It seems there was no GQG Partners in trade today at Vedata counter; the stake sale by the Promotor group entity, Finsider International was through Open Market.

I find this very interesting:

| No. of Shares | |

|---|---|

| Vedanta | 3,71,72,06,239 |

| HindZinc | 4,22,53,19,000 |

| Vedanta Holding in HindZinc | 2,74,31,54,310 |

| HindZinc Price | 721 |

| HindZinc M’Cap | 3046454999000 |

| Vedanta’s Value | 1977814257510 |

| Value Per Share for Vedanta | 532 |

8 Likes

Does Vedanta think that their debt doesn’t pose a big risk in future post the demerger and are hence distributing such hefty dividends?

Are the hefty dividends in recent years aimed at boosting investors/bond holder confidence in the fiscal strengths of their organization?

Answer to your last question is an obvious Yes.

2 Likes

Dividends is the way of rewarding shareholders with real cash. (Not rewarding to salaried at higher tax bracket though). The promoter is a big shareholder, so inherently he benefits from it.

Privatize the profits socialize the losses - mantra of capitalism.

4 Likes

Vedanta paying heavy dividend was to cover interest cost of parent company …as parent company has huge debt…

5 Likes

Found this on Youtube, would love members’ opinion on the de-merger if you’re tracking :

The Group’s debt repayment has been heavily supported by dividends from Vedanta Limited. While current profits are helping to service the debt, the long-term sustainability of this arrangement remains uncertain. With Vedanta now undergoing a demerger into several entities, this restructuring may offer a temporary opportunity to attract funding from investors and lenders to help the parent company maintain its debt obligations. Welcome for more thoughts on this!

2 Likes

Vedanta Limited has announced the allotment of three series of Indian Rupee (INR) denominated unsecured, redeemable, rated, listed, non-convertible debentures (NCDs) on a private placement basis, totaling ₹5,000 crore

Series 1 Debentures: ₹2,400 crore

Series 2 Debentures: ₹1,750 crore

Series 3 Debentures: ₹850 crore

Total Issue Size: ₹5,000 crore

More money and more to pay

1 Like

Vedanta-Final-20250709.pdf (5.1 MB)

Most of it has already been in open to public. I don’t think much has been shaken. Not following the stock, experts can comment.

2 Likes

JP Morgan considers Vedanta to be “cheap” within Asia and within the EM metals and mining space, with healthy EBITDA generation (~$5 billion run-rate), improving funding access (~$1 billion bank loans have been raised by VRL in FY26), and attractive yields (8-10%).

it Prefers

VEDLN (Vedanta’s) 29s (102.3 offer, 10% YTW)

VEDLN 31s (103.4 offer, 10.2% YTW) along the curve,

Neutral on VEDLN ’33s (99.14 offer, 10% YTW).

I think all shorting research report will have “scam”, “ponzy scheme”, “heist” etc. and them selves being “activists” if not “governor” , “kings representative”…Me know little on these bond things, me like dividends, i think AA will manage to do dividends going forward, invested from 2022 lows..holding.

Frase Perring is famous ..was once mentioned in UK’s House of Commons.Aidan Lau could be an expert on mining.

3 Likes

expand on this please.

1 Like

If i would try to describe all the details & wht i read into those details…It’d be like a conspiracy or speculation. ![]()

Search for

- Fraser Perring -Babcock International- Boatman Capital - UK parliament.

- Aidan Lau - Syrah Resources - Konkola copper - (cant search much on his background/history…everything comes up as a speculation)

I am assuming there would be some Cayman Island, hedge fund etc involved somewhere based on wht i read about hindenburg saga…we may see more on this if any news agency decides to figure it out.

I think, Vedanta’s debt is a known issue to investing community, to be seen how AA manages it going forward..demerger was a spin most of us knew.

In my opinion, whats important to note is recent goverment annoucements on mining push & possible benefits to Vedanta > https://www.aninews.in/news/business/govt-encouraging-private-companies-to-mine-critical-minerals-overseas-for-domestic-needs-minister-g-kishan-reddy20250703154503/

(i see this as a something more than magnets/rare earth covering many non-ferrous minerals)

Vedanta stands to gain from India’s REE push / National critical mineral mission, through mining access, subsidies, market demand and its expertise.

However, Viceroy’s bond shorting, SPOOKS LENDERS & may raise borrowing costs and limit capital access, though government support may offset some financial strain, its to be seen how AA navigates the funding requirement.

3 Likes

This article says exactly what I always wanted to say. Many institutional investors and us retail investors have seen the debt burden and other red flags already. The thing is it’s been so many years, no regulators came out and solve the misconduct of the company and this keeps going, when is it gonna stop?

https://www.livemint.com/mint-top-newsletter/companyoutsider.html?webview=true

Why no one blows the whistle until a short-seller turns up

Below is taken from the article:

The reaction to US-based short seller Viceroy Research’s scathing report on the Vedanta Group was as predictable as it was performative. The company, not surprisingly, called the allegations “baseless”. There was also the familiar barrage of nationalist rhetoric summed up by former Rajya Sabha MP and BJP national executive member Swapan Dasgupta, who tweeted: “Is there a concerted attempt by dodgy US financial entities.research organisations to undermine India’s corporates/financial institutions?”

But strip away the outrage, and the uncomfortable question remains: why did it take a foreign short-seller to say what no one in India’s financial ecosystem had the courage or incentive to? After all, as Vedanta’s CEO Deshnee Naidoo admitted, the points raised in the report are not new and have been previously disclosed to shareholders.

Viceroy’s dossier alleges opaque structures, questionable related-party transactions, and fragile debt positions across the sprawling Vedanta empire. You don’t need to agree with every bit of the report. The key issue is that in a market ecosystem populated by regulators, exchanges, research analysts and institutional investors, why was such scrutiny absent until a short-seller showed up?

The discomfiting answer is the lack of incentives. Reviled they may be, but short sellers are among the few market participants who have a genuine incentive to unearth problems inside companies. Since they make money when stock prices of their target companies fall, they are financially motivated to find what others ignore. Their motives are certainly not altruistic, but they drive the kind of transparency and accountability that almost all other market players shy away from.

Of course, short-sellers can be wrong. They exaggerate, cherry-pick and even manipulate. But their work, when rooted in data and grounded in fact, performs a critical function. They are often the only ones willing to publicly accuse a company of fraud — because they have the most to gain if they’re right, and the most to lose if they’re wrong.

Could the questions that Viceroy posed to Vedanta have been asked by its independent directors? Or its bankers? Or rating agencies? Or large institutional shareholders (foreign institutional investors (FIIs) and domestic institutional investors (DIIs) who together hold over 27% stake in Vedanta Ltd)? Possibly. But the brutal truth is that for none of them did the risk-reward trade-off make sense.

Any thoughts on this everyone?

2 Likes

Out of curiosity, At what point do regulators step in?

Mostly after the damage is done or something breaks / tangible happens.

Some Institutions filter such stocks out and don’t touch them with a 10 ft. Pole by branding them as ch*r promoter (a la Marcellus). They have no bone to pick.

Next up we have independent directors, either they are “yes men” or resign if there’s too much conflict.

The institutions that have stake in the company won’t call out as they are living in glass houses and won’t throw stones.

Independent analysts or Research orgs are at risk (a la Nitin Mangal) if they expose something and it gets viral.

5 Likes

Here comes another allegation:

This is previously unknown financial link between Vedanta and Serentica Renewables, a company tied to the Agarwal family. They suggest Serentica may be used to divert funds and obscure liabilities, raising serious concerns about transparency and governance within the Vedanta Group.

It’s true—red flags around Vedanta have been waving for years, and yet regulators stayed silent. But this new report doesn’t seem just another warning now, it’s a revelation.

We’re not talking about vague concerns anymore. This is more of a concrete, previously hidden structure involving Serentica Renewables, allegedly used to channel funds away from Vedanta under the ESG banner.

So now the question is:

Will regulators finally act, or will this be another case of “too late, too quiet”?

Because if this is allowed to slide, what message does that send to every other conglomerate playing fast and loose with governance?

It’s about accountability.

2 Likes

Let’s see how Sebi response:

2 Likes

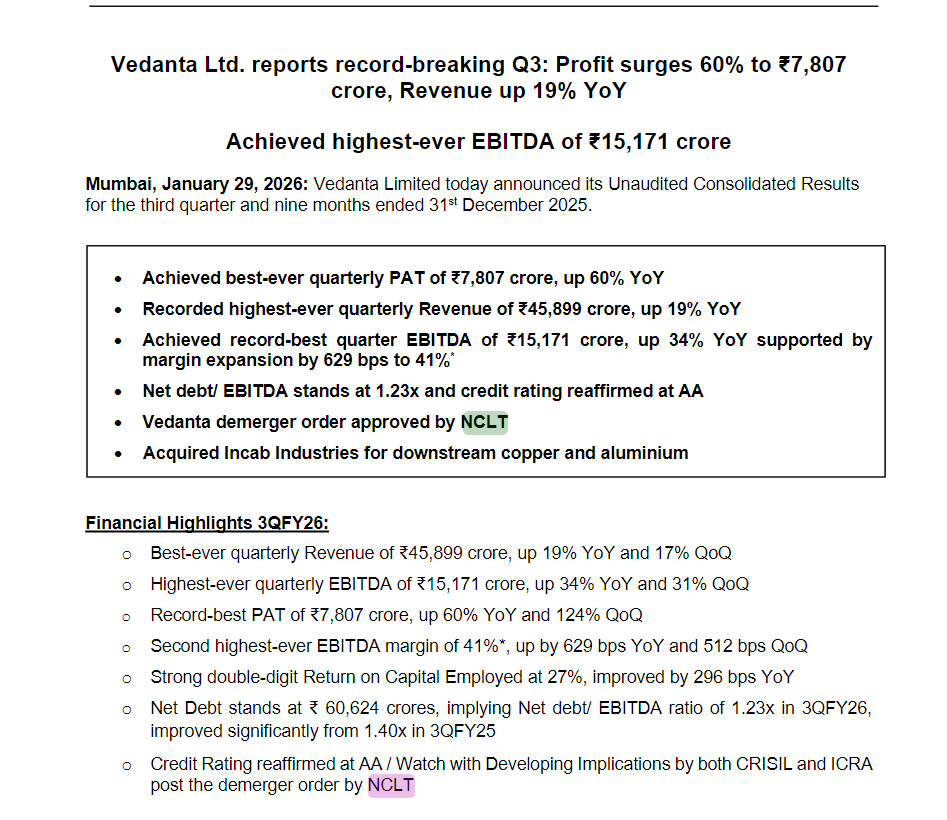

Metals price are rallying up sharply which will show up in Q3 results of many metal companies just like vedanta.

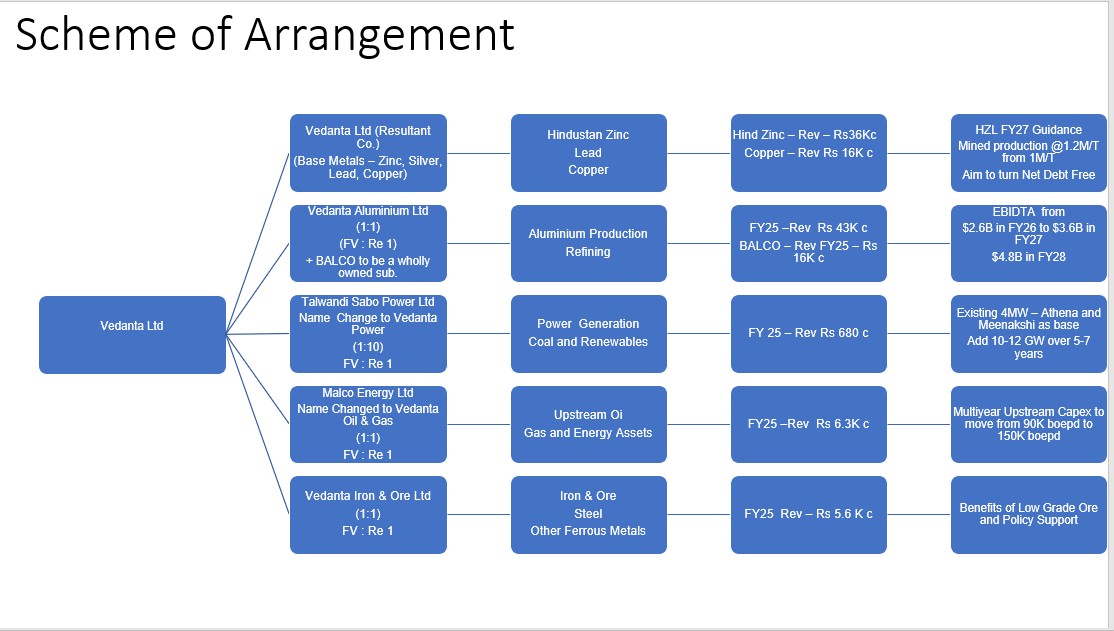

Vedanta demerger has been approved by NCLT on 9th Jan 2026. Lets see what happens next.

2 Likes

Vedanta is being split into five distinct listed companies, each carrying a core metal vertical: Record date - May 2026

-

Vedanta Limited (base metals) – retains Hindustan Zinc and other base‑metal assets, such as Copper/Lead.

-

Vedanta Aluminium –aluminium business, including Jharsuguda, Lanjigarh and future expansions + importantly the BALCO subsidiary shifts under the Aluminium business

-

Vedanta Steel and Iron – the ferrous cluster – imp - iron‑ore mining via Sesa Goa and steel assets under Sesa Steel

-

Talwandi Sabo Power (Vedanta Power) – 4‑GW thermal‑power‑plus‑ supplying power to the group and external consumers.

-

Malco Energy (oil & gas) – upstream hydrocarbon assets under Cairn Oil & Gas, targeting 150,000 boepd over medium term.

Risks - Imp to see how debt would be carved out over all the 5 entities – await details on this imp element

Metals are highly cyclical and influenced by Policies.

Every once in a years compliance issues have cropped up

Invested over years, hence biased: pls do your own due diligence

3 Likes