I don’t know. This data is from an HDFC Securities report available in public domain. You may Google for it. My concern is more with the extent of correction rather than the actual value.

Valid point. But then we should understand why no one is adding capacity (and some are in fact exiting!) if ATBS is such an attractive business as is made out to be.

No one is adding capacities as Vinati is the lowest cost producer and attaining purity in this chemical is one of the most difficult things. Vinati itself took nearly more than 5 years to attain desired level of purity. Who would go throu such a gestation period? Existing players can’t compete with Vinatis cost. It’s a cost leader coupled with a greener process. Definitely there’s an entry barrier. However, valuations seem to be too high as of now. Will get interested if it falls due to the shallow cyclical nature of the company.

Very true. NCL is holding the global patent for that highly efficient process & Vinati is the only commercial licensee.

NCL-VOL team has received much praise from their competitor Lubrizol for installing such a well-streamlined and compact plant. While Lubrizol is struggling with the recovery and recycling of acrylonitrile that has not been converted (85%), VOL is successfully utilising the recovery process invented by the NCL team. Due to their uniqueness, the plant and the recovery process have been patented by NCL. The monomers in the effluents from the process are polymerised and sold to the construction industry, thus minimising the environmental impact of the manufacturing process.

On ATBS patent part:

Patent would be expiring in March 22 ( two more years), but does it count much, or the further process enhancements/expertise which probably are not patented counts more?

I am saying it so because, one or two other patents they have let expire and no patent they have for their new products.

Q

Dependence on Enhanced Oil Recovery / any one application?

Impact of patent expiry in 2022 ( it is still little far away)

How much of price control in the Vinati’ hand for ATBS?

Who are the competitors, will they play price game or enjoy new enhanced profitability?

I am stating a probability and not the conclusion.

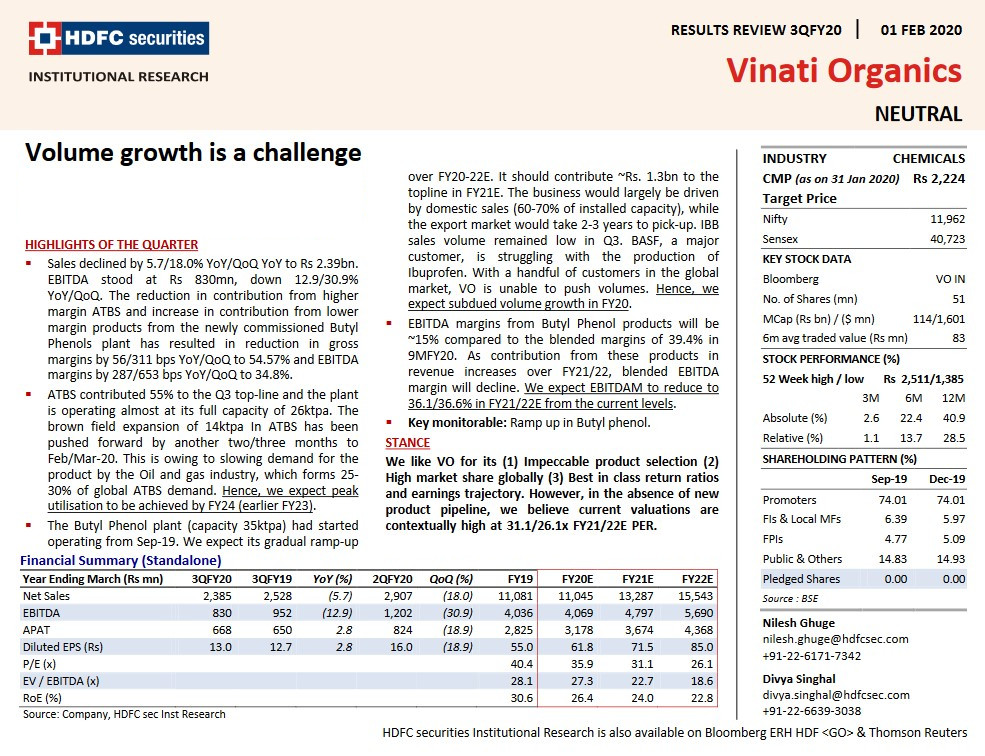

As management has highlighted there is no shortage of ATBS in the market more over additional capacity is being created, I suspect margins may decline to pre-Lubrizol era. Quarterly sales numbers and margin contraction may be indicating the same.

Discl: No investment but keenly tracking to understand market and commodity cycles

Q3 is on the lower side historically. This was an one-off quarter.

Sales of higher margin products like ATBS were down this quarter but have started picking up from January.

FY20 is likely to finish flat with a PAT growth of 10-15% coming from tax benefits.

FY21: volume growth in Butyl Phenol will start from Feb onwards, new line of ATBS will be operational from end of February. A total of 15-20% volume growth is expected.

Vinati Organics had last split the face value of its shares from Rs 2 to Rs 1 in 2019. The share has been quoting on an ex-split basis from February 05, 2020.

There is no disruption due to Coronavirus to Vinati’s business

Impact:-

ATBS: China is a major competitor, so fallout has been that greater number of enquires have come to the company and they are expecting a better Q4 than Q3.

IBB: A mjajor customer has been impacted. However, other manufacters have increased production of ibuprofen and company is not seeing any slowdown in IBB sales.

The new capacity is to start from April and the company is expecting 15%-20% revenue growth in the next 2-3 years.

The new Butyl Phenol plant will add around 350-400 cr at full capacity. India imports 25,000 tons of butyl phenols and the global market is about 100,000 tons pa. The company should easily be able to sell its entire capacity.

Additional line of ATBS is likely to start next month.

French Health Minister has issued an advisory not to use Ibuprofen and shift to Paracetamol instead, amid the corona virus scare. The French Government website on COVID-19 recommendations now says “ NSAIDs should be banned ”. This can have serious long term implications for Vinati Organics, though at the moment there are conflicting opinions on this with some experts questioning this stance. A couple of reports given below, please Google for more.

More concerning is the pressure that Shale Gas industry will face. As nearly, 20-25% of ATBS sales are done to the Shale Gas industry. Its important to study the entire Value chain in B2B businesses to understand where the fragility lies. This source of fragility can be a future source of risk and opportunity at the same time.