Thanks.

I understood what u said, except the free cash flow part.

How do we check this free cash flow and what is it used for ?

For a minute, I thought I was looking at my portfolio . My question is if everyone is picking the same stocks , won’t the profits be shared equally. I guess that’s why people venture into small and mid caps to gain those extra returns

1 Like

@vibhor_vaish

The profits will be shared among shareholders according to their stake on pro rata basis and not equally. Well venturing into small and mid cap stocks are not bad when one does the detail study and due diligence. The greatest danger is that innocent and gullible investors fall prey to the media and half illiterate investors where they daily throw bait for them. Beware of such sheep in wolf clothing. Following them blindly will ruin your health and wealth.

1 Like

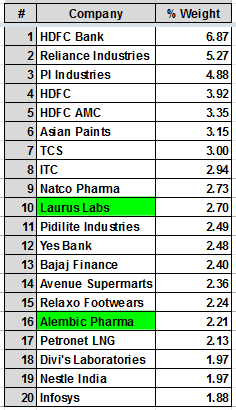

PF Stock Update as on 30.10.2020

Top 20 Holdings:

Note: No additions in the month of Oct’2020 in core PF except for Nestle.

8 Likes

Great learning. Thank you for sharing!!

1 Like

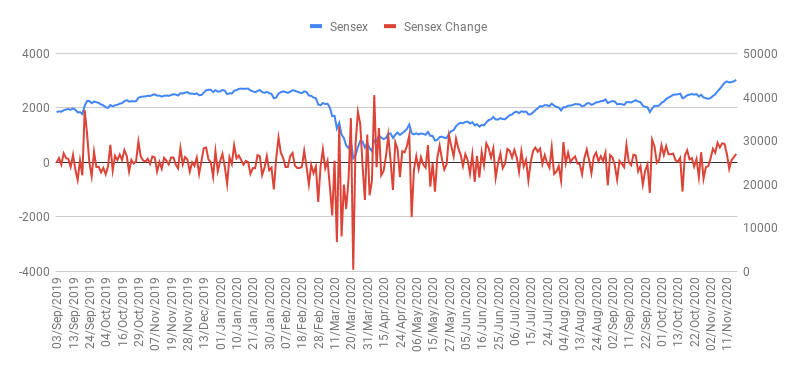

Sensex hit the All time high of 44000 today!

And this moment is worth revisiting and pondering.The upside in Sensex since I posted couple of months ago has been very ferocious and unexpected. IMO, the confirmation of ‘Mega Bull run’ has been strong and now I observe that the Sensex will make peak of around 55000-58000 in next 12-18 months with intermittent corrections. It’s a wait and watch period!

Long term investors need to be watchful of valuations before taking plunge.

Happy investing!

VK

1 Like

NATCO Pharma:

Concall Summary dated 13th Nov 2020

Revenue: ₹802.2 cr (▲65.2%) Net Profit: ₹203.9 cr (▲73.2%)

Financial Performance:

- The revenue from operations was ₹802.2 crore in Q2 FY21 as against ₹485.7 in Q2 FY20, an increase of 65.2% YoY.

- During the quarter, the net profit grew by 73.2% YoY to ₹203.9 crore from ₹117.7 crore in Q2 FY20.

- It had a cash and cash equivalent of ₹206.2 crore as on September 30, 2020.

- The net debt was ₹431 crore in Q2 FY21 with actual borrowings of ₹105 crore and foreign bill discounting of ₹326 crore.

- It declared a dividend of ₹3 per share during the quarter.

Business Performance

- The active pharmaceutical ingredient (API) had a revenue of ₹199.7 crore during the quarter.

- The domestic formulations business revenue was ₹108.3 crore in Q2 FY21 while the formulations, export business stood at ₹482 crore during the quarter.

- It witnessed a decline in the sale of Hepatitis C drug and ~70%-75% of the sales potential had been realised on account of lower visit to hospitals for cancer treatments due to Covid.

- The cardio and diabetology business performed well, with a demand pick-up of 70% towards oral business. The chemotherapy business remained subdued as the maximum revenue is derived from 5 major states Delhi, Mumbai, Hyderabad, Chennai and Bangalore, which witnessed a decline in patient’s visit.

- The decline in oncology business was more in USA than in India. It witnessed a less decline in India on account of branded nature of the business here.

- The total capex spending towards agriculture-chemical (agro-chem) business was ₹31 crore during the quarter and overall capital expenditure towards it had been ₹140 crore. The company would be hiring 80-100 people for launching its new product portfolio. It is utilising its capital expenditure mostly towards manufacturing facilities.

- The company had settled the litigation process towards its launch of Revlimid during March, 2022.

- Its marketing partner Breckenridge Pharmaceutical Inc. had received approval for the abbreviated new drug application (ANDA) for Pomalidomide capsules from the USFDA, and both the companies had settled litigation for the filing approval.

- The marketing partner which sells Pomalyst in the USA market for specific cancer treatment had a sale of ~$1 billion during the year.

- The retail business had performed better in Brazil and Canada as compared to USA.

- The other expenses were ₹207.2 crore which increased during the quarter on account of Remdesivir launch in USA and the company incurred this as a one-time expense and expects it to normalise during the upcoming quarters.

Disc: Invested in Core PF.

PIDILITE:

Concall Summary dated 6th Nov 2020

Revenue: ₹1,880.3 cr (▲4.1%) Net Profit: ₹356.4 cr (▲9.7%)

FINANCIAL PERFORMANCE

- The revenue from operations was ₹1,880.3 crore in Q2 FY21 as against ₹1,806.6 crore in Q2 FY20, an increase of 4.1% YoY.

- The net profit grew by 9.7% YoY to ₹356.4 crore in Q2 FY21 from ₹325.0 crore.

- Export revenue was ₹695 crore during the year.

- EBITDA (before non-operating income) was ₹514 crore, which grew by 39.3% YoY.

OPERATING PERFORMANCE

- The company’s plants are running at a capacity utilisation of 90%.

- The material cost as a percentage to net sales was lower by 226 bps YoY. Its major raw material vinyl acetate monomer (VAM) had reached ~$900/tonne. During Q2, the prices were $765/tonne and the spot prices has now increased to $900. The company expects the prices to increase further due to availability constraint.

- The net sales grew by 3.4% YoY. The international subsidiaries had a double digit growth while the domestic business witnessed challenges due to pandemic and signs of revival is observed for the latter part of the quarter.

- The company’s sales had been largely impacted in the real estate segment whereas the small semi-urban markets (artisan, construction and non-wood business) are picking-up well. Its products were utilised towards construction business for Jammu and Kashmir tunnels.

- It is planning to emphasize on advertisement and commercial spends to drive sales and volumes for the coming months.

- It more than doubled its online penetration in a year, revenue being generated from customer and bazaar segment.

- The company witnesses no competition from paint brands in water-proofing segment, as the company has a strong brand market share in this segment.

- The overall market is growing at 1-1.5 times of GDP (excluding Covid phase).

BUSINESS PERFORMANCE

- The overseas subsidiaries sales during the quarter was as follows: ₹87 crore from Asia, ₹119.1 crore from America, ₹65 crore from Middle East & Africa. The revenue from overall subsidiaries was ₹575 crore.

- The domestic subsidiaries sales comprises of: Nina Percept Private Limited which de-grew by 35.5%, ICA Pidilite Private Limited grew by 1.1%, Cipy Polyurthane Private Limited declined by 24.2% and other subsidiaries grew by 59.9%.

- Its product portfolio comprising of adhesives and sealants, construction and paint chemicals and art and craft materials has 79.9% sales from C&B products. The industrial adhesives, industrial resins and constructions, and pigments & preparations has 18.7% sale from B2B products and rest 1.4% from other segments.

HAMSPL ACQUISITION

- The company has completed the acquisition of 100% stake in Huntsman Advanced Materials Solutions Private Limited (HAMSPL) for ₹2,100 crore on November 3, 2020. Huntsman sells adhesives and sealants under brands such as Araldite, Araldite Karpenter and Araseal.

- The acquired business (HAMSPL) is a profitable business with strong leadership and distribution channels. It has miniscule amount of fixed assets, as the assets are through tolling arrangements and are done on the basis of cost conversion route.

- The acquisition was funded through the liquidation of the company’s treasury business.

- The transaction value was 90% upfront payment and the balance 10% in 18 months, on deferred consideration through mutual consent between both the companies based on the condition of certain revenue achievement in the coming 6 months due to uncertainty in markets.

- Pidilite Industries has a current plan of reflecting the acquired business as investment proceeds in its financial statement and run it as an independent entity.

- The strategy of Pidilite would be to enhance its portfolio brand through this acquisition and increase its footprints through distribution channels and accelerate its revenue through it. There would be a cost and revenue synergy from the acquired business as the product category is already known by the parent company.

- The acquisition includes the trademark license for Middle East, Africa and ASEAN countries.

CAPITAL EXPENDITURE

- The company plans to operate at a capex of 4%-5% of revenue.

- There would be no differential spend on capex. It has 9 plants which are in work-in-progress phase and there would be no extra spending on capex towards these plants beyond that range.

Disc: Invested in Core PF.

1 Like

RELAXO:

Concall Summary dated 2nd Nov 2020

Revenue: ₹575.9 cr (▼7.4%) Net Profit: ₹75.1 cr (▲6.5%)

FINANCIAL PERFORMANCE

- Revenue from operations in Q2 was lower than previous year by 7.38% at ₹575.87 crore. The decline in operating revenue was due to the drop in economic activity because of the pandemic.

- Net profit in Q2 FY21 increased to ₹75.10 crore as compared to ₹70.54 in Q2 FY20. Profit after tax (PAT) margin stood at 13%.

- Profit before tax (PBT) was higher than previous year by 35% at ~₹100 crore. PBT margin was 17.4%.

- EBITDA margin improved to 22% in Q2 FY21 v/s 16.8% in Q2 FY20 on the back of reduced administrative expenses and benign raw material prices.

- Other income stood at ₹5.04 crore.

- For H1 FY21, EBITDA margin came in at 19.6% v/s 16.6% last year. PAT margin was 10.6%.

DEMAND SCENARIO

- Demand saw a volume growth of 2% YoY in Q2 FY21. Volume growth in H1 was -13% YoY.

- The demand from rural regions was higher than that of urban regions.

- The south and west regions were most impacted as Mumbai reopened late from the lockdown and parts of Kerala are still under lockdown. The demand here has de-grown.

- Even in the festive season during October, demand picked up across the season except in Kerala.

- The demand and production gap still persists in the open footwear category as the demand quickly escalated but it took time for the production levels to ramp up.

- Exports demand is similar to domestic demand after Covid-19. The focus is on the major market of Gulf region. A good traction is seen in the important international markets of Africa, Gulf, Central America and Oceania.

- The company always has a capacity cushion of 30%-40% to cater to the additional demand.

PRODUCT PROFILE

- The open footwear category has shown good traction in the quarter with the brands Hawai, Flite and Bahamas performing well. A major reason for this is the work from home practice due to which the demand for formal footwear declined.

- Open footwear has a revenue share of 80% at present. The closed footwear forms 10% of the product profile in volume terms and 20% in value terms.

- The canvas shoe category has not grown. Shoe as a category forms 10% of the overall portfolio.

- Sparx as a brand has seen recovery in Q2 but it remains far from the pre-Covid levels.

- No demand has been observed for school shoes yet.

DISTRIBUTION NETWORK

- The company as on 30 September, 2020 had 396 exclusive brand outlets (EBOs) which contributed 5% to the revenues in H1 FY21. It made 6 new store additions in the quarter.

- The EBOs are display-cum-sale counters established to capture the needs and preferences of the customers. The company has no plans of increasing such outlets (despite it being non-existent in the southern region of the country).

- E-commerce has a share of 10% in revenue. It is expected to increase further by 2% in the next 6 months.

- The number of channel trades and distributors remain same post-Covid while it is being estimated that some dealers might have shut down, especially in the north and south.

- The number of dealers and distributors has increased as the demand for open footwear across the country saw growth.

- The amount of security has been revised for both new and existing dealers to bring in more serious players. The implementation of the same was due in April but got postponed to June due to the pandemic.

- The supply time from the company to the distributors remains at 2-3 days on a regular basis. The distributors have been requested to maintain an inventory of 1 month at all times.

- The same level of margin is provided to both channel trade and e-commerce.

FUTURE OUTLOOK

- EBITDA margin shall not be the same as Q2 in the upcoming quarters as the expenses return to normal levels. However, on a YoY basis, the margin is expected to be better in the upcoming quarters.

- At the company level, a volume growth of 3%-4% is expected in H2 FY21.

- The capex for the year shall be in line with that of every year at around ₹100 crore with an eye on capacity expansion.

- The objective shall be to recover the loss of Q1 in terms of turnover and growth over the next year. Over the longer horizon, a double digit growth is expected.

- Rising raw material prices can be a trouble going forward.

- The management forecasts that the demand for slippers and open footwear shall remain strong in the next 2-3 years due to the adoption of work from home culture post Covid-19 pandemic.

- It will continue to focus on growing presence in the untapped and under-penetrated markets along with focusing on strengthening the brand.

Disc: Invested in Core PF.

3 Likes

In investing field especially in the case of stock market, most of the statements made by people has powerful content has meaningful context which is privy to himself. The followers of such statement when acted upon fall into trap more often because while the content was highly influencing but the relevant context was missing.

The less the homework done by retail investor more will be the pain compounding with time. The regret of underperformance will be so high that retail investor make more mistakes by being aggressively careless in order to compensate his apparent loss. More the returns are chased the sooner they find themselves blown out by couple of years atleast.

Bet is important but slow and staggered and diversified approach is only way forward for retail investors. I am of the camp who believes more on risk than returns.

Lesser the standard deviation and higher the mean is what gives ultimate edge to people with smaller funds.

6 Likes

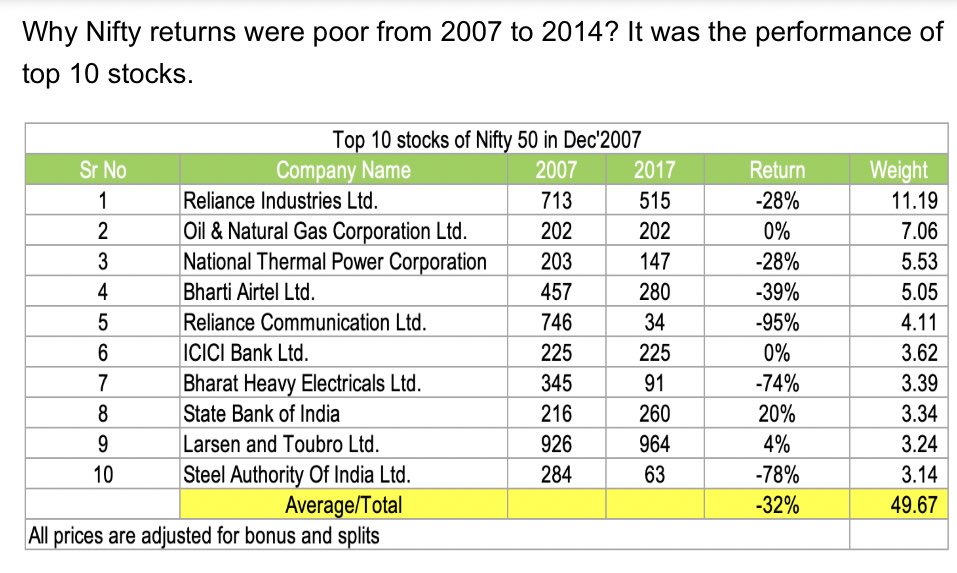

Why not hold the index instead?

Tcs and Infosys can be replaced by Larsen and tourbo

Relaxo,Divi,Asian paints,Bajaj finance are good choices

@Amritasen22 Thanks for your feedback.

I hold more than index in my pf

IMO in last 15 years of my investing I have seen that L&T is always replaceable by TCS anyday.

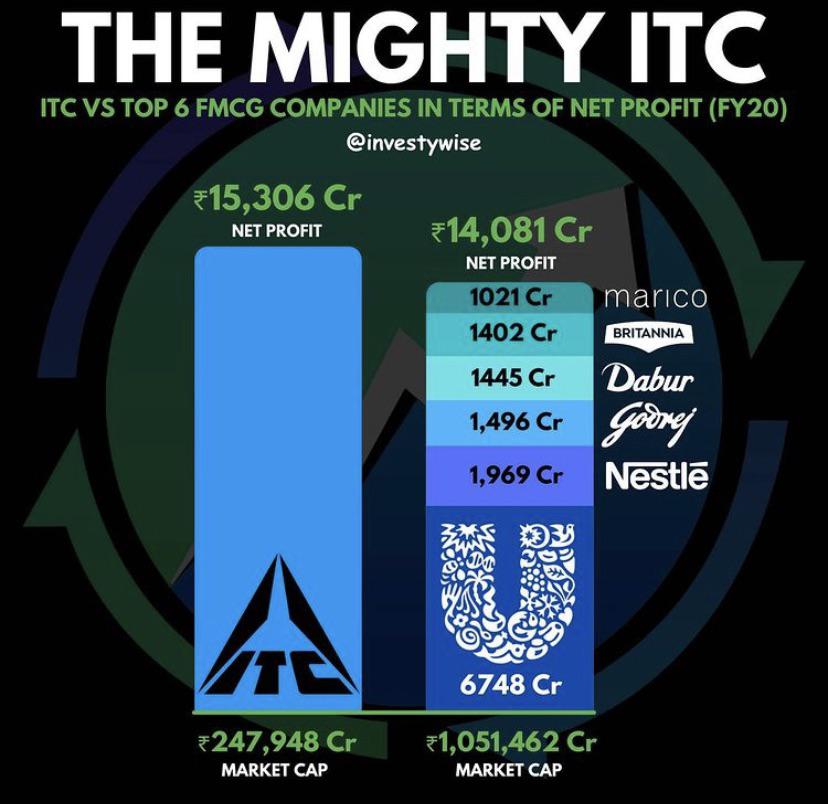

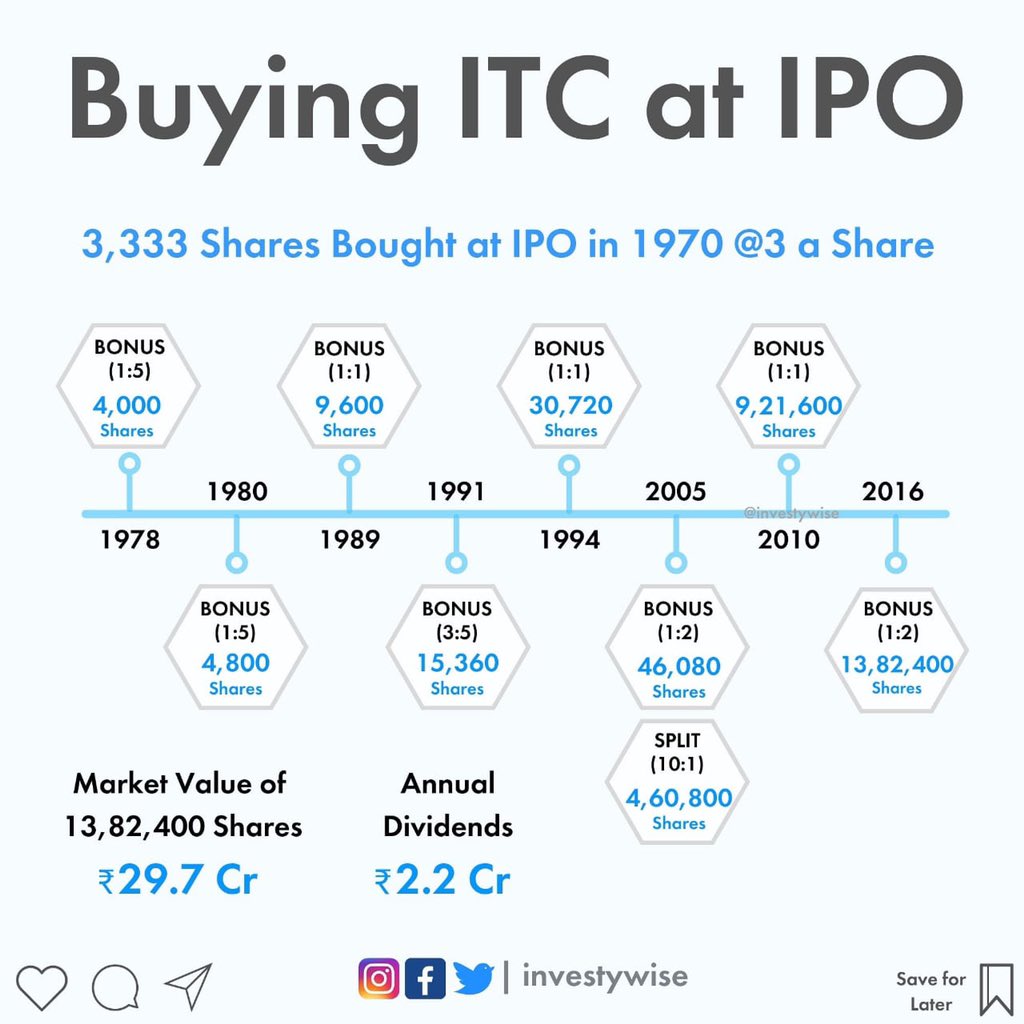

One more company which I admired a lot is ITC because of its giant moat but sadly it is not yielding satisfactory returns for many recent buyers of last 5 years. The problem with ITC in my opinion is more of a lack of promoter control and hence divided focus. The current management team after demise of its chairman is more comfortable with bonus, incentives and dividend.

Disc: invested in all names as mentioned in super long term PF.

4 Likes

Some reader has asked privately my view on ITC.

Regarding my view I already written on my thread about ITC. I am holding it since 2004  with long term cagr better than superstar MF of those Era.

with long term cagr better than superstar MF of those Era.

My expectations is different from majority. I am invested here for capital preservation for next atleast 30 years because this will not go bankrupt nor any greedy promoter is there to siphon the fund.

It is much better than Yes, laxmivilas, DHFL, ILFS, recap, relcomm, penny stocks,… lists are many

I am happily invested in itc as am happily married

6 Likes

Great to see real long term investing in practice, many just speak but admire those who practice. Nothing dwindled your faith in between ups & downs because you knew exactly what you were doing!! Respect! You are already on a 10 bagger in a stock which is battered at rock bottom since last 5 years (not to mention the huge dividends that may have already recovered most of the investment cost)…and when it start rising…in few years or decade, you may very well make a 100 bagger if you still hold it!! Happy to see your conviction & execution!!

Disc: Invested in ITC hence biased. Admire long term investors and wish to learn from their immense experiences!!

9 Likes

@Investor_No_1 Thanks for your kind words.

It is about learning the process along the way is more important than outcome especially in early days of career. It is an art and equally the science of nitty gritty of stock investing, portfolio construct, buying as well as selling. It will bring the real character inside out.

Patience, diversification, quality and staggered bets matter a lot along the way. There aren’t shortcut in this field. Oflate I am getting amazing results because of extensive study, research, analysis and patience.

Happy investing.

1 Like

Since you are investing for 15 years can you tell me your cagr?

@Amritasen22

Sure. Let me pull the latest performance report and will post shortly.

But before that I want to mention that though cagr return is important metric to measure but is not everything if you are falling short of your set goals. I am benchmarking against my retirement goals that how near or far I am. As it stands currently I am more than half way mark in achieving my target corpus for retirement and I hope to meet that in coming 4-5 years timeframe from now with reasonable confidence of 95%. I am maintaining Equity:Debt ratio of 60:40 with 10% of allowed variation either way.

5 Likes