Interesting new blog post on valiant-

Technically stock seems to have bottomed out -

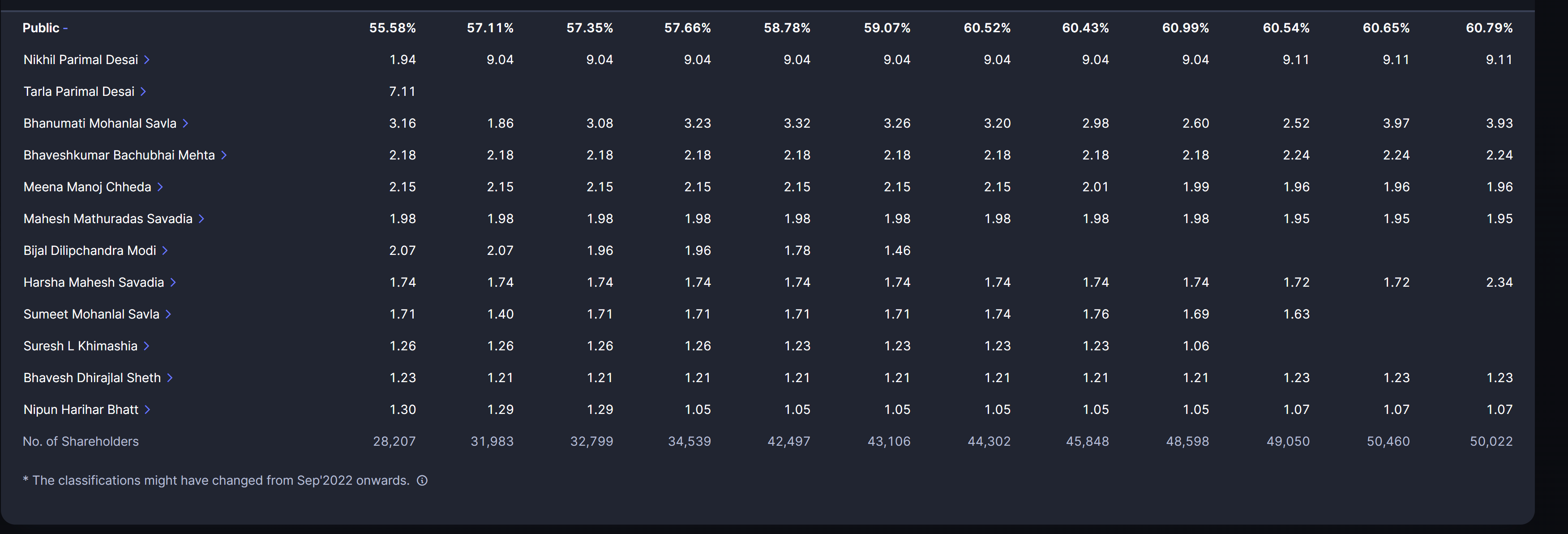

Also if you see the promoters in the retail section they have started buying the stock in the past 2 quarters.

Where is this information you’re picking up from? I can’t see any disclosures.

Is the company not doing any earnings call in FY 25?

In the absence of any earnings call how are people tracking the business?

Anyone on the group who has any meaningful insights on the business please do share it. Thank you!!

The company sells commodity chemicals, where they have no control over the demand. clearly topline indicates demand slowdown since 2022, Valiant business is cyclical and I believe the cycle is at its bottom for the following reason.

→ This year we had better Monsoon and its going get better in the coming years as the weather cycle is changing from El Niño to La Niña (google it if not known).

→ RBI will most likely start cutting repo rate as they are waiting for the inflation to settle (inflation will most likely settle soon in the coming months because of good rain fall and banks improving their credit to deposit ratio etc… to put it simply RBI has been taking strict corrective measures to curb inflation for the past few years, we are close to inflation settling down).

->Globally, central banks in developed countries have already started cutting interstate rate, this will increase the demand for the commodity products dependent on export market.

→ Technically as well stock seems to have bottomed out.

to your question. I believe the management is not conducting concall because they do not have anything to say other than the demand is weak because of that utilization is really low etc.

->To judge the management you have old concall to refer to.

→ The the promoter holding has been steady for this year.

→ there is slight increase in promoter holding the in public section (not sure why some are in public section).

→ Valiant Organics and the Aarti Group are closely related.

Disclaimer: Invested from the recent lower levels.

Valiant Organics is a demerged entity from Aarti Industries, but the connection is somewhat indirect. Valiant Organics was initially a part of Aarti Group’s operations. In 2015, it was spun off as an independent entity focusing on specialty chemicals, specifically in chlorination and hydrogenation processes, which were part of Aarti Group’s earlier business segments. The demerger allowed Valiant Organics to focus on niche chemical manufacturing independently, while Aarti Industries continued to grow in its areas of specialty chemicals, pharmaceuticals, and performance chemicals.

This separation has allowed both companies to pursue their own strategic goals and growth trajectories within the chemical industry.

I’ve been holding this stock for 975 days, which speaks to the importance of patience in investing.

One interesting aspect is that their Fixed Assets (FA) and Capital Work in Progress (CWIP) have more than doubled since the time when the stock was at its all-time high. This suggests a solid foundation for growth, and there’s a good chance that, when the time is right, it could yield substantial returns for its shareholders.

Disclaimer: I am personally invested in this stock, and my opinion may be biased. Whether my assessment proves right or wrong, I reserve the right to my own perspective.

My current average price for this stock is around ₹527, and I’m comfortable with averaging it further if needed. I’m not stuck—this is just how the stock market works. Not every stock will be a superstar right away, but with patience, there’s a good chance it will have its moment.

Disclaimer: I am personally invested in this stock, and my opinion may be biased. Whether my assessment proves right or wrong, I reserve the right to my own perspective.

Thanks for sharing your view! This stock makes up only 2.9% of my overall portfolio, so I’m comfortable with my current strategy and prepared to hold. I appreciate hearing different perspectives, but I’m set on my approach for now!

Pls give reasons for why you’re holding. Fixed assets and CWIP has doubled but profits have crashed, so that could indicate terrrible capital allocation by management. Building up capacities when time was good in a cyclical industry and then getting stuck with it.

Main thing one has to answer is, what is the demand supply dynamics for their main products? Because if chinese oversupply is there and expected to continue, then no amount of increase fixed assets is going to save the company.

had studied it when it was at around 450 levels. Passed on it because it has so many products and it’s impossible to track demand supply dynamics of them

Thank you for raising these points. Here’s a broad overview of why I’m holding the stock based on recent developments:

I’m considering these factors, along with potential improvements in demand dynamics. While challenges are present, and yes i agree last 4-5 quarters are not going in our way, there are also signs the company is taking steps to navigate them effectively.

Also, the company boasts a leadership team with significant experience in finance, chemical engineering, and corporate banking. This expertise, combined with their transparency in addressing issues such as the fire incident and low product demand as pointed earlier, suggests a well-managed and accountable company. Additionally, the re-appointments and new appointments of directors demonstrate a commitment to maintaining strong corporate governance.

As I mentioned earlier:

This stock represents only 2.9% of my overall portfolio, so I’m comfortable with my current strategy and prepared to hold. Just because I’ve held this stock for almost three years doesn’t mean I haven’t earned returns from other investments.

Disclaimer: I am personally invested in this stock, and my opinion may be biased. Whether my assessment proves right or wrong, I reserve the right to my own perspective.

Any views sirji after the Q3 FY25 results…

I think the demand is turning around. Revenue is up ~19% and EPS trued positive.

Dis : Continuing to accumulate.

Yes, kindly watch for one-two more quarter to make a solid decision.

Any views on their acquisition of Pro Zeal Green Power? They acquired a stake in it and now Pro Zeal has a DHRP which states an OFS from the same promoters- is this a red flag?

That acquisition was of an SPV floated by ProZeal with some assets meant for captive use by the company and not the main company that has filed DHRP. Several companies make these SPV acquisitions for captive consumption using renewable sources. What am I missing? So long as the deal is done at arm’s length. PS. Aarti group has a lot of cross holdings, but I don’t think anybody has found corp gorv lapse thus far with the group.

congratulations to all of them who have been patently holding I believe the cycle is turning around and its reflecting in the revenue/profitability and stock price.

I am studying Valiant since last few months and thought to share my views about the company. While Valiant saw peak profitibility and interest from investors community from FY19 to FY22, currently with declining sales and margins, the company is untouchable.

Valiant operates in consolidated industry structure for two of its major Products -Chlorophenols and PAP, Valiant being major supplier from India and other 5 players from China. PAP dynamics have chnaged with other indian players setting up capacities, that I will detail below.

Positives

Execution - The company has executed and scaled pretty well in the past, since IPO in 2016:

a) Scaled chlorophenol capacity from 5000 MT to 20,000 MT when it sensed oppportunity in form of reduced chinese competition.

b) Merged Promoter group companies and entered into related chemistries.

c) Setup 10,000 MT PAP plant at Capex of 400 Cr , majorly financed through internal accruals.

Heritage - The company has strong parentage (part of Aarti Industries) and uses the relationship that’s mutually beneficial for both the companies. Many raw materials fro Valiant are sourced from Aarti, and some of the final products are sold to group companies including Aarti.

Market Share and Scale - The company has dominant market share and scale in the chemistries that it operates in. Capacities a) Chlorination and Amonolysis - 29,000 MT & b) hydrogenation - 30,000 MT

Management - The jockeys are experts in complex chemicals and Valiant has their entire distribution network to sell the products.

Verticle integration - Company holds 45% stake in Valiant Laboratories, which is into manufacturing of Paracetamol API (9000 MT Capacity), large portion of PAP produced by Valiant Organics will be sold at arms length basis to Valiant Laboraties for Paracetamol API.

Negatives

What has gone wrong in past 3 years (FY23 to FY25)?

When Chinese PAP capacities (estimated 150,000 MT) was curtailed to 110,000 MT causing spike in PAP prices, Valiant sensed opportunity in PAP with rising prices and reducing PAP availability from China, and invested in creating capacities.

However, few things happened that broke company’s back:

Above factors had immence bearing on Valiant’s fortunes, profitibility vanished and there looks no signs of it returning back. While company was expecting topline of 1400 Cr in FY24, it actually ended up with Rs 700 Cr

While Valiant claims to be the lowest cost producer for most of its products, able to compete with China, it also suffered along with other industry players.

According to Granules, who have 30% global market share in paracetamol API, this is the worst paracetamol cycle they have seen in their history of 40 years.

Similarly on Chlorophenols, Valiant says that this kind of bear cycle was seen last in 1992.

What is the situation now?

Industry looks like consolidating with early signs of players getting bankrupt. Sadhana Nitro has not commissioned the newly setup PAP plant and defaulted on debt as per the latest Credit rating report. Few players in china are also heard of closing their plants.

Does it sounds like music in your ears? With typical capital cycle having painful consoliation for few years and market share gain for the last man standing over a period of time?

Or it feels like a most unpredictible place to be avoided? You need to decide as a invstor :)

Government support

As PAP is part of PLI scheme and there’s a strong pust by Govt to make it domestically, will Govt will provide support to the domestic industry in terms of Anti Dumping Duty or other measures from chinese competition?

Again time will tell…

Disclsure - Studying the company, no position. The post is not intended for buy /sell recommendation

@dhruva1705 who had been earlier contributor to this thread saying its an 25% cagr opportunity.

basically he is betting on **A classic non-linear turnaround where modest revenue growth (70%) triggers a massive profit explosion (350%) due to debt reduction and operating leverage, potentially doubling shareholder value by FY29 driven by mostly Net Margins expand from ~4% to ~10% without aggressive pricing.