Yes, IF the GOI is serious about removing China dependency for Pharma APIs and chemicals. Otherwise they will lose.

What is the reason for continous promoter selling…

I dont see any point in selling for donation

3 Likes

Some Notes from Investor presentation and results for FY22 (Link):

-

Consolidated revenue of 1153 Crs. Significant top line growth of 53% Y-o-Y after past 4 years of negligible growth. However, margin are impacted severely. Almost flat absolute EBIDTA on such health revenue growth has resulted into margin compression from 27% to 17%.

-

Chlorination (~29% of top line for FY’22) has seen a handsome 22% CAGR volume growth between 2019-22. However, revenue growth of 8.45% only. Most of the capacity addition has happened between FY’21-22. Realization dropped from ~275/Kg to 170/Kg between 2019-22. Managment projection of the same realization going ahead

(will be interesting to know what is the capacity utilization for chlorination segment alone. Some operating leverage can kick-in on higher CU -

Hydrogenation segment (30% of top-line for FY’22): 7% volume and 20% value growth between 2019-22. Realization has improved 100/Kg to 153/kg. (was Rs. 220/Kg) for Q4’22). This can be a growth engine in mid-term with the investment going in here. PAP scale up from 300 MT to 500 MT per month by this FY itself can have decent top-line opportunity. Further a continues process product qualification of PAP has potential to take the numbers to 1000 MT over a period of time. (though seem major technical challenges to achieve desired yield in continuous process). Best thing is that most of the PAP production can be consumed in-house by subsidiary Bharat Chem.

-

Concerning part is with Working capital degradation. On one hand the debtor days has extended from 75 days to 100+ days. On top, payable days has shrunk from 93 days to 58 days. As a result overall cash cycle has gone 2x. Real concerning if looked in context with shrinking margins.

-

Promoter holding is in one way direction only. Unfortunately, no convincing explanation by management.

Some Notes from Q4’22 Concall (link):

-

For the year ended in March 22, the revenue from operations stood at around Rs. 1153 crores which grew by around 53% year over year. EBITDA margin for the year stood at 17.77%. (was ~27% for previous year).

-

we are expecting to close somewhere around 1200, 1250 in FY23 and then about somewhere around 1400 in FY24 on a standalone basis

CAPEX

-

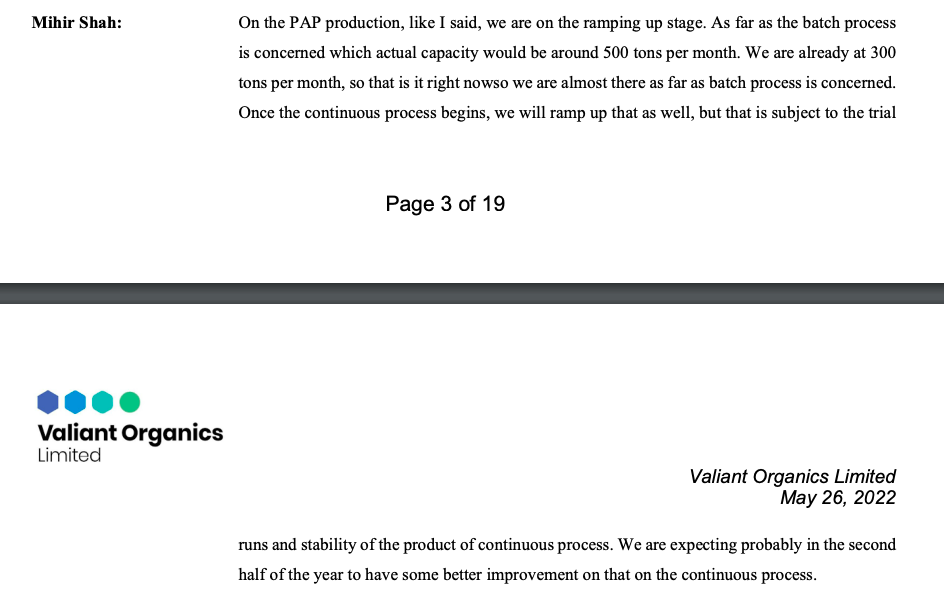

PAP ramp up continues to be on track, achieved a production of 300 plus metric tons per month. In batch production, optimum capacity will be for 500 MT/month. Can go up to 1000 MT in continuous process (subject to meeting the specs) by FY’24. 85% will be captive consumption (Bharat Chem).

-

While OAP and pharma intermediates projects both are on track with no significant delays. OAP phase 1 trial run has been successful. OAP volume projection of 10 – 20 MT by Q2’23 and 50- 60 MT by Q3’23.

-

Pharma intermediate plants expected to commence production from Q2 FY23. Capex for Pharma intermediate is ~55 Crs and OAP is ~30 Crs.

Margin compression:

-

~5% phenol price increase in Q4. Other RM were also at peak in Jan-March. Additionally, fright and fuel increase has impacted.

-

No pricing pressure due to additional cloronitation capacity built-up in domestic market by competion.

-

PAP in FY22 was around 1900 MT with EBITDA margin of about 10%-12%, but it will improve once the scaling up happens because there are again certain cost that are just right now getting loaded on very small volume.

Working capital and Debt Position:

-

D/E is currently at 25%. Higher debt due to OAP and Pharma intermediate capex. Additionally, working capital cycle has got elongated due to market dynamics.

-

Also, one of the earlier partnership entities (Valiant Laboratories) has been converted to Sub. Partnership capital is currently added under short term debt. (This is non-interest bearing).

-

Significant jump in top line towards March month (PAP sales to subsidiary Bharat chem). Due to customer credit period, receivables are high as on closure of FY.

-

Long term loan of Rs 128 Crs can come down to ~100 Crs by next FY

-

No new debt for additional capex for now. Will be funded internally.

Disc: No Investment

Thanks,

Tarun

16 Likes

I have gone through the concall transcript.

As I understand, previously they were into chlorphenol which had great margin.

The upcoming expansions are all into hydrogenation side, which carry lower margin.

That may be the reason for sharp derating and insider selling.

Note - this is my my takeaway from this con call summary.

I accept my interpretation might be wrong.

Disc - Have tracking position / Will be selling.

regards

1 Like

Fall of crude price is very good news for VALIENT… RAW MATERIAL will be cheaper by 15-20% but prices hike will help to him to recover margin.

DIsclosure holding and add few more

1 Like

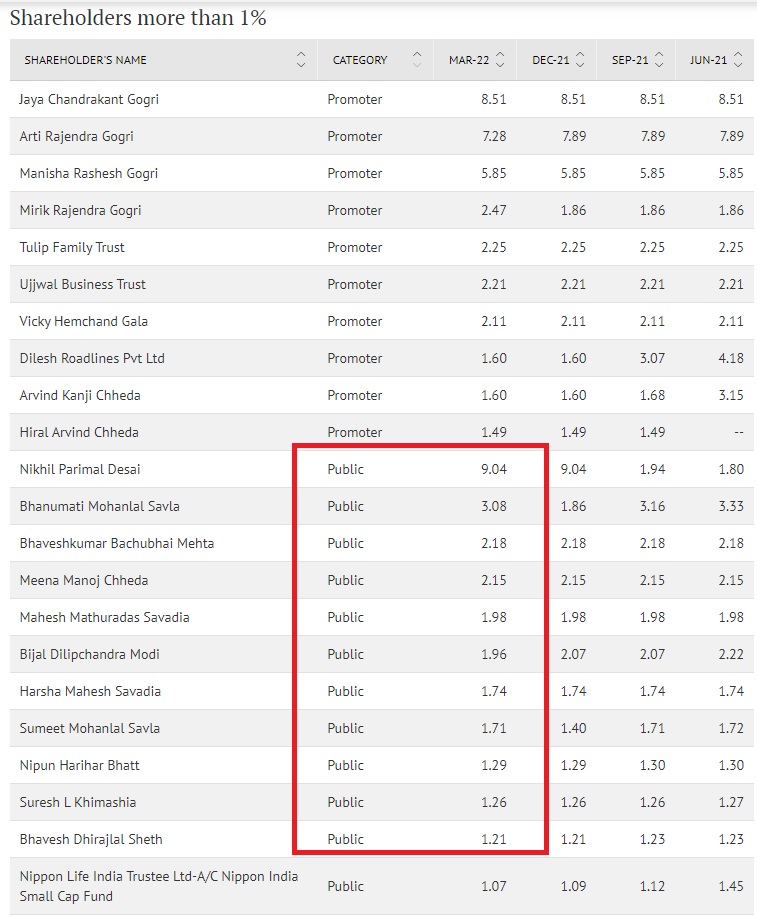

A lot of noise has been made about the continuous selling by promoters even as the share prices are falling. So I decided to dig a little bit and came across this interesting observation.

A total of 27.6% public shareholding greater than 1% is owned by individuals apparently related to the Aarti Industries / Kutchhi families (same community as Aarti Industries promoters). Furthermore, these individuals have meaningful holdings in other Aarti companies either in the present or past. For example, Mr. Nikhil P. Desai is the Managing Director of Aarti Surfactants. His shareholding has gone up from 1.8% in June 2021 to 9.04% in Mar 2022. If I understand correctly, his father Shri Parimal Desai is a Director of Aarti Industries.

On diving deeper, I was unable to find these individual names in any other list of public shareholding in excess of 1% for non-Aarti Group. Meaning, these individual investors have sizeable percentage of their wealth only in Aarti Group.

If you add this 27.6% public holding by potentially related individuals to the existing 39% promoter holdings, the actual promoter holdings may be closer to ~67%.

Please note that only the list of public shareholders where holding exceeds 1% are published. This still leaves the possibility of smaller related party share holding open, making the actual promoter related shareholders even higher.

Source of share holding: Value Research

Disc: Invested as a tracking position.

13 Likes

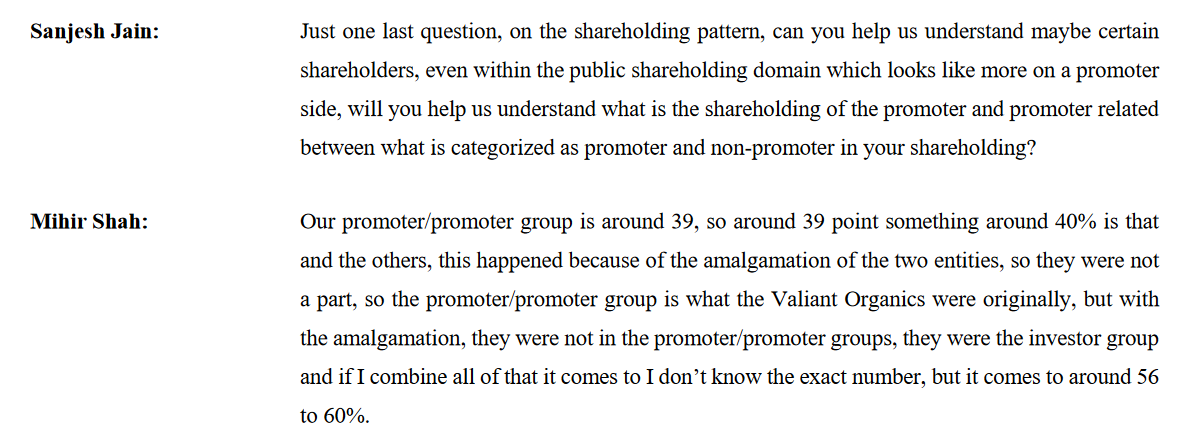

Adding on this, I was going through the last concall transcript (Link) and found the below snapshot as relevant

Initially I had assumed the selling as some form of internal adjustment while others picked up stake and now this realignment of shares seems to point to that.

4 Likes

Q1 results are out topline has fallen 20% and bottom line has fallen close to 50% QoQ.

Margins have fallen to a decade low of 11% ,contradictory to earlier guidance of management that margins of a minimum 18% will be maintained .

Will take managment guidance of growth targets of 30 to 40% with a pinch of salt considering the Q1 results.

what is surprising is despite a rise in fixed assets the depreciation amount is lower in this quarter compared to previous quarters

New capex has done more harm then good ,I hope this doesnt turn out to be a cyclical industry ,which might effect the bottomline further with more deprication and intrest hampering the bottomline.

Disc :invested at 1100 levels.

1 Like

There was a fire incident and I guess that factory was affected for most of June and July. Apart from that not sure what’s happening here. We’ll have to wait for the call on Monday. The price didn’t correct much today which was surprising. Maybe it’s a sign that the valuations are so low that the stock price won’t react too negatively to bad news. At 1.5 times sales, any whiff of s recovery can lead to a swift rerating.

Bought a small position recently at about 580, purely coz it seemed like close to a bottom business wise. Will wait to understand what went wrong and how much worse can things get before they get better, and then increase the size if it fits the risk reward.

2 Likes

Above is Sadhana Nitro press release where they claim that they have successfully commissioned PAP plan using Hydrogen based catalytic reduction of nitrobenzene.

I believe Mallinckrodt is the first player to develop this process.

Valiant uses a different process known as Bechamp conditions using NCB as starting product (NCB is procured from group company Aarti Industries).

The most important delta is - in Bechamp process - large amount of Fe/FeO sludge is generated which can not be recycled. Whereas in Hydrogen based catalytic reduction, by products are - Aniline Oil and Aluminium Sulphate. Both of these products can be sold.

With this development, if Sadhana can really scale up PAP production, I think scales are significantly tilted in its favour to capture majority market share. The competitive position of Valiant might be weakened, the ROCE profile of PAP capex is reduced and it might become a bad capital allocation in hindsight with this information now.

We need to validate this by asking question to Valiant in concall and also track Sadhna’s progress in commercialising PAP.

Disc - No investments

21 Likes

Even Vinati Organics tried to manufacture PAP through this route but didn’t get any success in 20+ years. I won’t take the comments by Sadhana on face value as their repo hasn’t been that good in markets.

Valiant has its own struggles - they are manufacturing PAP in batch process so far and can scale the production to only 500 tons per month. To achieve higher production (800-900 TPM), they will have to get some success in continuous process.

The only good thing which has happened in recent past is that management is taking queries of all the investors by organising concalls.

Disc - Holding from higher levels ![]()

6 Likes

In fact, I have even heard Valiant management casting apprehension about success probability with Nitrobenzene route.

However, how to ignore the hard fact that world’s biggest producer Anhui Bayi Chemical with a gigantic capacity of 60K MTPA (~55% of China’s/ ~38% of world Para-Amino Phenol capacity) was in fact on Nitrobenzene route only.

[different story that Anhui has shut down factory temporarily for relocation to Bengbu Industrial park]

Also, based on some reading, my understanding is that Nitrobenzene route is evolved process therefore much more cost efficient and environment friendly.

Tarun

16 Likes

I was trying to get a sense of whether the current occurrences in Europe (related to the energy crisis) will have material impact (in positive/negative terms) on the business over medium to longer term?

IIUC, this does provide a stronger footing to pitch the company as a quality alternative supplier to larger agrochemical chemical companies based in places like Germany, but at the same time there could be some demand destruction coming from Europe. Is that a correct way to understand all this?

disc: invested

2 Likes

Brief notes from Valiant’s call today. Not covering basic sales and profit figures

PAP

- Presently 400MT/month. Trying to get to 500 by next month

- Still trying continuous for PAP. If not possible, can do semi-continuous (with batch process) with minor capex and can ramp up to at least 800MT

- Continuous will only start by FY24 phase wise

- By FY24, PAP will be 20-25% of revenue and 30% of revenue at full capacity

- Most of it will go to the subsidiary to make paracetamol

Dyes and pigments

- Will take 2 quarters to get better + Europe pick up

- We have 2 amonolysis plants supplying there, goes into textiles

- Hydrogenation greater than chlorination followed by amonolysis

- Want to diversify end user industry

- This year, dyes and pigments looks larger due to chlorination issues (Saigram plant)

- PAP will be largest - largely pharma

- Chrolophenol will be largely agro

- Long term Pharma 30%, dyes and pigments 25%, Agro 30%

Guidance

- Immediate improvement in chlorination

- Amonolysis in a quarter or two

- For chlorophenol, RM prices have stabilized and FY24 will be normal

- This year 900-950cr sales (flattish)

- FY24 expecting 20-25% growth, mainly from PAP and Pharma Intermediates

- Q4 margins to be much better than Q1-Q3

- Margins at 20-22% long term conservatively

- Expect to go to earlier RoE/RoA (don’t thknk it will reach 30% but mid20’s is possible)

Factors considered for now projects

- Overall synergy with Aarti group

- Import substitution opportunity

- 15-18% return per project

Valiant Labs and IPO

- Bharat Chemicals became Valiant Labs

- Can’t divulge product details - competitive in nature

Other points

- No more major debt lined up

- Saigram at 60% capacity utilization - improving since the fire. Should go up to 85% by next year

- RM price rise will be passed on with a lag

- Pilot / campaign based multi-product pharma plant set up with asset turns of 1x for innovation

Disclosure: First invested a few months back, been adding through the last week. Average price about 550 and up to over 4% of the PF. Looking to play the impending mean reversion

10 Likes

Audio recording of Q3 FY23 Earnings

https://valiantorganics.com/assets/investors/recordings/recording-of-earnings-call-q3-2023.mp3

1 Like

Any reason for promoters keep on selling their stake. It was 48% in 2019 & it is 38% now. Looks like they don’t have confidence of coming back ?

Some of the promoter group are in public category. If you can check on screener website you will be able see the shareholding across Aarti group. This was also mentioned by the management in one of the concalls in FY23

2 Likes

**Valiant Organics - Q1 2024 Transcript of Earnings Call Notes. Things have slowed down for them **

Extremely volatile and challenging Qtr

Revenue from operations declined by around 24% YoY

EBITDA was reported at INR 24 crores, which was declined by around 25%

The net profit reported was around INR 15 crore which declined by about 12% YoY.

Sluggishness in the sales of dyes and pigments

Renewable plant benefits to start from Q2 2024

China is also dumping their excess products

Expecting the year to be difficult

Expecting around 5-10% of degrowth in this year

Revenue Guidance reduced from 1200cr - 800 cr

Capex just pushed it for a quarter or so

Q2 FY24 seems to be on a low-demand side

degrowth in volume is around 14-15% and somewhere around 10% is the price

Land sold to subsidiary company for expansion

we don’t see any employee costs going down

3 Likes

when is the con-call for Q4 ?

Hello everyone,

I have been in this for few months and the stock is 15% down from the buying price, although I bought it with the mindset of 1-2 year.

But their financial are not in good shape,

Is it wise to hold it? Or sell it at the loss?

Thanks

1 Like