SBI enrolled in PSBXalliance of Veefin solutions

3 Likes

Any tech guy who can do revenue projections considering the acquisitions they have and SCF model in PSB Alliance ? They acquired a digital marketing company and mentioned it as revenue increasing, do you think it is justified ? If it has potential and market to grow big. I mean SCF market + Technical capabilities.

1 Like

Yea genuine concerns. Any participants who are invested in Veefin Solution would like to address these please ?? Thank you.

1 Like

The company has announced a significant fundraise of approx. ₹94 crore through a mix of preferential equity allotment (~₹50.7 crore) and convertible warrants (~₹43.4 crore). While the capital infusion could support growth or expansion plans, the dilution—especially via warrants—should be watched closely. Execution and capital deployment will be key to long-term value creation.

1 Like

A reader of the original post sent the questions to the management and received a reply from them :).

I haven’t gone throught it in detail so can’t comment but here’s the post if you’re curious.

3 Likes

H1 result should clear how much these acquisitions are bringing to topline and bottom line. Also how much PSB alliance SCF is giving results.

1 Like

H1 and Full year FY2026 should bring more clarity

tech product and platform kind of business

front loading of investments will happen for sure

for product development before actual implementation revenue and license fees

hope for better FY26 and come out of ESM in FY26

PSB Alliance platform revenues they should come out with better picture

also they promised simplification of structure ( corp structure)

Today they posted about Srilanka MOU. Wondering how much is actually translating to revenue. Also psb alliance is not started yet as per the press release, it says yet to start.

1 Like

Forget the market noise. Focus on the signal !!

The signal is the blueprint for market leadership:

![]() Win the biggest clients (SBI

Win the biggest clients (SBI ![]() )

)

![]() Conquer new continents (USA & Africa

Conquer new continents (USA & Africa ![]() )

)

![]() Secure a war chest (₹94cr

Secure a war chest (₹94cr ![]() )

)

![]() Put Shareholders First (Promoter Share Gift

Put Shareholders First (Promoter Share Gift ![]()

![]() )

)

![]() First Transaction went live on PSB Exchange

First Transaction went live on PSB Exchange ![]() )

)

Act 1 was mastering Supply Chain Finance. The script was flawless. Now, Act 2 begins: A 5-year mission to build the World’s #1 Working Capital Ecosystem.

Don’t mistake their current success in SCF as the final destination. It’s the launchpad. The recent merger and promoter’s ‘shared growth’ realignment are the strategic re-tooling for this global ambition.

This all happened in just SIX months in Veefin Solutions

This is no longer a small company; it’s a fintech juggernaut in the making.

Here’s the full timeline of their recent masterclass in execution.

Sep 2, 2025: Marquee Client Win: Went live with India’s largest lender, State Bank of India (SBI), marking a landmark achievement and a massive validation of its technology.

Sep 18, 2025: Fundraising & Dilution: Raised ₹94 crores for strategic expansion and acquisitions. This resulted in a potential equity dilution of ~9.66% for existing shareholders.

Aug 2025: Global Expansion: Successfully entered two new continents with its first client wins in North America (USA) and Africa (Nigeria).

Apr - Sep 2025: PSB Co-Lending Platform: Launched the PSB Alliance co-lending marketplace, onboarding major public sector banks including PNB, Union Bank, Bank of Baroda, and Indian Bank.

Sep 12, 2025: Shareholder-Friendly Action: Promoters transferred 21 lakh shares for zero consideration to enhance minority shareholder value and increase public float.

Jul - Sep 2025: Major Tech Upgrades: Significantly enhanced its platform by launching an AI-powered underwriting module, integrating 15+ new API services, and partnering with CRIF for advanced analytics.

Aug 26, 2025: Corporate Streamlining: Simplified its structure by merging subsidiaries into the parent company for improved efficiency.

Oct 15 2025: First Transaction on PSB Exchange went live with Central Bank of India

4 Likes

Yes lot of actions but how much it is translating to top line and bottom line that is to be seen and that will move the stock. Price chart is very weak. Look like a weak result in H1. Price is even below the recent warrant/preferential.

H1 FY 2026 Veefin Investor Presentation .pdf (4.6 MB)

Think SCF. Think Veefin ~ Oldest

Think Working Capital. Think Veefin ~ Old

Think Digital Banking. Think Veefin ~ Latest

Simply increasing TAM

H1 FY 2026 Result seems mixed bag:

Positive ~

Revenue Grew Multifold

Good Cash Flow

negative~

Increase in Borrowing and Finance Cost

Increase in employee and other expense due to Acquistion

Significant increase in goodwill

1 Like

Surely will check out latest investor presentation. But looks like market is not liking both results and presentation. Stock was down 9 % earlier in morning, and now 5 %

Veefin Solutions: H1 FY 2026 Earnings Update - The Jockey Accelerates

THE OPENING GAMBIT !

Every great disruption begins not with a better spreadsheet, but with an unreasonable person who refuses to accept the status quo.

History shows that industries aren’t broken by consensus. They are broken by obsessive, passionate and visionary founders.

- Musk at Tesla, challenging a century of automotive dogma.

- Hastings at Netflix, betting against the retail giant Blockbuster.

- Jobs at Apple, insisting computers could be beautiful.

- Gates at Microsoft, turning software into a product.

- Zuckerberg at Facebook, forcing real identity into anonymous social chaos.

These leaders, these “jockeys,” share a common set of traits:

- A fanatical obsession with a fundamental problem.

- A contrarian vision that sounds insane at first.

- A relentless drive to turn that vision into engineering reality.

This archetype is well-understood when it emerges from a garage in Palo Alto.

But from Mumbai?

This is where our story pivots.

We believe this archetype has emerged !

Veefin Solutions H1 FY26 – A Measured Assessment Through Three Lenses

Standalone Numbers:-

Revenue ₹26.38 Cr (+108%)

EBITDA ₹12.56 Cr (+373%) → 47.6%

Core SCF 54% margin

OCF ₹26.52 Cr

PAT ₹6.44 Cr

EPS ₹2.77

Consolidated Numbers:-

Revenue ₹110.04 Cr (+476%)

EBITDA ₹20.14 Cr (+244%) → 18.3%

PAT ₹8.21 Cr

EPS ₹3.08 (accretive vs standalone)

Buffett’s Lens

A durable, high-return core (54% margin, strong retention) is generating surplus cash that is being reinvested without issuing equity. Acceptable capital allocation so long as the new investments eventually match or exceed the core’s returns.

Lynch’s Lens

Clear, understandable growth story: profitable SCF product → organic + inorganic expansion → larger addressable market. Revenue scale has outpaced valuation; pipeline conversion will determine the multiple.

Munger’s Lens (Inversion)

Fails only if R&D yields nothing durable, acquisitions prove value-destructive, or competition erodes the core franchise. None of these risks have materialised yet. Incentives and execution remain aligned.

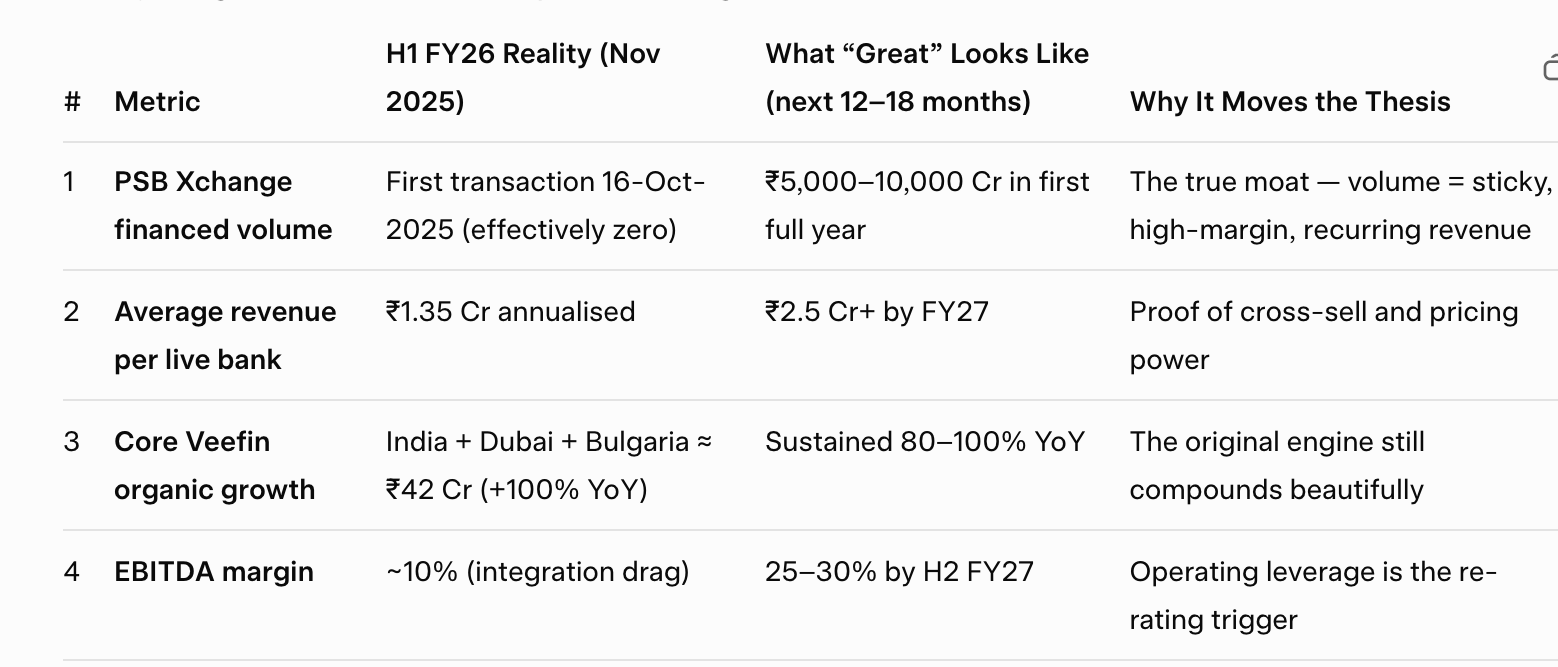

PSB Xchange – The Game-Changer Everyone Is Watching

7-year exclusive monopoly over India’s entire Public Sector lending ecosystem – now live and monetising.

Bank Status (as of 18 Nov 2025)

4 Fully Live: Bank of Baroda | Central Bank of India | Indian Overseas Bank | UCO Bank

2 Signed & Integrating: State Bank of India (SBI) | Indian Bank

→ 6 out of 12 PSBs locked in | SBI go-live in Q4 FY26 is the biggest near-term catalyst

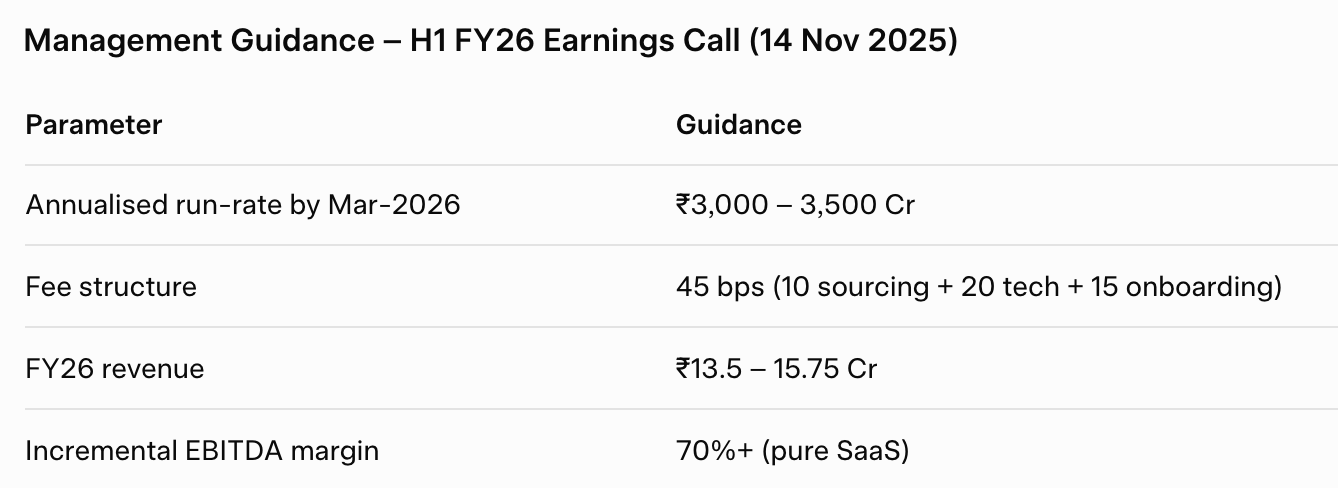

Management Guidance – H1 FY26 Earnings Call (14 Nov 2025)

Quick Rule-of-Thumb

Every ₹1,000 Cr annualised volume = ₹4.5 Cr revenue | ₹3.2–3.4 Cr EBITDA

Reality Check

The full 45 bps is already being billed to the four live banks since October 2025. The 20 bps technology fee is non-negotiable — Veefin owns and runs the platform end-to-end.

Bottom Line

At guided levels, PSB Xchange adds ~3–4% to FY26 consolidated revenue but 8–10% to EBITDA growth because of its exceptionally high incremental margins.

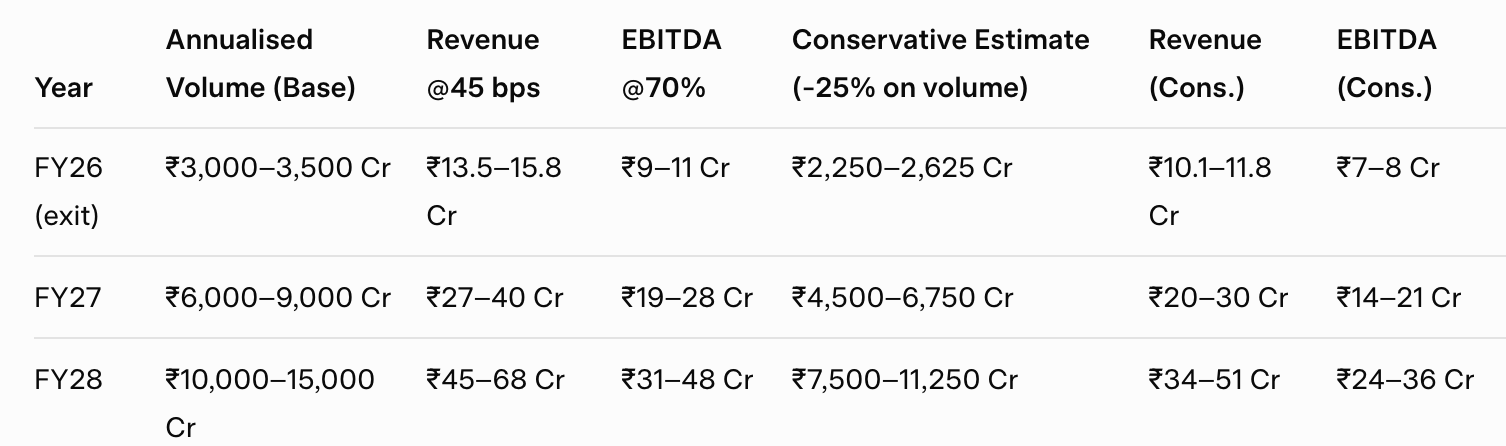

Food for Thought – Plausible Scaling to FY28

(Management has guided only FY26 exit run-rate; beyond that we use simple, transparent assumptions)

Even under the more cautious 25% lower volume scenario from day one, PSB Xchange still contributes ₹10–12 Cr revenue in its debut year and scales to ₹34–51 Cr by FY28 — representing 10–15% of Veefin’s total revenue at 70%+ margins.

The base case, which assumes steady onboarding of the remaining PSBs plus SBI’s full impact, looks the most realistic given the exclusivity and India’s SCF market growing at 15–20% CAGR.

This is no longer a pipeline story. It’s live, exclusive, and scaling fast.

SBI go-live = the 2026 re-rating trigger.

The Leadership Edge: They Already Won—Now They’re Playing a Different Game

14 leaders. 300+ years in the trenches.

Logos: Kotak, HDFC, RBL, Citibank, Oracle, Finastra, HSBC, Deutsche Bank, Deloitte.

These aren’t hires.

These are the people banks called when a $10B trade-finance engine was on fire.

They’ve survived Y2K, Lehman, demonetisation, and Covid supply-chain chaos.

They know every regulatory landmine, every core-banking quirk, every reason deals die at 11:59 p.m.

Most fintech teams are still learning what a Letter of Credit is.

This team has issued, digitized, and risk-scored billions of them.

They could each run their own company tomorrow.

Instead, they all bet their reputations on VeeFin.

When talent this deep pools in one place, it’s rarely an accident.

It’s a massive, quiet vote of confidence in what’s being built.

That alone is worth watching closely.

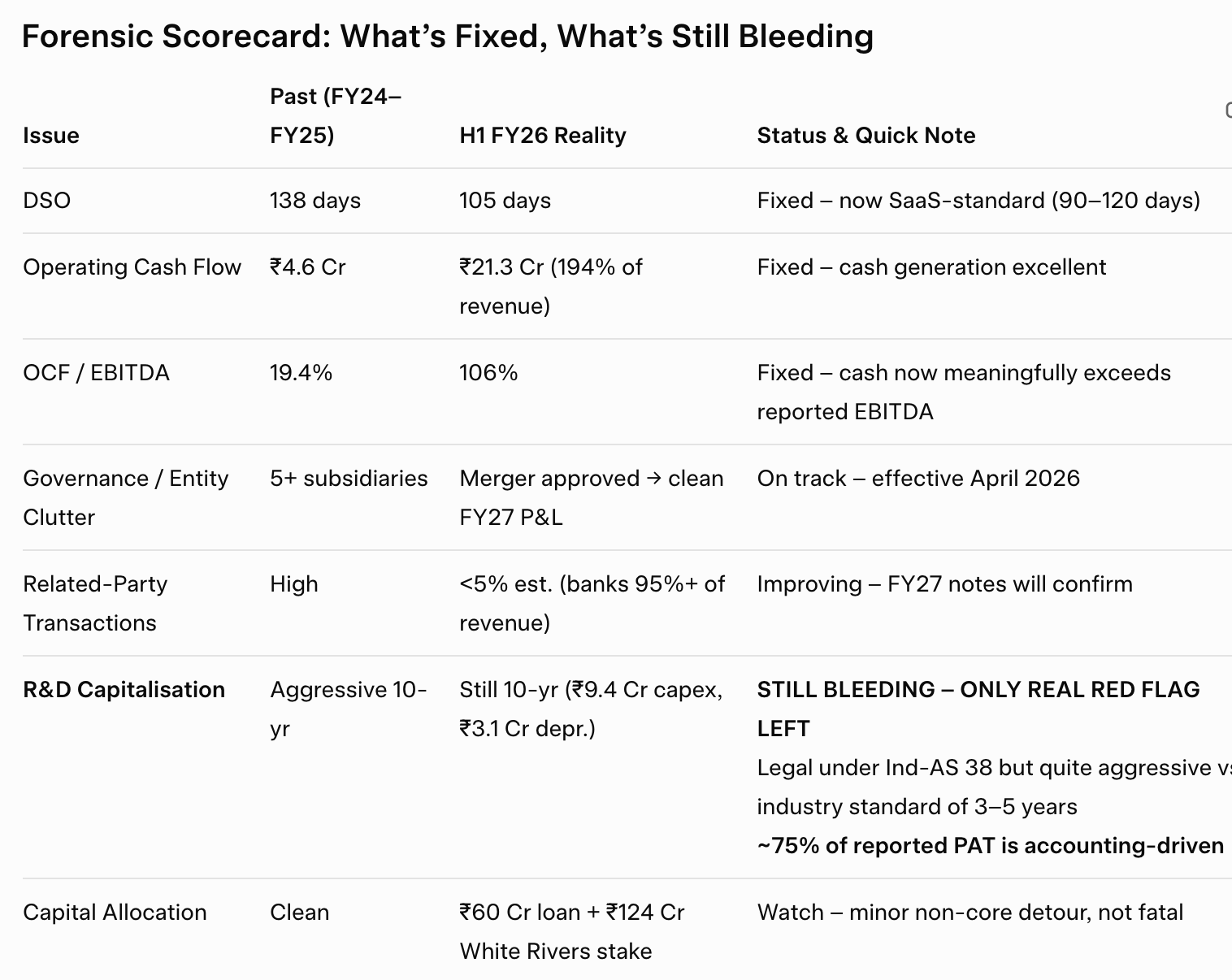

Forensic Scorecard: What’s Fixed, What’s Still Bleeding

(H1 FY26 – November 2025 | 100% sourced from Veefin’s own BSE filings & deck)

Most of the historic baggage is gone.

Cash conversion is now elite, operations are clean, and growth is real.

Only one thing still clouds the picture: the 10-year R&D amortisation policy — fully legal, but far more aggressive than the 3–5 year norm used by every serious Indian SaaS peer. Until that lever normalises (expected FY27), roughly three-quarters of reported profits remain accounting-driven.

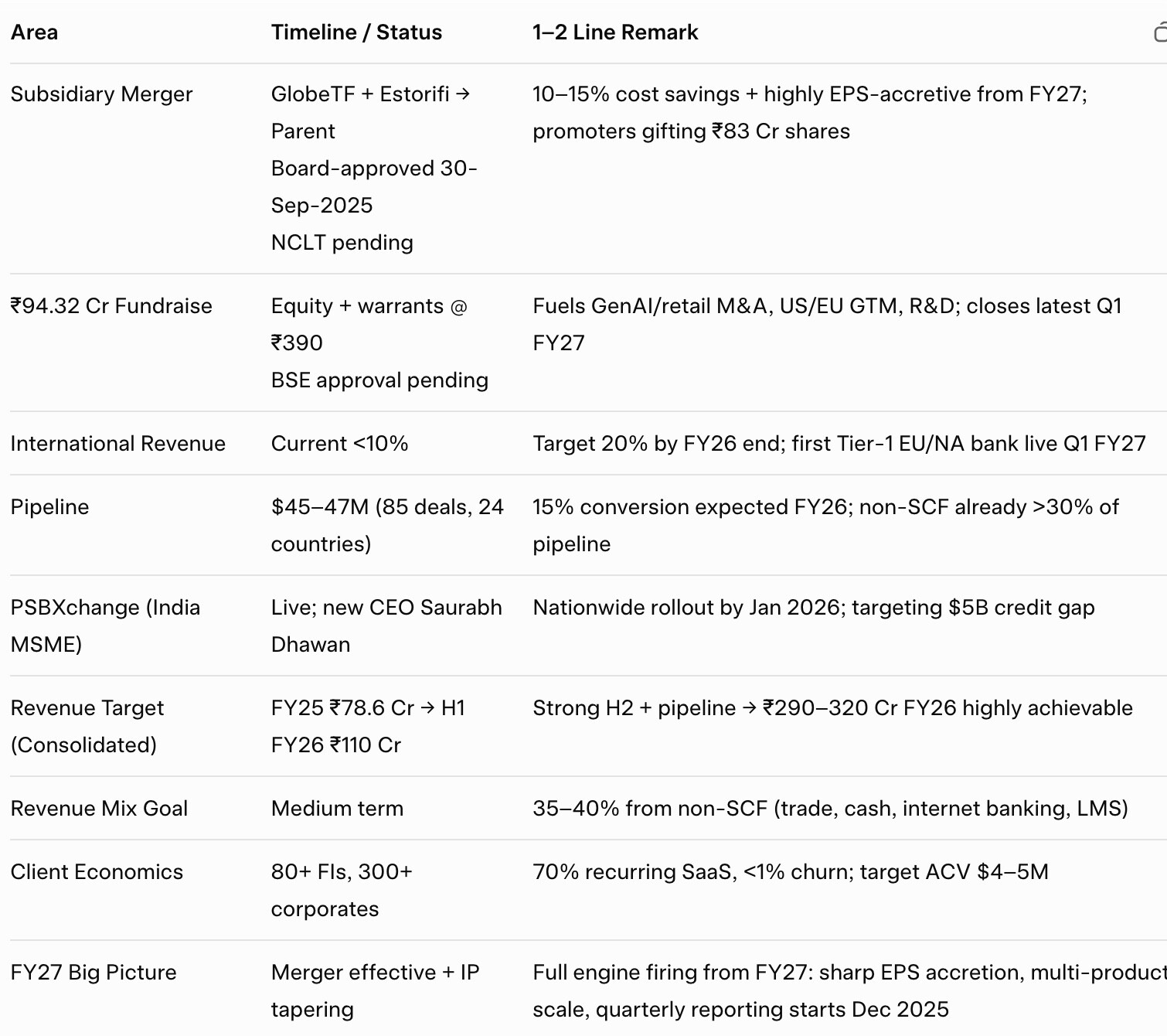

Near Term Playbook (FY 2026 & Fy 2027 Roadmap)

- ₹94 Cr War Chest Locked

Fresh capital @ ₹390/share + warrants → 40% M&A (GenAI/retail), 30% US/EU GTM, 20% R&D, 10% WC. Closes Q1 FY26.

- Subsidiary Clean-Up

GlobeTF + Estorifi merging into parent → 10–12% cost savings, zero dilution, promoters gifted ₹83 Cr worth shares. NCLT pending.

- Western Push

First Tier-1 EU/NA bank live in Q1 FY26 → Europe & North America unlocked. International revenue to 15–20% by FY26-end.

Medium-Term Vision (FY26 Focus)

- 6 New Products Dropping

Veefin 4.0 stack: GenAI fraud (Walnut AI), green lending, securitization, retail lending, marketplace APIs.

- Market to Conquer

$10T global SCF gap | $5B India MSME gap via PSB eXchange → deep-tier supply chains + fintech/ERP onboarding.

- Scale Targets

Standalone: 75–85% YoY → ₹137–146 Cr

Consolidated run-rate → ₹200–220 Cr

Non-SCF revenue → 35–40%

Client ACV → $4–5M

Risk Ring-Fenced

Veefin Capital (NBFC) isolated | Infini stays pure services | No new buys till integration done.

One-Line Verdict

54% margin cash cow + ₹94 Cr fuel + Tier-1 Western wins + 6 killer products = Veefin is India’s fastest-growing profitable digital-lending platform.

Think Digital Banking. Think Veefin.

Game on. 🚀

The Lynch, Munger & Buffett Checkboxes

Peter Lynch would love it

→ A business any teenager can understand, growing >200% from a base that is still tiny.

Charlie Munger would nod at the moat

→ PSB Xchange is a government-aligned network effect that no private competitor can copy overnight.

→ Veefin 4.0 single platform = astronomical switching costs once a bank is live.

Warren Buffett would say “not yet”

→ Still burning cash on growth and acquisitions, but the unit economics (80% gross margins, 30–45 day cash cycle, ₹1.35 Cr → ₹3–5 Cr per bank) scream future cash compounder the moment the spend tap turns off.

The Only 4 Numbers I Actually Care About

(Everything else is noise in enterprise banking SaaS)

Conclusion

Veefin has built a demonstrably profitable, high-margin core in supply-chain finance SaaS and is now systematically expanding into adjacent lending and working-capital products. The acquisitions have dramatically increased the revenue base but introduced short-term margin dilution and execution complexity. The upcoming amalgamation, pipeline conversion pace, and margin recovery in FY27 will be the decisive variables.

Investors who believe management can execute the stated roadmap will find the current valuation reasonable for the embedded growth optionality. Those who require greater near-term visibility or are uncomfortable with acquisition-related integration risk may prefer to wait for additional proof points.

As always, readers must conduct their own thorough analysis of the financial statements, earnings transcript, and subsequent quarterly updates before reaching any investment conclusion.

Disclaimer

- I am not a SEBI-registered research analyst or investment advisor.

- I hold a long position in Veefin Solutions Limited (BSE: 543931) and therefore have a vested interest.

- Nothing here is investment advice, a recommendation, or a solicitation to buy/sell securities.

- All facts are from the company’s official filings and earnings call dated 13–14 November 2025.

- Do your own research. Your capital, your responsibility.

7 Likes

Beautiful analysis and compilation.

I see problem in Veefin new acquisitions, are they really brining in something on table ? Atleast consolidated numbers are not suggesting so.

8 months already up in this FY , no synergy has come up either as of deals notifications to exchanges.

Lets see how things show up. Invested at higher levels. Not averaging as how far PSB exchange can scale, company is not giving an idea.

1 Like

Update to My post: Veefin Solutions: H1 FY 2026 Earnings Update - The Jockey Accelerates

As I am unable to edit my original post, I am providing this update as a reply with three key insights from the earnings call:

1. Western Push

- First Tier-1 EU/NA bank live in FY2027, unlocking Europe/North America.

- Recent ₹94 Cr fund raise (Sep 2025) funds this; full entry targeted for FY2027.

2. New Products

- Launching six: Trade Finance, Cash Management, Corporate Internet Banking, Retail Internet Banking, Fraud & Risk Solutions, Loan Management System (LMS).

- Aimed at ecosystem build and global rollout.

3. Cross-Sell Philosophy

- 70%+ incremental EBITDA margins on additional enterprise products cross-sold to existing bank clients.

- Enables multi-product sales to the same bank, driving ARPU uplift.

4 Likes

- Launching six: Trade Finance, Cash Management, Corporate Internet Banking, Retail Internet Banking, Fraud & Risk Solutions, Loan Management System (LMS).

These 6 are like entire banking IT. So like complete IT banking solution. Looks like entering everywhere and previous verticals yet to show results.

Couple of updates related to company:

- 19 Nov 2025: Tech/business press reported that Sorabh Dhawan has been appointed CEO of PSB Xchange (PSB Loans in 59 Minutes), a public-sector bank digital-lending platform built on Veefin’s technology stack. I think he is from SGFinserve.

- 24 Nov 2025: Veefin announced the appointment of fintech veteran Niraj Vedwa as Senior Advisor, aimed at accelerating global expansion and deepening partnerships for its digital lending and supply-chain finance platforms.

Seems things are slowly setting up nicely now.

Disc: Invested

1 Like

They are FIN + Tech but why they even fail to project their own numbers in terms of projections of revenue and PAT. They are promising big solutions, big continuous acquisitions. But where is synergy and numbers ?

Any financial projection you have fy 26 and 27 ?

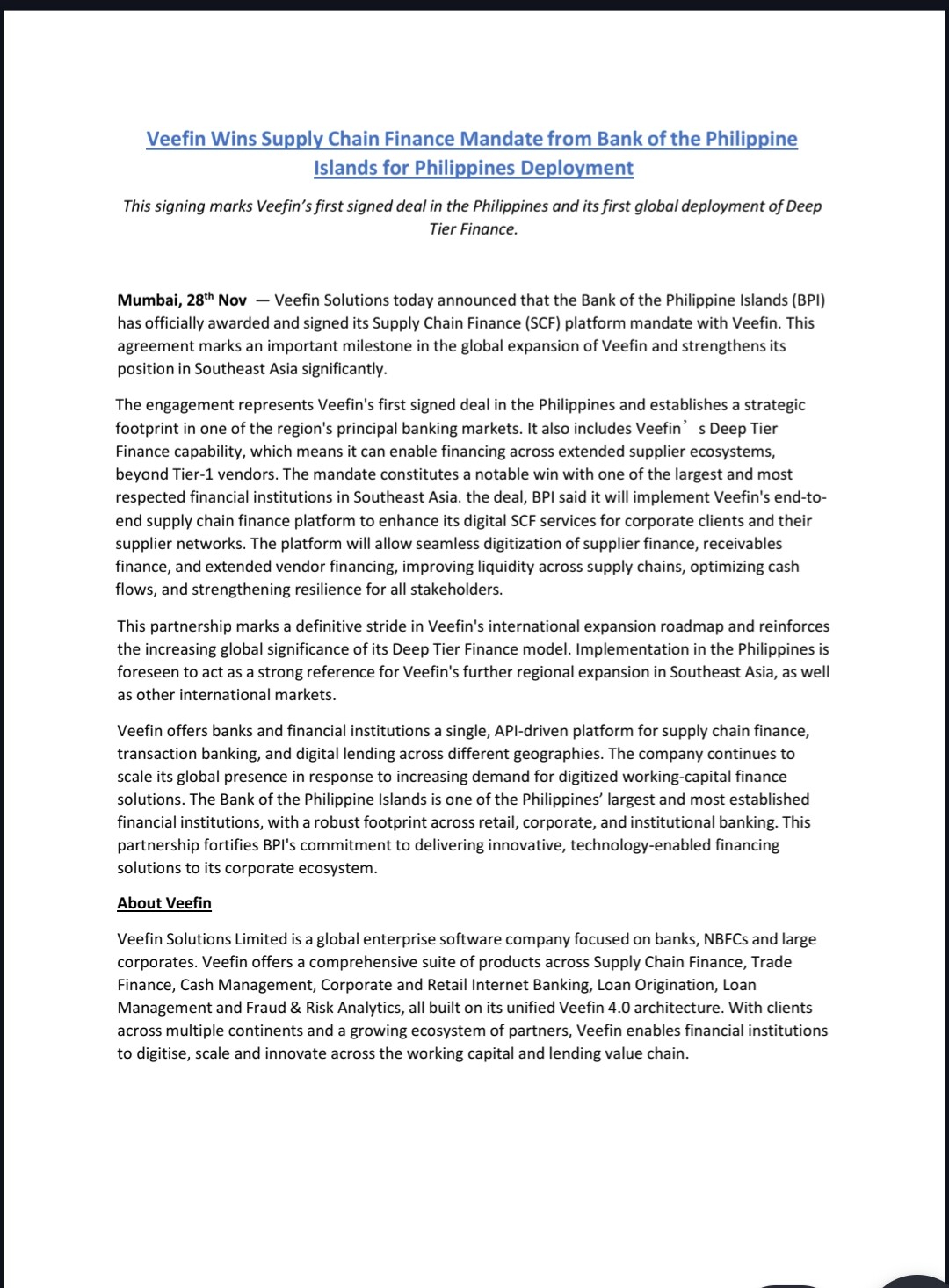

Veefin Solutions: Co Wins Supply Chain Finance Mandate From Bank Of The Philippine Islands For Philippines Deployment .

This Signing Marks Veefin’sfirst Signed Deal In The Philippines And Its First Global Deployment Of Deep Tier Finance

Disc: Invested

Haven’t they shared guidance for FY 26 standalone and consolidated wise ?

Standalone Rev Guidance. 75-80 Cr

Consolidated Rev Guidance 280-300 Cr

My Two cents on Product Tech and M&A

I. The Reality of Product Tech (Speed vs. Perfection)

• Tech is Perishable: One can’t take eternity for perfection. A perfect product delivered late is a failed product.

• Agile Beats Rigidity: Detailed, static projections quickly become obsolete. One builds by listening, not by rigid blueprints.

• Launch MVP Now: Focus on a Minimum Viable Product to get real feedback fast. Working software trumps exhaustive documentation.

• Iteration is Success: Continuous cycles of feedback and emphasized textdeployment are mandatory. One’s strength is the pivot, not the plan.

II. The Reality of M&A Synergy (Pacing vs. Rushing)

• Synergy is a Process: Integration is a marathon, not an instant flip of a switch. Rushing creates chaos and technical debt.

• Focus on Foundations: One must prioritize securing core assets and stabilizing systems first. Stability is the first synergy.

• Protect the Value: One must not break the acquired asset by forcing immediate, messy integrations. One paces to protect the product and the people.

• Track Milestones, Not Micromanagement: One reports on verifiable value metrics, not every daily cross-departmental detail. One delivers progress, not speculative projections.

1 Like