Will this news have any impact on vedantas stock in your opinion?

Disc: Not invested, just very interested in the Chip scene in India.

If I would have been a Vedanta investor I would have been relieved, according to me getting into the Chip business is deworsification for the company, I mean Chip manufacturing is a high-cost, high-tech, highly specialized business, with very concentrated supply chains. I mean just setting up FAB requires 5-10B USD.

Of course, I know the company is still looking for partners and they might be able to find some manufacturing and tech partners, and still get into this business but I don’t think it is tactful and will not be profitable for a long time, I mean China[not Chinese companies] is trying to develop own chip manufacturing plant, for at least 2 decades with all the backing of corporate espionage, state machinery, and almost limitless money, but they are still just trying, so I am very much skeptical that Vedanta can do better, or India for that matter, of course, if we are able to get big chip manufacturing companies[Intel, Micron, Samsung, Maybe TSMC] setup manufacturing in India with some Indian companies as Partners then we might be able to get some expertise with tech transfers and whatnot, get chip manufacturing of the ground in India, but most the big chip companies are already investing heavily in US, Europe, Korea, with better infra, more incentives from the governments etc, so we have to see, government of India is ambitious and they are trying, but it just so hard to get into this.

In summary, I am not rosy about the chances of Vedanta in Chip Manufacturing with all their debt problems as well, but they are least trying I don’t see any other company srsly trying even.

PS: Tata Electronics is much stronger and I would bet on Tata Electronics if they get into this, they have some expertise through Tejas, and they are very smartly integrating themselves into the supply chain with Apple product manufacturing, and what I have read they are working internally to participate in chip manufacturing, but nothing concrete as of now.

Read Chip War it is a nice book to understand Chip manufacturing, its history, and many other things.

4 Likes

No large chip manufacturer will set up a plant anywhere outside their own home countries as chips have become strategic assets. It’s not just about infra facilities or costs.

Samsung for example, despite having business ties with India in electronics / consumer durables categories, has decided to invest $228Bn in South Korea itself despite high cost.

1 Like

Whole heartedly agreed.

4 Likes

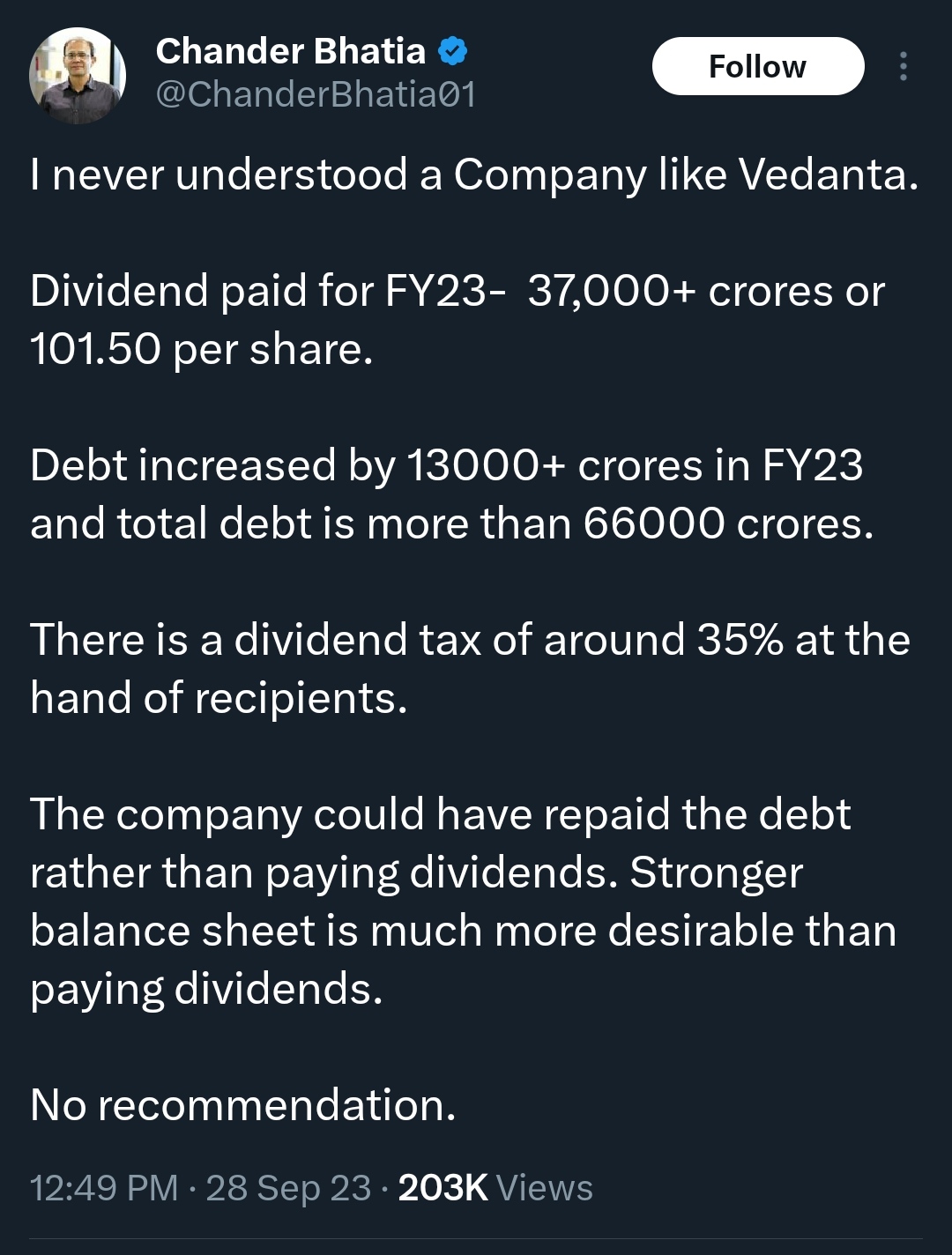

zinc price is again down to pre covid level…income will not be there to pay thse huge dividends… zinc, aluminium crude need to go back up for them to pay big dividends…

1 Like

Vedanta Promoters has increased royalty rates from both Hindustan Zinc and Vedanta Ltd to around 3% of revenue. And it can go up further. Based on this almost 35-37% of profits can be taken out without giving anything to minority shareholders. Now they have also resorted to selling Vedanta shares itself to raise money. Dividend could be substantially power going forward.

3 Likes

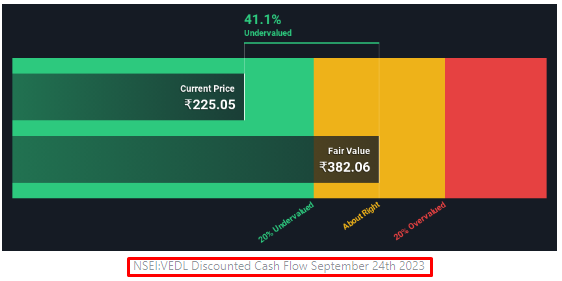

By two stage DCF following is presented, as valuation, at above article.

if valuation is attractive, what is not attractive these days ?

Vedanta demerger announcement:

“” In pursuit of this goal, the Vedanta Limited Board approved a pure-play, asset-owner business

model that will ultimately result in six separate listed companies, namely:

• Vedanta Aluminium

• Vedanta Oil & Gas

• Vedanta Power

• Vedanta Steel and Ferrous Materials

• Vedanta Base Metals

• Vedanta Limited

The de-merger is planned to be a simple vertical split, for every 1 share of Vedanta Limited,

the shareholders will additionally receive 1 share of each of the 5 newly listed companies.

Rationale for Demerger:

- Simplifies Vedanta’s corporate structure with sector focussed independent businesses.

- Provides opportunities to global investors, including sovereign wealth funds, retail

investors and strategic investors, with direct investment opportunities in dedicated

pure-play companies linked to India’s remarkable growth story through Vedanta’s

world class assets. - With listed equity and self-driven management teams, these demergers provide a

platform for individual units to pursue strategic agendas more freely and better align

with customers, investment cycles and end markets. - Enables to better highlight, and for the market to more easily value, the remarkable

technological advances, environmental stewardship and robust growth stories within

Vedanta’s family of companies. “”

Curious to know what will be the valuation of demerged entities. In this case will the sum of parts be greater than the single entity in future?

D: Not invested, Just tracking the news.

2 Likes

With the demerger, the debt would be proportional to the size of each entity? And some would be definitely worth less than the debt it is saddled with? Unable to pay and shifting it on to shareholders?

3 Likes

may be idea to sell some verticals is easy … to pay off debts of parent company… ?

Vedanta’s Anil Agarwal is ambitious. Wait to be seen if his gamble pays off. Inspiring to read.

Anil Agarwal ‘Invites Investors’ As Alumina Refinery Expansion Begins ![]()

So how does one play the Vedanta story from here?

It’s a given that the promoter Anil Agarwal does not hold minority shareholder interest anywhere close to his heart. The hefty dividends paid were due to the promoter’s need for cash to service the debt. It is also a given that no meaningful investor will invest in the Company in its current avatar. The Company did sell some stake in the recent past n the share price promptly took a drubbing! So any further stake selling by the promoter is not really an option for want of any takers, But therein lies the opportunity. Vedanta, as already proposed by the Co. recently, (link attached below) will have to be split up into many focussed commodity specific smaller companies & sell controlling stakes in a couple of them to raise any meaningful capital that could take care of the stretched balance sheet. The Co. is sitting on a number of prized assets which would find numerous takers if the current promoters are out of the equation! That seems to be the only possible way out for the promoters to get out of this debt trap.

If that were to happen there could be substantial gains for investors to be made over the next 12 months or so. The current price levels of about 215 appears reasonable to enter, but the basic investment thesis assumes that the demergers will go through.

(For some reason there seems to be two threads for Vedanta)

5 Likes

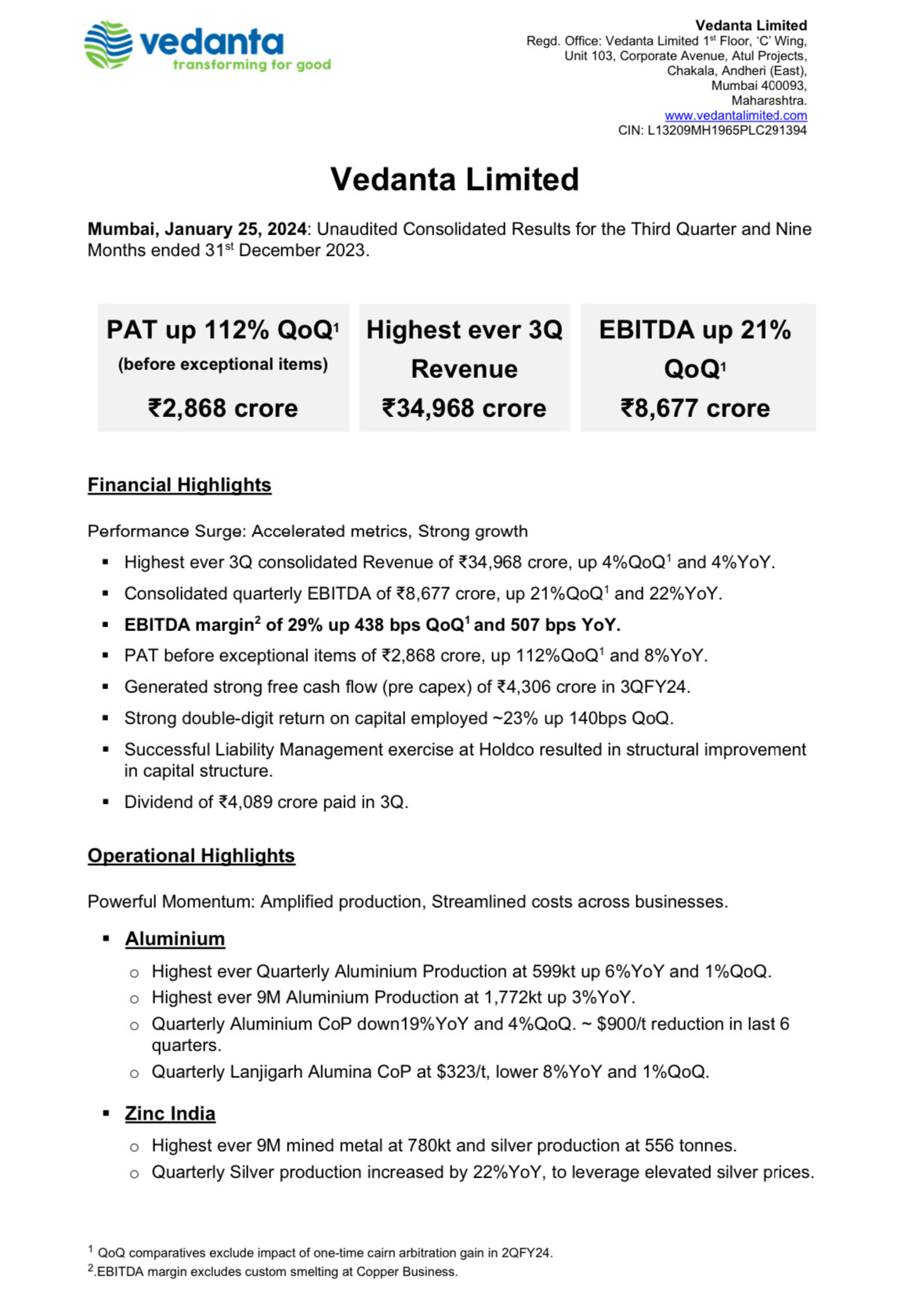

Any follow up on this?

“VEDL: Vedanta: 97% bondholders approve $3.2B restructuring

-

Vedanta Limited: Bondholders approve restructuring of $3.2 billion worth of bonds More than 97% of bondholders of Vedanta Resources VRL approved the restructuring of $3.2 billion worth of bonds due to mature in the next three years.

-

The company said in a statement that the restructuring will reduce its debt by $1.1 billion and extend the maturity of the bonds by an average of three years.

-

Vedanta’s shares were trading at Rs 263.80 on the National Stock Exchange on January 3, 2024.”

This is indeed good news for Vedanta shareholders as the Promoters now have enough time to successfully split the company into multiple focused entities which could create enormous value.

5 Likes

Any idea about the timeline of demerger?