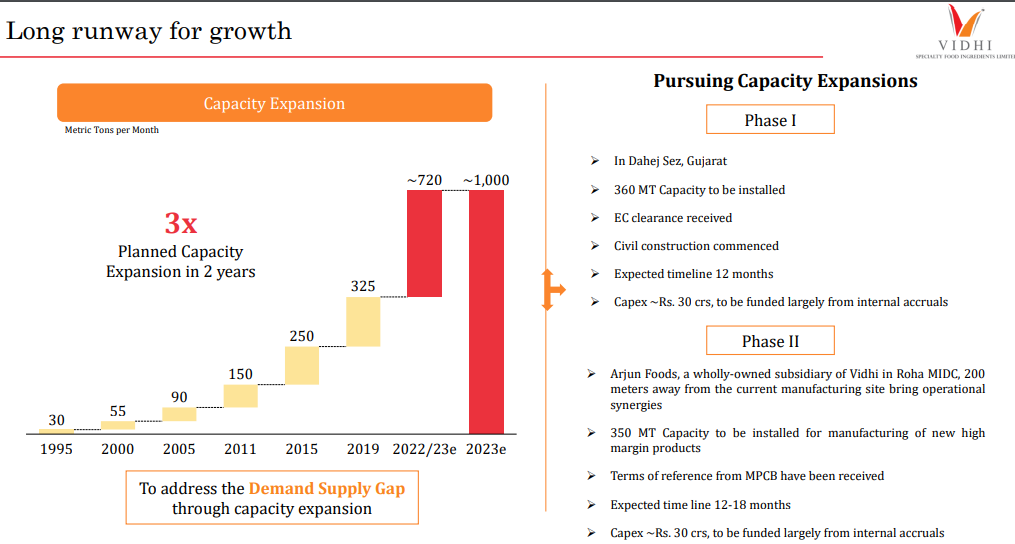

Company received Environmental clearance certificate for new plant in gujarat.

4 Likes

When is the new plant likely to start production?

Can anyone please share AGM recordings or notes/summary?

FY20 online AGM notes

Operations:

-

Demand: Extremely robust- all time high demand. Hence, undergoing CAPEX plans at two facilities. No impact of COVID-19

-

China was never into manufacturing of food colors, in-fact it is one of the largest importer

-

Competition: Roha is doing CAPEX in pigments and industrial dyes and so, no direct threat. Considers Dynemic to not be a competitor

-

Visibility: Demand is already there from existing clients and marketing won’t be an issue

-

Natural food color: Global leaders in this segment like Chr-Hansen are facing de-growth from past couple of years. They are also looking to sell off their natural food color segment.

-

Marketing: Attends many international exhibition and adds distributors under our company whenever opportunity arises

-

Domestic markets: Peers like Roha dyechem and Neelikon are serving domestic markets. Other small players. Vidhi is also supplying to ice cream manufacturer

-

Almost 60% of RM requirement are imported from China. No ADD on such RM would hamper our co’s margins because we have adequate licenses. All such RMs are available locally at incremental cost of 3-5%

CAPEX:

-

EC approval: Dahej very soon expected and Roha may take couple of months

-

Commercial production: Depends on EC. Once EC is obtained, Dahej expects to start within 15-18 months and at Roha expects to start within 8-10 months

-

Revenue potential: Total CAPEX outlay is Rs.90 Crores. Post CAPEX, co’s topline is expected to be 700 Crore at full utilization (remember couple of years back management gave a press release wherein they targeted 500 Cr topline by FY20 but that didn’t happen until now)

-

Backward integration: Currently producing 2 RM, after capex will make more RM

-

RM includes many dye intermediates and basic commodity chemicals. Total of 4 Key dye intermediates will be manufactured by the co. Commodity chemicals can’t be manufactured in house

Financials:

-

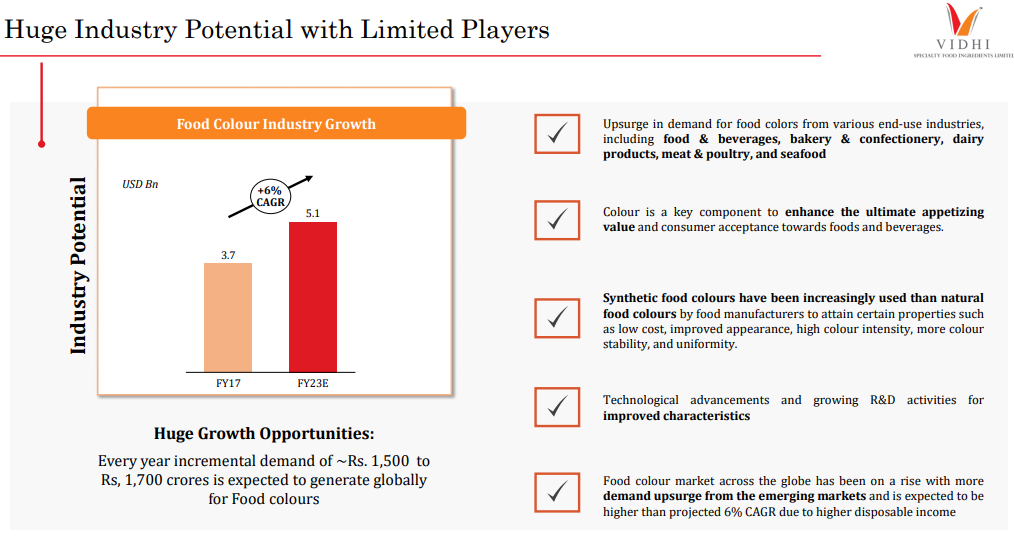

Synthetic food color: 45,000 MT market growing annually at 5%

-

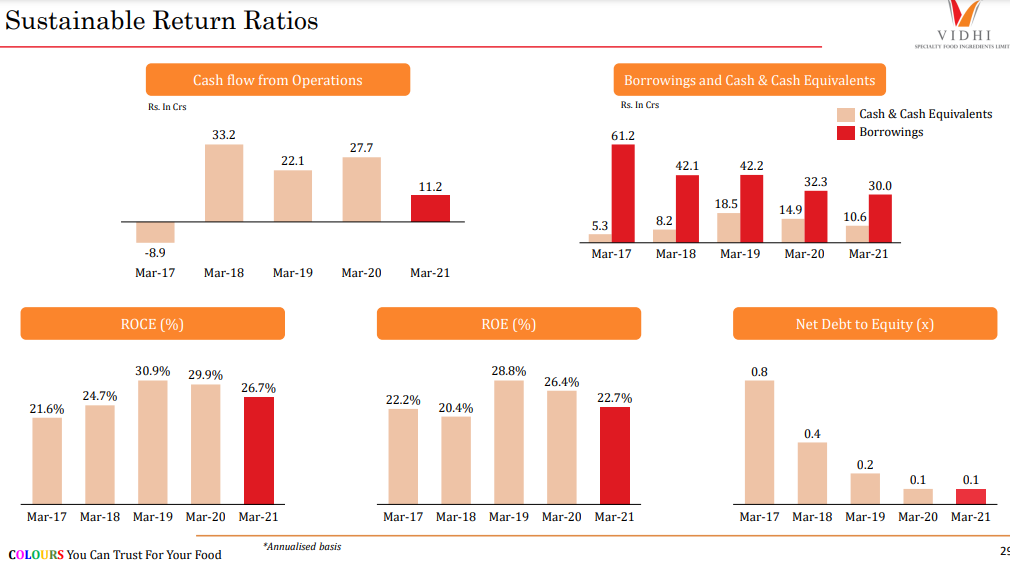

Margins are increasing due to enhancing and improving product mix, reducing down time and debottlenecking done in 2016, focus on quality conscious markets

-

Over 200 active customers over 80 countries. No dependence on any individual customers

-

Export incentives will continue, just scheme would be different

-

Since 2016, we are trying to reduce trading revenue relative to manufacturing revenue. Trading margins are around 4-5%

-

“Our operating margins are not volatile, they are in straight upward direction”

-

“After ramp-up of new CAPEX, confident of posting operating margins north of 24%, primarily because of inclusion of R&D driven products”

11 Likes

June 2022 (conservatively) as per management commentary. It is also worth mentioning that Dynemic is a competitor which got a similar EC in Dahej plant in Sep’18 and the plant is expected to start producing by April 2021. So that is a delay of 2.5 years.

Does anyone know why they don’t consider Dynemic to be a competitor? Both seem to be into food colors. Even this MoneyControl article seems to say that they are food color competitors

Disc: No investments to date, studying dynemic and vidhi

1 Like

Good results from vidhi:

Topline grew by 46% & EPS by 35%.

The reason that the topline grew faster than bottomline is that the cost of inputs (Raw material + stock in trade) grew by 58%. This could be due to a mismatch between prices of inputs and outputs (products manufactured when input costs were high being sold in this Q when output prices were not that high).

Disc: Invested in competitor Dynemic products

3 Likes

Hi Sahil, was researching Dynemic Products, came to Vidhi’s chain to understand the industry better and saw your posts here. May I ask your rationale behind investing in Dynemic as opposed to Vidhi? Is it cause it was available at a better valuation, the capex will make the company bigger than Vidhi etc?

Thanks in advance.

1 Like

Vidhi Specialty Investor’s Presentation

2 Likes

Question on this - How can 60crore CAPEX(30+30) produce 700cr of additional revenues?

Because Vidhi is not just a company, it is “An Institution in Edible Colour Technology” as per the presentation

6 Likes

its not about revenue 700 cr . its capacity addition 700MT… 1000MT…

, this proves there net proft margin > 10% , consistent growth, internal accrual capex, and long lasting client.

Why the promoter himself try to create unnecessary volume surge so that people take it to notice , what does that mean , expert plz explain

Did you find an answer to this? On 3500 MTPA capacity company produces ~30cr net profit. On 30cr additional capex they would produce ~40cr profit, payback period of less than a year on capex. Is their moat actually that strong?

3 Likes

Vidhi specialty - AGM Notes

Products demand

- The demand for the company’s product is at all time high and customer lead time is 2-3 months.

- To address the robust demand for its products, company has announced 2 expansions (Dahej & Roha).

- Growth in revenue will be by penetration in new geography and new addition to customers.

- Expected incremental demand for food colors is around 1500-1700 Crs globally.

- Management said that MNCs demand for its product is too high but currently company do not have capacity so doing capex.

- Two big manufacturers of food colors in US are degrowing and Indian players are increasing market share.

- Company expects its margin will also improve in next 2-3 years.

Dahej expansion update

- will be at full capacity utilization immediately once the plant become operational.

- Plant will start becoming operational by 1st Quarter of FY22.

- This plant will be basically used for Synthetic food colors (Finished goods).

- Plant capacity will be around 4320 MT PA and the total capex for this plant is 30 Cr.

- Currently CWIP for this plant is 9 Crs.

Roha expansion update (Arjun foods)

- Management expects to receive environment clearance certificate soon.

- This plant will take at least 1 Year to come at 100% capacity utilization.

- At Roha plant, company will introduce new products and few special products and high margins products.

- Management expects operating margin will improve more once this plant gets operational.

- Plant capacity will be around 4200 MT PA and total capex will be roughly 30 Cr.

- Currently CWIP for this plant is around 14 Crs.

- Company has spent total 23 Crs as of now out of 60 Crs capex and remaining 37 Crs will be also utilized from internal accrual only.

- Company has also option for 20 Crs term loan facility from bank, if needed.

- Management expects there will be some impact on capex due to rise in the prices of still & cement.

Dividend Yield

Company is currently not increasing dividend payout as there is planned capex which will funded from internal accruals.

Asset Turnover

- Management has said that asset turnover of 7-8X is possible after the capex gets complete which means we can expect topline of nearly 700 Crs.

- Current Asset turnover is also around 8X.

Synthetic colors vs Natural colors

- Natural colors are very expensive and it is very difficult to use so management expects synthetic colors will be large market as compared to natural colors.

Trading sales

- Trading sales for this FY was 31% as compared to 15% in FY20.

- Trading sales margins are around 7-8% only.

- Trading sales will be lower once the Dahej plant gets operational.

- Margins will also improve as the trading sales as a % of total sales will decrease.

China Impact

Management said our company currently supplier to China for food colors and they do not expect any competition from China in food colors business.

Disclaimer – Invested.

13 Likes

Devis,

Thanks for the notes. I wanted to understand the sales projection given by Vidhi. Y’day Dynemic gave the volumes for FY21 and based on that one member has calculated average pricing of INR 4700-4800 per KG for FC. If we apply the same realization on Vidhi, then from 300 MT per month of capacity in Dahej, maximum sales that is possible is ~180 crs. Roha will also generate same sales of 180 crs. Existing sales of another 180 crs. Put together ~540-550 crs. From where they will generate 700-800 crs of sales? Unless they intend to fill this gap from trading sales, I believe these are highly inflated estimates.

Thanks,

Disclaimer - no investment.

My bad in putting realization. It is INR 470-480 per KG, and not INR 4700-4800 per KG.

going by last 2 quarters topline on an average 100 cr per quarter giving them a topline of 400 cr per year this is on fixed assets of 30cr and current capex planned is of 60 cr so a topline of 700 to 800 cr doesn’t look to optimistic .