Scuttlebutt on VFL blog post -

3 Likes

Not justifying Vedant but sharing some details as I work in same industry (I am aaprel retailer)

Companies like Raymond or ABFRL brands (Allen solly, Peter England) target essential segment / daily wear segment.

In this segment - average cost of products is usually less (avg 2000)

Product life cycle - max 2 years

So customer needs to buy products every alternate year, that’s why highest volume are in this segment and that’s why it is easier to scale this business.

That’s why most apparel manufacturer target this set of buyers and this leads to excessive stock production, leading to discount and thus compression of margin.

In case of wedding, customer buys garment once in his lifetime (designer suit or sherwani or lehenga). Thus he is willing to spend more. That’s why margin are higher and volume is low.

Simplest anology will be comparing apple and other Chinese manufacturer.

Both make similar products but has vastly different margin,despite being from same industry.

17 Likes

Is that why vedant fashions moved to manthan brand which is everyday use low cost and cater towards the masses

1 Like

Ravi Modi Family Trust, the promoter of Vedant Fashions, plans to sell 7% stake in the company through an OFS. The offer is being proposed with an option to sell an additional 2.88% stake in the event of oversubscription. The floor price is fixed as Rs 1,161 per share, which is nearly 7% discount to the last closed price.

Last reported shareholding pattern shows promoter holding as 84.87% (screener).

If additional 2.88% stake is also sold, maximum 75% promoter holding direction will be complied.

Disc-Interested, Not invested.

6 Likes

I think Vedant Fashion is a very well run, asset light somewhat seasonal business with a long runaway for growth, which as of now is very reliant on one brand. A lot to like but very hard to get valuation comfort when its trading above 50x forward earnings.

A couple of concerns I had -

- If you go to a wedding do you want to be seen wearing the same Sherwani, lehenga as someone else? I personally think its great but don’t think everyone shares my view here. A risk that remains, especially for a brand like Mohey.

- While it may not be a concern but I do believe that with scale, production will not get easier. Basically if production is to double or triple, will they be able to find similar high quality vendors as they do right now? (A happy problem though, as that means you are growing)

Done a deep dive on the business and shared some of my thoughts here.

5 Likes

Here is an article on Manyavar/Vedant Fashions.

https://www.thryvv.in/article/manyavar-a-bet-on-the-growth-of-the-big-fat-indian-weddings/

1 Like

Any news or view, apart from market correction, which is leading to this non-stop decline in the stock price? One main reason is valuation (in my view) aided by unjustifying lower growth rates and the patchy seasonality of business.

But any other reason or factor which Mr. Market is looking at?

1 Like

What will be the impact of IT notices company received for previous years? Please share your thoughts.

Disc: Tracking position

I think you misunderstood. The latest filing found here is actually stating that the ruling has been in the company’s favor and the disallowance of the expenses for the mentioned years has been deleted which effectively means the expenses have been allowed thus no tax implications on the company. It mentions the same in the last row of the table.

1 Like

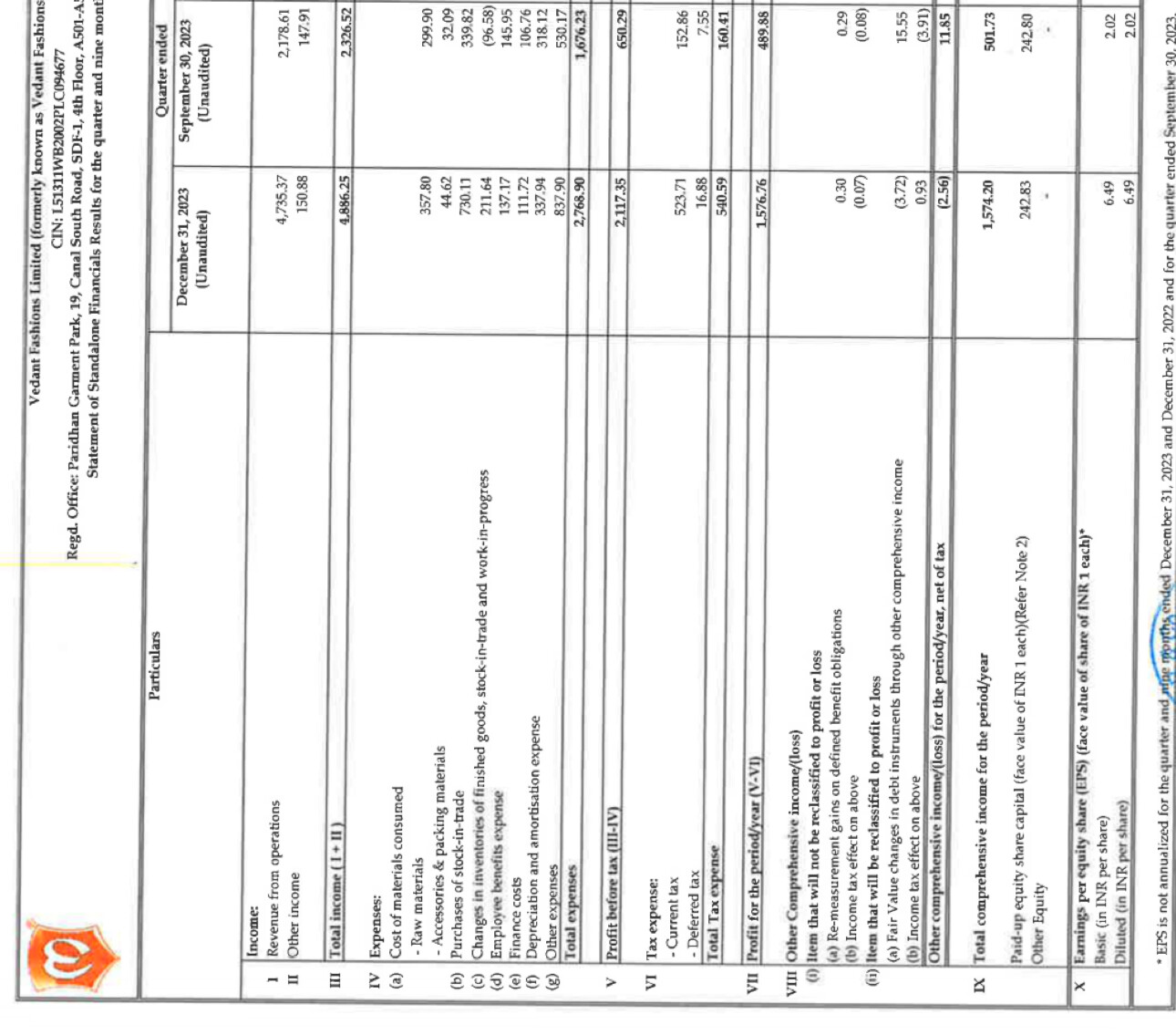

Bad H1 results and few wedding days in Q3 this year. Company in the latest concall says it’ll cover up in H2.

I think their concall is always the copy paste of what they say in the previous calls. “Added XX lac store area, fewer wedding dates, dont see Q-o-Q and next year would be great”.

It is because of this seemingly callous tone of the Management, that I am trying to figure out if this business is actually scalable the way I perceived it to be.

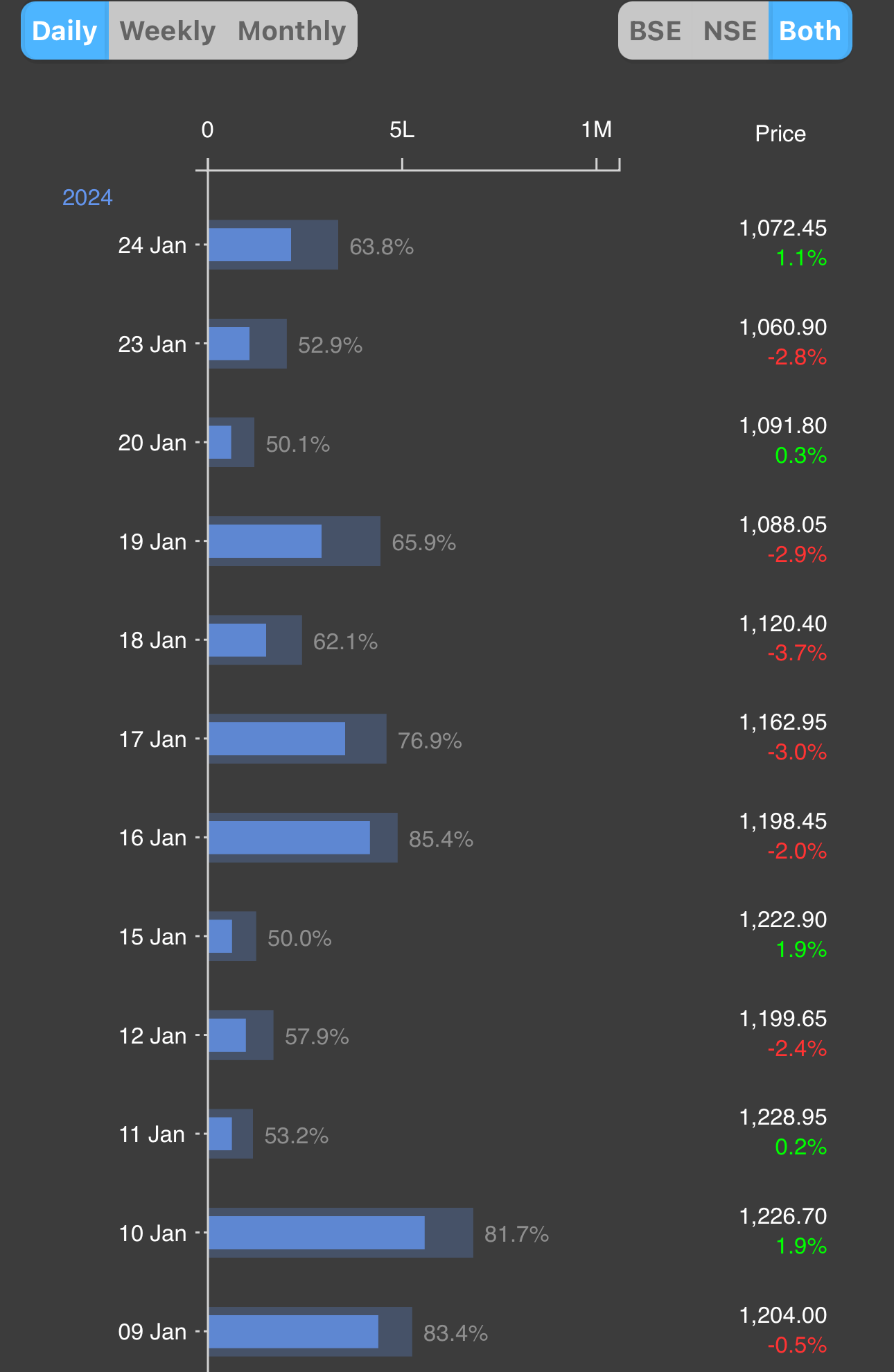

The Company has a very low free float and retail holds mere 3.5% odd stocks, maybe some Institutional holder is selling because the stock is down each day since it touched 1,460 on 8 Dec’23. It is down almost 30%.

The results are going to be bad for Q3 as well, looking at the consumption numbers but are they going to be this bad that stock fell 30% already!

1 Like

Thank you for the clarification. Much appreciated.

12% revenue CAGR for the last 5 years ex of 5-6% price hikes would be mere 5-6% volume growth, so whatever the story might be of low penetration of organised retail and India’s wedding potential etc. clearly it is not visible in the numbers. Multiples were jacked up only on the expectation of future growth, for which i think the market is now course correcting

3 Likes

Thanks of putting in simple numbers. It is strange that we as investors looks at such growth figures only after stock falls and when it keep rising, the same business’s numbers tell a different story…

1 Like

Problem with 5 year CAGR is the covid impact from Apr20 till atleast CY21 season and hence I would not like to look at that. But yes what you are saying is correct qualitatively because people started touting it as the next Titan! And hence it went to a PE of 90 with not more than a 15% sales growth irrespective of the Covid-19 impact.

If at all, this should be more like a 40-45 PE stock at max considering it has good return ratios (GM, OCF to EBITDA, ROE) and a possible sales growth of 20% in the future.

My personal view. Invested in the stock and biased.

1 Like

")

A good interview of Vedant Modi which provides many insights about the working of Manyavar. The emphasis he is giving to analyzing data for every aspect of business is quite commendable.

3 Likes

srtrong delivery percentage in volumes; and very good numbers in Q3, hoping to see the bounceback to 1500 levels

Since it is seasonal business, you need to compare results on YoY basis ( this quarter with same quarter last year). YoY numbers are 11% top line growth and 7% EPS growth. For a stock having 67 PE, it is pretty average performance to be honest. Not sure how market would react though…

2 Likes

What I fail to understand is why they still compare with FY20! FY23 was a very normal base especially Oct22-Dec22, why do they not compare with it?

Plus their sales increase is always meagre and margins have started to decline, marginally but yes they are!

Their whole strategy is to open more stores and drive sales from data driven marketing and collection which does not seem to work so far. They are already in all the metros and Tier 1 towns of India. I doubt they will have a much customer base in Tier III and IV as compared to Tier I and II.

Wearing nice looking clothes in weddings isn’t a habit which they will inculcate in people. Just saw the interview of Vedant Modi, shared by another member an hour back, and he mentioned that almost 90% of their sales is wedding driven. I do not see a lot of optimism at this point of time with the subdued numbers one quarter after another!

4 Likes

Philosophy of BAAP (Buy at Any Price) has always have frustration at the end ! Stock either stays at same price till earing catchup or correct it for reasonable price.

As per my assessment, company was having highest margins at lower base but when company switch into growth mode either margin get hit or sales will not grow…which is happening presently. Competition is also increasing from known brands in India. With aggressive stores expansion and premium retail exposure, it will be challenging to sustain margins in near future!

3 Likes