Have been losing interest in VIP due to the low growth rates.

Don’t see any point paying 40-50 PE for a company which always managed to find excuses for their low growth rates.

Dilip Piramal says that their sales management is poor as their new promoted CEO was heading the sales and marketing division previously and that caused internal strain. It sounds ridiculous to me as managers get promoted to CEO if their team has been doing well and naturally the new CEO will bring up his loyal subordinates to occupy his previous role. In fact, if he had two loyal subordinates, he would have assigned the second guy to lead another division.

Another excuse cited was avoiding low margin deals, but I see that Safari has posted best margins in Q3FY20 over the past six quarters.

Also, as I dig into quarter level details, I see that the growth in the past has been quite patchy too and there are no signs of consistent performance by the company. Only FY19 was quite impressive which pulled up their overall CAGR to 15% over the last five years.

2020

2019

2018

2017

2016

2015

2014

Q1

564

518

400

374

353

328

309

Q2

412

402

309

284

294

217

197

Q3

432

430

338

306

290

252

235

Q4

435

363

303

274

244

226

Q1 Growth %

0.088

0.295

0.0695

0.059

0.076

0.061

-

Q2 Growth %

0.024

0.300

0.088

-0.034

0.354

0.101

-

Q3 Growth %

0.004

0.272

0.104

0.055

0.150

0.072

-

Q4 Growth %

-1

0.198

0.198

0.105

0.122

0.079

-

If you look at Safari during the same period, they have shown CAGR of 30% over past five years and that’s definitely more consistent.

Though I appreciate management’s initiative to have their own manufacturing facilities, these kind of excuses and patchy growth is putting me off. And though Safari is very consistent in terms of growth has poor margins and WC. So decided to sell VIP and also not enter Safari. Will consider Safari if its margins and working capital improves and also reduce their dependence on China but these don’t look close-by.

I have sold my small holding in VIP due to above reasons. Just tracking using one share. Used that cash (actually added more to it) to buy Endurance Technologies as a core position. If anyone else looking to replace, you can consider Endurance as a good option. It has improved its EBITDA margins throughout the slowdown and the sales de-growth is lower than other 2W companies de-growth. Endurance has actually improved its PBT throughout the slowdown (if you account for corp tax cut, PAT growth is even higher). I have posted more details on Endurance thread.

Discl: Not a SEBI registered advisor. Please do your own research / talk to your investment advisor before buying / selling any of the companies mentioned above. As mentioned above, I have sold VIP and hold only one share now. Never bought / sold Safari. Bought Endurance Technologies as a core position this week.

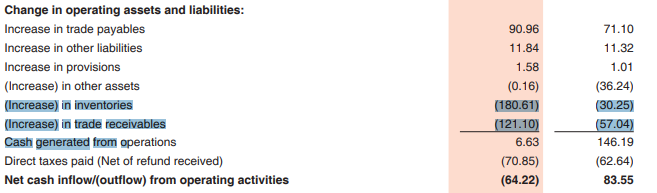

The Cash Flow from operations of the company is constantly less than reported net profits for the last 10 years. Why is it so? I reckon this business operated on cash-and-carry model

Working Capital requirement is increased heavily, a big number in 2019.

as per the AR Mar 2019, there has been a big jump in inventories and for trade receivables. Both of which is not good.

The sales growth was a dull 7.6% for the year ending 2019-20. This year the Sales are likely to see nosedive due to the travel industry being largely affected. Therefore, I see no reason to pay 21PE for this stock. A correction of 50% is likely. This stock is probably a safe buy at Rs.95.

This seems to be the accounting approach adopted by the company. They book revenues aggressively and also build inventories accordingly. Not sure if this is the norm across the industry or not.

However, considering this and the latest impact of COVID 19 on tourism, some adjustments will have to be made in valuing the company now.

Revenue for the quarter at Rs 317 crore vs Rs 437 crore YoY

PAT for the quarter at Rs 10 crore vs Rs 25 crore YoY

ROCE for full year improved to 25% as compared to 22% last year on account of improvement in working capital

Inventory at Rs 451 crore vs Rs 527 crore YoY; Debtors at Rs 267 crore vs Rs 299 crore YoY

Borrowings at Rs 32 crore vs Rs 86 crore YoY

ConCall highlights:

VIP has increased its borrowings and there is no challenges on account of liquidity

Leisure travel likely to be bouncing bank earlier than business travel

VIP can run the business profitably with very low volume

Company has lost revenue of Rs 120 crore and PBT of Rs 26 crore due to this Covid in Q4

Gross margin has improved to 58% from 48% in the corresponding quarter last year due to higher procurement from Bangladesh, increased contribution of hard luggage and lower raw material cost

During Jan-Feb 2020 VIP made PBT of Rs 38 crore, which is higher than Q4FY19; but company has reported revenue of Rs 32 crore in the month of March and Loss of Rs 27 crore

Large number of stores are in malls which are all closed due to lockdown

Company has guided revenue range of Rs 750-1,500 crore for FY21

Company has taken many steps which will reduce cost by around 30%

VIP spends around Rs 100 crore on advertisement but this year company won’t spend any on advertisement, only very small amount will be used on digital platform

Earlier company used to procure 60% from China and 10% from Bangladesh and rest from domestic market; but going forward procurement from Bangladesh can increase up to 80-90%. During Q4FY20 Bangladesh contributed 55%

Bangladesh plant procure 90% raw materials from China

VIP has increased its borrowing sanctioned limit to Rs 220 crore from Rs 100 crore

Company has made a provision of Rs 8.5 crore during this quarter for receivable

VIP has no contractual labor for Bangladesh plant; while for India 50% is contractual

Backpack season will move to August-September from April-May this year as school season will start August onwards

Samsonite had around 300 stores and they are closing 100 outlets. VIP has 250 EBO and will shut 50-100 stores. Per store revenue for Samsonite is double than VIP

E-commerce contributes around 10-15% currently for luggage industry but in next three years contribution will increase to 30%

Cheers saninv… my main worry with VIP was that they used to be too dependant on China for soft luggage. This would have left them really exposed in the current situation with China and to the rupee depreciation. I’d imagined they’d take years to fully shift from China to Bangladesh but they’ve done some black magic and managed the same. The way I see it is they are expecting low demand for a few quarters due to the impact on travel. For this low demand period they will be able to easily manufacture soft luggage in Bangladesh. They’ll use this period to increase the manufacturing capacity in Bangladesh. Long term this will improve their margins and my main worry which was dependency on China and hence fluctuating margins will go away! They also mentioned hard luggage demand increased which they produce in India anyway so a lot of positives here and I am now very interested in its CMP. Few quarters of pain but VIP needed this kick to wake up and improve their margins which have been in single digits too long. The only point i dint like was that Bangladesh plant procures 90 percent raw material from china. If that is true then the dependency on China would still exist. Il try to get more clarity on that.

Thanx Malkd. Whole industry directly or indirectly dependent on China as of now. They are now planning to manufacture the final product from Bangladesh unit with raw materials procured China, which may aid their bottom line.

Cheers saninv. Overall their margins this year will increase greatly. This stock could surprise the markets due to that. What I like about the management is they’ve clearly stated the revenue will drop to 750 to 1500 Cr for this year ie a 30 to 60 percent drop. the CMP is currently assuming worst case scenario and has dropped nearly 60 percent. If the margins improve (which it will due to Bangladesh) then it means it’s currently at a bargain price. So basically not much risk in the short term of further downfall and in the long term things will go back to normal and they’ll be running at better margins. I may have just convinced myself to invest at CMP … will do it in tranches though. 10 percent now and the balance over the next 2 years based on results and commentary.

By saying that the market has already assumed the worst case scenario i.e. a 60% price drop assumes that the stock was priced perfectly before the drop. In this case, it seems like the stock was overpriced before the drop. My concern here is that because VIP’s major sales takes place proportionately to the amount of discretionary income and overall travel, there is still a huge amount of uncertainty.

Agreed. There’s still some pain left here. However, considering the main issue I’ve always had with vip is their low margins and dependancy on china for the majority of their revenue I’m very happy that those issues are going to be gone soon. The stock was overvalued back in 2018 when people went overboard buying it and the volumes were crazy. It then traded at the same level ie for nearly 2 years since people realised that as long as the margins were low this stock wasn’t worth the high price. Their cashflows and prospects finally caught up with the stock price in december so I do believe the market got the price about right. Then corona hit. If vip had been more proactive regards shifting to Bangladesh earlier(last I heard they said it would take a few years to do so) then the margins would increase and price would increase too. Now that they’ve miraculously done the transition (im still a little suspicious as to how they did it so quickly and why they dint do this as quickly in normal times) I believe the valuation should be even higher and hence why it could be a bargain at cmp. Reveneues will be hit for a few quarters obviously since travel is basically dead… but if they can use this time to improve margins and increase revenues from backpacks ans skybags I feel long term it’s going to make vip an even better bet. I’m using the next two years to accumulate in 10 tranches. First tranche done and 9 more left based on quarter results and commentary over the next 2 years. I’m almost hoping the price stays stagnant for 2 years so this definitely isn’t a short term play for anyone reading this

That makes sense. However, I work in the bag/footwear industry and have an inherent problem with VIP. See, if you look at it honestly, VIP really does not have any moat. Yes you can argue that there is economies of scale available, however luggage and backpacks are overall a commodity sort of product. There is not a lot of differentiation in terms of quality or brand image between the existent brands (Safari etc.). Also, this makes it very susceptible to foreign (more likely Chinese) brands to come in and sell the exact same product for 10% lower. No matter where they buy the product from, there margins will never drastically improve because in this business the brand moat is very fragile. There is also very less space for innovation. Let us not give this business more credit than it deserves. It is a trading business where there is practically no barrier to entry.

Haha. Harsh but true. The only moat they have is economies of scale. Gst began killing the unorganised sector and even if that sector will never die it’s going to get very expensive to be able to make a product and sell it at the same low prices as VIP. Add corona and I can see VIP eating up the share of the unorganised sector. Samsonite and safari will always be threats but there’s competition in evert segment. The pivot from vip into Backpacks went brilliantly and they are market leaders there if I’m not mistaken… and their Caprese handbags have sold beyond expectation too. So atleast they aren’t one trick ponies anymore. With their hopefully increasing margins and command of their supply chain by manufacturing in Bangladesh their moat could well become quality with pricing power compared to their competitors. There is scope for new launches in the future too to add to their portfolio(though top of my head I can’t think of anything bag related apart from Luggage, Backpacks and handbags ) . You may be right though. It’s not an exciting buy for sure. Me and the people around me that I know just really like all 3 of their products ie vip, skybags and Caprese so considering the brand recall of all 3 products they could easily command a much bigger market share over the next decade imo

I hadn’t heard of their Carlton line until I began researching VIP and I’d never heard of their cheaper/mass market brands and can’t even recall them now lol so they have work to do in those segments. Maybe I’m a bit biased now that I have a small stake but I can see runway for growth. That being said I spent so much time studying this business that I almost felt like itd be a waste if I dint take a position… so I took a small one today . I like this company and the promoters along with Sudip Ghose (though new) seem trustworthy and haven’t made too many mistakes that I can catch over the past few years. So yup… I’m committed now. Hopefully it’s a profitable journey over the next few years. Sometime i swear I enjoy the thrill of investing more than the investment

Cheers Ritu. That article covers exactly why I want to accumulate VIP over the next 2 years and also explains why anyone looking at short term gains should stay well away. When everything opens up this will lead the pack. The unorganised sector will get a huge hit too. VIP is sitting on huge cash reserves to weather the storm and has its backpacks and handbags to help them over the next 2 years and apart from employees and factory rent they have no real fixed expenses. Expecting them to come out even stronger after this.

Yes, one thing that makes me always interested in VIP is Dilip Piramal. He is a veteran in the industry and has seen many ups and downs. If i were to invest (which I would if the stock falls about 20% more), the owner family would be a big reason.

If it does fall 20 percent more il buy my entire planned amount in one go instead of waiting for 2 years with an sip. I think the shock has abated and it’s already moved up from its lows of sub 200 so I really doubt it… though Q1 results could cause a temporary dip. almost hoping it does crash so I can buy all of it in one shot lol.