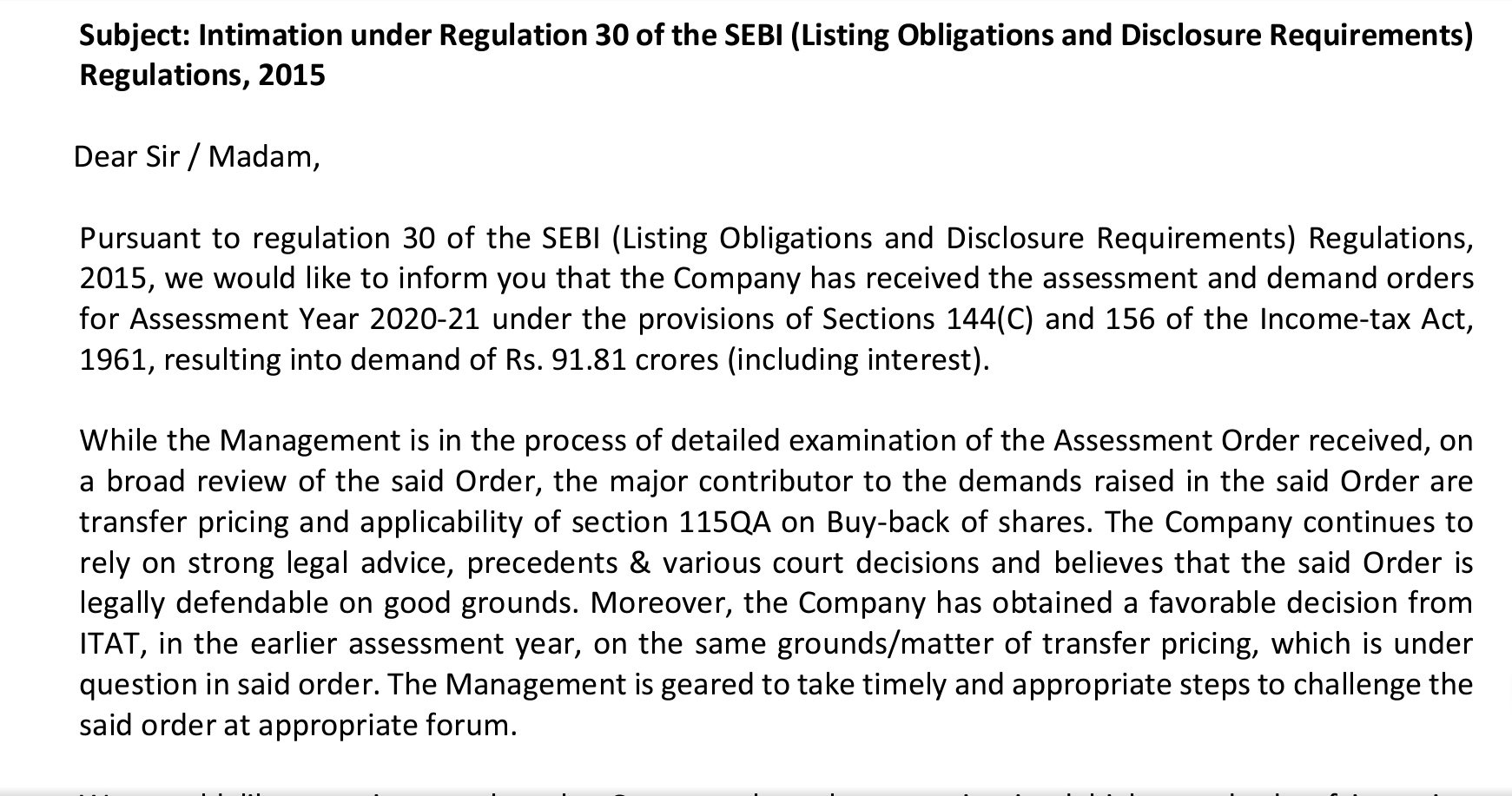

“Advertising Inflation” at crazy levels.

Excerpt from AR:

For example, advertising on Facebook, costs 47%more than the year before. Apple privacy updates in iOS 14.5,prohibits cross-app data-sharing unless the user chooses to opt in. This has had significant ramifications leading to less effective advertising across Facebook and Instagram.

Very dissapointed with OCF numbers

74(17) 41(18) 204(19) 214(20) 326(21) 88(22)

• 0.5 Million No. of Unique Customers

• ~20,000-25,000 No. of SKUs ~

• US$ 29 Average ticket size

• 253 K New customer acquisition in FY22 (Adjusting for essentials, growth rate would be 16% over FY21 and 60% over FY20)

• 40% Customer retention rate

• 8 No. of Manufacturing Facilities

• 63 Million Meals provided to school children in India, US and UK since inception of our flagship one-for-one meal initiative

• Vison: Be the Value Leader in Electronic Retailing of Jewellery and Lifestyle Products

• Revenue split: 70% Jewellery & 30% Non-jewellery

• Revenue by format : TV-63% & Digital 37%

• USA Revenue – 68% of total

• UK Revenue – 31% of total

• TAM increased by 20% due to German presence

• Ventured into manufacturing apparels

• Focus on expanding non jewellery portfolio

• 255 revenue contribution from in house brands

• The call centre in India became operational. This has helped us in achieving excellent CSAT (Customer Satisfaction) scores of 95% for both US and UK . Presently, ~50-60% volume of US & UK is being catered by Indian call centre

• We acquired one apparel manufacturing unit thereby expanding our lifestyle products category.

• Further, commissioning of GEEK+ robots at our warehouses in US and UK have been completed which is expected to improve the picking productivity by almost 3 times vis-à-vis conventional manual picking, while reducing error rates. We also acquired majority stake in a packaging company in Sri City. This investment is already enabling us to cut our packaging box costs in US and UK.

• On Key Focus Areas in FY23 Our business model revolves around customer centricity with a wide range of product, engaging content and deep value proposition supported by a vertically integrated supply chain. In FY23, our key focus area will be to further strengthen our omni-channel presence enabling cross-selling potential and resultant improved customer lifetime value. We also intend to increase our TV reach by increasing the number of households we broadcast to. We will continue to invest in strengthening our ‘Digital’ capabilities. We will work on further improving shopping experience of customers by improving various customer touchpoints, while maintaining overall profitability. The recent challenges related to inflationary trends and recession fears might affect consumer sentiments in the short term. However, with focused strategic pillars in place which are ‘broadening our omnichannel reach’, ‘expanding customer base through compelling content and promotions’, ‘increase retention by improving customer experience’ and ‘increase repeat purchase through varied product offering’, we expect continued and sustainable growth in the medium and long term.

• Also, we have started to directly serve our B2B customers from our existing supply chain in Asia and that seems to result in better ROIs for the Group.

• We have undertaken a cost optimisation program in the recent times and are expecting annualised visible saving of US$ 6 million to US$ 7 million through these cost efficiency initiatives

• . Negative free cash flow of ` 214 crore are on account of planned CAPEX towards technology infra upgrade, warehouse automation, free view channel upgrade in UK, new headquarter in US and initial setup cost of Germany

• Our warehouse automation project was another significant investment of the year. This refers to GEEK+ robotic automation and is set to deliver huge benefits on operational efficiencies. We expect that nearly 55-60% of the picking will be done through robots in future. IT-related projects on technological infrastructure upgradation were another key investment of the year. Besides, we also purchased land in the United States to move our headquarters from rental premises, this investment is expected to provide synergy in terms of cost optimisation and functional integration.

• Core investments FY22:

• Kickstarted German operations and stepped investment in digital marketing across social media, OTT and OTA Undertook warehouse automation with GEEK+, which is expected to improve the picking productivity by almost 3 times vis-à-vis conventional manual picking Upgraded technology infrastructure on Salesforce Commerce Cloud Updated Mobile App 3.0 and OTT Apps in US and UK Launched direct-to-consumer brands TAMSY and Rachel Galley to strengthen brand portfolio Purchased land in Texas to build new integrated headquarters of Shop LC (US). To bring operational synergies and substantial cost savings Acquired 60% stake in Encase Packaging to consolidate existing supply chain and gain substantial savings in packaging of jewellery products. This will also strengthen our efforts towards developing a sustainable packaging for our products.

• Key benefits of GEEK+ Robots Better customer experience due to faster shipping time Reduced delivery days by ~30% and fewer lost orders Reduced operational costs with a smaller ~2.5-3 years payback period

• Advertising Inflation”

Excerpt from AR:

For example, advertising on Facebook, costs 47%more than the year before. Apple privacy updates in iOS 14.5,prohibits cross-app data-sharing unless the user chooses to opt in. This has had significant ramifications leading to less effective advertising across Facebook and Instagram.

I think two major drags on profitability are the jump in digital advertising costs on Facebook (which a lot of online businesses have faced across the world ) and the investment in developing Germany market. The negative impact of these two factors on profitability is diminishing . I think with savings from cost cutting initiatives (as outlined in the post by @SanketB ) kicking, chances are that the stock has bottomed out as far as margins is concerned. The post-Covid soft landing has been experienced by a lot of e-commerce businesses. There is a lot of pessimism built in the stock price. (Discl: A small tracking position)

Qoq EBITDA margins increased. Q3 is usually the best quarter. Month over month yoy degrowth also slowed down. All it needs is some Increase in revenue and operating leverage will take care of the rest. Mgmt talked so many times about this.

On technical charts the stock seems to be bottomed out. Recently in q1fy23 vijay kedia also increased stake.

Disclosure: Invested with small % of pf and planning to increase.

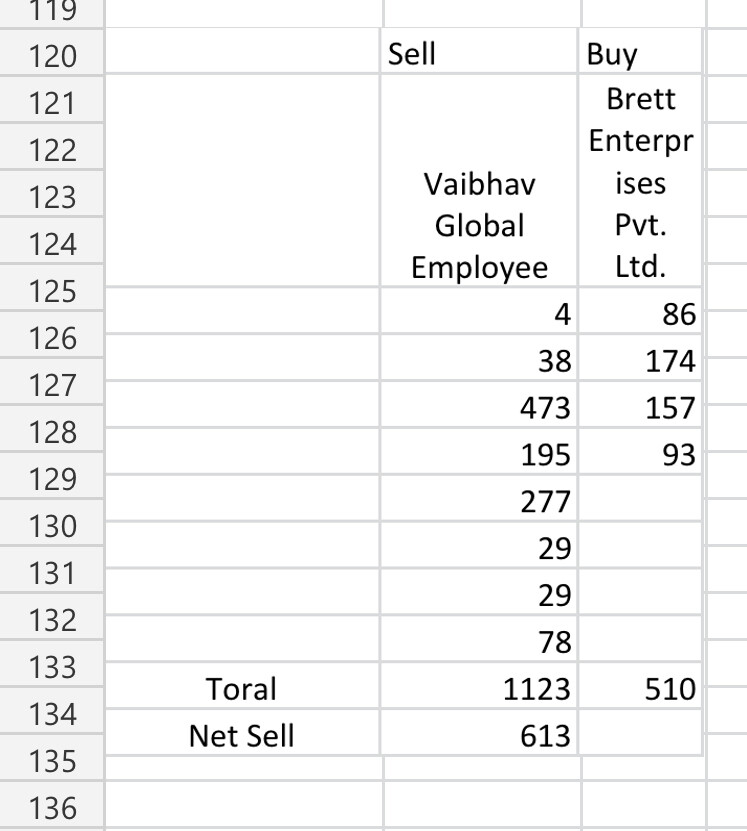

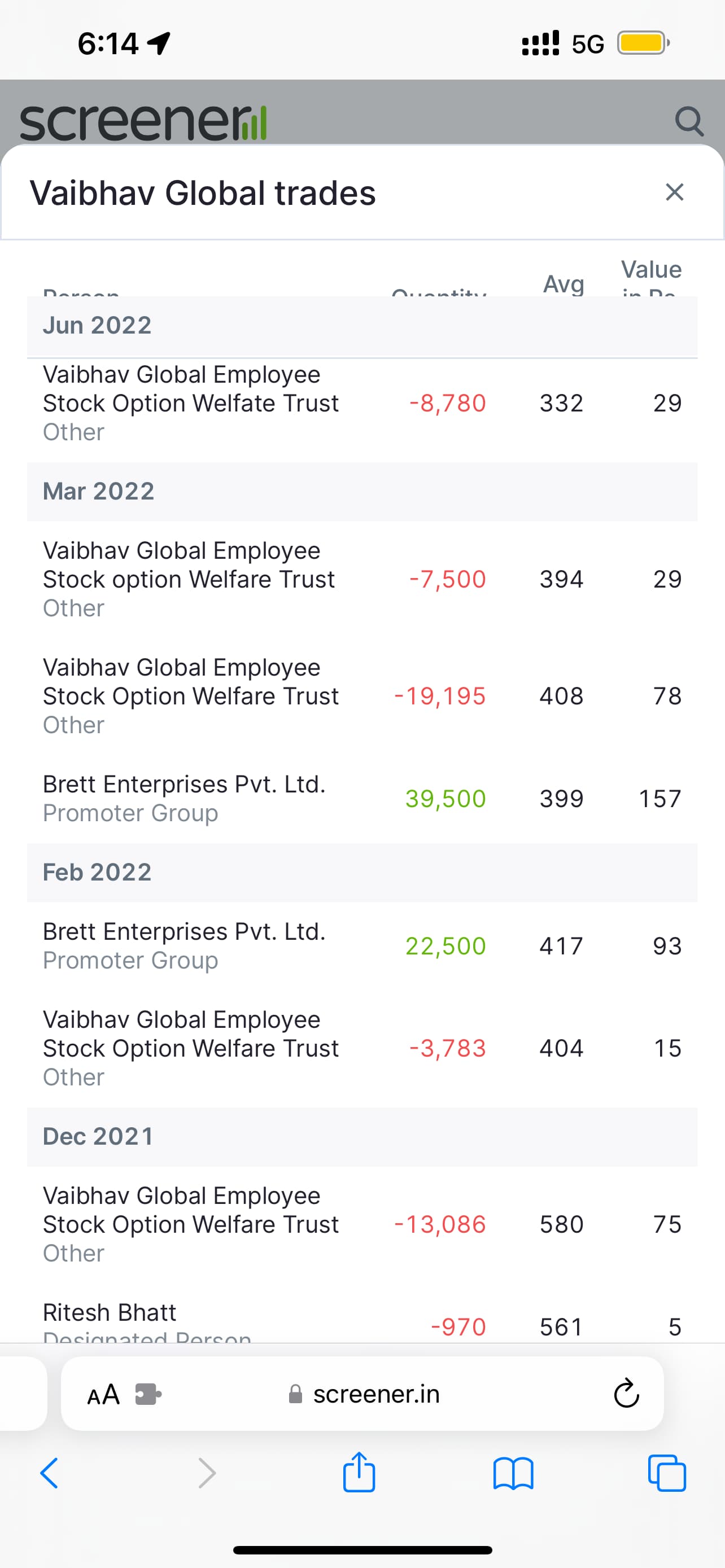

Since from March 22 there’s is buying and Selling by Promoter Group.

From screener one time got misjudgment that promoter is buying. But actually when I calculate promoter buy about 510Cr worth Share.

VGL Employee Option TRUST Have Sold about 1123cr worth share.

In this case employee or promoter is net seller

Also what we should interpret from this transaction ?

Employee Selling their position should interpret as positive or negative?

Technically bottom was made. coupled by promoter buying, vijay kedia increasing stake. And now the result. Revenue jump by 2.8% qoq thanks to operating leverage eps jumped from 1.2 to 1.4 qoq. Sometimes technical charts give early indication

Market valuation is for the future not the past of the company. The revenue growth guidance has been lowered yet again. Just see what is happening to Amazon. It has been butchered because Holiday sales are expected to be lower. This effectively means that imo it is too early to celebrate the technical predicted fundamentals narrative. I expect it to give negative returns in next 6 months at least. Don’t have visibility beyond that right now.

Then how do u justify stock price getting butchered even though revenue didn’t decline much since last one year? stock price follows the eps right?Plus technicals don’t lie. Price volume reflects everything much before fundamentals show it (check the price volume of best agro before Q2FY23 result the volumea were screaming and the q2fy23 result was a blast, but by the time result was out everything was priced in). There are people who knows the company better than we outsiders and they are buying. That’s what is reflected in price volume.

Honestly speaking I expected the revenue to degrow on sequential basis. Now q3 being a festive season will be good. Even if it’s somewhere around q3fy22 then due to operational efficiency (mgmt told about this in past concalls) eps will blast again. To me it looks like a cyclical play + operating leverage. So sequential eps growth matters to me most. I don’t care much about revenue growth. Even if it stays flat eps will grow on sequential basis. Everything seems to be priced in when stock doesn’t react much on bad result (q1fy23 result). Plus I have buying price comfort around 313. So I’d bet on the future eps growth rather than narratives. It’s not a buy and hold forever type of stock entry and exit timing matters a lot

Decent result. Finally normalcy returning. But would definitely need to get to know more about the cyber attack, reduction in retention and repeat orders. Hopefully, we would be on the blunt end of operating leverage EOY.

Yet to listen to concall. Would update this post that. VaibhavGlobal.pdf (5.2 MB)

Update: Nothing, nada, nope. No analyst asked this. It’s like mgmt had already privately discussed this with them before.

Slow growth of 8-10% guided for next year.

Vaibhav Global earnings call highlights for Q3FY23.

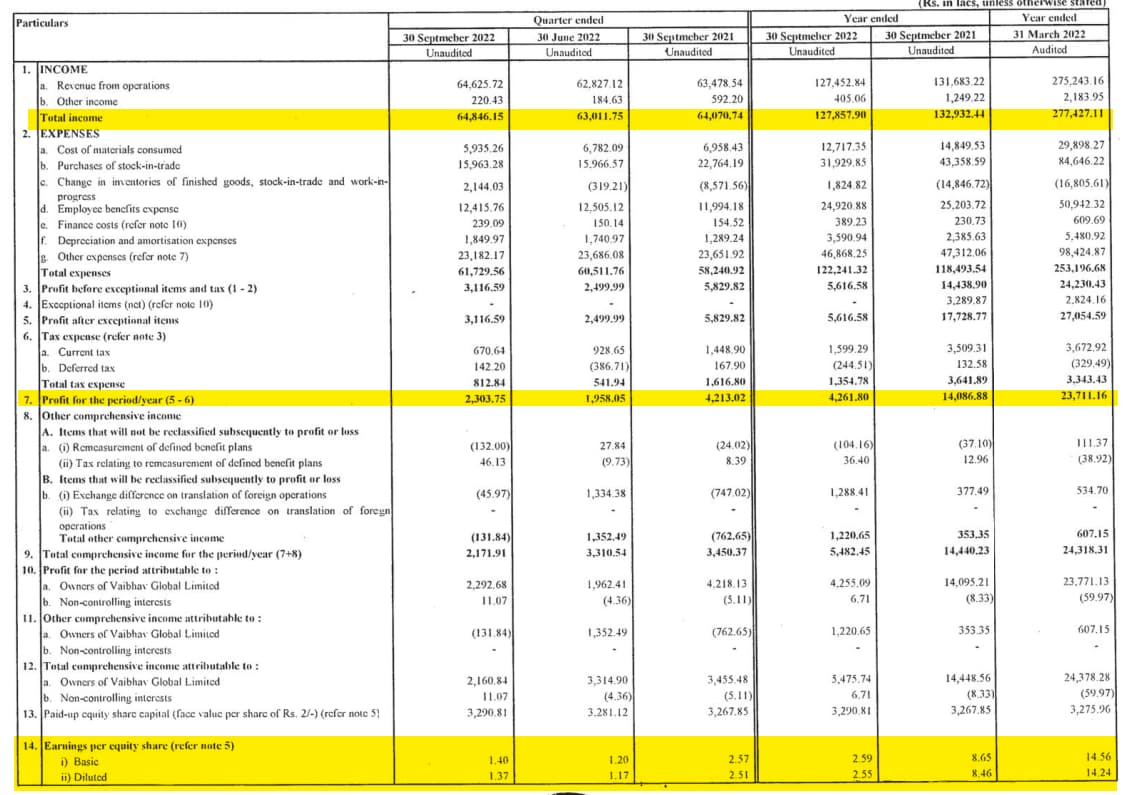

Sales for the quarter were Rs. 724 crores, down by 3.6% from Rs. 750 crores in the third quarter of last year. However, the topline is encouraging over pre-COVID period of Q3 FY20 with a strong growth of 28.5%. This performance is with the backdrop of current moderating consumer demand amidst inflationary environments. In our UK market, many of major delivery partners are facing strikes which had an industry wide impact on deliveries. Further, during the quarter, we faced a cyber-attack which resulted in temporarily disruption to our US and UK businesses. The company has demonstrated resilience in current economic environment as our revenue growth would have been flattish YoY if we negate the impact of cyber-attack and delivery disruption.

Our gross margins continue to remain strong at 60.6%. Our vertically integrated business model allows product differentiation with lower ASP and helps us maintain market leading gross margins.

During the quarter, our Germany business continued its growth momentum and is now clocking approx. 1.4 million Euro revenue every month. Other business matrices are also trending positive. Today, we are dispatching more than 3,500 pieces a day. In terms of customer engagement, our CSAT score in Germany is 96%. We are under discussion with other affiliates to gain more households in Germany.

Our D2C brand- Rachel Galley is performing very well with 200% YoY revenue growth on low base.

In US, even though inflation is inching downwards, consumer sentiments remain muted.

We are taking proactive measures to mitigate the impact of these headwinds on our business, including expanding portfolio of under 10 and 20 dollar products, content improvement, expand our TV footprint, digital and OTT promotions, etc.,

Our vertically integrated supply chain network spanning 30 countries is the backbone of our business and a key differentiator. It is helping us with increased product availability. The low cost manufacturing with value sourcing enables to serve value conscious customers in our addressable markets in US, UK, and Germany, thus achieving industry-leading gross margins.

Considering current macro indicators, we expect to achieve flattish to 2% topline growth in Q4 and end this fiscal year with negative 3% to negative 2% topline growth. For FY24, we expect to deliver revenue growth in 8% to 10% range with strong operating leverage over current year. However, our mid-term outlook remains intact, and we expect to deliver mid-teens revenue growth in subsequent periods with decent operating leverage.

Shop LC (US) had a decline of 11.3% in sales which was majorly driven by the weak consumer sentiments and cyber-attack in last quarter. However, with declining inflation rates in US, we hope that it might trigger the consumer sentiments positively and may create new opportunities as the US economy continues to evolve

In Shop TJC (UK), growth in ‘new tv customer acquisition’ on Freeview TV continued during the quarter reassuring our investment in upgrading our channel position. However, weak consumer sentiment in UK overweighted the growth prospects and hence Q3 revenue have shown a decline of 10.9% YoY. Performance in UK were also partly affected by the cyber-attack & disruption in the delivery market during the quarter.

59% of new customers being acquired digitally.

The reach of our TV networks by the end of Q3 FY23 was approximately 129 million TV homes, which is ~2% higher YoY. We have been expanding our customer base by leveraging diverse product portfolio and omnichannel presence. Our unique customer base is at half a million, new registrations on TTM basis are at 3.2 lakh. New customer acquisition on TTM basis stands at 2.4 lakh, which is lower by 1% YoY but significantly higher by 79% over pre-COVID period of Q3 FY20.

We have more than 250 people within our product development team that constantly comes up with new ideas, new product, and so more-and-more manufacturing is going towards our own units. So, predominantly, jewelry will be manufactured by us and apparel, the ladies fashion garments are manufactured by us. Within Jewelry and Fashion Apparel a very small amount that we buy from outside. We buy like home product or beauty product or accessory, handbags that we buy from outside.

Customer Acquisition Cost

On TV, the store for acquiring and selling is same. So it’s very difficult for us, it’s impossible for us to differentiate what is acquisition cost and what is the selling cost. So we don’t look at it that way. How we look at television broadcasting is that within 18 months, the TV cost, the broadcasting cost should be 10% to 12% of our revenue. So, we look at it in 18-month basis.

On our digital customer acquisition, we try to acquire customers at one-third the lifetime value of that customer. And different channels have different lifetime value. For example, Google, Facebook has about $70 to $100 lifetime value, whereas OTT like Roku or Fire TV or Apple TV, there is about $2,500 lifetime value. So we try to keep our customer acquisition cost at one-third the lifetime value or below one-third the lifetime value.

our model is that we would source product or even third-party brands to be sourced, but only that will afford our gross margin of 60%. If it is lesser than that, we just don’t entertain that brand. So that in fact would exclude, say, Apple or Samsung or Dell products for us. And we are happy to stay in the space where our brands would, over the years, become more ubiquitous and known and would have developed equity value within the brands.

other income includes the foreign exchange gain, which is around $800,000. So it’s around Rs. 7 crores to Rs. 8 crores. Apart from that, the other income is mainly will be received through interest or the cashbacks from credit card companies.

Unaddressed market (approx figures)

US: 10 mn households out of 75mn

UK: fully distributed in 27 mn households

Germany & Austria: 15 mn households

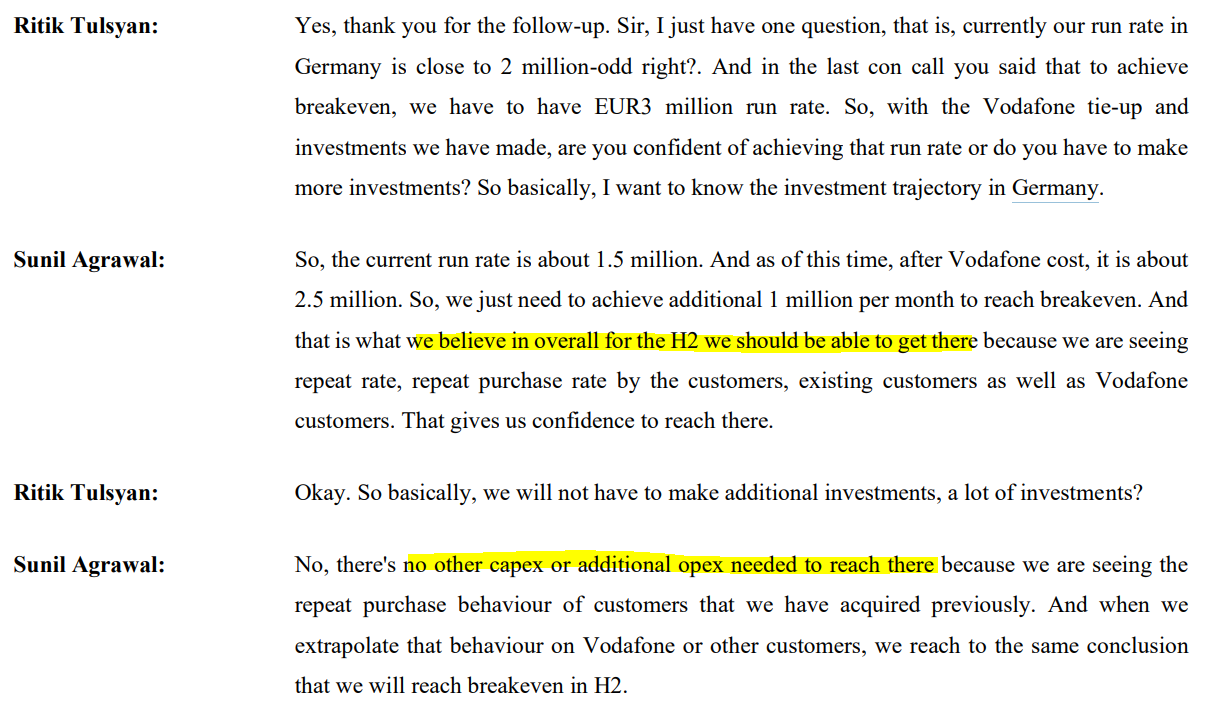

Germany:

So if it was not for inflation or current subdued environment, we would have been profitable earlier. But we are still feeling fairly comfortable to become breakeven in H2 of next financial year. For the full year, we won’t be profitable, but we will be breaking even in H2 of next financial year.

, the current run rate was EUR 1.4 million, about $1.5 million, and the profitability comes at EUR 2.5 million. That is a current state. But now, from next year, we may get more airtime or we may have additional expenses. So we believe that it will need to be around EUR 3 million for it to breakeven at that level of expense. So, this is what we’re expecting in H2 of next year. We’re expecting about EUR 3 million per month net revenue.

once Germany is successful and profitable and scaling well, we may look at Japan next before coming to India.

Imp points Vaibhav global Q4FY23 Con-call & Investor meet:

• FY 23 Rev - 2691 vs 2752

• FY23 EBITDA – 227 VS 303

• FY 23 PAT – 105 vs 237

• QOQ Revenue has declined to 693cr from 724cr & EBITDA 55CR from 61cr & PAT 23cr from 39cr

• Recommended final dividend of Rs. 1.50 per equity share making annual dividend to be Rs. 6.00 per equity share

• Expect expenses to grow at rate lesser than revenue growth & thus operating leverage playing out

• Will break even German by H2, right now at 60-70% level

• 5% of sales annually approx. should be auction sales at 1$

• Uk & US both struggling last 21 months in local currency numbers

• Want to increase lifestyle product mix to 50% from 28% by Fy 2028

• Opportunity is there to Cross sell & get more wallet share, with focus on digitisation

• Last 8 quarters was period if investment, now investment will only be in Germany till we reach breakeven level, leverage should start playing & we should see that in our numbers

• Can reach 15-20% EBITDA below 1 Billion $ revenue

• 20 Billion $ should be approx. addressable market for us globally

• Our moat is value proposition in markets we operate, for example for 60$ product sold by competitor we are in between 50-55$

• See a runway of next 8-10 years attest with current business model

• In US and UK, the macro challenges are weighing down consumer sentiments and resultant demand, however, we are taking all mitigating measures like focus on lower ASP products, increased air-time allocation for under 10 & 20 $ products. Further, we are continuing to augment our reach by adding more TV cable and OTA households. Our strategic partnership with Vodafone Cable Network in Germany has enabled us to extend our reach to additional 13 million households, thus expanding our presence to approx. 90% of the total households in Germany.

• The reach of our TV networks by the end of FY23 was 141 million TV homes, which was 124 million in FY22, i.e., ~14% higher YoY. New registrations during 12-month were 3.0 lakhs comp141ared to 3.18 lakhs in FY22. This is significantly higher by 69% over pre-COVID period. 57% of the new customers were acquired digitally in FY23 vs 56% in FY22.

• Guidance: to deliver 8-10% revenue growth in FY24 and to deliver mid-teens revenue growth in subsequent periods with decent operating leverage.

• Gross margins at 61% reflecting strength of vertically integrated business model

• EBITDA margin at 8.0% vs 6.9% in Q4 FY22. YoY improvement on account of cost rebase and better pricing

• Unique customer base at 4.6 lakhs with new registration number at 3 lakhs on TTM basis

• Current revenue mix: ~30% of B2C revenue Target revenue mix: ~50% by FY27 of B2C revenue

• Global household reach 141 mn

• 87% retention rate for 20+ pieces

• Update on Germany: TAM increased by 20%, Now clocking monthly revenue of Euro 1.4mn+ at 60%+ gross margins Omni-channel presence (digital is now 29%) Covering 40mn HH, dispatching 3.5k+ pieces/day

• Partnership with Vodafone in Germany-

• Weak numbers due to cost-of-living crisis in UK, Inflationary pressure & low consumer demand in all geographies

Sells jewellery and other fashion related stuff in US, UK, Germany and Canada

Sourcing from India & China

Uses silver, gold, platinum, steel, brass, copper and bronze

Machines used for precision and polishing on jewellery

Sells on TV channels in US and UK, D2C website, marketplaces like Amazon, OTT platforms like Fire TV, Roku etc, Social media platforms like FB, Instagram

FY23 review

Vertically integrated supply chain combined with strong sourcing enabled them to maintain gross margins at 61%

EBITDA margins were lower at 8.4% because -

Short term impact of investments on digital capabilities

Losses in Germany

Macro slowdown in UK

Cyber attack in Q3 caused disruption

Market share improved despite poor industry performance

Segment Mix

Jewellery

2% growth over FY22

1914 Cr

Non-Jewellery

-13% over FY22

696 Cr

Geography Mix

US

68% revenue mix

-11% over FY22

UK

27% revenue mix

-8% over FY22

Germany

38M households

3500+ pieces in a day

Monthly revenue run rate = 1.4M Euros

Facts

141 M households reach in US, UK & Germany

Repeat 23 pieces per customer p.a.

38% retention rate

Volumes (FY23 vs FY22)

TV - 5.3M vs 6.9M

Digital - 4.4M vs 5.4M

ASPs (FY23 vs FY22)

TV - 38$ vs 32$

Digital 27$ vs 24$

Channel Mix

TV - 1633 Cr

Web - 977 Cr

Management commentary

Remain well.poised for long-term sustainable growth with our unique value proposition, which holds huge growth potential.

Cost optimization programmes saved $4.2M = 35 Cr

New customers on TV increased by 8% in UK

With 31 brands in the portfolio, the focus remains on enhancing their performance. Currently, revenue from branded products contributes approximately 29% to the overall B2C revenue mix, while the target is to increase this share to around 50% by FY27.

Focus on customer retention and repeats

Aim to increase share of digital to 50% by FY28

Aim to increase share of Lifestyle category to 50% by FY28

During the year FY24, management expects to deliver revenue growth within the 8% to 10% range. However, the mid-term outlook remains intact, and we expect to deliver mid-teens revenue growth in subsequent periods with operating leverage

New Initiatives

Expanded product portfolio under $10-$20 with increased airtime

Started Live TV for live video commerce

Invested in Salesforce Commerce, Shopify, Salesforce Marketing, Salesforce Cloud

Robotic Automation at US & UK warehouses

Partnered with North beam and Triple Whale in UK to track customer journeys to optimise marketing spends

Added hollow jewellery gold jewellery line (bar pendant, bar ring and bar earring) in 9, 10, 18 and 22KT and platinum

Added ultrasonic stone cutting machine for precise cutting

Push for innovation with monetary reward for 1% of sales for game changing ideas. 6% of revenue comes from innovation programmes of past

Collaborated with Rangeme platform for onboarding new brands on the channel

Partnering with engineering and design institutes for talent and skills

With Design Thinking Approach, they always keep our customers at the centre of every innovation. Conducts ethnographic interviews directly with the customers to understand their pain points before coming out with a solution, apart from that, we do conduct Focus Group meetings with customers to discuss products, processes, and engagements.

Improvised warehouse management process for significant increase in the productivity in picking, from 500 per person per day, to 750 per person per day.

Acquired Encase Packaging in FY22 that reduced packaging cost

Key update from Q1FY24 results: The goal post of breakeven in the Germany operations postponed by 1 Year and that too with additional investments → shifted to H2FY25 [was projected as H2FY24 earlier]

-------------------------Edited on [03-Aug-2023]: Q1FY24 Conference Call Notes :-----------------------

EBITDA Margin Improvement (2%)? Cost Optimization: Logistics cost improvement – Order Clubbing | Shipping and IT cost negotiation | Marketing Cost improvement

Germany operations break delayed by 1 Year? Got additional opportunity for airtime, which comes occasionally | Investments planned to make in Q3 | New airtime takes 12~18 months to become profitable. Hence, Profitability will be delayed.

Volume down but ASP going up? Inflationary environment. People buying high value items (gold products).

Q1FY24 has sales growth of 5%. But, comparable YoY Q1FY23 had a sales de-growth of 8%.

Right to Win: Vertical Model [Manufacturer and Retailer] | Low-Cost Operator

Germany operations guidance? Base too small. Need to see how it scales up. However, inference from competitors scale is that Germany’s revenue shall exceed UK in the long term (7+ Yrs.) by 20~30%.

Looks like the stock price is already running ahead of improving fundamentals. Lets see what happens. Although this year they should report slight growth. Sometimes price makes top and bottom much before the actual events. I was wrong last year lets see if I’m correct this year.

Technically the stock made a gap up before q1fy24 earnings. Gaps before earning or after earning are very powerful and signifies a change of price trend.

lets see.

Disclosure: Invested.