Jt. MD Siddarth is focused focused on international marketing & strategic initiatives of the company

Exports

The company currently exports to 52 countries

The company is concentrating on export markets

Products

The company is planning to add following products - chrome plating salts, chrome metal to be used in aircraft

The company has also created sulfate product which is used in detergents etc., this is dedicated product for Colgate Palmolive

Barium subsidiary

106Cr sales, 11cr PAT

The company expects to earn PAT of 15Cr in FY20

Barium products find their end usage in construction (Bricks etc.), Caustic Soda, water purification.

Bankers refused to issue NOC for merger of Barium subsidy due to -ve net worth.

RM

The total chrome ore consumption of the company is ~ 1L tonnes

The company has entered into contracts to get chrome ores on long term basis from South African players

60-70% of RM will be sourced from long term contract & rest will be sourced from spot market

The OPM margins of the company came down from 17-18% to 13%, primarily due to chrome ore price rally

The products are produced only in 5-6 countries & sold in 80 countries. The logistics cost is an important aspect due to this & the company is negotiating logistic cost as well for RM

Currency

Since the company is net exporter, it is not hedging everything

Loans to related parties

Shareholders questioned the resolution to give out loans to related parties

The company claimed that it is using R&D facility of Vishnu Life Sciences on lease

For Infra company, the company claimed that there is no business activity as of now & the company has not taken on any guarantees

Cumulative Redeemable Preference Shares

The company has reduced the rate from 7% to 1% till 2033

The bankers were treating this as debt instead of equity

Anti-Dumping Duty (on Sodium Dichromate ?)

The company was not successful in getting ADD because it was fighting the lone battle

Competition

It is not possible to link the output product prices with chrome ore prices due to competition. The end product prices will be market driven.

Sisecam Chemicals, Turkey is one of the big competitors & it had some advantage due to Turkish currency

There is another competitor in Kazakasthan as well

Lanxess, Argentinian competitor went out of business & company was able to capture market share in exports in FY18

Elementis is the competitor based out of US

For Chinese players, GST for chrome products is not refundable & hence they are not present in export markets. China is self sufficient in chrome chemicals.

The company claimed that they are operationally strongest but financially weakest

End Industries

Currently company gets 40% revenue from natural leather industry, 20% from pigments, 20% from electroplating & rest

The company is focusing on electroplating market & expects to take the share to 30% over medium term

Capex & Capacity

The company is not planning for any capex for next 2 years except for maintenance capex which is 2% of topline

Current capacity is 70kT & utilization is 50kT

Debt

The company is planning to bring down the cost of debt from 12% to 10% in FY20

Entry Barriers

The end industries are growing at 2-3% which discourages the newer players from entering

Huge capex requirement is another entry barrier - e.g. it costed company 100mn$ to put up a plant of 70kT. Lanxess got 135mn$ for their plant.

The company aspires to reach 20% EBITDA margin by FY21

Disc - token investment in company to attend AGM, not a buy or sell recommendation, not a SEBI registered analyst

Vishnu are doing better as compared to their precarious situation earlier.

They are doing well with their Dichromate production and they have also resolved their Chrome Green production issues. After several years of closure, they are starting their Bhilai (East Central India) plant.

Concerning Barium Carbonate which is in our area of activity, some more detailed input for your understanding:

Operations: Availability of Baryte no longer an issue. They can produce upto 3000 tons per month of product.

India

Domestic market stagnant at 40,000 tons per year

Caustic soda market experienced strong de-growth for Barium Carbonate. (Current requirement 15,000 tons per year in India)

Some producers switched to membrane process, others have improved the input salt quality so the requirement for BaCO3 has come down to 30% of past levels.

Vishnu allows small scale to fight for the caustic soda market.

Vishnu focus on Ceramic market in India, which is growing.

Global:

They are focused on the glass and ceramics market for growth in India and globally.

They are making good inroad to the export markets, they undercut the Chinese too and have very good quality, so they can make meaningful penetration.

Management

Mr Murthy is a technocrat to the core.

His son who has joined him is an engineer by training, but currently focused on international market development.

High debt in Balance Sheet is a real concerning factor. Does anyone has any insight on why such huge borrowing? Is it for any capex / production we expansion? I can’t find any vision from management about when to reduce the debt

excellent results. The company is through with much of its expansion and debottlenecking. It has also achieved good results on the export front despite high freight rates

Really surprised at how inactive this thread is.Company has been doing very well recently and EBITDA margins have expanded all the way to 15% in Q3.Vishnu is one of the rare chemical companies that has been able to fully pass on logistic and freight costs.

The 50% higher Barium capacity will come online in Q4 and the backward integration plant has already started.In it’s Q2 call management had guided for 500 bps margin expansion post backward integration and even higher expansion,given the prevailing Soda ash prices.It is also worth noting that volumes in Q3 were hit due to heavy rainfall in southern states.Otherwise revenues would’ve been better.

Even assuming a similar 300 cr run rate in Q4,company will end the year with over a 30% growth in revenues.In their call company guided for a 20% volume growth in both chromium and barium segments for few years to come.They have plans to expand Chromium capacity to 100k from the current 70k over time.With additional Barium capacity one should see good growth in Fy23 alongwith decent margin expansion.Company has expanded it’s product basket a lot in recent years and is able to toggle well b/w better performing end user industries.

Post Q3 stock has been on a tear in an overall weak market.After some cool-off,I feel this still offers good upside potential on earnings growth alone.

Good points. Surprisingly such a big wealth creating cos thread has been totally in active.

Co seems to be walking the talk as is visible from recent results & indication given in Q2 concall.

Is the company into Commodity business with no pricing power or sp chemical with pricing power ? any competition in India & who are in abroad? Whats the moat co enjoys?

I think their biggest moat will be backward integration plant which will increase their EBITDA margins by 4 to 5%. Also this will give them pricing power.

They have 4 international competitors in chromium segment.

Vishnu Chem reported a strong set of numbers in Q4.

Margins expanded even on a qoq basis inspite of various headwinds faced by chemical cos. & many other industries.Concall highlights:

→ Chromium util at 90%,Barium at 85%. Chromium capacity to rise to 80k in Fy23 via debottlenecking.Barium now at 60k,mgt expects 40% kind of volume growth in Barium segment.

→ 120 cr. capex in FY23.90 cr of this will be towards a new import substitution opportunity: Barium Sulphate.Product is used as filler in Paint industry.India mkt size is 25 k MT and this product is completely imported.Global mkt size=130-40 k MT. Import contribution from China=70%,rest 30% is from Italy.Company sees a strong opp here since logistic costs are creating issues in imports.Expect to be as high quality as Italian imports.This capacity will be over & above the 60k barium capacity and will start contributing to topline from Q1FY24.

→ Russia was strong in Chromium segment.80k MT capacity is offline due to sanctions,etc.This has opened up a larger market for Vishnu.Growth is coming from both existing & new clients.

→ Q4 Barium segment EBITDA margins were hit since production in Q3 was delayed.So company had to honour Q3 prices in Q4 as well.From April this has normalized and expect 15-20% EBITDA here in FY23(vs. ~10% in Q4)

→ Backward integration plant will contribute in full flow from Fy23.Expect 400 bps kind of margin improvement in Chromium segment.

→ Seeing no slowdown in demand or inquiries from customers inspite of interest rate hikes,etc.Company remains confident of strong growth and industry leading RoCE.

Overall company seemed very confident of sustaining volume growth & improving margins.Debt/Equity will stay <1:1 even post capex.I don’t think there were any questions on pledging this time.

Sir seeing as how you were yourself a participant in the concall and asked some insightful questions,it will be great to have a more elaborate view from you on Vishnu Chem. Also given your large experience(over 3 decades) in markets your insights will be even more useful.

The company seems to be changing their credit rating agency frequently. They used to be rated by Ind – Ra in the past which was changed to CARE somewhere around 2016-17. In 2020-21 they have moved again from CARE to Infomerics Ratings. How should investors view this, and how credible is Infomerics?

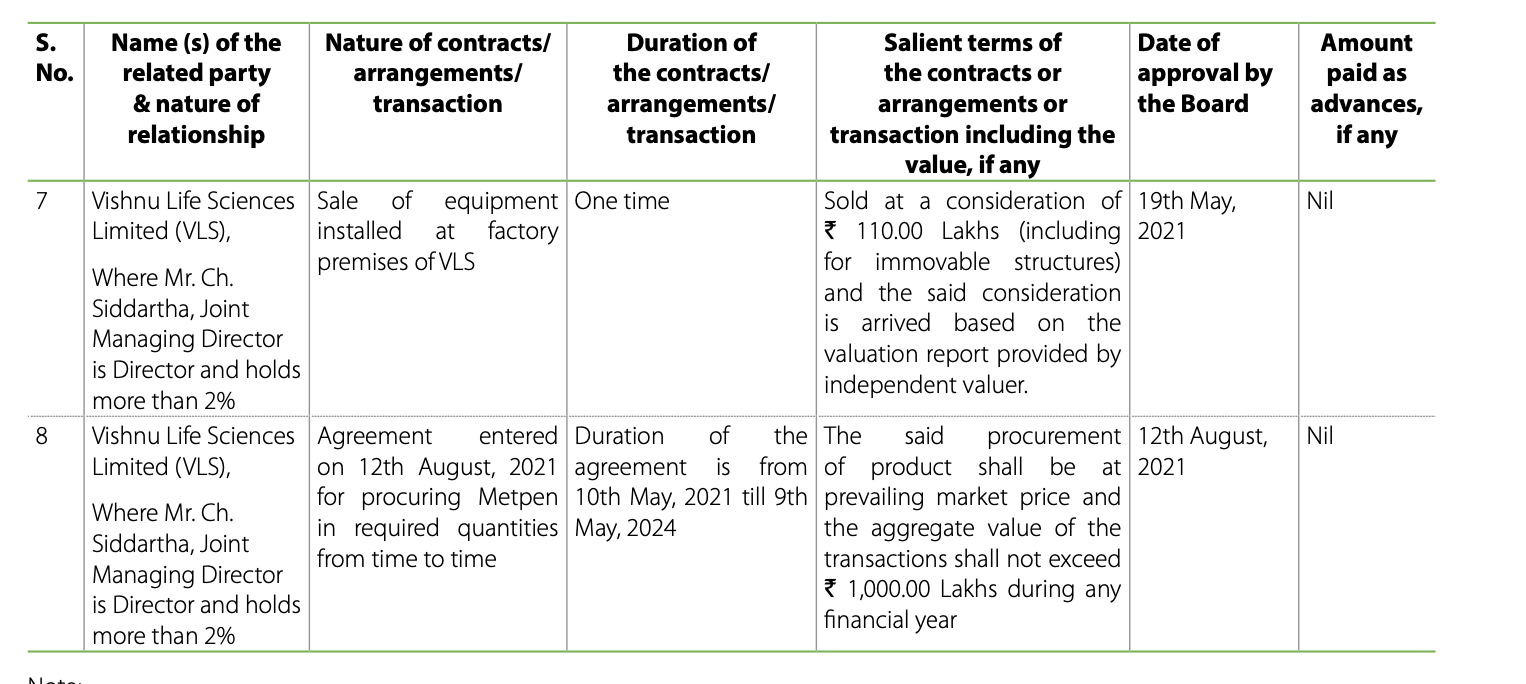

The number of related party transactions seems to be higher for me. Can anyone more experienced in reading the annual reports confirm if there is something to be concerned about these transactions?

The promoters are drawing low salaries (1.3 crores combined) so I think the lease amount paid by the company to the KMP is fine. I am not sure how to interpret some of the other transactions. Eg: 3 & 8

Disc: Invested with minimum position sizing due to higher debt and promoter pledging.

FY2023 saw a 31% increase in income and a 68% surge in profit on a consolidated basis.

Consolidated EBITDA margin increased by 550 basis points over the last two years.

Consolidated debt to equity ratio stands at 0.9 times now compared to 1.3 a year ago.

Consolidated domestic and export sales continued their growth trends, growing by 36% and 26% respectively on a year-on-year basis.

Consolidated EBITDA margin for FY2023 was 17.4% compared to 15% in FY2022, an increase of 200 basis points on Y-on-Y basis.

Consolidated PAT for Q4 FY2023 was 36 Crores compared to 29 Crores for the corresponding quarter previous year, up by 25% Y-on-Y basis and 12% on Q-on-Q basis.

Capex:

The company has 98 Crores of CWIP, out of which 93 Crores is towards its precipitated barium sulphate project, which is expected to be completed in the first half of the current financial year.

The company plans to sell 30,000 volume of barium sulphate in the first year and has already spoken with big end users and distributors in India, Europe, and North America.

The company expects volume growth in both chromium and barium chemicals in FY2024, with a focus on targeting certain EBITDAs and maintaining margins.

The company has pending capex of about 10 Crores for FY2024 and cannot give a guidance for top line growth in FY2024, but expects growth to continue with the addition of the new product in barium.

Vishnu Chemicals Limited plans to undertake a capex of Rs. 90 crores for a barium sulphate plant.

New Products:

Upon commissioning, the company will become the largest producer of barium chemicals in India.

Precipitated barium sulphate finds its application in the paint industry, powder coating, battery industry, and is also being researched by some of the most acclaimed scientists globally to create the whitest paint in the world directly from precipitated barium sulphate.

The company plans to add 20,000 tons in chromium and has backward integration of soda ash of 30,000 to 35,000 tons.

The company is working on new value-add products in both chromium and barium.

Guidance:

Company expects margin improvement in chrome and barium.

No guidance given on volume or value growth for FY2024.

The demand for barium sulphate is steady, and the company is seeing regular volumes.

The supply scenario for chromium remains steady, and the company is not witnessing any major production cuts globally.

Raw Materials:

The use of barium sulphate has seen consistent growth of 12% YoY in the powder coating industry in India, which is replacing titanium dioxide due to its oil absorption and cost-effectiveness.

The pricing of chemicals is determined by raw material cost, freight cost, and demand and supply, with a current correction in realization of under 10% due to the decrease in freight costs.

Raw material cost reduction through backward integration in barium.

Miscellaneous:

The company is recovering soda ash from the process by pumping in carbon dioxide instead of sulfuric acid, and as production increases, the recovery will be proportionately increased.

Barium sulphate is used as a replacement for TiO2 in certain applications like the powder coating industry.

The powder coating industry in India has grown from 76,000 tons to 140,000 tons in three years, and as it grows, the demand for barium sulphate will continue to increase.

The demand for barium sulphate in the powder coating industry is estimated to be about 15-20% of the overall demand for TiO2.

Utilization rate for barium chemistry was 55-60% in FY2023.

Company targeting to utilize barium carbonate capacities upwards of 70% in 2024.

R&D for chromium metal ongoing, hoping to start looking at a pilot plant towards end of 2023.

Board approvals received for QIP, enabling approval for 12 months, no update on timeline for raising funds.

Investors can reach out to the company for further questions or queries.

Any view on what the anti-thesis is on Vishnu Chemicals. They are into Chromium and Barium Speciality chemcials with a trailing PE of 13 with an anticipated PAT growth of 25-30% in the next year with the commercial production of Precipitated Barium Sulphate. The management has been delivering on their guidance for the last 2-3 years . The overhang of the promoter shareholder being pledged is also out of the way now