We need to study Laxmi Dental works as it can be competitor for Vasa Denticity

Invested and Biased for Vasa

dr.vikas

We need to study Laxmi Dental works as it can be competitor for Vasa Denticity

Invested and Biased for Vasa

dr.vikas

It’s a good company no doubt, but Vasa Denticity is an online marketplace vs Laxmi Dental being a manufacturer. With Smileworks there could be competition but other than that I am not sure

Sir have you studied prevest denpro also recently it moved from sme to main board and almost in similar spaces though not exactly

And today’s news of KKR buying some dental lab chain in USA this space looks interesting

i guess we are reading too much into the review ratings…overall business model looks good and the valuation as well as overall revenue, profitability numbers are reasonable.

Actually now we ‘‘will have to study’’ other Dental lab manufactures also as Vasa aka Dentalkart is entering into manufacturing business.

Now I will be slightly more cautious with the allocation of Vasa in my portfolio. Was planning for 10% but will now reduce it.

Personal Opinion

dr.vikas

Waiting for your final analysis

If they have to expand their private label business sir, in house manufacturing is crucial for a high SKU, high customisation/control over product quality - no reliance on contract manfs as they have set MOQs - this allows them to calibrate the production according to demand fluctuation of individual skus. Although yes Yet to see the quantum of capex/r&d into this in near term, as long as they are taking it as a step function and not stretching a balance sheet a lot at once while their core biz also burns cash, it’s a good move for the long term

Sharing the latest filing by Vasa

Invested and Biased.

dr.vikas

I’m new to studying this company and was curious to know more from people with direct experience. Does anyone here personally know a dentist who uses Dentalkart? If yes, I’d love to hear their opinion on the company’s products and service quality. Also, if anyone has insights into what distributors think about Dentalkart—whether they find it reliable or competitive.

Hi, I just wanted to do an experiment to see whether we can blindly trust Mouthshut reviews and form an opinion about the product. I asked google which is the No. 1 brand in the world and searched for the reviews of the same in Mouthshut.com. You see for yourselves.

I know a couple of dentists who buy regularly from Dentalkart and have not faced any issue and are happy with their products. Although Vasa Denticity is becoming better and better, from an investment point of view, if they don’t grow as they have promised, then valuations seem stretched. Right now, the P/E of 50+ is factoring 30-35% growth per year or higher. If any drop in this growth, the valuations may correct. Waiting for Q4 earnings. Disclaimer: I am invested in the company for longterm and any drop in price and valuations become cheaper, I am planning to buy more.

I also know a dentist too who uses DentalKart. He is happy so far.. i am invested.

Spoke to a dental equipment provider in a tier-2 town. He mentioned

So overall a positive feedback.

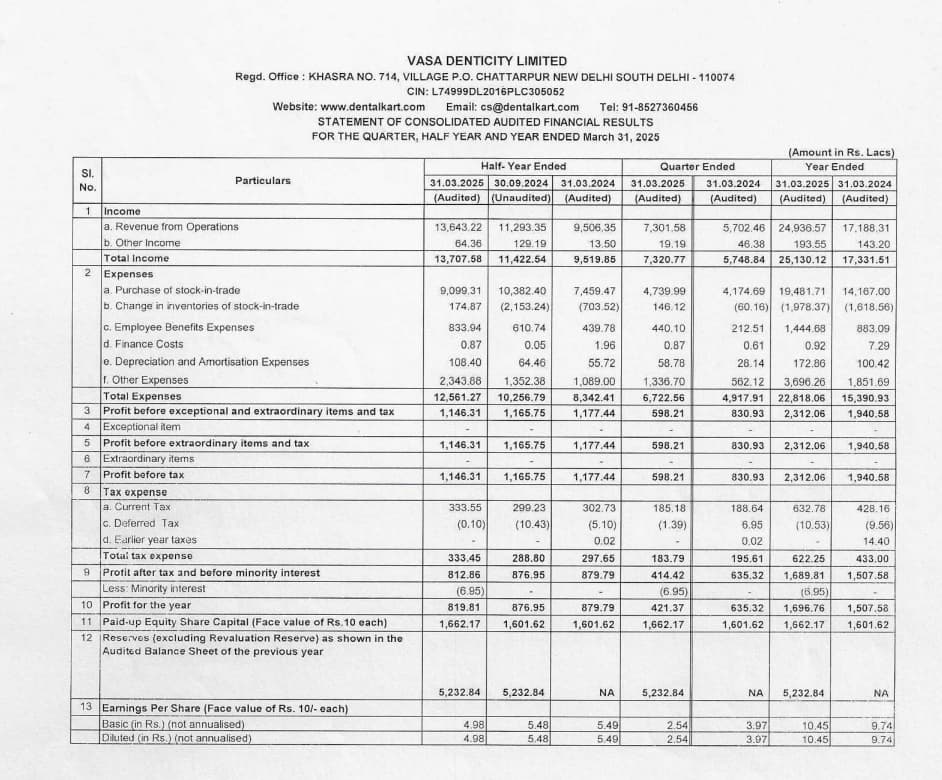

Results are out. FY 25 vs FY 24

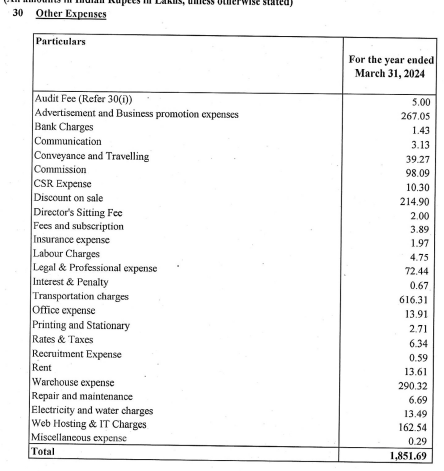

Other expenses from the Annual Report FY 24. Need a similar breakup for FY25. Should be asked in the earnings call.

Disclaimer: I have a 1% tracking investment.

It’s good that they are decreasing their average delivery days which was a barrier for mass adoption by clinics and dentists for their solutions. There needs to be a shift from only unavailable and exclusive products to all products sourced from Vasa thus their shortening delivery days is good.

Looks like last years Q4 results was an anomaly as margins were way too high compared to rest of the quarters, so the results may look optically bad. I don’t blame them for spending money on advertising, discounts, warehouse expansion and manufacturing entry as these are necessary catalysts for further expansion.

While it’s nice to see average order value surge, I am disappointed by the only 8% increase in monthly active users on their app. This would be something to be addressed as MAU are the founding blocks to future revenue.

Margin improvement will come with time so currently my main importance is revenue growth which has been decent. Again the exceptional Q4 2024 results seem to make growth look less exceptional in spite of a 10Cr + revenue gain QoQ.

MAU growth is slow because their TAM (practicing dentists) in India is very limited. The only way forward for Vasa is through increasing their penetration to increase their AOV.

This can be done either by capturing more market share by selling more through proper growth marketing, selling more non-consumables (a tall task), expanding into other geographies or by venturing into additional product segments (like they are doing with SmileLabs).

I had used their app and their growth marketing seems at a very nascent stage. Overall, a little skeptical of their future growth at current multiples.

Disc: 2-4% holding

You can check the Notes to account for the detailed breakup of other expenses once the annual report is approved and published.

HI agni,

Can you please explain why selling more non-consumable is a tall task?

Because people still prefer buying these items offline due to servicing being provided by local distributors.

Thank you Agni for sharing this insight.

So as investors, we should focus on the company’s serviceability aspect — specifically, whether they are actively building service centers. In the recent conference call, the management mentioned plans to open new service centers. Although creating a good service network will do take time and effort.

Here are the extracts from the Q4’2025 earning call transcript -

“Although we plan to open some service centers, we have opened 1 service center recently in South India. And in future, we plan to have some service centers. Apart from that, no big CAPEX plan.”

*"We have opened our first service center in Chennai, and we have opened a small showroom also there. We are planning to open 2 showrooms and service centers in the prominent part of India, versus this we are expecting to invest almost like Rs. 3 to Rs. 5 crore for these showrooms and service centers across India."

Also if you are aware of some other small nuances about the dental retail space please share the same. This helps in understanding the business and its model. Once again really appreciate your time and insight.