Gaurav,

They are definitely importing some of the Chemical compounds with niche players around the world with whom they have contacts. No need to get clarity here.

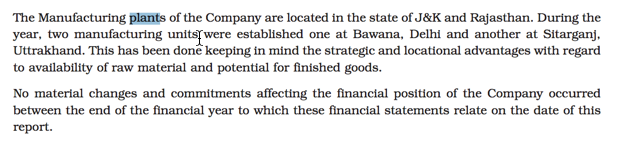

Their other 2 plants are definitely existent. What do they do in these plants needs to be investigated?

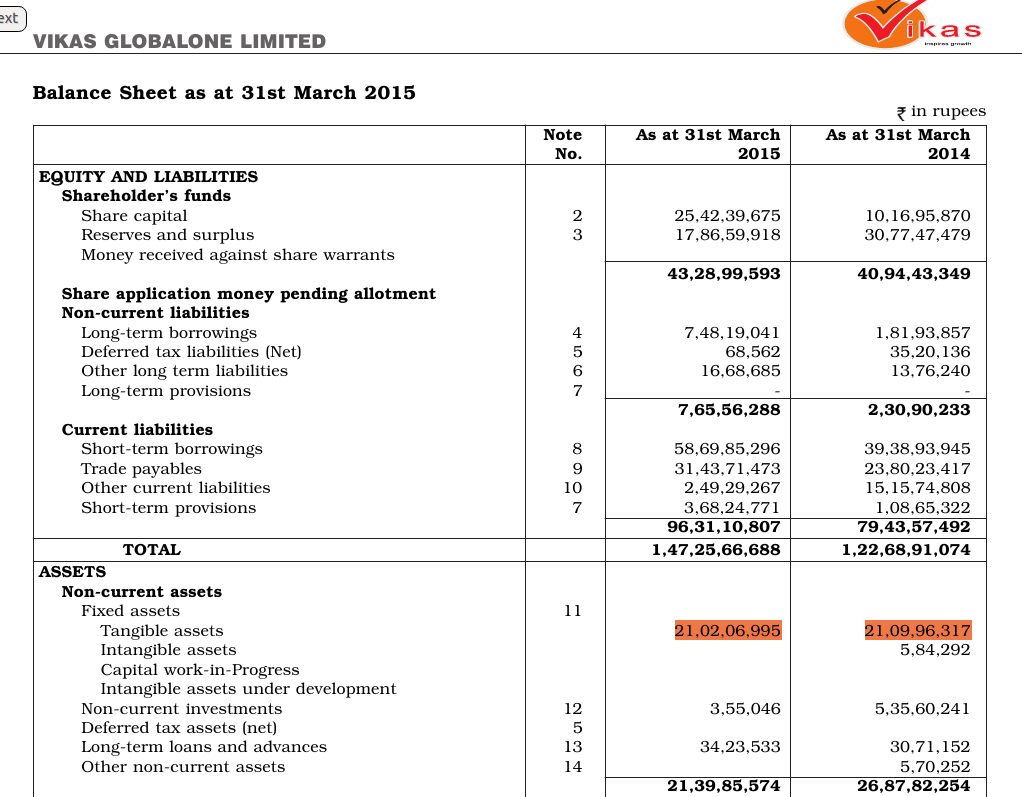

One thing that is strange is that the receivables/sales is typically around 1/6 for major chemical companies. If Vikas Ecotech has such a wide client base (50% export business included), it is not clear if all of them can delay payments to the order of 4.5 months concurrently.

We would have to understand the following w.r.t their operations:

When do they declare a sales as done? After the order is received or after the shipment of products?

What is the typical payment cycle for variety of products

Is the delayed payments concentrated over a single customer/Single product or is it happening for all products. With 45% in Trade receivables, it is unclear how all of the products will have such inordinate delays.

Something is amiss that is making both the local and international procurers to delay payments.

Quick glance of the balance sheet of Havells/Liberty shows that they do not keep a lot of “Trade Payables” outstanding

Does Vikas Eco get paid only when products are disposed off the shelf by customers or immediately after shipment?

Is there any agreement to take back unused products from the customers?

If you or Ashish can get these answered while calling up the folks or during concalls, it would put a lot of doubts behind us.

[quote=“anand_paxonet, post:21, topic:5549”]

They are definitely importing some of the Chemical compounds with niche players around the world with whom they have contacts. No need to get clarity here.

[/quote]

You are right. I missed the following in the annual report.

Hey Anand and Guarav, I am new to this forum and I have been following this company for a while… the details shared by you are great. My two cents to add on the discussion so far;

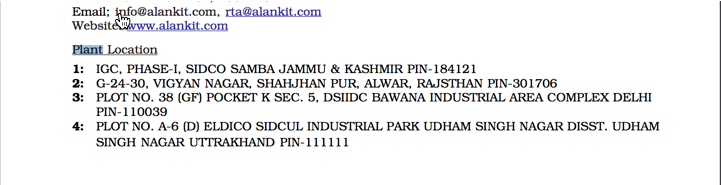

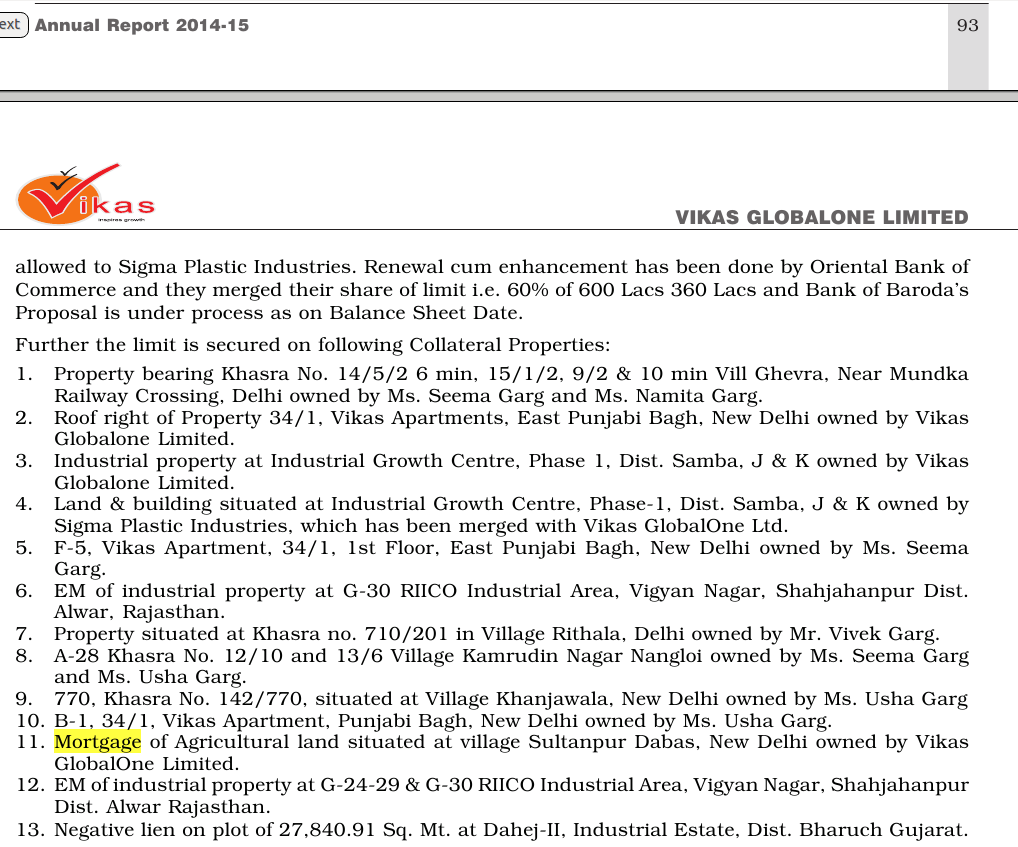

About the question of missing plants, it seems that additional two plants are mentioned in the AR2015.

There is also a more descriptive mention of the two plants is also mentioned on Page 17

I also called them to check when FY16 Annual reports will be out and it seems that it would be in 1st week of September.

Some updates after talking to investor relationship team in Vikas Eco:

The two plants in Delhi and Uttarakhand are no longer operational. They have been consolidated into Shahjanpur plant

Receivables issue:

a) Company has added a majority of customers in the last 1-1.5 years. Most of them having business with Vikas Eco first time around, wanted extended payment cycles.

b) They have a agreed upon 60 days with most customers but since the relationship is new, delays are being accepted

c) With top ranked customers like Liberty, supreme, Havells management expects the payment cycles to be on time in the future.

d) Expectation from the management is to have stringent payment cycles of 60 days in 3-4 quarters

e) Almost zero bad-debts reported in the past. This gives a better indication of the realization rates.

I would believe that this may be due to re-balancing of inventory. Usually Q4 and Q1’s are the toughest ones to compare due to inventory disposals.

Overall mgmt expects 80-20 in terms of revenues from manufacturing/trading. Since trading carries almost negligible profits, most of the EPS will be reflected by the flow of revenues from manufacturing.

Again i may be wrong, but these are probably fair enough inventory management assumptions and they are not going to be similar over every quarter.

You can probably say that both these people (Prince Pipes and Navneet) are people ‘acting in concert’. Since it is a customer who has picked up the shares, one must consider if this is some kind of ‘funding’ deal for the Co.

The company’s debt is more than its equity(Risk is high) . Most of the debt is short term in nature. However the company has very little cash balance . If the company is asked to pay it’s short term debt, How will they do that ?

The net profit margin Is around 9%. To meet the working capital requirement which is around 29 crores, more debt will be required.

The raw material cost is almost 75 -80% of the total revenue.

The company’s growth is totally attached to their flagship product organotins. However the sales of this product was 50 % of the total current capacity.

The receivable days are very high , which is not helping the company.

Gaurav,

Are you sure if VEL was talking about Tin stabilizers?

Next Interesting read from “Unusual Billionaires”. Asian Paints in the early 1970’s had an issue of High receivables and had to take Short term borrowings for working capital requirements. Someone figured out an ingenious idea of incentivizing the customers with a discount of upto 3.5% if they made payments on time. With this the working capital requirements came down, interest outgo went down and Balance sheet started appearing more healthy. Quite intelligent and way too simple.

Not sure how difficult this is to implement in the case of VEL also. Some food for thought.