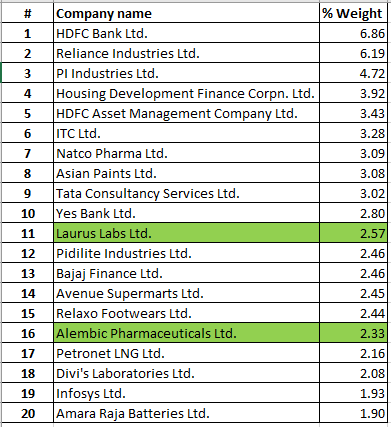

Top 20 Holdings:

Two new stocks in the portfolio from Pharma sector - Laurus and Alembic. Incremental capital allocated to HDFC pack, ITC and PI in the month of September during fall.