Vidhi Dyestuffs Manufacturing Ltd. (VDML) is the third largest manufacturer of synthetic food colours globally with a capacity of 4200 MTPA. It is among the very few USFDA approved manufacturers of food grade colours in India. Over the last 20 years, the company has established strong relationships with global majors like Mars, Pedigree and Sanofi among others. The company has been able to grow its revenues substantially by 21% CAGR over the last five years, while the industry has witnessed a growth of 4-5%. Going forward, the company’s investments in capacity addition and reduction in its low margin trading business would help it achieve its targeted margins of 20% plus over the next 4-5 years. Following is Transcript of our Meet with the Management.

What are the entry barriers in our business? How strong is the customer stickiness for a seemingly commodity product?

Ans: Switching suppliers is a big hassle for clients as colour component is very small (colour comprises of ~0.5% of the cost of the final product). We have spent 20 years carefully establishing relationship with clients and distributors across 80 countries.

Is our business a commodity business? Are there any risks to our business?

Ans: ‘You may keep a halt on buying Ferrari during recession, but what about strawberry cream biscuits and flavoured chocolates?’ More than 95% of our manufacturing revenues are from exports thus exposing us to currency risks but apart from that none.

Who are our direct competitors?

Ans: Due to a small overall market size of synthetic food colours, there are only four major players worldwide. Sensient Technologies (20,000 MTPA), Roha Dyechem (9000 MTPA), we are the third largest manufacturers with 4,200 MTPA, Emreld USA (2,200 MTPA). No competition from china as market size is too low for them (40k MTPA, growing at 5%).

Where is Sensient focusing given it is losing its market share in synthetic food colours? Sensient’s website suggests increased focus on natural food colours, how strong is the shift in trend? What is the natural vs synthetic dilemma all about?

Ans: First it is a myth that Synthetic colours are harmful. Natural flavours have less variety in terms of colour and only premium products are using it. There is no apparent trend shift towards natural colours and it is just a propaganda. We are selling our product 25% cheaper than the world leader Sensient and thus gradually taking their market share.

What is our expansion plan and how are we planning to fund the upcoming expansion?

Ans: We are aiming at capacity of around 8,400 MTPA by 2020, capturing around 20% of market share. We are just waiting for environmental clearance to start with the incremental capacity addition. Mix of internal accruals and debt will be used for the same, around 60:40 ratio.

Why the decision to stop trading and cause a de growth in the coming year as the new capacity will take time to ramp up?

Ans: Trading is a high capital and a low return business and thus we will discontinue it from the next month onwards. Trading is ruining our balance sheet and we rather use that WC for manufacturing. We are running at almost full capacity and want to focus on high margin manufacturing business.

Is there any pricing differential in our product and Roha Dyechem? Will get any benefit in terms of lower raw material price with recent fall in crude oil price?

Ans: There is none and we don’t touch their customers and nor they touch ours. Yes some of the benefit we will pass to the customer but some we will keep for us.

Can Sensient buy us out in coming years? Will we be open for it?

Ans: Yes, if they have an ‘offer which we can’t refuse’ !

Are we looking to enter in the Naturals arena? Do we have any presence in that segment? Apart from that do we have any other opportunity to expand?

Ans: Yes, we are developing one colour at a time in natural segment. So far we have developed couple of natural colours and we are the sole manufacturers for one of the colour. Apart from Natural we have the Pigment market of 15k Crore to explore in future. So market opportunity is there.

Where do we see ourselves in 2020? What is the vision?

Ans: Over Rs. 500 Cr. in top line with 20% OPMs, Capacity of around 8,400 MTPA.

What dividend policy have we decided?

Ans: As discussed in the last AGM, we will continue to distribute 20% of the Earnings.

Thanks for the management meet updates. It is very useful. Especially, the answer to Sensient buying out VDSL was very interesting!!

If the management’s vision plays out, it looks like a very interesting bet. However, there is one big “If”. We, as an investor, must assess the odds of management’s vision turning into reality. I did some number crunching and few inferences base on the same

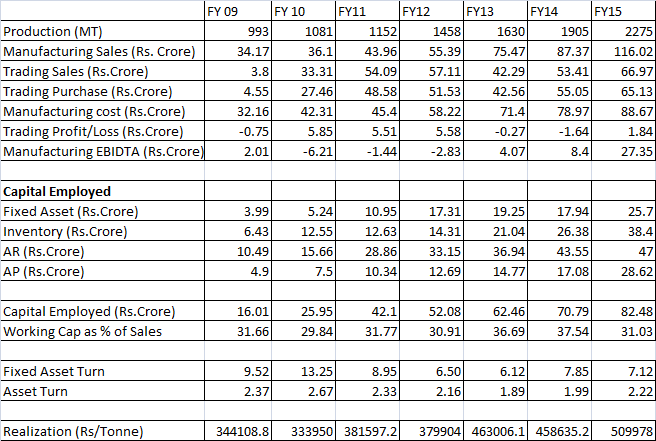

Company is currently making a loss in its trading activities thus reduction in trading revenue as % of sales will improve margins. However, it is important to note that in the past, company made EBIDTA losses for manufactured product also.

For the manufactured product, company’s margin have increased consistently over last 3 years from 7% to 10% and this year it has increased to 23%. Thus, it is possible to improve margins from here on if the manufacturing/trading ratio changes in future.

Company’s working capital cycle has remained stable despite growing at 25% CAGR which indicates that company is managing it’s capital well.

Realizations have improved at 7-8% CAGR over last 6 years from 3.44 lakhs/ton to 5.09 lakhs/ton . However, a part of realization improvement has come from rupee depreciation. Thus, in constant currency terms, the realization may have only increased marginally.

Company has grown consistently over last 6 years(25% CAGR) with managing its balance sheet well thus there is a fair chance that in future, company will be able to grow without impacting the balance sheet quality.

Sansient, makes around 20-22% EBIDTA margins in spite of operating in high cost countries, thus 20% EBIDTA margin seems achievable for Vidhi.

It is an asset light business, and fixed asset turns are very high (due to high value product) thus any improvement in margin combined with asset light business, can fetch very decent ROCE. In fact, ROCE can increase beyond 25%, if company is able to achieve 20% EBIDTA margins.

After looking at competitors like ROHA and Sensient, I too come to same conclusion that it is a industry dominated by few large players and business is growing for companies like Roha and Vidhi as companies like Sensient are forced to look at natural colors due to their existing clients demanding the same. At the same time, I also got an impression that there exist a slow but sure shift from synthetic color to natural colors (even though, as management rightly pointed out, there is no evidence of synthetic color being harmful). Thus, it will be prudent to start developing products for natural colors market.

On whole, it remains interesting idea worth tracking to me

Disclosure: Hold small position @ Average price of 48.

Another interesting observation from the AR is that despite the major break down due to fire of a critical equipment (which affected 30% of the production), they were able to grow at a steady pace.

I feel discontinuing the trading biz is a very wise move and must result in superior ROCEs.

Also as I’m new here, Is it compulsory to put Discl. at the end?

Thank you for the mgmt meet update. i hav just couple of queries:

what has led to increase in ebitda margins of manufacturing in last 2 years. ebitdam in mfg has increased frm 5% in fy13 to more than 20% in fy15 . ny reasons for the same ?

also mfg sales were arnd 115 cr in fy15 nd they r going to discontinue trading. doesnt the company’s tgt of 500 cr in 2020 look aggressive ?

Increase in margins was due to capacity expansion and higher utilization and several efficiency revamps.

With the current capacity of 4200 MTPA they will do around 250 Cr of sales by FY17 and the incremental expansion will double the capacity and thus double the topline by FY20.

The importance of colors to attract the buyers is very well known to the industries. As such, the market of color pigments is growing at a very fast pace. A wide range of pigments are used in textile industry and they are increasingly substituting dyes. Other than textiles, pigments are used extensively in the sectors like cosmetics, paper, building material, ceramics, and glass. (Even pharma)

Vidhi says it is the lowest cost producer (probably because it is in India). What stops other players, especially Sensient to produce from India

Company says it wants to target 500 crores and 8400 MTPA by 2020. Since u mentioned Industry is growing at 5% only, this good growth can come only at the expense of taking market share away from leader. Do you think market leader would give away such a huge pie (almost 30% of its share) just because it is not producing in India.

Why is there such a huge gap between Sensient and Roha. Is Sensient’s product and management so superior to command double the size to next competitor. If it is, how come it is not addressing question asked in Point 2

As you can see from Sensient’s website, they are now focusing on Naturals market. Due to high entry barriers (explained in note) and small market size, there are only four major players globally. Sensient with its deep pocket can buyout Vidhi (that question is covered in the note).

In past few years Vidhi and Roha has gradually taken up a decent market share. How they did it? They are able to produce 30% cheaper than Sensient and they have established a brand as 2nd/3rd largest player in the industry.

As explained by the MD, Mr. Manek, India had a poor reputation globally until a few years ago i.e. nobody believed we could be able to manufacture high quality colours. In last decade the scenario has changed substantially and Vidhi and Roha both have taken a huge market share from Sensient.

Now how will Sensient give a comeback or are they even interested in a comeback? Is synthetic colour market too small and insignificant for them? Will they acquire Vidhi and Roha? Story yet to be unfolded

I agree Valuation is a bit stiff at this price and I wish I had met the mgt few months ago.

Mgt did explain that synthetic colours will take a long time to be replaced by natural colours due to several reasons (naturlas have less variety in shades, they are expensive, it is just the propoganda that several countries have made naturlas food colour obligatory, it is like govt. making organic food in all the restaurant mandatory

Regarding customers: If you are getting same quality stuff at a substantially cheap rate from a branded player who is positioned second in the industry, would you buy? that is how Mr. Manke explained.

Though Abhjit has answered your questions, here is my thought process on the same.

Vidhi, at current realizations, is selling around 3600 MT in the market both from manufacturing and trading. Thus, out of 40,000 MT market, it is commanding around 9% market share. Now, let us for the moment, assume that market actually grows at 5% CAGR for 5 years, market will expand to 51,000-52,000 MT. Thus, if Vidhi is able to sell 8400 MT (as the management claims), it will have 16% market share. Thus market share gain will be around 7%. Now this market share gain can come from either Vidhi capturing new demand/market agressively or taking away existing market from other players or both. Most likely, it is likely to be both. Having said that, I do not want to suggest that we shall take management commentary on face value. However, i am just alluding to the fact that it may not mean Sensient ceding 30% market share and the projections do not factor in highly unrealistic situation

Coming to the revenue aspiration of 500 Crores, again we shall consider that the realization may improve over next 5 years as it has in the past (except for substantial strengthening of rupee, which also can not be ruled out). So, with volume expanding to 2.3 times (3600 Tons to 8400 Tons) and realization improvement by 3% CAGR (reasonable assumption in my opinion considering historical realization growth) will mean that realization in 2020 can be 1.16 times current realization. Thus if capacity, as claimed, come on stream and company able to market it, revenue can reach 500 odd crores. (2.331.16180 Crores)

Another, interesting thing, which has not been factored in currently and may give fillip to revenue growth is that realization from natural colors is 10-20 times that of synthetic colors. Thus, even if company is able to produce and sell 5% of its capacity for natural colors in 2020 (Again an assumption), can add 150-200 odd crores. Here is the maths

Natural color production: 5% of 2020 Production = 0.058400 tons = 420 Tons

Natural color realization: 10-20 times synthetic colors i.e. Roughly (105,00,000)/ton = 50,00,000/Ton

Revenue from natural colors = 420 * 0.5 Crore = 210 Crores

Now as you can see, there are number of assumptions here, as always is the case. however I find most of them reasonable in the context of the industry and business’s past performance. So, I feel that 500 Crore target is a tall task by all means but something which is not unrealistic. The key monitorable is how well company is able to manage increase in production capacity over next 5 years and then create market for it.

Having said that, I typically am very cautious of management that gives aggressive guidance and have missed many multi-baggers due to that. So, the prudent approach will be to build our own scenarios and see, whether VDSL presents an opportunity where downside is limited with fair possibility of good upside. Such cases, we can analyse

15% sales growth; Margin expansion to 20%

20% sales growth; Margin expansion to 18%

25% sales growth; margin expansion to 20% (best case)

15% sales growth; no margin expansion (worst case)

What can kill the idea?: In my opinion, single factor that can kill the idea is the currency appreciation as it will impact realization thus margins and will make the India’s product less competitive thus slowing/stopping shift from market leaders to Indian players

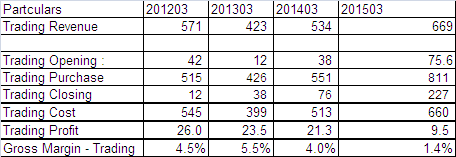

Just a correction,trading is done in chemicals which form raw-material for manufacturing food colours and only 118 crs from 2275 MT of production is sales of food colours. So market share right now comes to 5.75% roughly.

Another thing I would add regarding natural colours is that capacity up to 8400 MT is purely for synthetic colours and not fungible. New set-up will be needed for natural colours.

Thanks for pointing out on trading sales being chemicals and not the end products. I agree with you that the trading sales is not the final product but RM or intermediate one as mentioned in AR annexures. I had missed out that somehow.

Regarding natural colors capacity, my central point is that even if VDSL ventures into natural colors on small scale (as compared to synthetic colors) it can contribute handsomely to the top line. I do recognize that the processing facility may be different from the synthetic color, however if the company is able to develop products and market it, there exist a significant possibility of company setting up capacity and capitalize on this opportunity.

it’s Great stock worth investing… few piece of take away from my buying reason

under valued

Wide Moats

high margin of safety

above Cash flow growth which impressed me most i.e, > 25%

Disclo : i’m taking position in company and will accumulate at appropriate time

Very good post indeed,

Couple points to add, @desaidhwanil, In the table u have taken only Trading purchase, For determining the trading cost we must consider (increase)/Decrease in trading stock.

I have done the same and derived following figures, (no. in Millions)

If the revenue from manufacturing is Rs.121 cr, Then to reach Rs.500 cr in 5 year, they need 32% CAGR in manufacturing revenue, Since the production was 2275 and expected to reach 8400 MT (30% CAGR, Assuming Production is nearly same as sale), Just concerned about the market share gain (is the company capable of such Market gain?)

Whether the Rs.500 cr target includes natural and Pigments as well, Any developments on Pigments front (Capacity, Investment, Production start date, Which area company is targeting)?

!

!