I’m not disheartened with latest no…management I think doing the best they can…sometimes market dynamics tests even big businesses patience…titan I remember has also gone trough long hiatus in its stellar journey…what matter me is just management with leading brand where consumers are upwardly mobile…not many consumer businesses are available having gross margin of around 67%…hope south India campaign with Ram Charan brand ambassador works out…my logic is simple…remain with leading brand in every sector…

disc. invested,vested, 3% portfolio.

Comments are encouraging, but I would like to add a point-of-investment thesis on my end. The bet is on the premiurization and management strength and, of course, the liquidity available at the free float. They are doing great business in their niche area, with increasing foot traffic and the expansion of stores. They operate on a franchise model, which is asset-light, and of course margins have not changed with the addition of so many new outlets. The crux of margin impact can only be seen in the EBO’s, but with Twamev stores, the asp ticket is about in the range of 30k to 40k, and selling the goods of 10-15qty itself is sufficient to overcome the expenses of individual stores, and the rest would lead to profits. I have visited Twamev EBOs in Hyderabad. The collection is extremely good, and the price point starts at 30K+. The area in which they operate this store is elite. Of course, the footfall may be less for Twamev, but the sales average is close to Manyavar even with the lower volumes. In otherhand, in terms of age of population, India is a nation with a higher number of youngsters who are unmarried. The mantra is simple, an increase in per capita will lead to an organized market, and when this happens, it is a win-win for Vedanta fashions and shareholders.

11 Likes

The derating story continues, I believe the next leg of rerating for consumer companies will only come from Volume growth as the market now understands that lucrative story eventually doesnt always translate into numbers

3 Likes

Vedant Fashions Q1 FY25 Analysis: Key takeaways!!

Vedant Fashions faced a challenging Q1 FY25 due to an exceptional lack of wedding dates. However, management remains optimistic about the rest of the year, expecting business to normalize from Q2 onwards. The company saw positive trends in July, particularly in Tier 2 and Tier 3 markets outperforming Tier 1 cities. Management is confident about the upcoming festive and wedding season in H2.

Strategic Initiatives:

- Focused on enhancing back-end operations, training, and retail network administration during the slow Q1.

- Planned retail expansion strategy for the remaining year, with a healthy pipeline for new store rollouts.

- Hired a new creative agency (McCann) to strategically rethink brand positioning and marketing campaigns.

- Launched a training app for fashion advisers to improve service quality consistently across stores.

- Implementing AI-powered cameras in stores to gather consumer experience data.

Trends and Themes:

- Shift towards larger stores in key markets to improve productivity and customer experience.

- Growing focus on premium offerings through Twamev and Mohey brands.

- Increasing emphasis on Tier 2 and Tier 3 markets showing potential for growth.

- Rising average selling prices (ASPs) driven by premium brand offerings.

Industry Tailwinds:

- Early start to the wedding season in FY25 compared to FY24, potentially extending the shopping period.

- Normalized spread of wedding dates across H2, allowing for better business planning and execution.

- Growing aspirational consumer base in Tier 2 and Tier 3 cities.

Industry Headwinds:

- Unpredictable wedding date patterns affecting business planning and inventory management.

- Potential economic slowdown impacting discretionary spending on wedding attire.

Analyst Concerns and Management Response:

- Store closures: Management clarified that closures were part of a strategic realignment, with many being replacements or shifts to better locations. The company aims to maintain a 2-2.5% churn rate in its retail fleet.

- Competition: Internal studies show stores near competitors outperforming by 4%, suggesting limited impact from organized competition.

- Ad spend reduction: Management explained it as a strategic decision to focus spending on H2 when wedding season peaks.

Competitive Landscape:

Vedant Fashions maintains its leadership in the organized wedding wear market. The company’s focus on service quality and expanding premium offerings (Twamev, Mohey) differentiates it from competitors. Management sees potential for 15-20% of the market moving to the premium segment (Twamev) in the next 3-4 years.

Guidance and Outlook:

No specific guidance was provided, but the management expressed confidence in achieving planned store expansion targets for FY25, primarily in H2. They aim to maintain the 14-15% annual retail area growth over the medium term.

Capital Allocation Strategy:

The company continues to invest in store expansion, particularly focusing on larger format stores in key markets. Investments in technology (AI cameras, training app) and marketing (new agency partnership) indicate a focus on enhancing operational efficiency and brand positioning.

Opportunities & Risks:

Opportunities:

- Expansion in Tier 2 and Tier 3 markets showing promising growth.

- Premium segment growth through Twamev and Mohey brands.

- Leveraging technology for improved customer experience and operational efficiency.

Risks:

- Dependency on wedding seasons and date patterns.

- Potential economic slowdown affecting discretionary spending.

- Increasing competition in the organized wedding wear segment.

Customer Sentiment:

Management noted positive customer responses to new store formats, particularly for Twamev and Mohey, with high Google review ratings (4.8-4.9) for new stores.

Top 3 Takeaways:

- Despite a challenging Q1, Vedant Fashions maintained healthy margins, demonstrating the resilience of its business model.

- The company is optimistic about H2 FY25, with an early start to the wedding season and normalized spread of dates.

- Strategic focus on premium offerings (Twamev, Mohey) and Tier 2/3 market expansion presents growth opportunities.

2 Likes

Not good growth (YOY) - which is to be compared for Vedant Fashion. Hype of premiumization or more marriage dates / festive buying not impacted positively on bottom line. Paying high valuation is not justifiable for such growth.

1 Like

Management believes this issue is more of a macro-economic slowdown rather than a category-specific issue.

Competition wasn’t seen as a significant factor as stores with and without nearby competitors performed similarly. Management says there have been no competitor brands that have excited them in terms of numbers.

Other retailers and MBOs are also experiencing a slowdown.

The company does see pain in many other players operating in the market, but denied to comment on consolidation in market.

4 Likes

Wondering who this competition is ![]()

possibly Ethnix from Raymond Lifestyle.

It’s a large number of players opening a few stores, that is what we are seeing on the ground majorly. And if I give you an example of a city like Raipur, we used to have one exclusive brand outlet which we operate. And maybe another 25, 30 stores would have opened in that market.

From google maps, I don’t find much store in Raipur. Even in my my locality I dont find new entry stores.

Commentary from promoters on no sales growth is just “less marriages” across last couple of quarterly calls. On questions on competition, they again reiterate that it is not competition that slowing them down it is the marriage situation.

It is hard to trust this to be honest. I don’t understand how number of marriages go down unless there is a covid like event. Someone did ask them how do they know it is a market downtrend rather than their product is not selling - I belive the response was like they collect data from other shared chains as well.

Overall, nothing suggests the high P/E it is commanding now. Downtrend/Consolidation may continue unless there is a bumper Q1 appear which is unlikely

3 Likes

Slowdown can be more attributed to gaining too much of market share maybe because if you go on certain occassion like weddings, engagement, or any festive and find other guys wearing same or similar clothing makes you want to switch to other vendor even though the product might be great. I think so this can be one of reason as it had become leader in wrong industry where its structure is so that no one can dominate too much.

I am not invested nor i have any short interest just 2 cents of my view how things i think are.

4 Likes

Industry Feedback from a Ground Retailer – Supporting Manyavar’s View on Marriage Seasonality

I’m not currently tracking or invested in Manyavar, but I do operate in the same industry. I run a retail apparel business in a Tier-3 town in India and also sell wedding-focused ethnic wear like Manyavar, sherwanis, and salwar-kurtas.

Based on my on-ground experience:

FY24 (last year) saw around a 13% drop in sales for my store.

This was primarily because the April–June 2024 period had fewer auspicious marriage dates, which significantly impacted wedding-related purchases.

In contrast, CY2025 (January to June YTD) has had a strong wedding calendar, and my sales have picked up sharply this year.

So when I heard Manyavar’s management attributing seasonal softness to wedding date availability, it absolutely resonated with my local experience. If this trend is visible even in a small town like Pandharpur, it likely reflects a wider industry truth.

In my view, the management is being transparent about the seasonality impact on their performance.

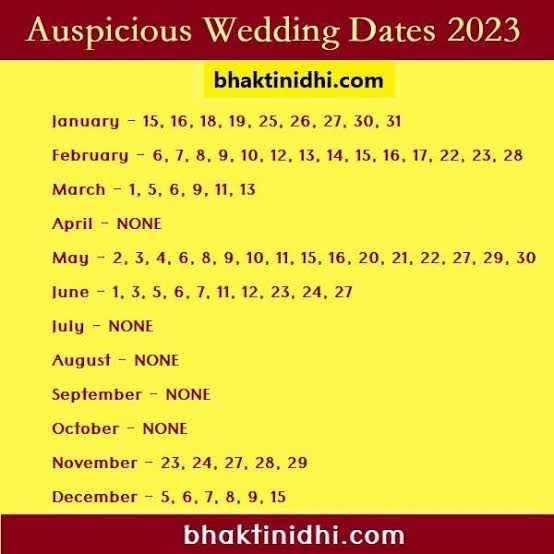

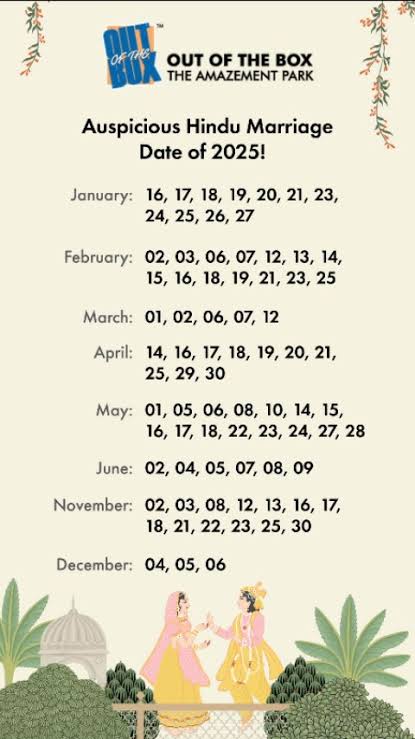

I have attached major marriage dates for last 3 years. They might give a better picture.

10 Likes

Yes, this could be a valid reason. I guess the growth will be very much linked to how the industry size grows. It will be difficult to outgrow at their market share levels.

This is very interesting, the atheist in me could never think this direction. Thanks Nikhil! Looks like 2025 APR and MAY could turn around this. Let’s see.

2 Likes

Its still lurking around the lower lows for shareholder. What could be the reason behind the long downward trajectory?

Low sale growth (5 year cagr of 9%) and gst increase from 12% to 18% as most of their merchandise is priced 2500+.

1 Like

GST may not be the appropriate reason, people who are buying for weddings doesn’t look bother about 5-6% increase. However, lack of growth would be the reason for no movement in price. There is no growth in last 3 years sales, margins are down by 4%, depreciation increased (might be due to new store addition).

Basically demand is weak in the market, pricing of the product is also premium side to maintain the margins.

1 Like

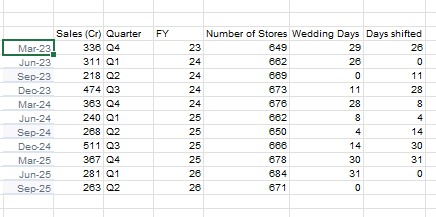

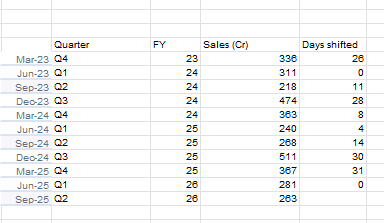

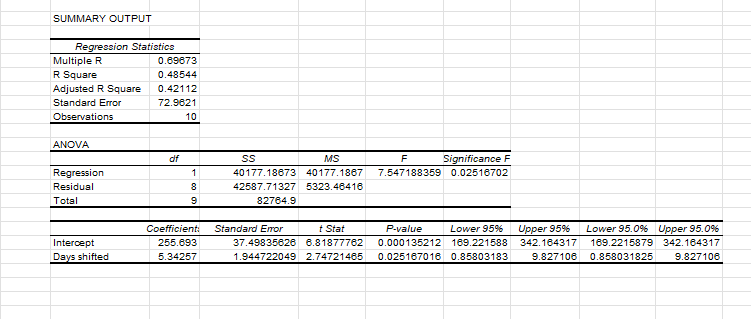

So I was actually trying to understand the validity of the claim by the company that wedding days drive their sales. I just started off by using @nikhildoshi 's number of wedding days provided here. (And I completely understand that this is very few datapoints to make any statistical conclusion)

But essentially ~50% of the variation in sales can be attributed to the number of wedding days in the upcoming quarter (So people usually start shopping in the previous quarter is what I am implying here) and that seems to be a valid proposition by the company.

Which begs the question that is the market really punishing the company for this kind of seasonality or is there something fundamentally wrong with this company which I am not aware off since the margins look amazing, the company has no debt and they don’t have any real organized competitors.

And would be glad to analyze a bit more if anyone can provide a reliable source of future wedding days!

PS: Attached the screenshots of the values I used

Original Data

Relevant columns

Regression output

1 Like

The biggest problem is no tangible moat left. If you look at competition many organised players have also entered this space, eg Tasva by ABFRL, Raymond Ethnix, Siyaram also has some brand. So the market has become even more competitive with no apparent design or pricing advantage.

These are just cursory observations on business. Haven’t evaluated but to my knowledge, seasonality was anyways an important factor but it’s the competition that’s also fighting for the market share.

Disc: No holding & transactions

4 Likes

It does sustain really high margins, probably the highest in the industry, wouldn’t the competition drive that down? Or is it because of their positioning they are offsetting it by increasing prices. (I also observed they don’t even provide any discounts)