Vikas Ecotech is a chemicals company.

History

Earlier known as Vikas Globalone. It was an NBFC listd in BSE in mid-1990. The company started as agent to Reliance, SRF, Nirma, Arkema etc in North India. Company backward integrated into manufacturing in 2003.

Products

According to 14-15 Annual report main product of the company is

Thermoplastic Rubber Compounds which form 31% of turnover of company.

Thermoplastic Rubber (TPR) Compounds are formulated using Styrene-Butadiene-Styrene (SBS) or Styrene-Ethylene/Butylene-Styrene (SEBS) block co-polymers. Most of TRP formulations are 100% recyclable.

Some typical applications of TPR compounds are footwear products, gaskets, cable jacketing, toys, automotive applications, soft touch over-molding and general purpose molded goods. These compounds can be formulated to provide weather resistance, ozone resistance, low temperature flexibility as well as excellent resistance to many chemicals. They are light weight and can be colored to meet your

requirements.

Other products

Methyltin Mercaptide

Tin Tetrachloride

Epoxidised soya bean oil

EVA compounds

PET compounds

PVC compounds

Raw Material

Tin Alloy

2-Ethylhexyl Thiogycolate

Tinmate

PVC compound

TPR compound

Hydrogen Peroxide

RSO Refined Soyabean Oil

Styrene Butadiene Copolymer

Thermal Plastic Elastomer

Methyl Chloride (Gas)

Customers

SRF

Escorts

Cables - RR Kabel, KEI industries, Havells India

Shoes - Relaxo, Liberty

Plastic Furniture - Supreme Industries

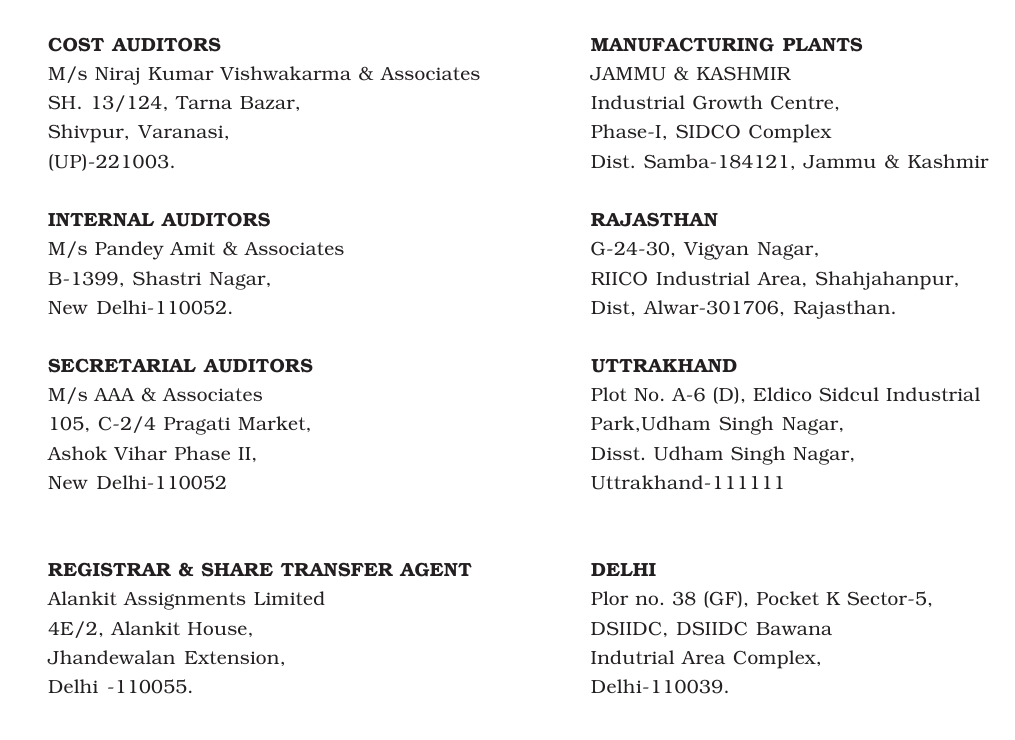

Plant Locations

I. Jammu & Kashmir, Dist. - Samba

II. Rajasthan - Shahjahanpur, Dist. - Alwar

III. Uttrakhand, Dist. - Udham Singh Nagar

IV. Delhi, Bawana Industrial Complex

V. Gujarat - Dahej - Under construction

Subsidiary

As of 31-Mar-15 company does not have subsidiary.

Financial

Profit and Loss (Source- Screener.in)

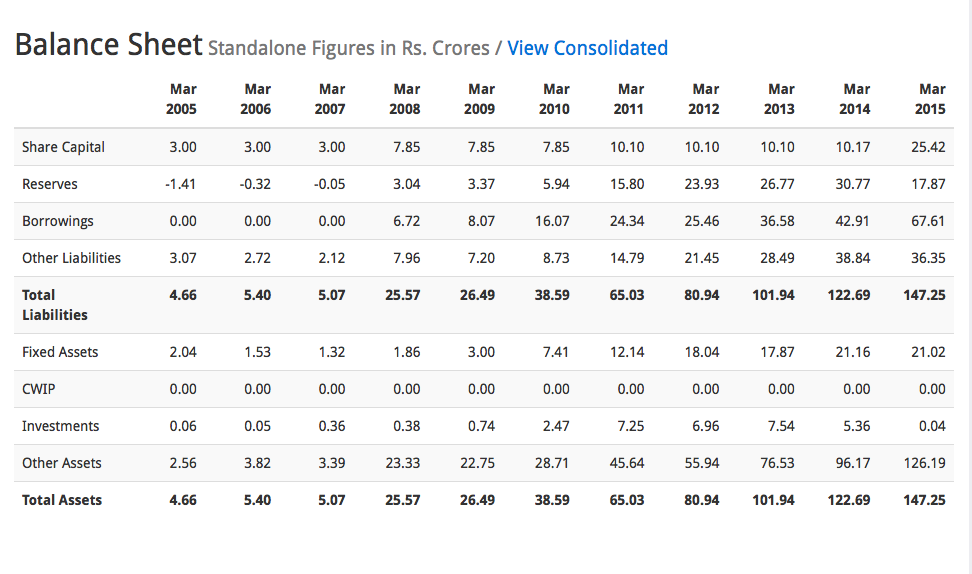

Balance sheet (Source - Screener.in)

Recent Management Guidance

On a recent interview on CNBC here the MD of the company Mr. Vikas Garg said the following about the company.

I. Specialty chemical manufacturer and products are not manufactured in India.

II. Will grow at CAGR of 35-40% for next 3 years.

III. Maintain a margin of 22%.

IV. Margin expanded due to - Doubling of exports in Fy16, in-house R & D.

V. Manufacturing to trading ratio 80:20

Key Risk/Concerns

I. Management inflating guidance - In an interview to Inc500 in 2011, MD guided for 800cr revenue in next five years but revenue in 2016 is 312cr.

II. Low promoter holding - Promoter holding is less than 50% with Vikas himself holding only 23.xx%

III. Very high trade receivables - Trade receivables are high. As percentage of revenue close to 45% this year.

IV. Cash flow from Operation not matching Net profit over 10 years period - Summation of Cash flow from operation from 2005-15 is -27.5cr whereas same for net profit is 28.8cr

V. Company is working capital negative.

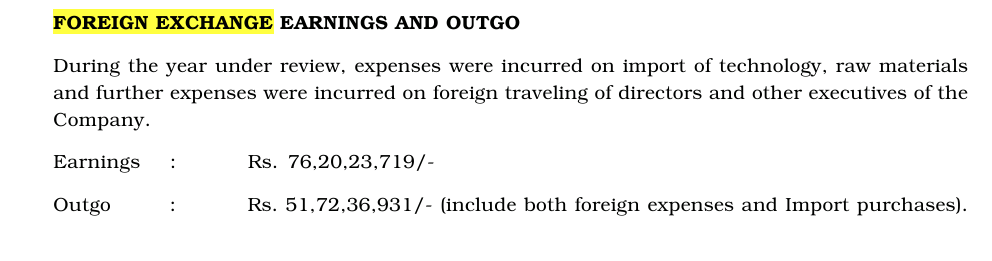

VI. Unexplained forex outflow - Forex inflow/ outflow of 76cr/51cr respectively. What are they importing?

VII. Plant in sensitive area - Company has a plant in Samba - J & K. Army camp in Samba was attached by terrorist in recent past.

Other points

I. Merrill Lynch Capital bought 1.9m shares at Rs. 20.25 in Feb-16.

II. Shares are trading today at lower circuit at Rs. 11.

III. Company is growing at scorching pace, revenue growth this year is 46%. Net profit grew at 571%

Interview of MD by Business India (360.1 KB)

Disclosure

Not Invested. Opinions Invited.

. With the current plant installation revenues of 325cr from the manufacturing unit seems pretty conservative from the management. Overall topline should be 400 cr.

. With the current plant installation revenues of 325cr from the manufacturing unit seems pretty conservative from the management. Overall topline should be 400 cr.