Vinati Organics was trying to manufacture PAP through Nitrobenzene route which is a highly complex and greener way of producing PAP (Vinati has been trying to manufacture through this route for the last 10+ years) whereas Valiant Organics is manufacturing through the standard and established PNCB route.

5 Likes

Could you please explain how this will give Rs.3000-4000 Cr additional revenue?

It is typo boss it 300 to 400 crs quick calculation 550 per kg for 12000 tones give 660 cr but if you do adjustments for what is sold outside and what is sold to bharat chemical may be you will get around 400 crs.

I have added positions couple of days back and expect a recovery in the stock price as they complete expansion.

2 Likes

out of 12000 tons … 9000 tons will be supplied to bharat chemicals and rest 3000 tons to the market

1 Like

the color issue is now sorted and they are getting the off white color which is desired by the market … also they are now mastering manufacuturing it in bulk … just to update they sold 200 tons of pap in july 2021 to bharat chemicals

1 Like

perfectly said … assume 400 rs per kg for safe calculations given the price rise has been abnormal in last 8-10 months

1 Like

Where is this info from?

They didn’t update the market, I thought the plant was still not commercialised

this info is basis my meeting with the mngt … also attached this latest report

637656916559208002_Valiant Organics Ltd - Management Meet Note - SMIFS.pdf (362.6 KB)

6 Likes

Valiant Organics Annual report 2020-21

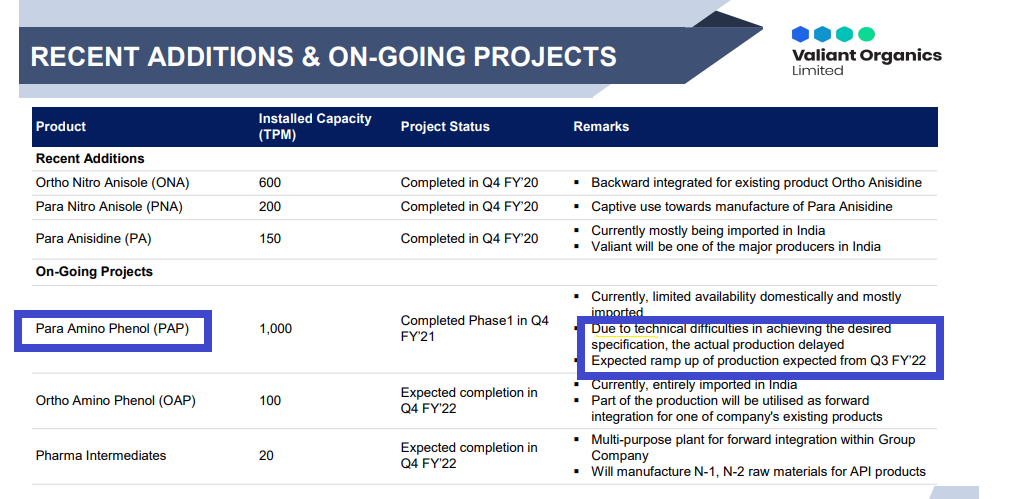

At the outset I was disappointed to note that there is no mention on PAP production progress with its details.

There is a general mention of completion of Phase I of PAP plant in three places merely reproducing the same text… But in Management discussion, there is little more additional details.

The Company has been working on scaling its capacities in the

Jhagadia facility. During the year, the Company completed the

Phase I of Para Amino Phenol (PAP); however, continued efforts

to achieve the desired specification of PAP is in progress

It appears that pilot batches have not yet stabilised with the associated colour issues.

Some saliant points.

The Company’s Phase I expansion of Ortho Amino Phenol (OAP) is also under way.

The Company has focussed on hydrogenation expansion, which has reduced its dependence on buying Ortho Nitro Anisole / Para Nitro Anisole from vendors. This expansion has enabled the Company to attain captive consumption of the aforementioned material for manufacturing Ortho Anisidine / Para Anisidine…

During the year, we completed the expansion of ammonolysis capacity at Vapi plant.

We aim to produce

drug intermediates so as to reduce our dependence on importing them. We aim to forward integrate Paracetamol in the near future. This will enable us to cater to the growing demand of drug intermediates and APIs in enduser industries with a focus on the pharmaceutical industry.

We are proactively undertaking forward integration and adding new, high-margin products to strengthen our product portfolio.

We are also backward integrating to manufacture key raw materials and reduce our ependence on suppliers and lower procurement costs.

3daa9e2a-455d-4ed3-a137-8e3a5d232b82.pdf (bseindia.com)

Discl: Invested from lower levels.

4 Likes

Management guiding for 800 Cr Standalone revenues in FY 22 and around 1100 Cr for FY23 @ 22-25% EBITDA Margins

5 Likes

Valiant Organics Investor Presentation.

Some more light is thrown on PAP project Progress.

Production ramp up expected from Q3FY22

3 Likes

4 Likes

neutral results again

Can anyone help pls?

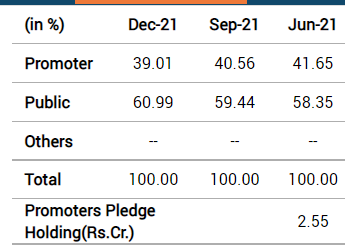

Is there any disclosure from the company or promoter why the stake is coming down by every passing quarter? In last interview (sep.21) it was told no further selling will happen but it is continuing

disc. I: Not invested, just studying … and promoter selling is a concern

2 Likes

Valiant Organics Q3FY22 Concall Highlights

Other chemistry dropped due to other segment debottlenecking activities.140-200tonnes debottlenecking in other chemicals plant

and other Chemical plant was shut down for a month for this process

Capex final project pharma intermediate and OAP in Q4

PAP utilisation levels. Batch wise 25-30%

Technical issues almost resolved.

10-20tones to 200 tonnes in last 9 months

Next FY good ramp up in next year.

500-600 tonnes to 1k tonnes in continuous process can happen in 15-20months

PAP colour issue resolved.

90% of sale to Bharath chemicals subsidiary

20cr of 220cr capex of PAP project will be used for converting from batch to continuous project

Early next year PAP 40-45% utilisation

Vol of paracetamol 500tonnes/month gradually to 750tonnes in 3quarters

As we expand we can have 20-25% margins

Pharma intermediates plant is pilot . Land parcel available to expand based on demand

45-50cr revenue

Multi product facility

and mostly used To supply to Aarti industries

Prices will be passed on MoM basis

Phenol prices has stabilized , but freight cost is high for next 2-3 months. Phenol affects only chlorophenol chemistry

24D plant on hold due to ban on the molecule. It’s same unit of PAP & Pharma intermediate

Aarti revenue exposure FY21 25-30% and

Purchase exposure 20-30% from aarti

PNA is the main product that we sell to Aarti

Technical support will get from aarti,

No price discount from aarti

FY22 850 CR ,FY23 will have 30-40% growth ,

Margins will 22-25% ebitda when things stabilize

Standalone 20-25% growth rate ,fFor next 2-3 years

Promoter selling - Donation & personal use. No strategic exit plans

Overall utilisation 80-85%,excluding PAP

10 Likes

China’s biggest PAP manufacturer to restart production . Prices are bound to come down and rationalise valuations.

6 Likes

Dear Vibhor, May I request you to share source on restart

Granules management has echoed the same thing about PAP restart in China.

3 Likes

Can’t share the report here due to copyrights. But you can search articles using the company name.

anhui bayi chemical industry co. ltd

2 Likes

Can the company compete with Chinese suppliers? Pre covid prices of PAP hovered around 150 to 20 to currently above 400 to 600.they do have the support of Aarti industries

How badly will it effect there revenues? they are already doing 200 cr topline quarterly before PAP which started in q3,so we can assume they will be able to maintain a minimum 800 cr topline in the future?

2 Likes