Q4 FY24-

SME company doing PPT and concall

This growth is driven by an increasing awareness of the oral health, higher disposable income, and the rise of multispeciality hospitals offering comprehensive dental care.

Sir, currently, there are around 3,20,000 approx. registered dentists in the country. Apart from that, we expect more than 1,00,000 unregistered dentists in the country. There are more than 1,00,000 dental students in the country. And then, there are 352 dental colleges, more than 5,000 dental laboratories. These all are the Total addressable markets (TAM)(Huge TAM available)

in next 3 years- 500-600cr revenue

in next 5 years- 800-1200cr revenue(70% CAGR)

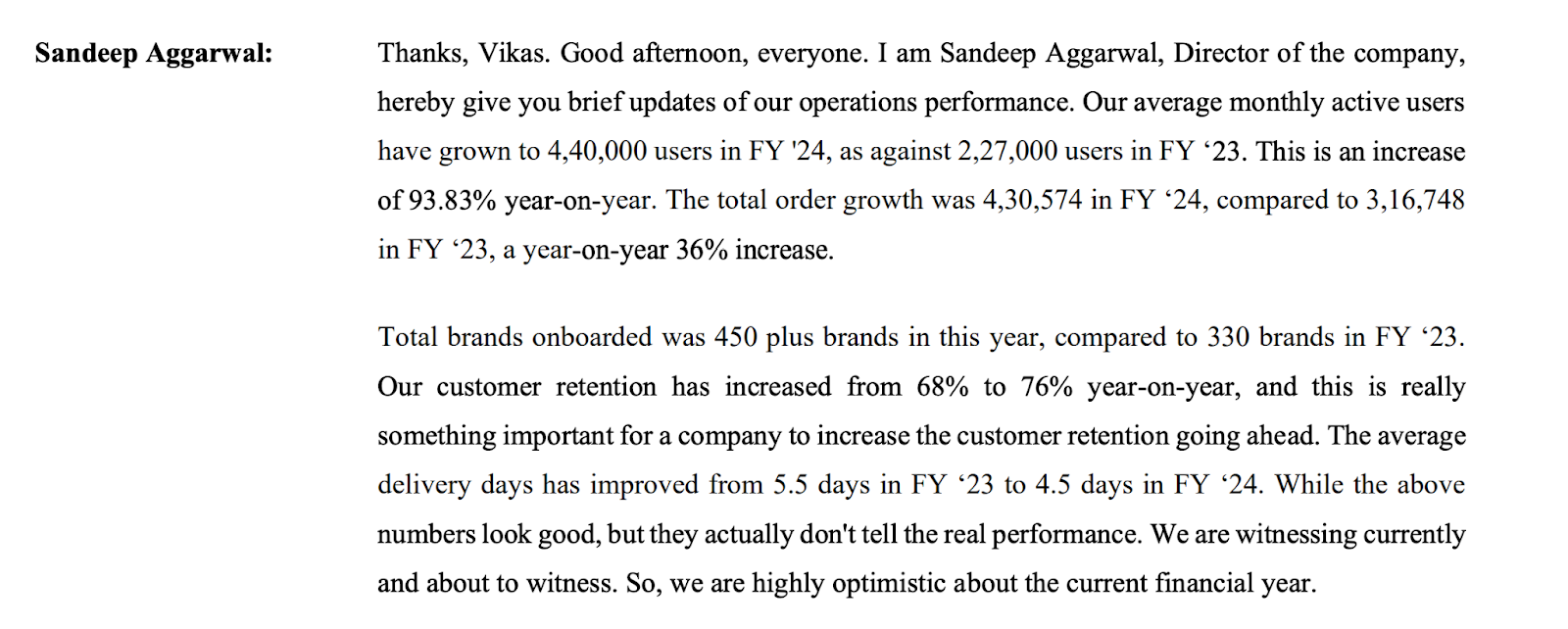

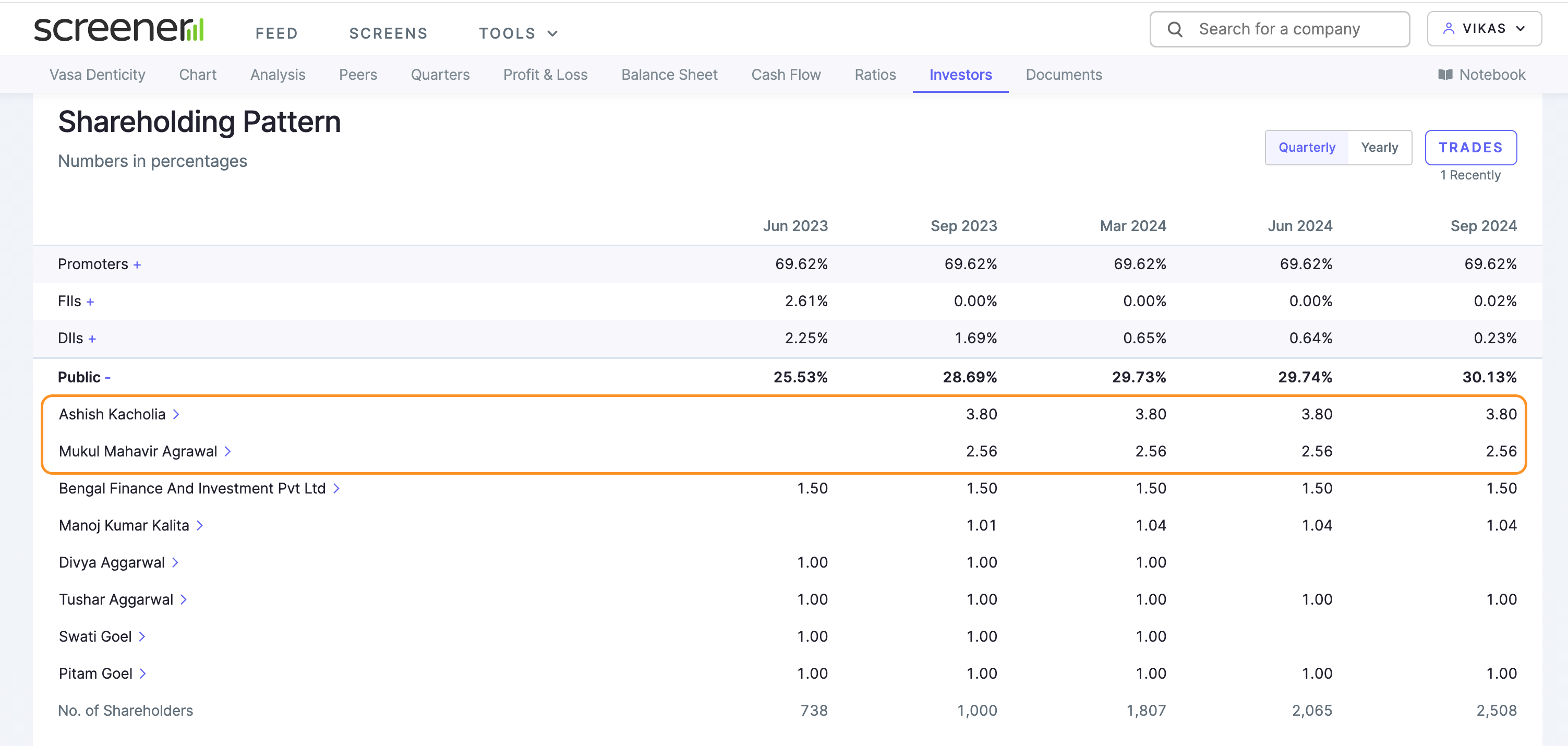

Total brands onboarded was 450 plus brands in this year, compared to 330 brands in FY ‘23. Our customer retention has increased from 68% to 76% year-on-year.

new operational warehouses in Mumbai, Nagpur, Kolkata, and Guwahati .This will take delievery time from 5.5 days to 4.5 days and our aim is of reaching 2 days

The total order growth was 4,30,574 in FY ‘24, compared to 3,16,748 in FY ‘23, a year-on-year 36% increase.

Grow 40% as against the guidance of 70% because a lot of international companies have not been able to register themselves in the new drug license policy in India. So, this will subside this year and we expect those revenues to come back in this financial year.

Investing in cloud, warehouse automation and heavily on technology to reduce the time.

When we have a mother warehouse in Gurgaon, it is highly optimized and automated.

11cr receivables are showing wrong bcz they were COD orders and our delivery boys collected that money.

So, we expect a good growth from Baldus (have exclusive rights, not only use in dentist but also in other industries as well , Sedation system not only is used in the dentistry, but it is also used in derma, hematology and a few other segments of the medical end. )in this financial year. Last year, I think it was under INR2 crores sales from Baldus overall. So, there is not much significant contribution from that.

we have exclusive rights to distribute them in the Indian market to help us in marketing the product and training the doctors and the employees. And if needed, they provide the certification of nitrous oxide training to the doctors. That is the reason we are responsible for developing the market and making this

our own branded products or white label(china se import karke apna label lagakar bechna)contribute to 54% sales which is high margin business

So, 80% of the orders we need to be delivered faster. So, one of the opportunities that we have opened our own warehouses, we’re going near the customer and trying to deliver the products faster

From the total online sales we do, 98% of that sale comes from the individual dental practitioners and 2% comes from the hospitals. So the hospital business is more of a credit-based business, which we are trying to evaluate this year and trying to tie up with a good financial partner who can provide credit to them.

So we don’t see a large growth on EBITDA margins in the short run, but in the long run definitely if 70% of the sales comes from our own brands and a lot of exclusive brands, we see a good EBITDA numbers in the future.

We have to study the data how it is working out and depending on that we will ultimately decide that if we have to open smaller warehouses in cities like Chennai, Kochi, maybe Lucknow, Jammu. So these small cities we have to see in the future, but that will all depend on the data we’ll have from the current warehouses.

we are currently not looking to manufacture anything. But yes, in future we are looking to assemble some of the items which are difficult to be imported in India. So we’ll keep a small assembly line for those products.

Yes, in the long term, we are looking to go beyond India, but in the short term next 2 years, 3 years our focus is only India because it’s a big market and we have a long way to go.

B2C I think is 90% of the business and B2B and B2G together contribute 10%

And currently, for a very few number of dentists, we are the primary source ofbuying the dental products. Like most of the products, the people who are in the Tier-3, Tier-4 cities. For Tier-1 cities and most of the Tier-2 cities, we are the secondary source of purchase currently. And we are looking to go up the ladder and become the primary source by providing all the values which I mentioned a few minutes back.

Secondary source. Majority of the revenue is coming from a large number of customers who are keeping us as a secondary source because they are not able to find the products locally or they are able to find a lot of new products on our website which they want to buy again and again.

For example, a dentist purchases products worth 40,000 consumables in a quarter. So the most common consumables like the dental stone or alginate, they prefer to buy from their local dealer. But some products worth maybe 5,000, 6,000, they prefer to buy on DentalKart, which they are not able to find locally. So this is the current situation. And we know the situation, and we have a target to get that 40,000 worth of revenue from every dentist. And we are trying to find ways to support it, and this also shows in our presentation.

We are going to have more orders from the same set of customers we currently have. That is one of the parameters. Then we will be expanding our catalog, our product range. We’ll be doing strategic marketing to acquire new customers. So, currently, we have served half of the dentists of India. But we have not served them fully. It was a minuscule level of sales to the number of people we have currently serviced. So, if there are 90,000 doctors who bought our products last year, we want to get into their clinic and provide them with the right set of values, so that they can buy everything from us. So there, we see a 10x upside from the same set of customers.

Sir, if we decide to launch B2C products for which these market places are accustomed, Amazon, Flipkart, if we launch B2C products like mouthwashes or toothpaste or many other oral care products for the B2C segment, we will look at listing our products there. But for our products which are meant for Dentist, there is an access issue to list our products there. And we want to keep the exclusivity within B2C 68:40

Disclaimar: Not invested

")