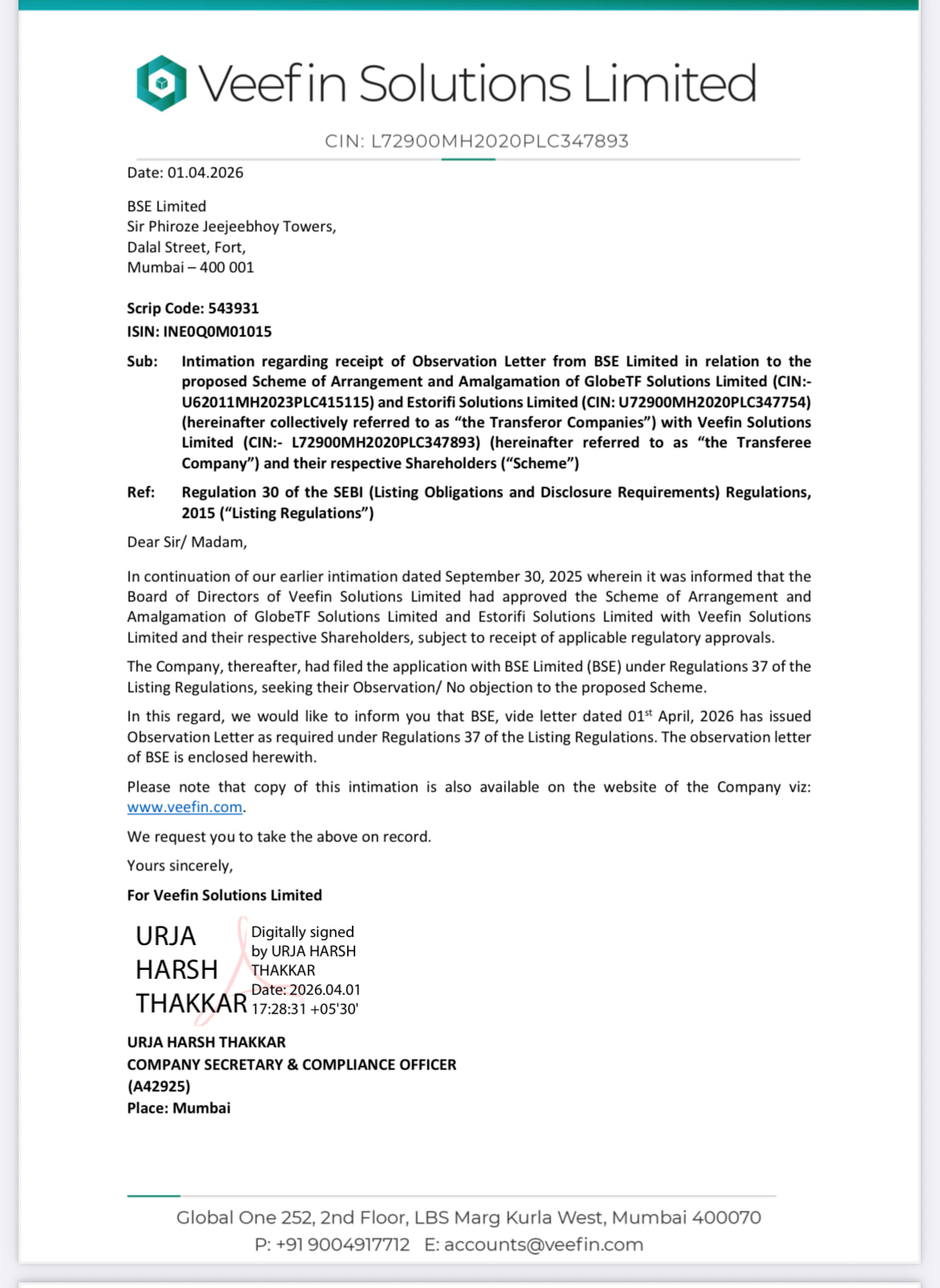

Veefin has received BSE’s no-adverse-observation letter for the proposed amalgamation of GlobeTF and Estorifi into Veefin. This is a positive regulatory milestone and allows the company to move ahead with the NCLT process. However, it is not a final approval—Veefin still needs to comply with SEBI/BSE disclosure conditions, shareholder/creditor requirements, and obtain NCLT sanction.

This was another positive update; 1st anchor corporate live on PSB Xchange for Bank of Baroda.

Seems like Tata Hitachi is the anchor ; not confirmed .

They are hiring big names as well. Rrkabel is decent size company, one success story will create ripple effect. Lets see if rrkabel manages to improve their working capital via psb platform

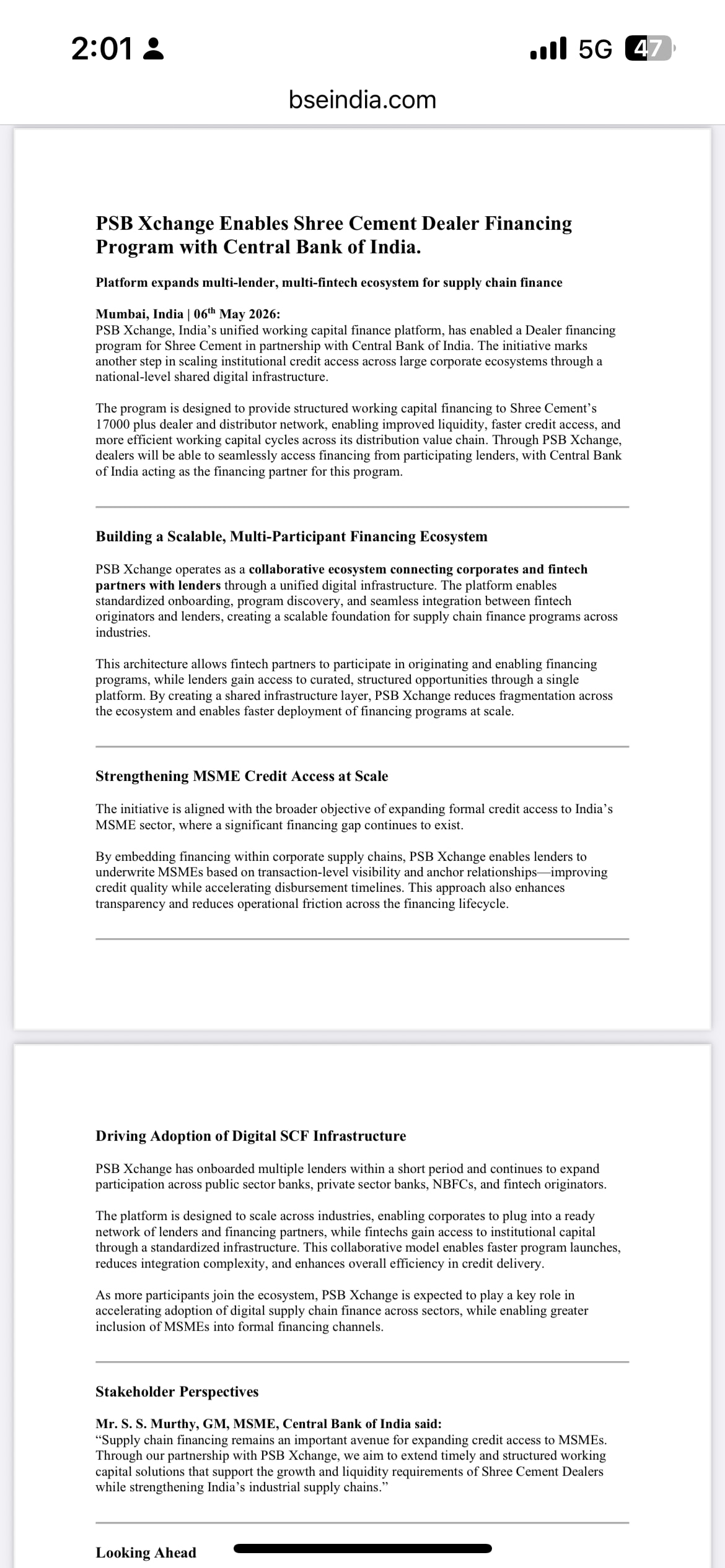

17,000 dealers. One credit rail.

Shree Cement has plugged its dealer network into PSB Xchange, with Central Bank of India as the financing partner.

This is the part investors should not miss:

PSB Xchange is not trying to become another lender.

It is trying to become the shared financing infrastructure between large corporates, their dealers, fintech originators, and banks.

That is a very different game.

Banks get curated supply-chain credit flow.

Dealers get faster working capital.

Corporates get a healthier distribution network.

And PSB Xchange gets closer to becoming the default SCF rail for India Inc.

The metric to track now:

How many anchor ecosystems move from announcement → active disbursement → repeat utilization?

First was RR Kabel and now this. Even a single success corporate story will create a ripple effect. Increased allocation in recent fall. Lets see how it goes. Stock has some move in 2 days. Quite big fall from recent warrants at 390

Veefin Solutions Limited Posts Strong Growth in FY26 Results

• Financials (Consolidated):

-

Q4 Revenue: Rs 13,134.65 Lakhs (Up from Rs 10,374.36 Lakhs in Q3)

-

Q4 Net Profit: Rs 1,597.96 Lakhs (Up from Rs 777.59 Lakhs in Q3)

-

Full Year Revenue: Rs 34,512.92 Lakhs

-

Full Year Net Profit: Rs 3,196.26 Lakhs

• Financials (Standalone):

-

Q4 Revenue: Rs 2,416.72 Lakhs

-

Q4 Net Profit: Rs 575.59 Lakhs

-

Full Year Revenue: Rs 7,073.69 Lakhs

-

Full Year Net Profit: Rs 1,820.38 Lakhs

Hey bro, in today concal Mr Raja said at 49 minutes while explaining psb flowchart, he said company like r r kabel has to come to psb alliance via a fintech. Why cannt r r kabel directly reach psb alliance ?

Also qualified enterprise pipeline is usd 80 million means around 760 cr, Mr Raja said in 6 months, 25% will be converted for sure so means revenue potential of 190cr ? since the process is a long cycle, how much do you expect it to be booked in Fy27 ? and if we suppose 50% pipeline for FY27 so how much can be reasonable to be considered as booked?

Do you mind an updated revenue and projection in light of concall ?

@Shail1234 This is my understanding of PSB exchange. Onboarding an Enterprise is a tedious task. I believe Veefin just wants to focus on the technology part and doesn’t want the hassles of onboarding big companies/conglomerates when they can just share few margin points with a fintech.

PS: This is my interpretation.

@shubham2 Thank you Shubham ji. Yes for purpose of scaling and swift adoption they are using fintech for enroling companies. But they are open to direct enrolment in future as per their IR.

A positive corporate testimonial would be the cleanest soft trigger. One real acknowledgement from a serious corporate is more powerful than 20 presentation slides , because it proves the platform is solving a real operating problem, not just creating a nice investor narrative.

If one anchor says PSB Xchange made dealer/vendor financing faster, smoother, or more efficient, it can create a ripple effect. Other corporates trust operating proof more than platform claims.

But even if no corporate publicly acknowledges it, that does not automatically weaken the thesis.

Many corporates may not want to publicly discuss working-capital arrangements, dealer limits, vendor finance, bank tie-ups, or internal credit processes. In B2B finance, silence is normal. The real question is not whether they praise the platform publicly. The real question is whether their behaviour proves adoption.

So we should track both paths:

Case 1: Corporate acknowledgement comes

That becomes a trust signal. It tells us PSB Xchange is not just onboarding anchors, but actually solving friction for their ecosystem.

Case 2: No public acknowledgement comes, but numbers keep improving

Then numbers become the testimonial. If approved limits convert into active programs, active channel partners, utilisation, ADPO, repeat usage, and PSB Xchange revenue, that is even stronger than a quote.

For me, the hierarchy is simple:

Testimonial proves trust.

Utilisation proves value.

Revenue proves monetisation.

Cash flow proves durability.

So a corporate quote would be great. But if we don’t get one, I’ll still stay focused on the operating data.

The only weak case is where we get neither: no testimonial, no utilisation disclosure, no ADPO, no revenue clarity — only rising “approved limits.” That would be noise, not proof.

On the first point — why RR Kabel or any corporate has to come through a fintech instead of directly going to PSB Alliance — my understanding is slightly different.

It is not that RR Kabel cannot talk to a public sector bank directly. Of course it can. Large corporates already have banking relationships.

But PSB Xchange is not just a loan enquiry website. It is an operating workflow where anchor, dealer/vendor, sourcing partner, platform, and lender all interact in a structured way.

That is where the fintech/sourcing partner comes in.

Think of a dealer sitting in a Tier-2 or Tier-3 market. He may be excellent at selling cables, cement, paints or electrical goods. But he may not know how to navigate every small banking step — onboarding, KYC, GST/PAN data, turnover details, anchor relationship proof, documentation, lender mapping, limit application, offer acceptance, and activation.

A good analogy is insurance TPA desks in hospitals.

The patient theoretically has insurance. The hospital theoretically accepts insurance. The insurer theoretically has a claim process. But in the real world, someone has to coordinate between hospital, insurer, documents, approvals, and customer.

That is why TPA/helpdesk teams sit inside hospitals.

They are not the insurer.

They are not the hospital.

But they make the system usable.

Similarly, the fintech/sourcing partner is not merely a broker. It is the operating bridge. It converts corporate intent into bank-ready digital workflow.

And many of these sourcing partners may already have an active relationship with the corporate in some form — IT systems, ERP integration, channel management, onboarding, data handling, reconciliation, or other workflow-related services. That existing relationship matters.

Because when a new platform has to be adopted, the best trainer is often not the bank. It is the person who already understands the corporate’s process, speaks to its team, knows its dealer/vendor ecosystem, and can sit between business, technology, and finance.

So the simple answer is:

RR Kabel can reach banks directly.

But to run dealer/vendor finance at scale through PSB Xchange, it needs a fintech/sourcing partner layer to package, onboard, map, train, and push the ecosystem into the platform.

This is exactly the difference between a loan relationship and a platform business.

A loan relationship is one corporate talking to one bank.

A platform business is one anchor, hundreds or thousands of dealers/vendors, multiple banks, standardized data, repeatable workflows, assisted onboarding, and continuous navigation.

That is why Veefin’s ground army matters. If this was just direct corporate-to-bank lending, you would not need 26-city physical execution. The ground layer exists because trust is physical, but speed is digital. The Ground Game: Why Veefin Solutions is Hiring an Army

On the pipeline point, I would stay conservative.

I don’t track pipeline as revenue. Pipeline only shows demand or interest. My focus would be on numbers that have already entered the operating layer — signed, integrated, live, active programs, active channel partners, utilisation/ADPO, and actual billing.

So until the pipeline becomes integrated/live platform activity, I would treat it as optionality, not base-case revenue.

@udaychandak Quite crystal clear. Thank you for taking time to revert ![]()