This quarter results seem pretty bad, compression on both topline and bottom line. Could be attributed china lockdowns ?

Do you know why the company needs bank guarantee by promoters, and then pays commission to promoters for the same. Given the cash flows and current leverage, it seems external bank guarantee is not required

1 Like

Do we know why the OPM% has been decreasing since June 2019.

Has the product mix that is sold changing which could impact the margins or is it to do with increase in RM?

1 Like

Thesis is working out, clear that trading business revenue has come down which was affecting operating cash flow. Manufacturing demand does not seem to be hit as such, degrowth in revenues is due to trading biz coming down.

OCF as of March 22 was -23cr

OCF 6 monthly as of Sept 22 result is at 50 cr!

Further triggers of capex will play out in coming quarters.

2 Likes

Why are both revenue and margins down?wouldnt reduction in trading buisness lead to margin improvements and any source for your thesis?

Hi. My team has released a report on this which I have attached as a pdf two posts previously in this thread. There are clear inflationary issues most co’s are facing globally so it’s but obvious margins won’t be the same YoY. Compare it to Dynemic , their margins are wrecked. Vidhi has maintained margins over last few quarters, shows good market pricing power. And capacity is doubling, we will see effects in coming quarters and better cash flow metrics will further re rate the stock

5 Likes

Q3 FY24 Update:

The discussion has been dormant. So kicking this off.

Chemical Sector:

The chemical sector across India has been suffering due to a downturn in the industry. The demand slump caused by inventory destocking, the Red Sea crisis, higher inflation worldwide and Europe’s issues added to the list of problems.

During this downturn, many chemical companies have taken the opportunity to scale up their operations and undergo Capex. Going through different chemical company reports, I can sense that the sector headwinds are almost over and demand recovery is foreseeable in FY25, as evidenced by larger diversified companies like Aarti Industries in their concall.

Company Q3 FY24 Update:

The effect of the recovery is yet to be seen in the quarterly reports. Sales figures are still on a downtrend with QoQ and YoY degrowth of -21% and -27% respectively. However, margins (OPM & NPM) are expanding. Overall, a dull quarter on the top line and flattish on the operating level and bottom line.

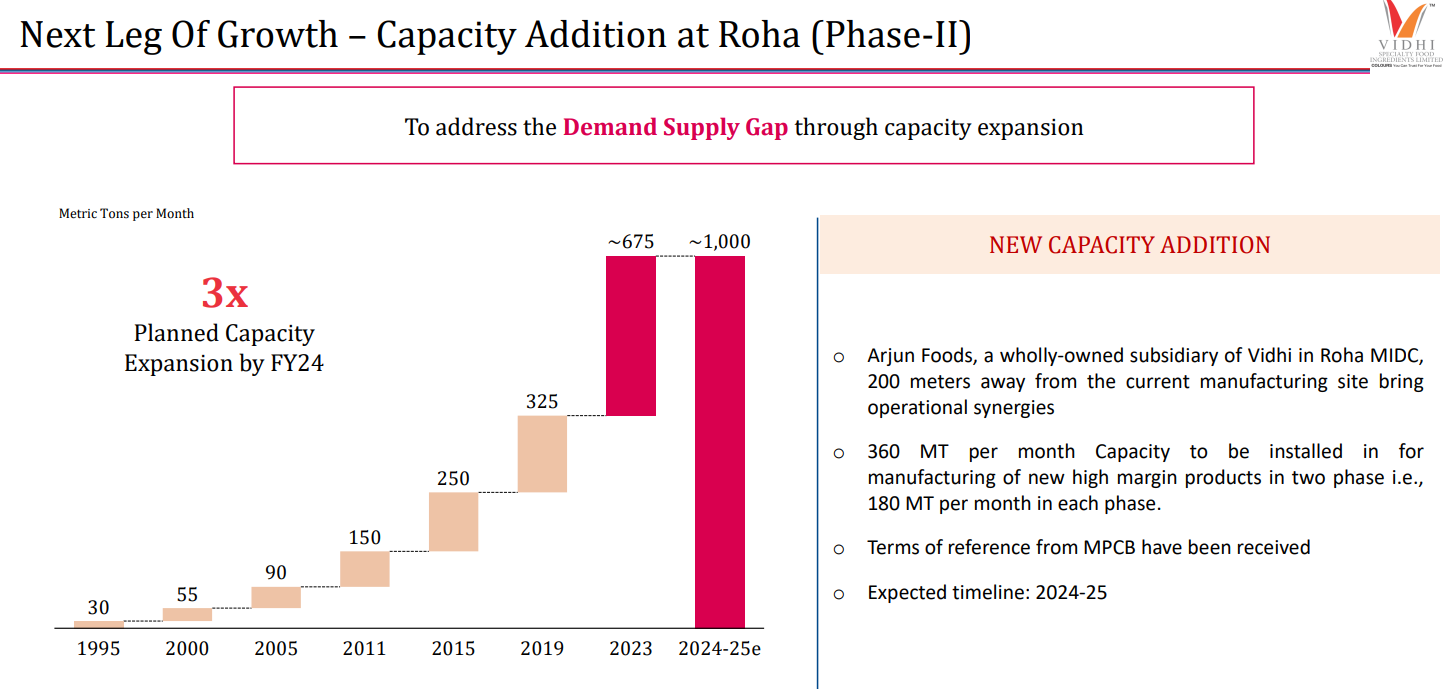

Growth Drivers: Expansion

Despite most chemical sectors facing deep cuts in their stock price, Vidhi has consolidated since Oct 21(Q2 FY22). This is most likely because of the future growth that the company is investing in.

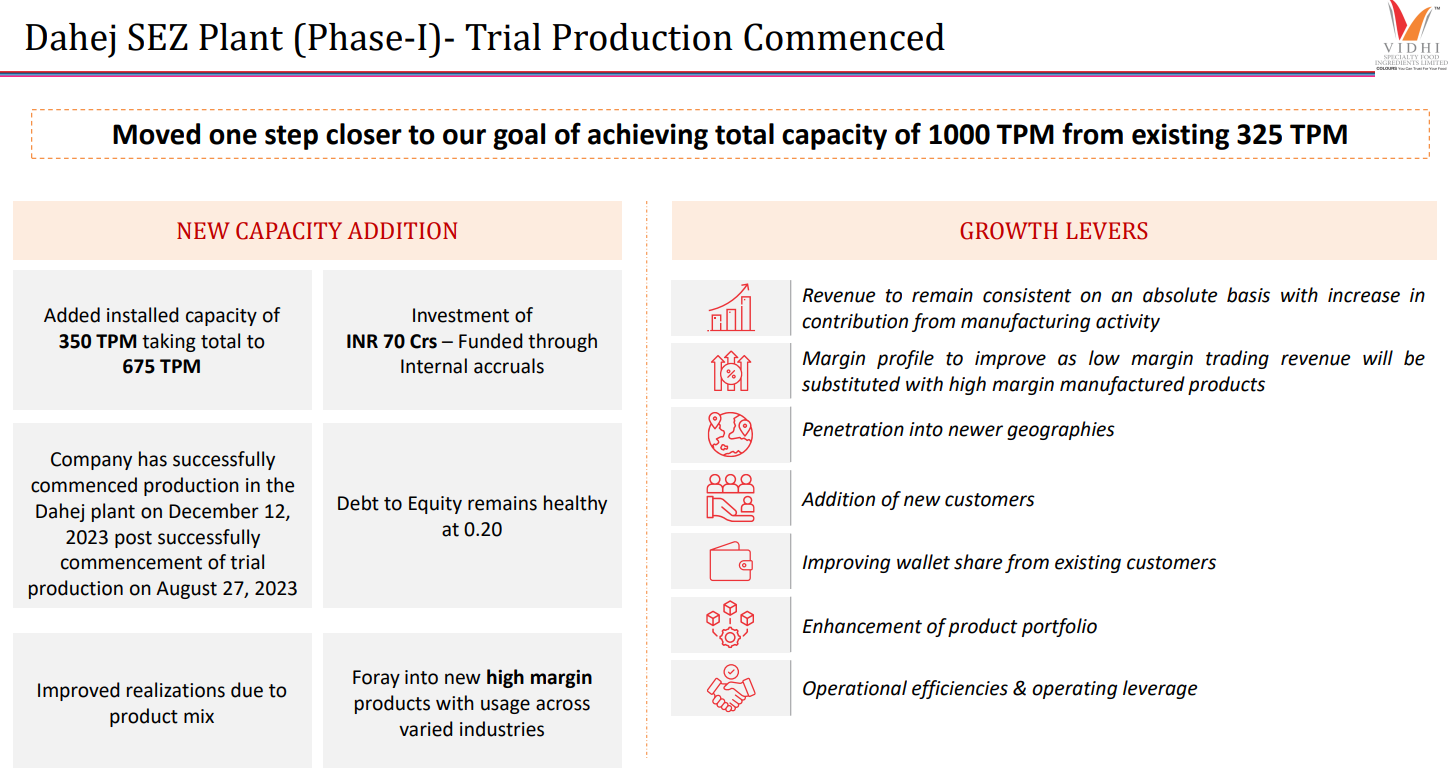

The 1st Phase of the Capex has come online and should contribute to sales in the coming quarters.

The Global Food Colour Market (2021-2026) is expected to grow at a CAGR of 4.7% and the emerging food colour market is growing faster at 6%. Incremental demand to be expected Y-o-Y basis in the global food colour industry at 1500-1700 Crs.

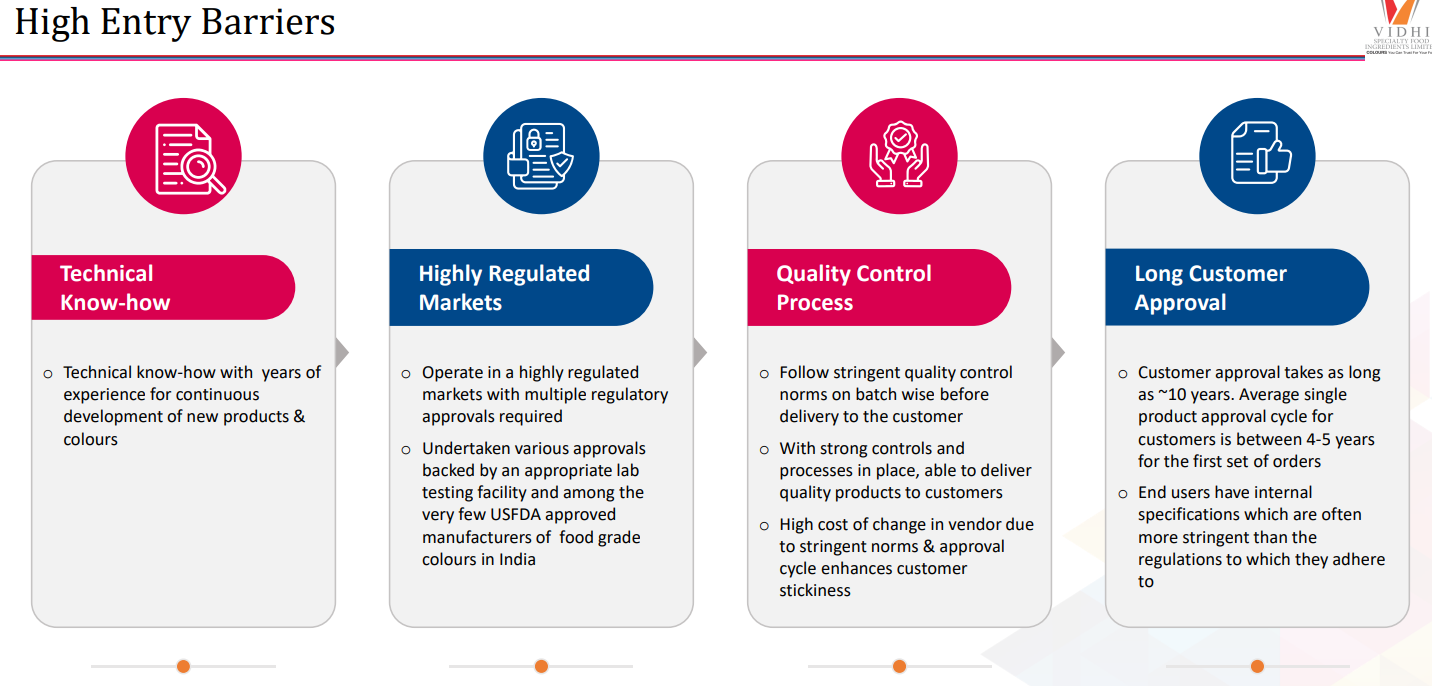

There’s limited competition with a few players: Camlin Fine and a few others who derive a small % of revenues from this business. There are high entry barriers in the food colour industry due to stringent compliance and approval timelines. It’s the 2nd Largest food colour manufacturer in Asia, with an existing Capacity of over 3,500 MT p.a. with ~8,500 MT p.a. under expansion.

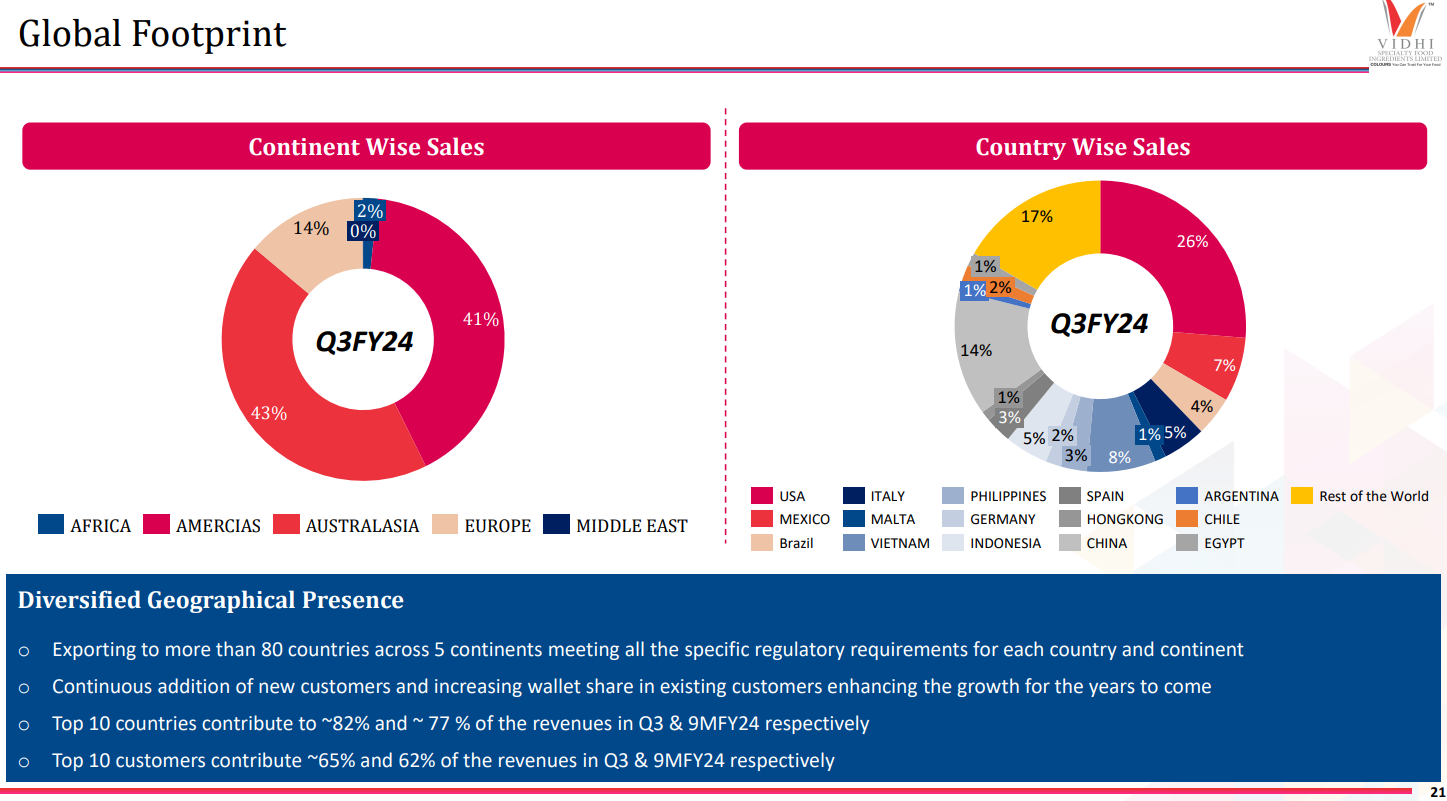

The company sales are 5% domestic & 95% export. Well diversified across geographies & client base and has a smaller portion of the portfolio exposed to Europe.

Expectations:

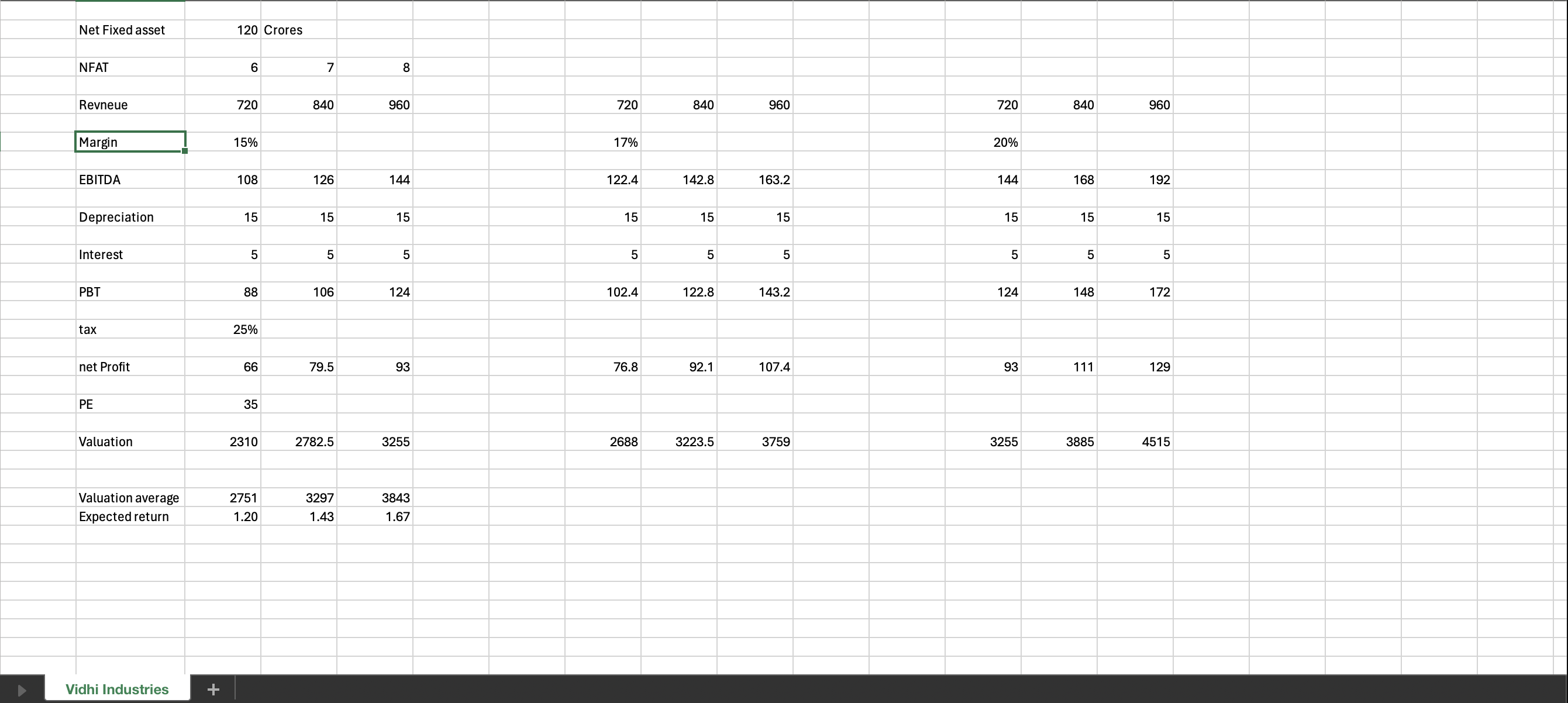

With no CWIP present on the balance sheet as of (March 2024, Q3 FY24), all capex of phase 1 has been operationalised. Assuming a Net Fixed Asset Turn(NFAT) of 8 (5 yr Avg) on 121 Crs of NFA gives me a sales jump of ~3x. A conservative 12% NPM gives a ~3.3x jump in earnings (PAT).

If valuations(P/B) rerate on the higher side returns will be more lucrative.

The stock has been sideways for a long time with good growth triggers for the upside.

Disc: Please do your own Research. Not a Buy/Sell recommendation. Have taken conservative figures for the calculation, so upside surprise has a higher probability.

More importantly, their trading revenue must have become minuscule now as they are focusing on manufacturing based revenue. Wanted to know the latest sales mix. FY23 topline was very high due to trading revenue.

Disclosure- recommended and invested since 385

1 Like

The current valuation seem to have factored in the base case of 6x NFAT turnover and 12% margin (from manufacturing revenue) at 35x PE (historical 5 year average) at an EBITDA margin of 15% (a bit conservative while management is guiding higher margin)

Key valuation drivers are higher NFAT (7x or above) and margin expansion (17 - 20%)

Please note, I have excluded the trading revenues while arriving at NFAT turnover.

2 Likes

Very good results posted by vidhi.

I think dye and pigment industries is recovering after long time.

2 Likes