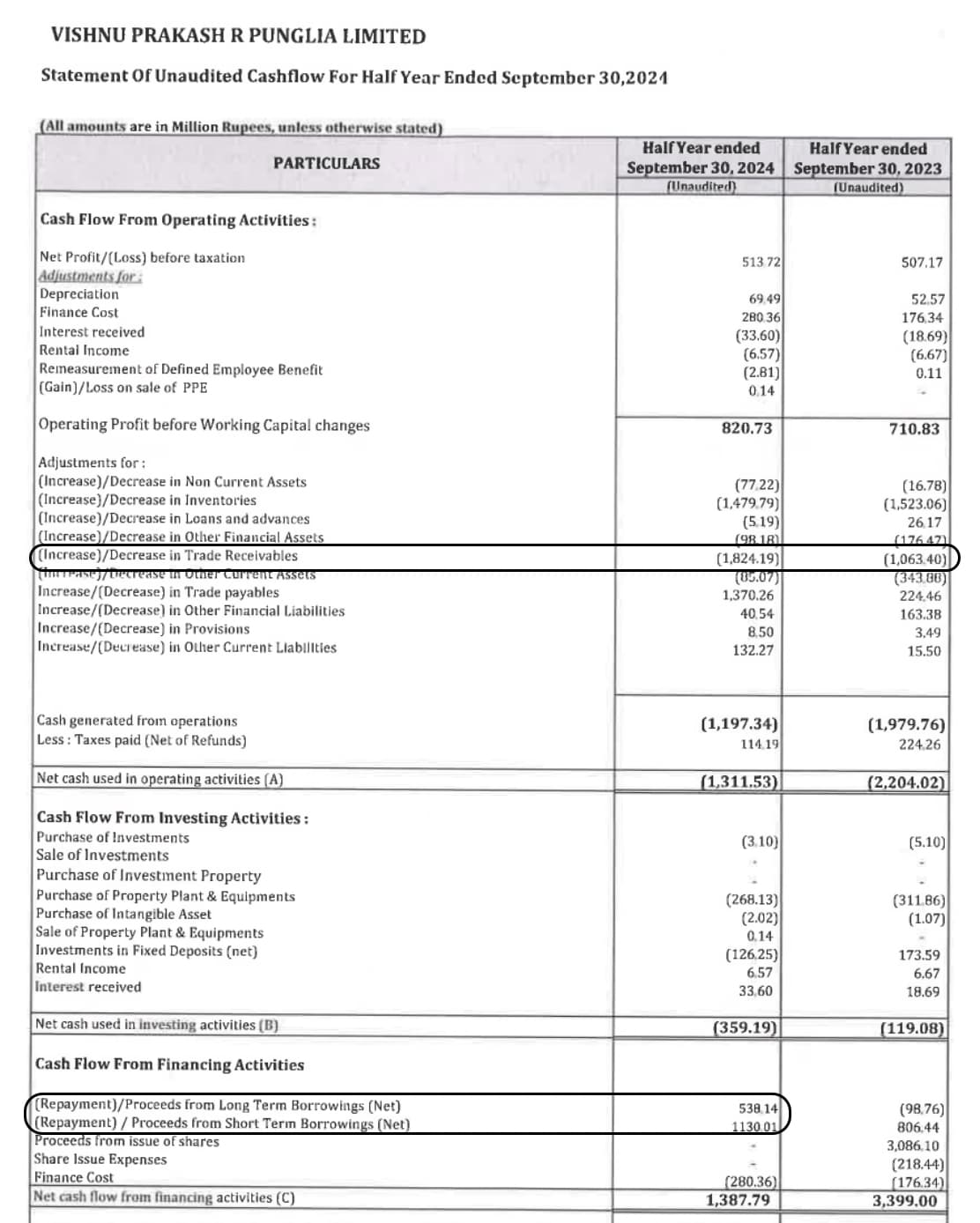

- Trade receivables will take about 3-4 quarters to come down. Due to which debt levels have went up.

- Debt is still in comfortable position. More debt might be taken until the payments are cleared from government.

- Revenue Growth Guidance of 10-15% on conservative basis.

- Lots of questions on PAT growth but due to increased debt, it might be restricted.

- All orders are from Government entities, no orders from private companies.

- This year due to center and state election, payments are delayed.

- No QIP plans at the moment.

- No affect to them due to Raw material price changes.

Vishnu Prakash R Punglia just won order from Office of the DYCE/C/AII, Ajmer division of North Western Railway

Order value:102.9cr![]()

Segment: Railway

1 Like

Are there any concerns in VPRPL on multiple family members (am given to understand more than 12 of them) being given positions in the company leading to perceived inefficiencies and overall opacity in the functioning?

Can anyone shed light on this particular aspect?

1 Like

VPRPL | Work Order

Project involves the EPC, commissioning, and operation of a 30 MLD capacity sewage treatment plant in Jaipur, using Sequential Batch Reactor (SBR) Technology.

Total project value: ₹513.99 million.

This orders would be not valuable for company if they dont improve their negative operating cashflow. Debtor and working capital days are also increasing

If one will carefully observe company’s income statement company is doing “bill and hold aggrement” which means they have to showcase their last quarter glommy so they tell their customer to purchase whatever material is there even if customer doesnt need it and tell the customer to pay the payment whenever they want and this will eventually increase the debtor days and disturb the operating cashflow cycle and this has been im observing from last few years in many companies

So be careful while investing in this type of companies

4 Likes

40a4ddf7-c4ca-4283-848c-d5a923739407.pdf (2.6 MB)

Results are out as expected sales and profits halved

1 Like

a. Q3 was weak, but Q4 was an absolute disaster.

b. I expect them to “revise guidance” downward.

c. They made big promises in the Q2 concall—no way they’ll meet those targets!

Can’t trust this management anymore!

1 Like

Agree, management has given reasons in the past attributable to monsoons, elections etc.

Not sure what reason will it be this time. Even though the order book is strong, execution is ordinary.

2 Likes