[Update] Veefin Solutions Q3 FY26 result:

Following up on my previous analysis after the last results. Since my last post, the “Jockey” (Raja Debnath) has moved from building the machine to industrializing it. The three major updates covered in this thread are:

- The Ground Army: Deploying a physical sales force in 26 cities (The Bajaj Playbook).

- The “Vanishing Act”: Restructuring to reveal a ~60% EBITDA SaaS core.

- PSBX Velocity: Approved limits have officially hit ₹4,000 Cr.

The Ground Game: Why Veefin Solutions is Hiring an Army

`Trust is Physical. Speed is Digital. Why the “Jockey” is betting on boots on the ground, and how the financial clean-up is priming the business for a massive value unlock

Think about Amazon for a second.

Is Amazon a “Tech Company”? Yes. But does the website deliver the package to your door? No. A human being in a van does. Amazon wins because it mastered the rarest combination in business: Digital Speed + Physical Reach.

Veefin Solutions is doing the exact same thing for Indian Banking.

Most investors misunderstand this company. They think Veefin is just selling code to banks. They are wrong. Code is cheap. Code sits on a server. Code waits for a user to log in. Veefin realized that in the deep operational reality of Indian finance, you can’t just build the website—you have to drive the van.

The Thesis Compounds

We have been tracking this story closely, and with every quarter, the picture gets sharper.

- The Start: In Betting on the Jockey , we identified the Architect . We bet that Raja Debnath had the blueprint to solve the massive MSME credit gap.

- The H1 Check-In: In our last update (The Jockey Accelerates ), we verified the Integrity . We watched the cash flows stabilize and the runway clear after the first half of the year.

Now, with the Q3 FY26 numbers out, the narrative shifts again. We are moving from “Validation” to “Industrialization.” The Jockey has finished building the machine, and he is now hiring the army to run it

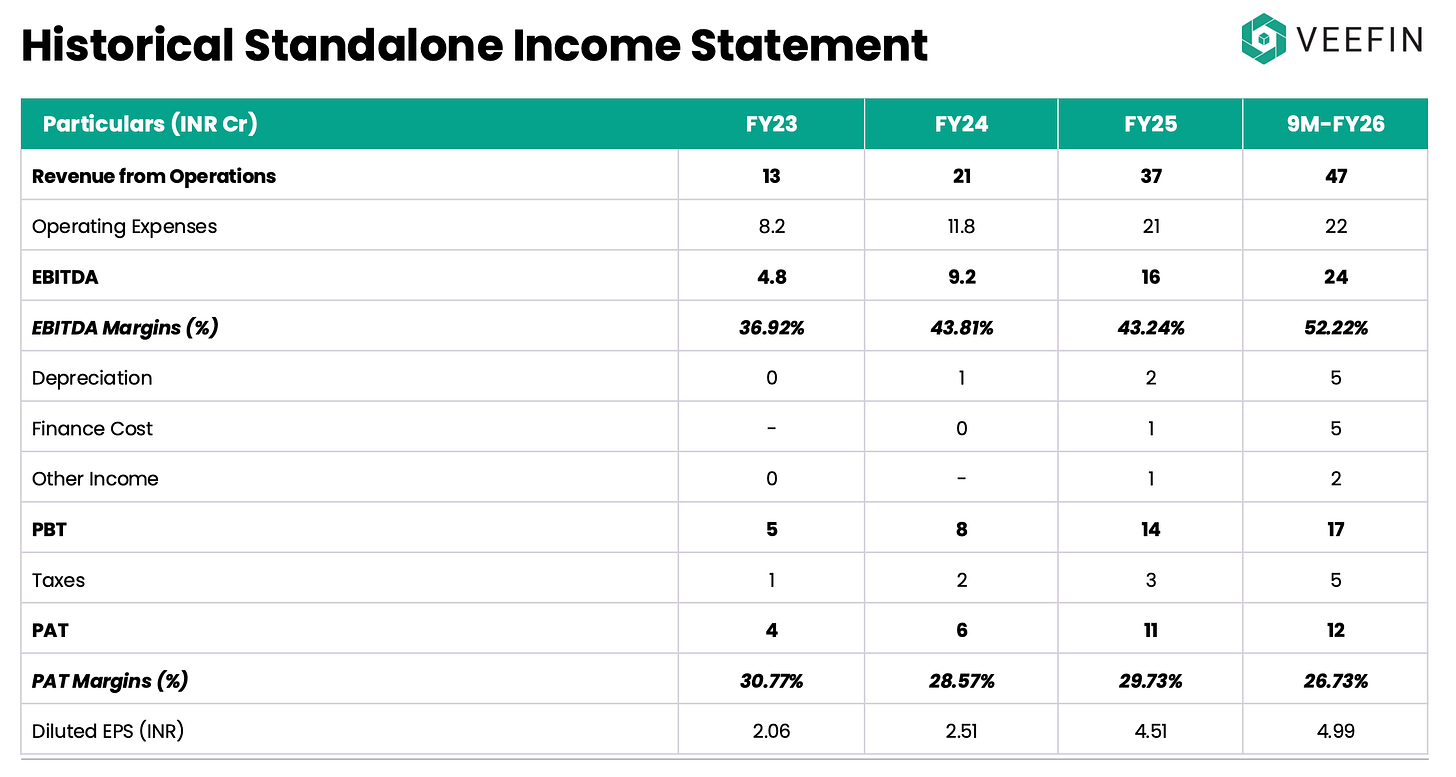

The Q3 FY26 Result Snapshot: Velocity vs. The Mix

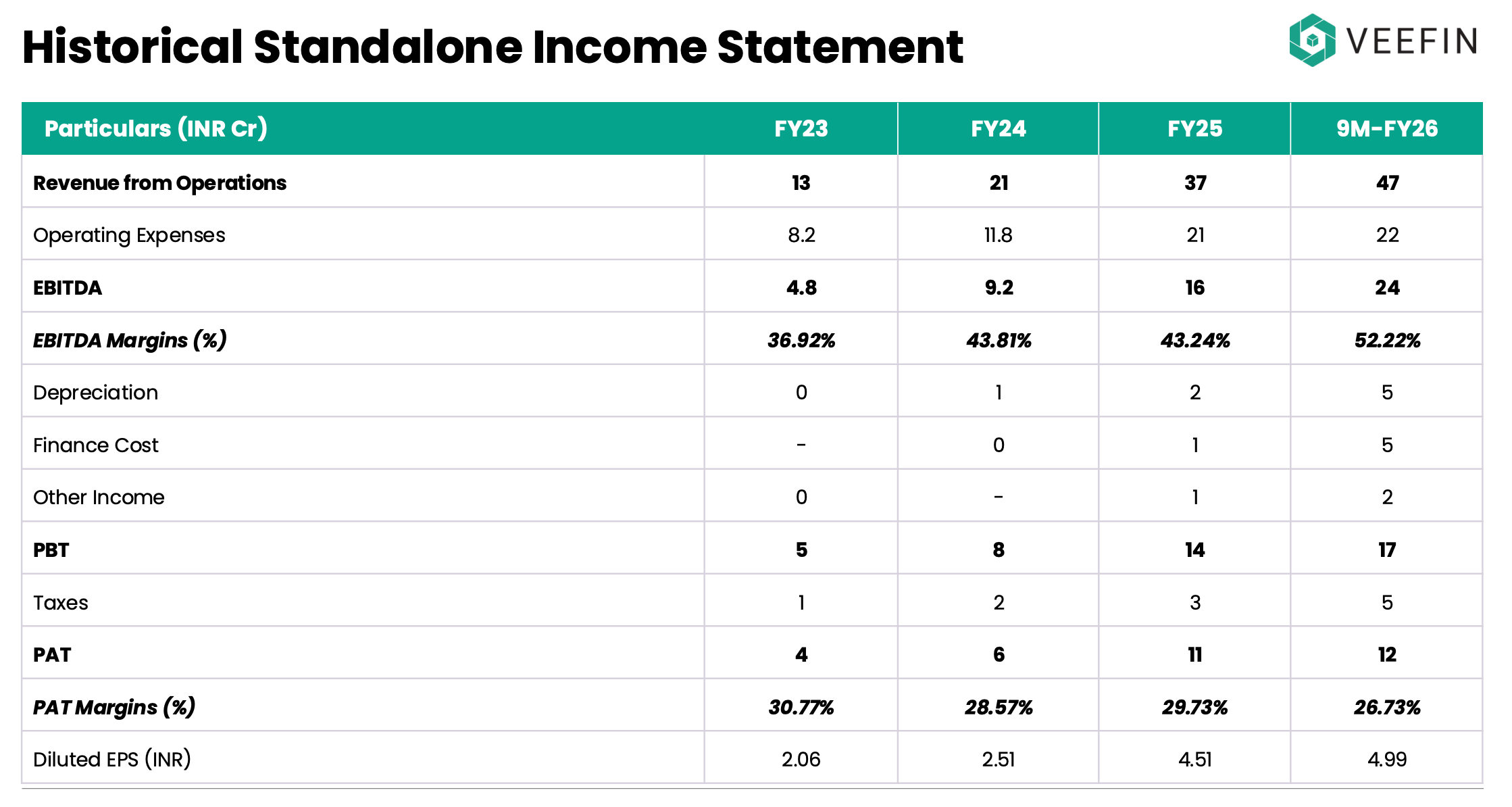

Standalone Income Statement

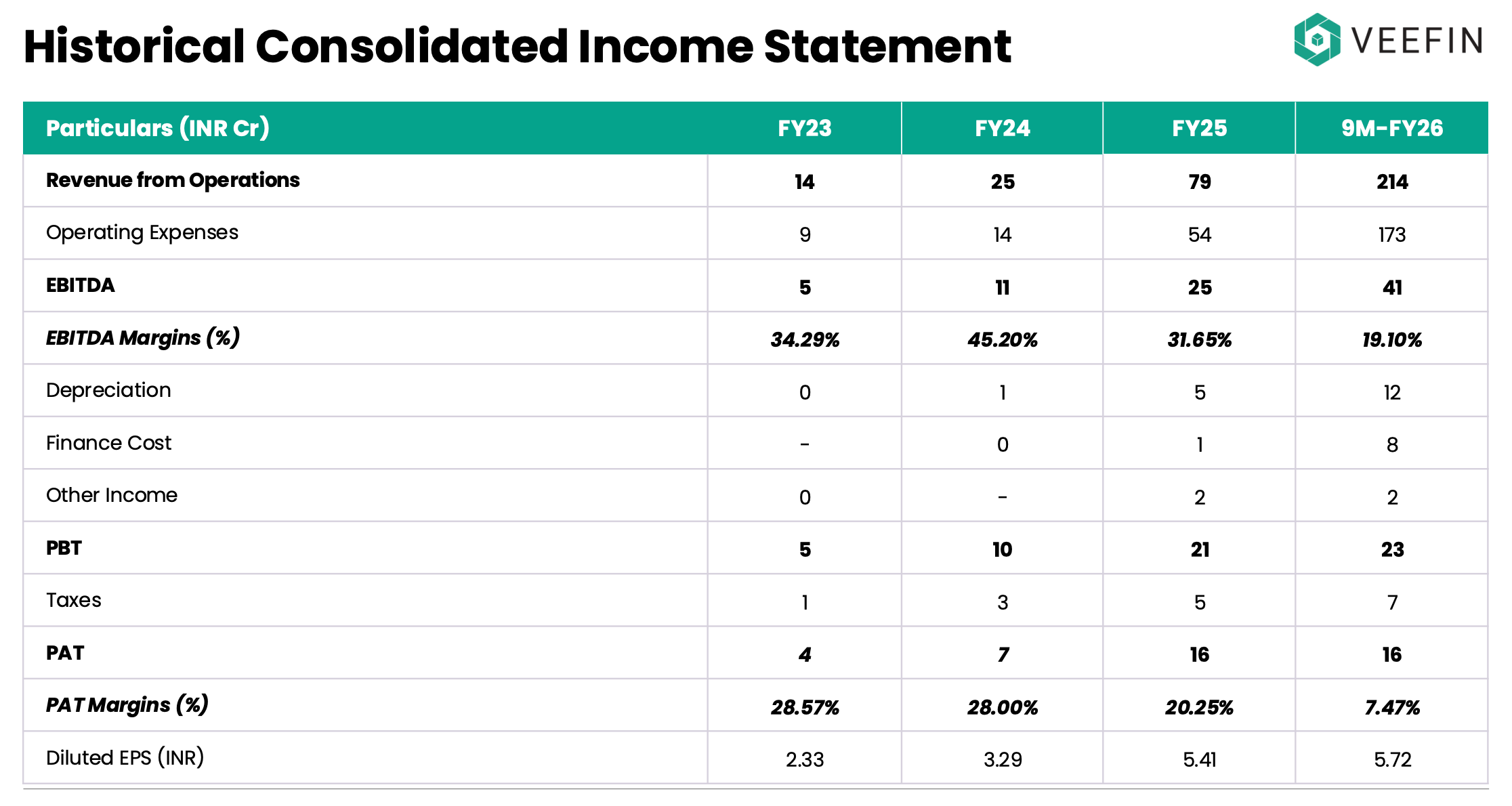

Consolidated Income Statement

The Snapshot: Velocity vs. The Mix

Let’s look at the financials with nuance. The Q3 numbers tell a story of rapid expansion, but also of a structure in transition.

- The Velocity: 9M FY26 Revenue stands at ₹213.78 Cr . (For context: That is 2.7x the revenue of the entire previous financial year combined.)

- The Margin Reality: Consolidated EBITDA margins have settled at ~19% . To the casual observer, this might look like a decline in efficiency. However, a deeper look reveals it is simply a **product of the mix.**The current structure blends two very different business types: the high-margin Product Business (Estorofi/GlobeTF) and the lower-margin Service Business (White Rivers Media/Nityo). When you consolidate them together, the Service business naturally dilutes the Group margins. It is a mathematical inevitability.

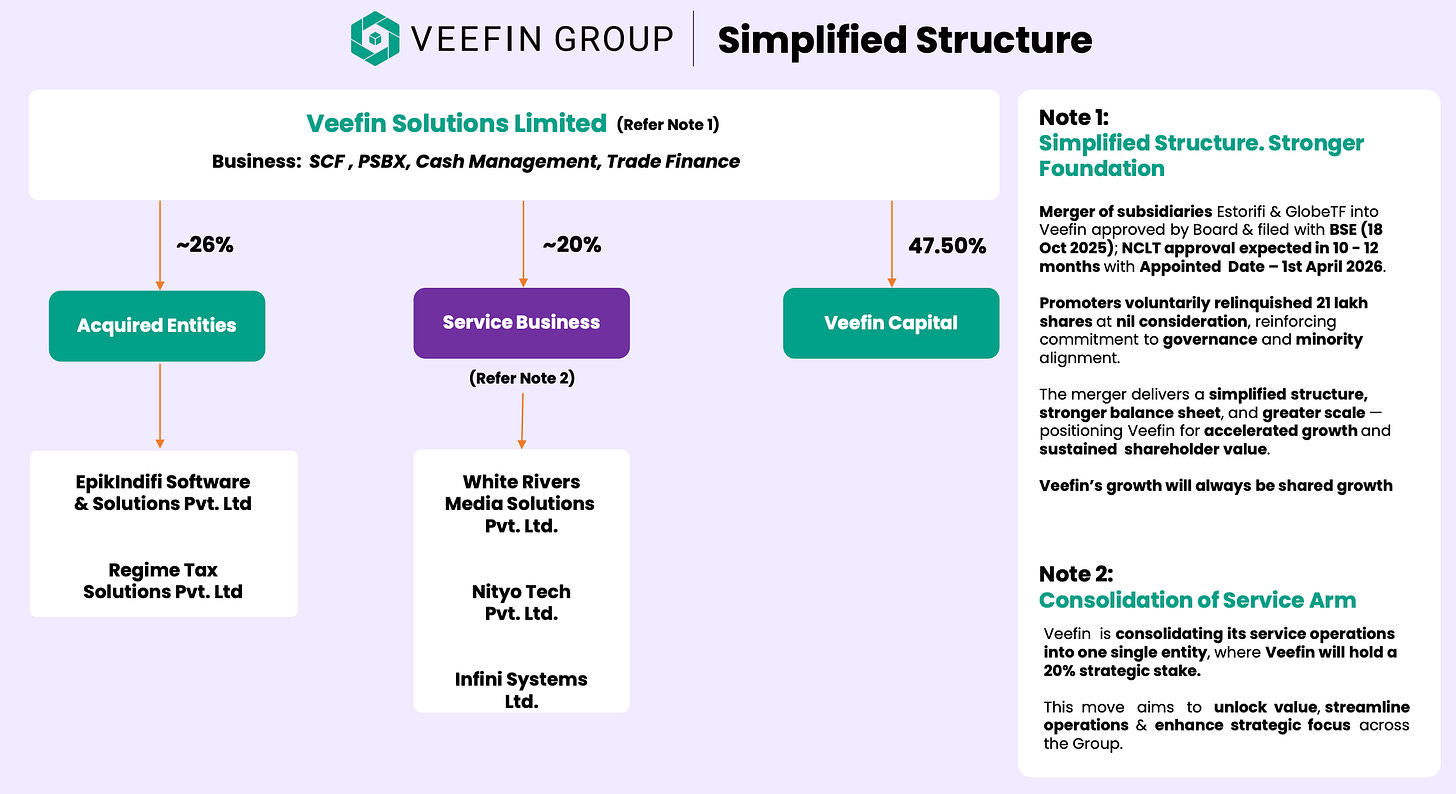

The Fix: Merger & Segregation Management has recognized this and is executing a structural realignment to fix it:

- Merging the Core: They are merging the Product subsidiaries (like GlobeTF) into the parent company to consolidate the high-margin IP.

- Segregating the Services: Simultaneously, they are de-consolidating the Service-heavy businesses.

The Deal Status: No Surprises This isn’t a reaction to recent volatility; it is a pre-existing roadmap. The Amalgamation Plan was originally submitted in October 2025 and was explicitly detailed in the H1 FY26 Concall .

The strategy has been set for months. We are now simply watching the regulatory gears turn:

- BSE Observation Letter: Received. (The Exchange has reviewed the scheme).

- Management Reply: Submitted. (All queries have been answered).

- SEBI NOC: Pending (10-15 Days). (This is the final regulatory green light).

- NCLT Filing: Next. (Once SEBI clears it, the matter moves to court).

- Effective Date: The corporate restructuring and merger of subsidiaries are set with an appointed date of April 1, 2026 .• Retrospective Accounting: This ensures that the full P&L and financial performance of the merged entities will be consolidated from the start of the 2026-2027 fiscal year, regardless of when the final verdict is delivered but within the 2026-27 calendar window to avoid over complication

The Pivot The growth is real. But the real story is hidden in two massive strategic pivots that transform Veefin from a “software vendor” into a “banking utility.”

- The Ground Game: Building a 26-city ground army to solve the “Last Mile.”

- The Clean-Up: “Firing” low-quality revenue to let the high-margin profits explode.

The “Bajaj Finance” Blueprint: Why Veefin Built a Ground Army

The Insight: Technology cannot solve a distribution problem.

To understand Veefin’s strategy, you simply have to look at the Bajaj Finance Playbook . Bajaj Finance didn’t become a giant just because they had an app. They won because they acknowledged a brutal truth about India: Trust is physical. They built a distribution network so deep that you could find a Bajaj agent in a small electronics shop in a Tier-4 town , long before private banks even had an ATM there.

- The Bajaj Moat: They captured the customer at the Point of Sale (the store), verified documents physically, and used tech only for the instant backend approval.

- The Result: A valuation multiple of 8-10x Book because they combined “Physical Reach” with “Digital Speed.”

The Pivot: Applying the “Bajaj Model” to B2B Veefin realized that Public Sector Banks (PSBs) are failing at MSME lending for the same reason: they are waiting for customers to walk into the branch. Veefin decided to replicate the Bajaj model. Instead of placing agents in consumer stores, Veefin places its “Ground Army” at the Anchor Corporates (the B2B equivalent of the “Point of Sale”).

A. The “Phygital” Infrastructure (Logistics for Credit)

Most analysts think this is a Tech Platform. It is actually a Logistics Business . Veefin has hired a physical operations team across 26 locations (Delhi, Mumbai, Chennai, Bengaluru + 22 Tier-2/3 hubs ) to solve the “Last Mile” friction:

- Sourcing (The Legwork): The team physically visits the “19 Anchor Corporates” and sits with their suppliers to digitize them. A supplier in a Tier-3 industrial belt requires hand-holding. Veefin provides that.

- The Handover: They verify documents, package the credit file, and hand it to the PSB ready for approval.

- The Result: The Bank Manager shifts from “Sourcing & Processing” to just “Underwriting.”

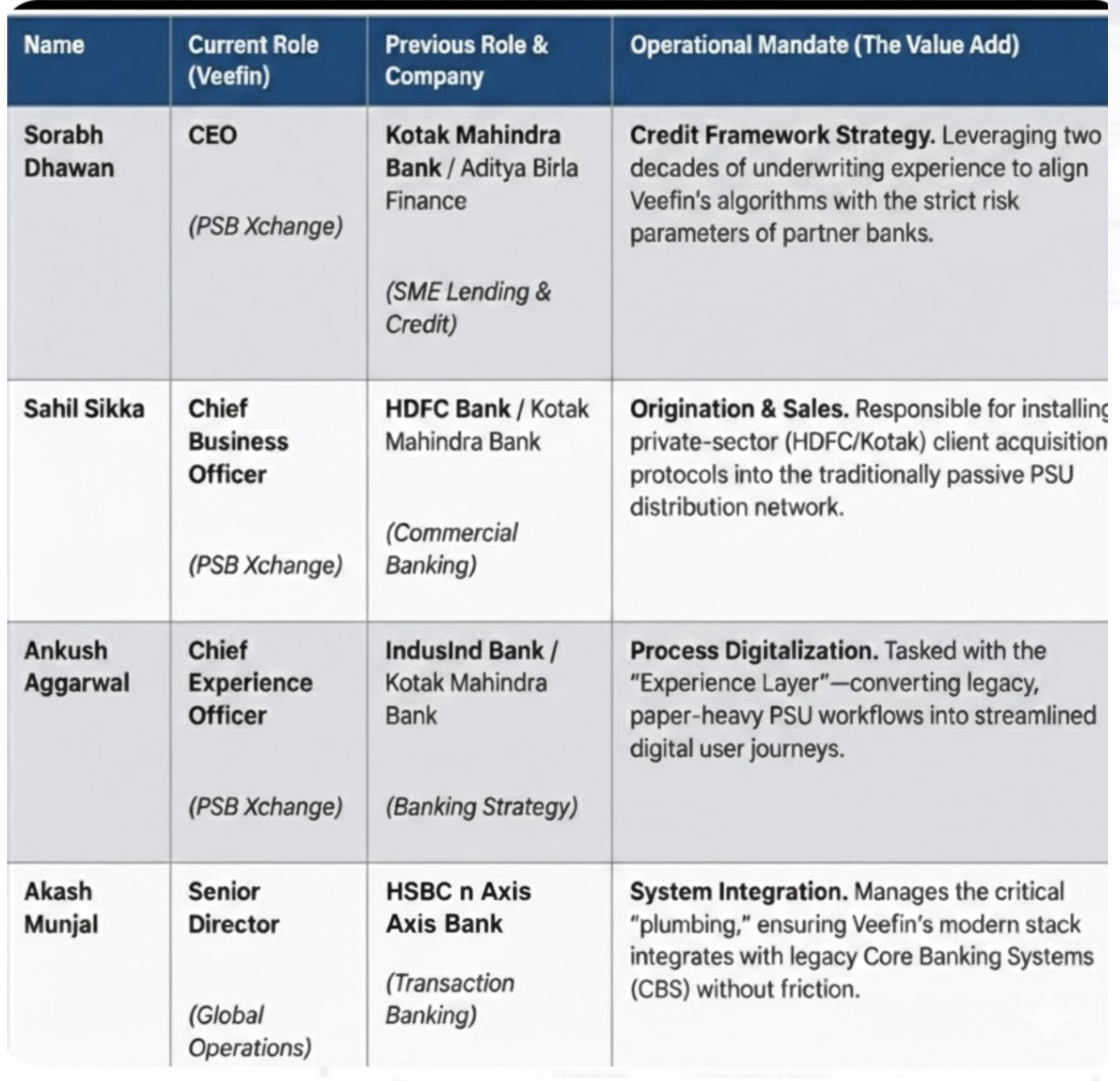

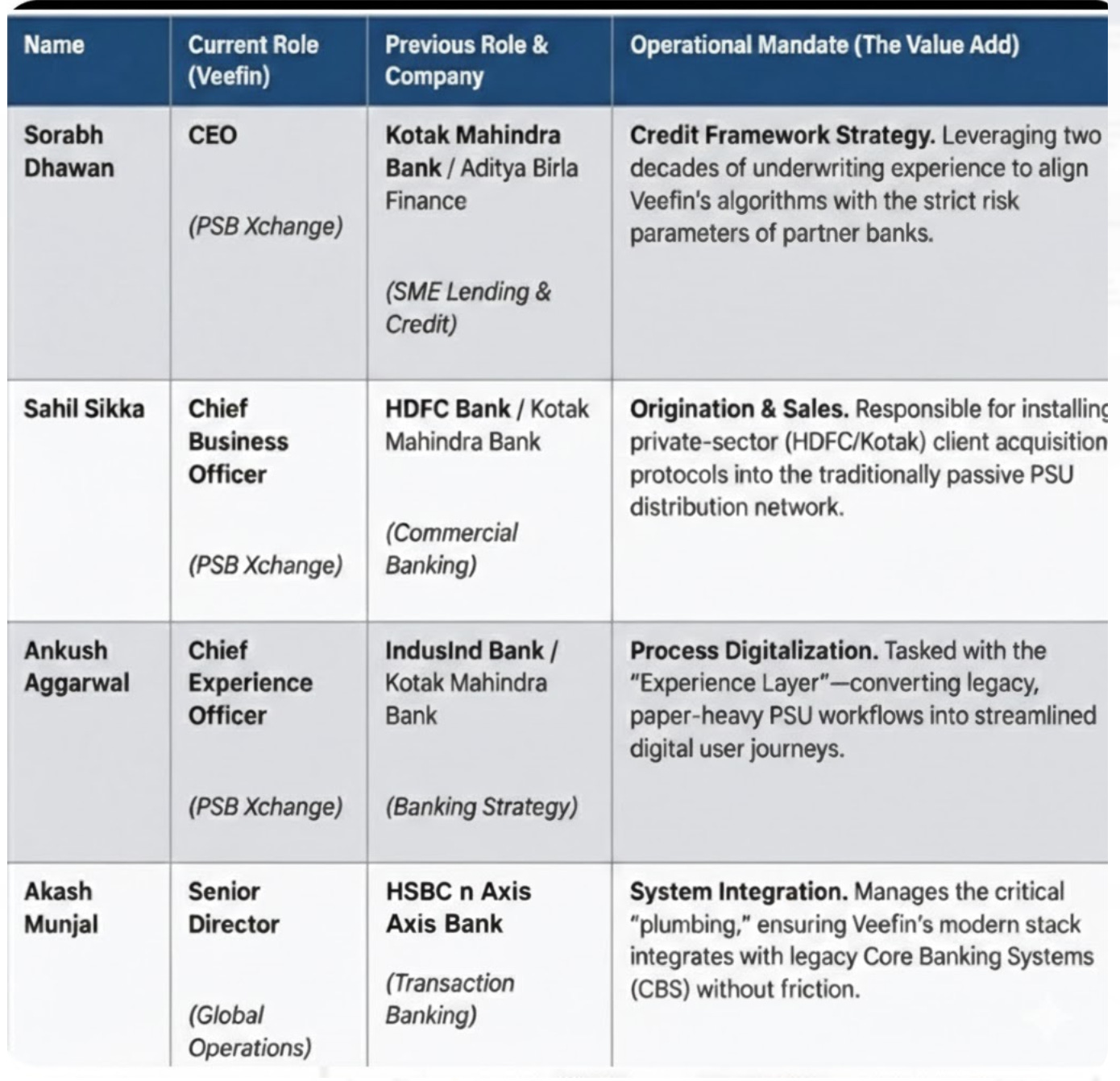

B. The “Peter Lynch” Signal: Hiring Operators, Not Visionaries

Peter Lynch famously loved companies that hired “operators” to run the complex parts of the business. The “Tell” that Veefin is serious about this pivot is in who they hired . They didn’t hire generic sales heads; they recruited Career Bankers who understand the specific risk protocols of Indian lending.

The Leadership Grid (The “Banker” DNA)

The “Hidden” Order Book: Reading the PSBX Data

The Insight: Revenue is a rearview mirror. “Approved Limits” are the windshield.

For the last year, PSB Xchange (PSBX) was a promise. In Q3 FY26, it became a statistical reality. To understand the trajectory of this company, look past the current P&L and focus on the “Traffic Data” from the latest presentation.

The “Leading Indicator” (Q3 FY26 Actuals):

- The Pipeline: ~12,000 limit requirements processed.

- The Reality: ~₹4,000 Crores in credit limits have been formally approved by banks on the platform across 19 anchor corporates.

- The Upside: Management noted that these 19 anchors are currently “testing the waters” with small initial limits. As they validate the platform, these same corporates are expected to route a significantly higher portion of their total credit mandates through PSBX.

The Revenue Pivot (Portfolio vs. Disbursement)

Crucial Correction: Veefin does not earn fees on a one-time disbursement basis. Instead, the revenue model is linked to the Average Daily Portfolio Outstanding (ADPO).

- Why this matters: In a disbursement-based model, you have to keep running to stand still. In an Outstanding-based model , Veefin earns a “toll” every single day that capital stays deployed. It turns transaction revenue into SaaS-like recurring revenue.

- The Billing Engine: While the “toll” is tracked daily for pinpoint accuracy, each month Veefin collects a one-time fee based on the accumulated total of the month’s average daily outstanding balance. This ensures zero revenue leakage from intra-month repayments while aligning with the bank’s monthly reporting cycles.

The Fee Stack (Veefin’s Take Rate: 30–65 bps)

Veefin earns on the total volume of credit active on the platform. The yield varies based on the “service mix” chosen by the lender:

- Sourcing Fee (30 bps): For origination of the borrower.

- Own-Sourced: Veefin retains the full 30 bps .

- Partner-Sourced: To scale via ecosystem partners (Fintechs, B2B marketplaces), Veefin shares the pie—retaining 10–20 bps while the partner gets the remainder. This incentivizes the entire market to route deals through PSBX.

- Technology Fee (20 bps): The “Toll Tax.” A non-negotiable, recurring fee for platform infrastructure. Veefin retains 100% of this.

- Onboarding Services (15 bps): The upfront “kicker.” A fee for digitizing the borrower (KYC/Compliance), creating immediate cash flow the moment a corporate joins.

The Thesis in Plain English

The “Base Case” is already signed. The current ₹4,000 Cr in approved limits isn’t a one-time sales target; it is the installed capacity of the platform. In Supply Chain Finance, these aren’t “loans” that get paid off and disappear; they are revolving lines . As these 19 anchors move from pilot to full deployment, they maintain this ₹4,000 Cr “pot” as a constant balance.

The Investment Case: Veefin has built a machine that earns 50–65 bps on the stock of debt , not just the flow. With a target EBITDA margin of 28–33% for the PSBX segment and a 26-city operational footprint already live and “paid for,” the platform is hitting its “operating leverage” sweet spot. Every incremental crore of utilization now drops almost entirely to the bottom line.

The Restructuring: Unlocking the Hidden SaaS Engine

The Insight: Veefin is “firing” vanity revenue to hire institutional-grade margins.

Veefin is currently a victim of its own top-line growth. By housing high-value SaaS IP alongside low-margin “services,” it has accidentally built a valuation ceiling. The market sees a ₹200 Cr+ revenue base, tags it as a “services firm,” and slaps on a low multiple—completely missing the pure SaaS engine humming underneath.

This restructuring is a Surgical Strike . It isn’t just “cleaning up”—it is a deliberate move to collapse the revenue “quantity” to reveal the profit “quality”.

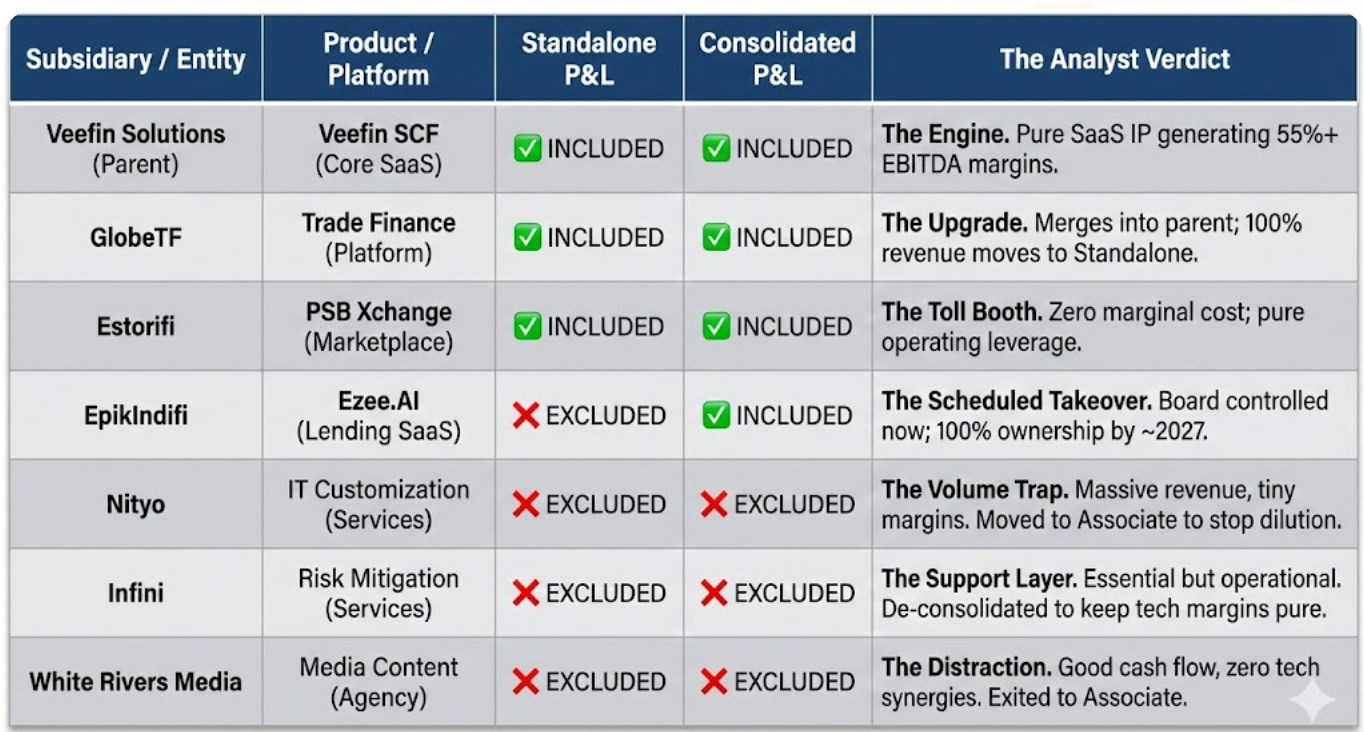

A. The Blueprint: Separating the Signal from the Noise

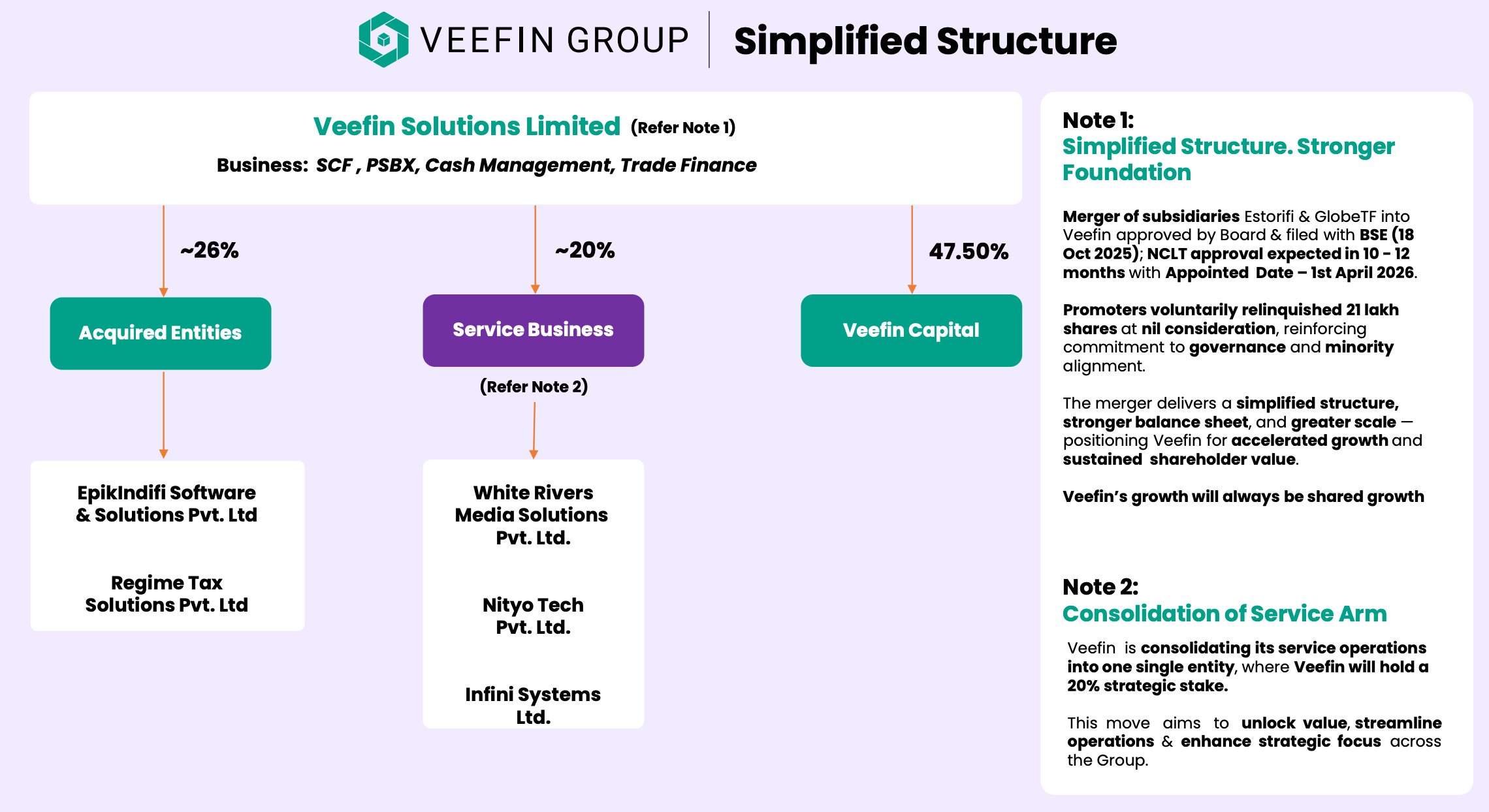

The following mapping identifies exactly what stays on the main books and what gets moved to the “Associate” layer to fix the group optics.

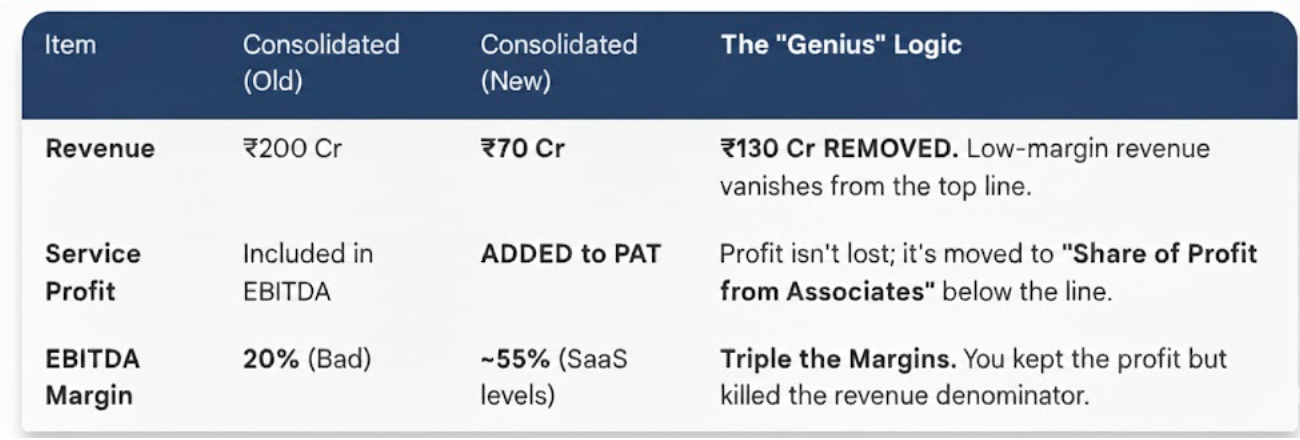

B. The “Consolidated” P&L: The Vanishing Act

This is where the magic happens. By reducing their stake in the Service Businesses (White Rivers, Nityo, Infini) to only 20%, Veefin triggers a “De-consolidation Event” .

The Revenue Rule: In accounting (Ind AS), if you own less than 50% (and don’t have control), you generally DO NOT consolidate the Revenue line.

- Revenue Drops: The massive (but low-margin) revenue from the Service Business will disappear from Veefin’s top line.

- Profit Stays: You still get to keep 20% of their Profit (PAT), but it shows up as a single line item called “Share of Profit from Associates” below the operating line.

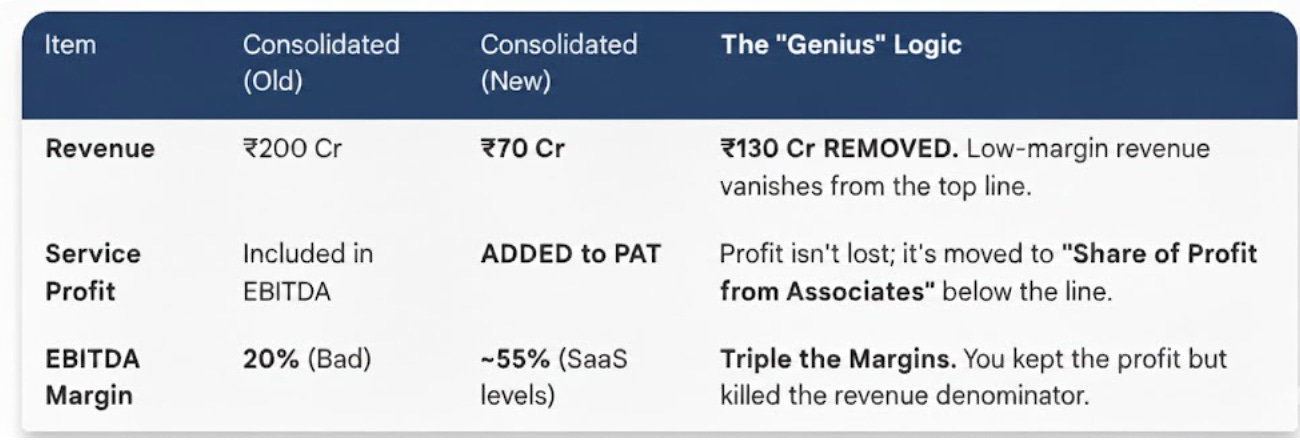

The Alpha Grid: Why This is Genius

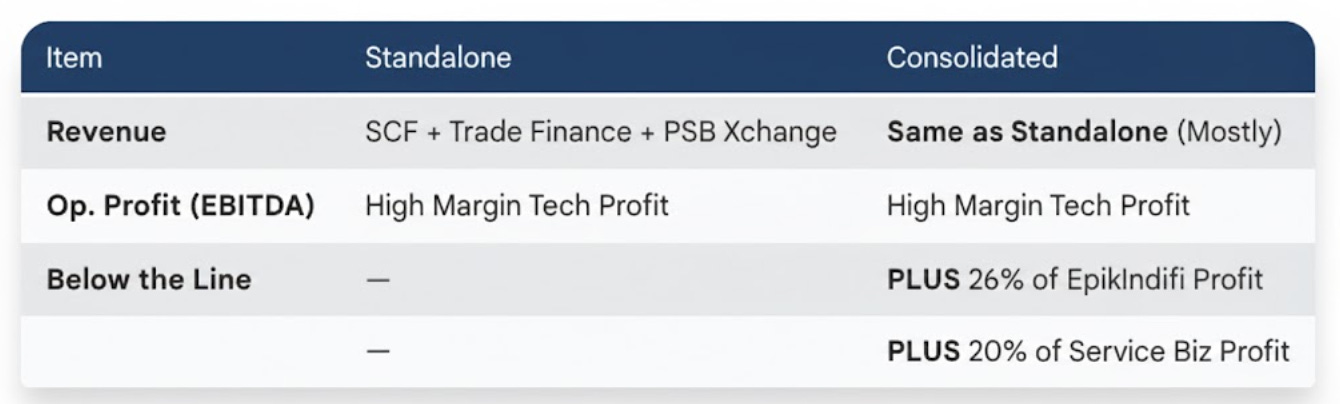

C. The Final Picture

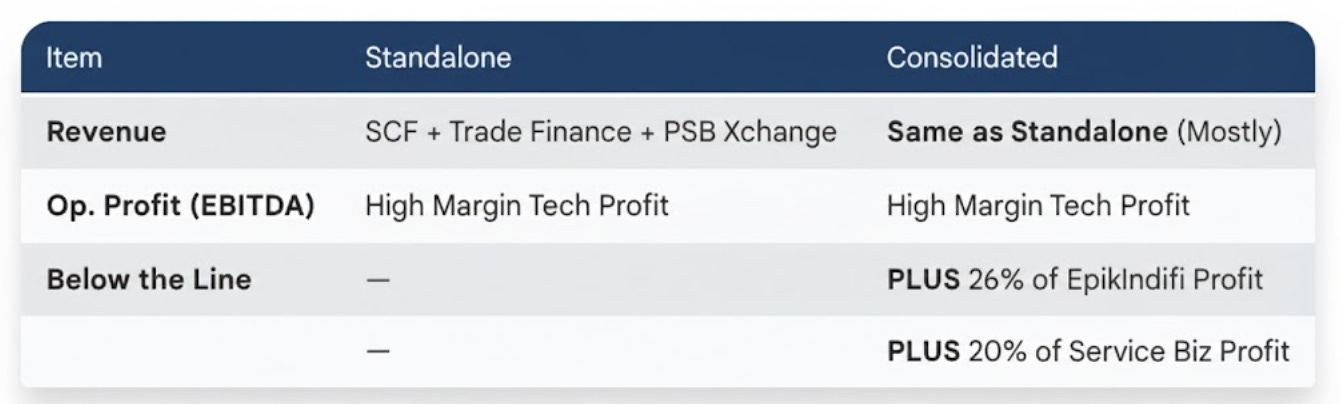

Going forward, “Standalone” and “Consolidated” will actually look very similar in terms of Revenue.

D. The “Munger” Takeaway: Firing Revenue to Hire Margins

Veefin is essentially “firing its revenue.” They are willingly giving up the “big revenue number” of the service business to ensure that the quality of the revenue remaining is pure, high-margin SaaS.

- The Promoter Signal: Promoters recently cancelled 21 Lakh of their own shares (worth ~₹80 Cr+ ) for zero consideration to get this merger approved.

- The Verdict: Insiders don’t burn ₹80 Cr of personal wealth for charity. They did it because they know the “Clean Entity” will be worth exponentially more to the market than the messy one.

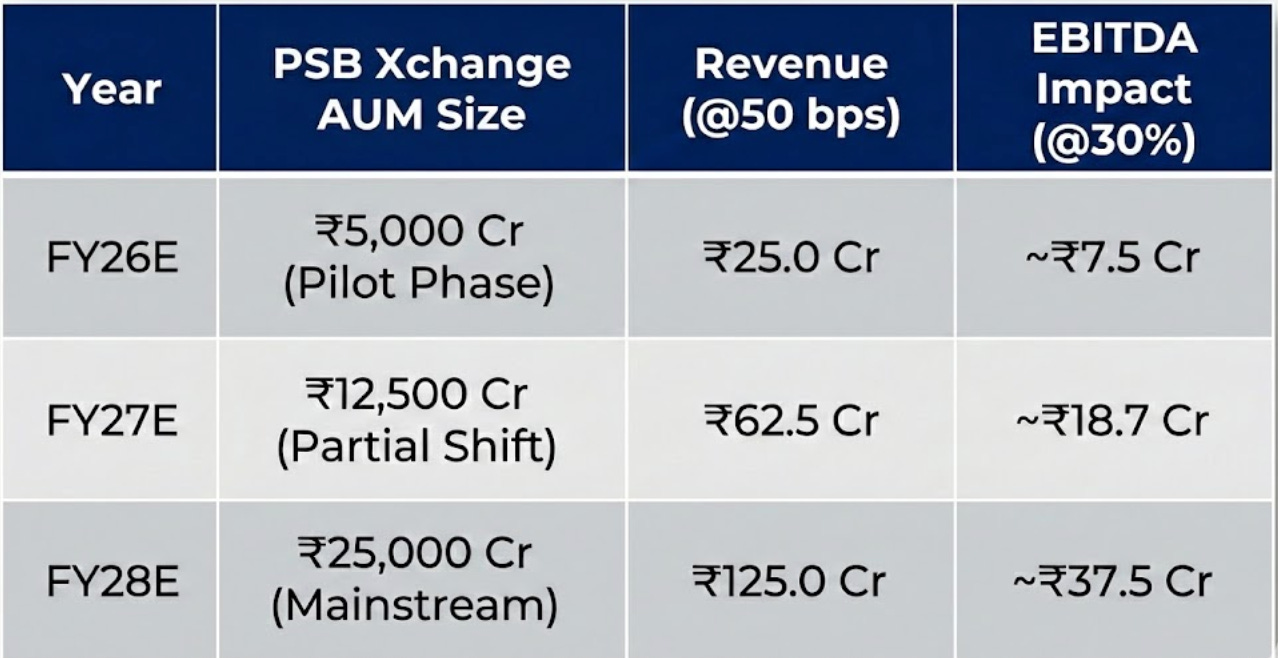

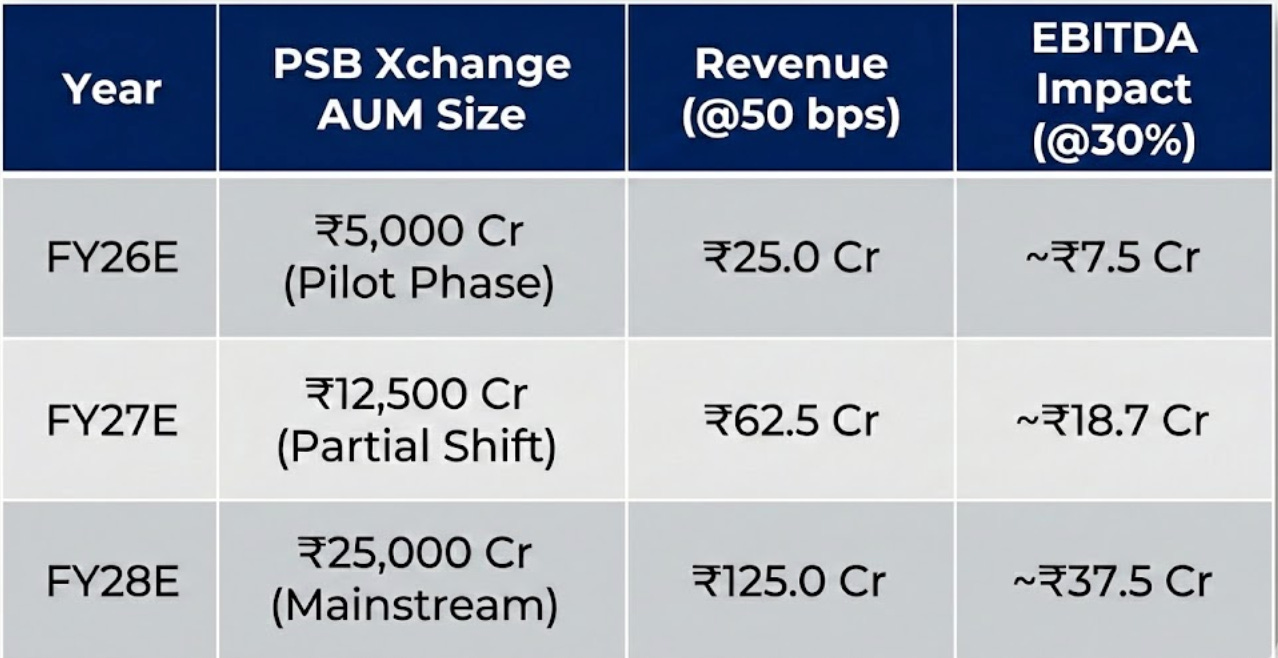

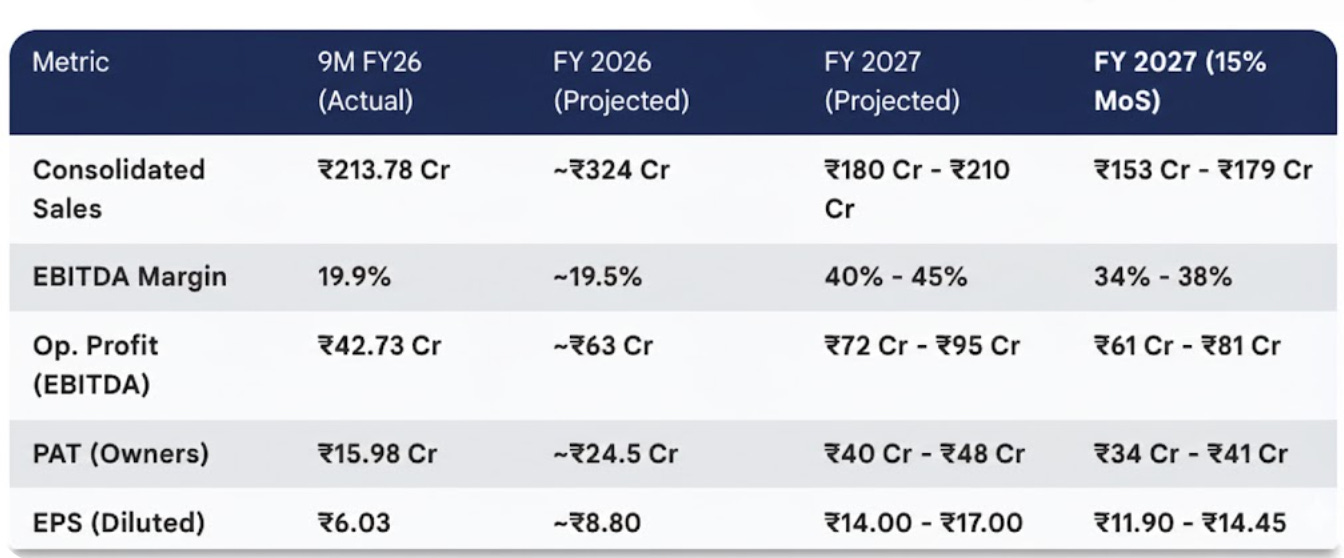

The 3-Year Roadmap: Scaling with a Safety Buffer

The investment thesis hinges on a legal reclassification. By FY27, the “Vanishing Act” removes approximately ₹130 Cr of low-margin service revenue, exposing a high-margin technology core. To account for transactional variability, a 15% Margin of Safety (MoS) is applied to the base projections.

Restructuring Ledger (FY26 - FY27)

The Anti-Thesis: Strategic Challenges & Risks

The Insight: A robust thesis must account for the competitive moats and regulatory hurdles that could slow the transition.

1. The TReDS Ecosystem: A Different Market Segment

It is important to distinguish between the mandate of TReDS (RXIL, M1xchange) and the white-labeled SaaS model.

- Regulatory Focus: TReDS is an RBI-governed exchange specifically designed for MSME Invoice Discounting . It provides a transparent marketplace for small suppliers to get liquidity.

- The Capability Gap: Most TReDS platforms are not currently built to handle complex Dealer or Distribution Finance (DF) —the larger-ticket, non-MSME side of the supply chain where Veefin focuses.

- The Logic: While TReDS serves as a public exchange, Veefin acts as a private technology partner for banks. They coexist, but TReDS’s specialization in MSMEs limits its direct threat to the broader corporate distribution ecosystems Veefin targets.

2. The “In-House” Alternative (HDFC & Bajaj Finance)

The most significant competitive risk is the “Buy vs. Build” decision made by major financial institutions.

- Internal Capabilities: Institutions like HDFC Bank and Bajaj Finance have deep technical resources and have built proprietary supply chain modules internally.

- The Challenge: If the largest private banks decide that keeping this technology in-house is critical for data security or long-term cost, the addressable market for third-party SaaS providers like Veefin could be constrained. Veefin must continuously out-innovate these internal teams to remain a viable “White-Label” choice.

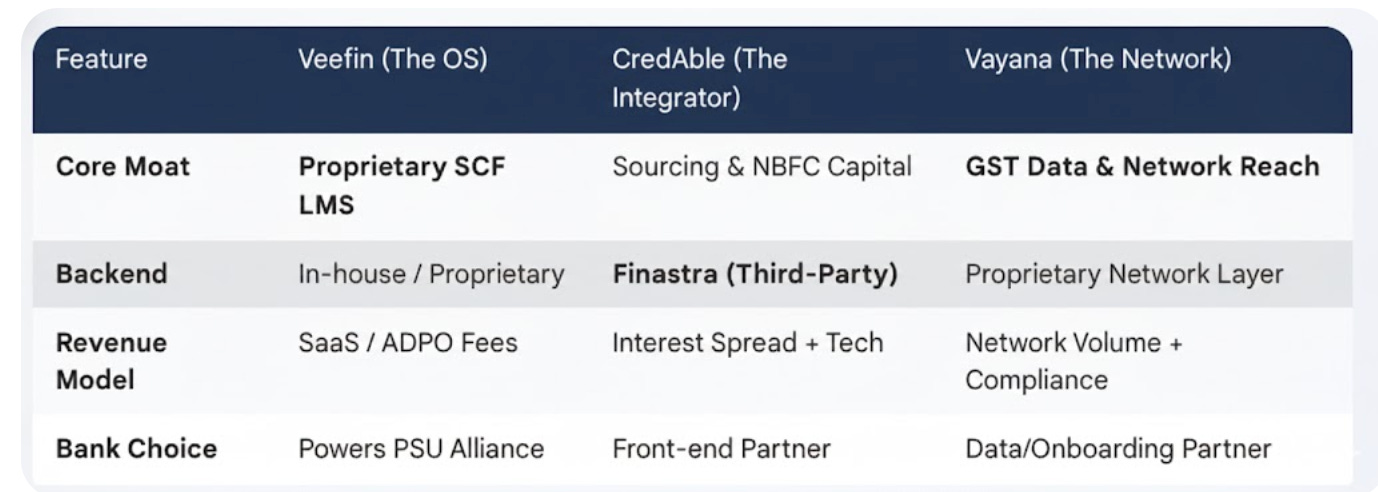

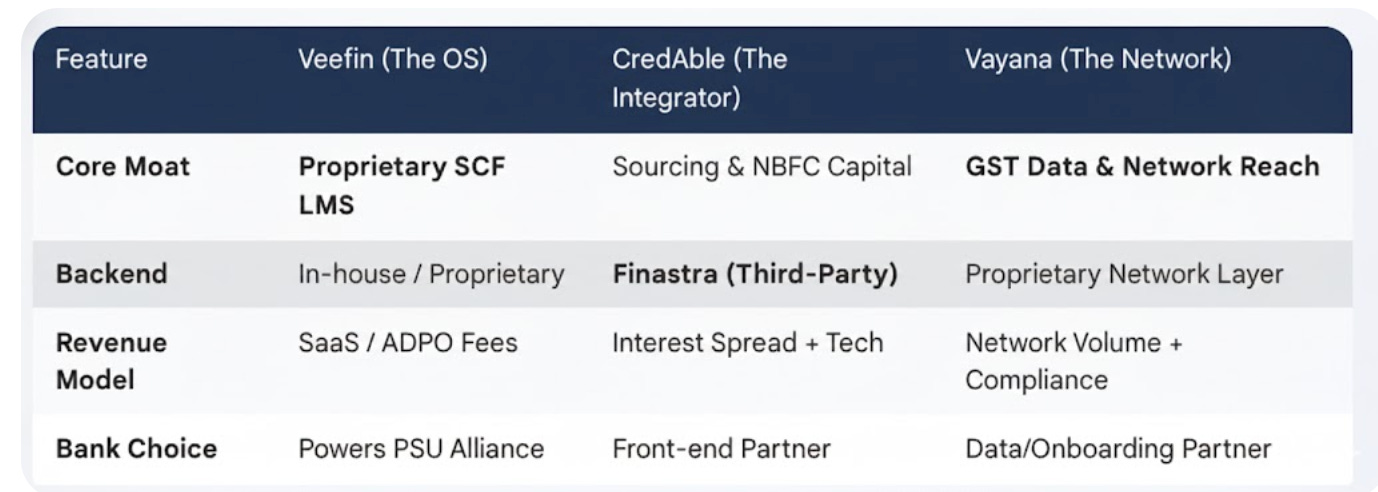

3. Peer Competition: The “Backend” Moat

In the Indian fintech landscape, the word “Technology” is often used loosely. To understand Veefin’s true competitive edge, you have to look under the hood—specifically at the Loan Management System (LMS) .

CredAble: The “Front-End” Specialist

CredAble is a powerhouse in the market, but its DNA is fundamentally different from Veefin’s.

- The Revenue Engine: Unlike Veefin, which is a pure-play tech provider, CredAble primarily operates as a LendTech/NBFC . They make the majority of their money through the interest spread on their own books.

- The Technology Gap: A critical distinction lies in the backend. CredAble lacks its own proprietary SCF Loan Management System (LMS) . While they have a world-class front-end for customer experience, they rely on a partnership with Finastra for the heavy-lifting backend booking engine.

- The “Axis Bank” Signal: Axis Bank is a strategic investor in CredAble. However, the fact that even a strategic investor like Axis does not use CredAble’s LMS for core operations—preferring to build their own digital corporate bank (NEO)—signals that the tech stack is not an end-to-end proprietary “IP” for heavy-duty banking.

Vayana: The Goliath of the Network Layer

If Veefin is the “Operating System,” Vayana is the “Infrastructure Layer.” Vayana’s strategy is built on unmatched volume and data reach.

- The Numbers (2025-26): Vayana has facilitated over $30 Billion+ (₹2.5 Lakh Cr+) in financing since inception. It has achieved a massive monthly throughput of ₹14,000 Crores .

- The Reach: The network spans 300,000+ enterprises across 3,000+ supply chains and 600+ cities .

- The Data Moat: Vayana’s core strength is its integration with the GST network , where it holds over 20% market share in e-invoicing. This data allows them to underwrite and onboard suppliers with “zero-change” to existing workflows.

The Verdict: Proprietary IP vs. Third-Party IntegrationThe risk of “Aggressive Pricing” from peers is mitigated by a simple technical reality: Ownership of the IP.

4. The NCLT Timeline

The timeline for the restructuring is subject to the NCLT (National Company Law Tribunal) approval process.

- The Delay Factor: Regulatory approvals in India can be time-consuming. Any significant drag in the merger or de-consolidation process could delay the “purification” of the financial statements.

- The Investor Impact: Until the restructuring is legally finalized, the market may continue to view the company through its current “conglomerate” lens, potentially delaying any valuation re-rating.

Conclusion: The Arbitrage of Identity

Veefin is currently a high-margin technology core masquerading as a low-margin conglomerate. The investment thesis relies on the market eventually looking past the “total” revenue to see the transaction platform hidden beneath the service legacy.

The Three Pillars of the Thesis

- The Physical Army: Veefin differentiates itself from “pure-tech” rivals by deploying a specialized sales force of former bankers. This “army” solves the Origination Problem for Public Sector Banks (PSBs) by managing the ground-level credit and risk dialogue that software alone cannot address.

- The Restructuring: The de-consolidation of the service arm is a “Purification Event.” By shifting low-margin units to an associate stake, the company removes the 15–20% margin “noise” from the consolidated books. What remains is a technology core with an underlying EBITDA margin profile of 40–45% .

- The PSB Xchange: This functions as a high-velocity “Toll Booth”. While the 30% margin is lower than the core SaaS, the transaction-led model is designed to drive the volume required for a long-term valuation re-rating.

Disclosure: Invested with High Allocation

Thesis Written On: Jan 28, 2026

Current View: Biased due to holding.

Conviction: High conviction driven by direct professional experience in the lending sector and the SaaS.

Formal Disclaimer

I am not a SEBI-registered research analyst or investment advisor. Nothing in this post constitutes investment advice, a recommendation, or a solicitation to buy or sell securities. All cited facts are sourced from the company’s official filings and the Q3 2025 earnings call

Please conduct your own thorough due diligence before making any investment decisions. Your capital, your responsibility.