Ms Vinati was on CNBC saying that the ATBS plant is fully booked. This is completely understandable as customers at this point are more concerned about supply and logistics issues rather than demand related problems.

But, if the COVID situation is prolonged, demand will fall sharply. Last night Bill Ackman of Pershing Capital laid out this nightmare scenario on CNBC (USA) of a prolonged disruption due to COVID.

At this point, cash is king and to think that COVID will be a short interruption is taking a huge risk - especially for manufacturers.

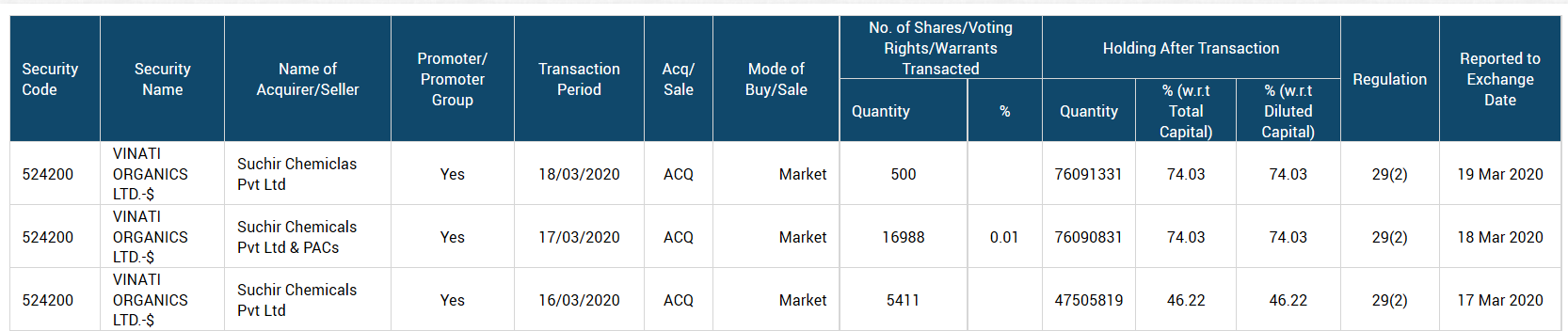

There is further more buying from the promoter in the last week. An overall buy of 51760 shares which translates to approximately 3.6Cr INR at 700Rs per stock. The total ownership by Suchir Chemicals went from 46.21 to 46.26.

Does such series of purchase through March mean promoters feel that the stock is priced fairly? A few years ago, the management decided to do a stock buy back from the open market and was priced at around 1000 Rs while stock was trading at around 900 if I remember right. When asked in an interview, Vinati Saraf mentioned that they believe that 1000 Rs was a fair price given strong outlook for the company. The stock later went on to double and then had a stock split and CMP of 774 translates to 1500 pre-split. However, can we bet on this management buying spree?

One report on this thread (possibly by HDFC securities) indicated that recent margins for Vinati suffered because of slowdown in the Oil industry. Given that oil prices will remain low (higher supply, lower demand - more so in the post COVID world), isn’t this going to further play spoil sport on margins in ATBS?

There seems to be negative outlook on IBB product as well with the covid situation (see some previous posts where Govts are recommending not to use ibuprofen causing side effects in those suffering from Covid)

The other product coming up is the Butyl phenols which is more of a domestic market play, is still to pick up steam but is anyway known to be a lower margin product as compared to ATBS and IBB.

The difference between us and the business owners is that the business owners are actually in it for the long term. Yes, there are disruptions visible in the short term. But, what if the company has visibility of launching new products in the next 5-10 years. Given the company’s innovative culture, it won’t come as a suprise.

Yes, growth in this sector remain. However, more worry is from chemicals used in Oil sector especially shell oil. Oil price below $25 will default shell oil producers.

"To sustain high growth, companies need to overcome this “portfolio treadmill”

effect: for each product that matures and declines in revenues, the

company needs to find a similar-sized replacement product to stay level in

revenues—and even more to continue growing. Think of the pharmaceutical

industry, which showed unprecedented growth from the mid-1990s, thanks to

so-called blockbuster drugs such as Lipitor and Celebrex. When the patents for

this generation of drugs expire between 2010 and 2015, revenues from them

will plummet. Pharmaceutical companies need to launch similar-sized drugs

just to make up the difference, let alone keep growing. But finding sizable new sources of growth requires more experimentation and a longer time horizon than many companies are willing to invest in.

One can draw many inferences from the bolded text. One of the most important things that investors don’t value in my opinion is the culture of the organisation. Their continued persistance with chemicals like ATBS (CASH LOSSES) and PAP (Trying to make it since 1998), just shows the management actually thinks in a long term manner. This is a competitive advantage in itself. Won’t be suprised to see new products being launched in next 5 years or so.

I have been tracking Vinati for some time now. They have excellent return ratio’s for last 10 years and what is most stand out is their OPM which is north of 40%. I did study their business model which is heavily dominated by 2 products one is ATBS (50% revenue) and the other one is IBB which contributed around 9% to top line last year. They have IB which is raw material for ATBS.

I am holding off my investments for the below reasons:

Management commentary: They projected 15% CAGR in growth then downgraded to 10% then again to FLAT.

Heavily dependent on few products: Majority of revenue is coming from ATBS and they had lot of demand due to exit of Lubrizol but now that effect has worn out and management is projecting lower margin due to increased competition. IBB is into single digits.

They are getting into low margin BP business which would further contract their operating margins.

I tend to believe Vinati of 2020-2030 may not be same as that of the one from 2010-2020.

Thanks for the video

Just thinking loud:

Ms Saraf said IBB roughly 25% higher pre covid level. This was 17% of business so revenue should increase by 5%

Average revenue of 1071 per quarter at 105% would be roughly 281

She also said raw materials have reduced due to crude prices

So operating margin might be 118 at 42%

Reduce depreciation of 9 and add roughly some other income, NP before tax might be roughly around 120 levels

This will be more than offset by ATBS for which both pricing and volumes would be down. In the above interview, both Ms.Vinati and Dr.Palekar were cautious. She said the whole China-to-India move will take atleast 5 years and is only predicting 10-15% growth till then.

-Total income fell Year on year from 306 crores to 261 crores (down by 15%), if we exclude the other income then total income is down by 18%+. This is due to realizations being down as crude prices have corrected a lot. Better to look at bottom line/volume numbers (management doesn’t give).

Depreciation increase from 6.81 crore to 9.7 crore due to new capacities.

-The cost of material consumed (rm cost) also reduced by 26% due to softening in crude oil prices as Vinati works on pass-through model.

Operating margins remained at 41% when compared to last year, expect them to come down as the lower margin Butyl phenol capacity gets commissioned.

-PAT fell by 10% YOY. Majorly on account of slow uptake in ATBS as 20%+ consumption of ATBS happens in the shale production.

Balance sheet update

Property, Plant, and equipment went up by 280 crores. Majorly on account of the commissioning of new capacities (ATBS+Butyl phenols)

-CWIP reduced YOY from 191 crores to 31 crores on account of the commissioning of new capacities.

Trade receivables fell YOY from 244 crores to 201 crores. (Major improvement, will reflect in the cash flow)

Bank Balances increased from 3.76 crores to 44 crores YOY.

Book value increased from 1227 crores to 1442 crores (YOY), majorly due to the increase in other equity.

Cash Flow Update

Net cash flow from operating activities went up from 200 crores to 415 crores.

This was majorly on the account of decrease in trade receivables and other current assets.

Company incurred a capex of 310 crores in FY2020, there was a positive inflow from capital advances/ cwip of 172 crores (not so sure related to what). Final capex (138 crores)

Cash&cash equivalents has improved from 49.12 crores to 158.58 crores YOY.

My take:

Going forward, expecting margins to compress, but free cash flow generation will improve as capex is likely to subside. Butyl Phenols is the new product which will be the likely growth driver in the coming years, and management has plans to further integrate into butyl-phenol oxides. There can be near term pressures on account of low offtake in ATBS due to crash in crude oil prices hurting producers

PAP on hold (announced last year), pilot trial failed; PAP is an important raw material for paracetamol and they are looking to get back into this because of governments focus on reducing China dependence

Butyl phenol: Started the plant manufacturing 3 out of the 4 molecules (not at full capacity yet), revenues will start flowing in from Q2FY21; Maximum revenue expected is ~400 cr. This year they are targeting 150-200 cr.

Guides for no revenue growth this year (demand for ATBS adversely affected due to oil and gas sector crash). Growth will come from FY22