Completely agreed on all fronts. Vgl actually does lot of experiments including experimental product launches and learns from their experiments. Eg: if they launch a product and it is not seeing good traction with customers they have a clearing mechanism which ensures that unsold products do not pile up in inventory. This is called rising auction method wherein products are all priced at $1 each and customers get to bid for the products. Very interesting! Low working capital is seen. the innovative culture and processes which enable low WC are unseen.

Key negative to current Valuations imho is whether they can sustain current growth momentum. Pre covid they used to grow 15%-17%. Until how long can they grow topline at 25% is the key question. When this growth stops, I expect some derating. Germany business scale up might take some time. I personally don’t expect it to contribute significantly (> 25%) to topline anytime before 7 years. However the growth trajectory is what market would discount whenever that becomes clear after initial business scale up.

Regarding valuations, as per my understanding market is OK with providing high valuations to companies having # Consistant and # Predictable 15 % topline growth with a very high quality and having a huge runway of growth ahead.

E.g. Tasty Bites, all other paint nd FMCG companies.

so, 25% growth, I guess even market is not expecting else, considering the quality, it may trade at 3 digit PE.

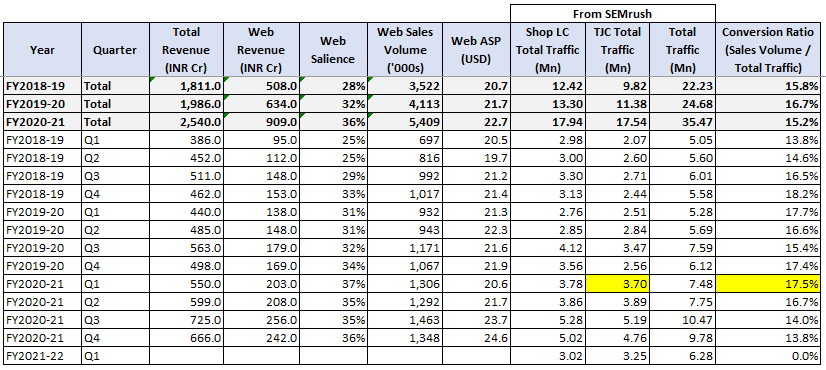

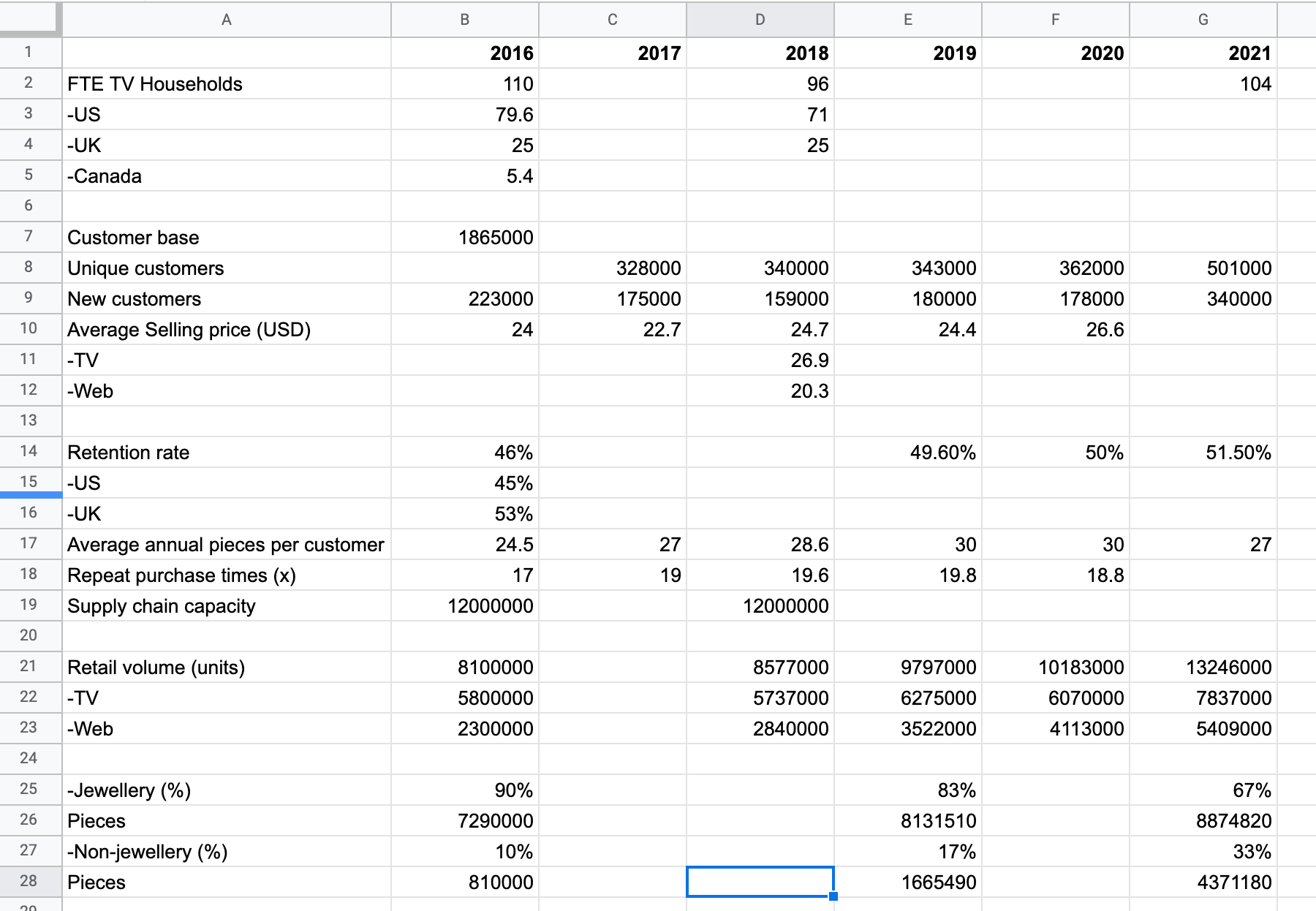

Analysis of web traffic on Shop LC and TJC indicates very high correlation with web revenues of VGL… Last 3 years data has a correlation of 0.94! This can be potentially used for projecting the web revenues and hence, overall revenues of VGL for upcoming quarters with somewhat good accuracy.

ASP from web revenues is increasing YOY by approx. 5% and volumes have grown significantly in FY21 (~ 30% growth over over FY20)

Conversion ratio has declined by 2 - 3% points in last couple of quarters

For Apr and May 2021, traffic per month is approx. 3.15 mn vs 3.26 mn in Q4 of FY20-21. This indicates that chances of sequential growth over last quarter look bleak at the moment…

Good numbers, at first glance. This, plus the loan waiver news above, should be positives in days ahead.

Interim Dividend of Rs. 1.50/‐ per Equity Share (on the face value of Rs. 2/‐ per Equity Share) for the financial year 2021‐22.

Procure products from 33 countries. Rapid product diversification. 25000 unique items. 150 new products added every day. Keep close eye on emerging trends, fashion, needs.

Commerce retail operations in Germany. 38M TV house holds. 17M households getting ShopLC gmbh.

Launched TJC+ for UK. Free and fast deliveries. Benefits will accrue in terms of retention and registration.

102.5M TV homes in US and UK. 17M in germany.

500M people.

2.9 lakh new registrations.

Retention rate of 46% is Impacted by high customer acquisition. Essential items offered last year.

Guidance of 16-18% retail revenue growth in constant currency basis in old geographies.

Non jewellery includes: Fashion, lifestyle, beauty, essentials. Provides diversification.

Budget pay contributed 38% to retail revenues.

Offer budget pay for high price. 2-6 installments. 1st is charged up front. Subscribed to fraud check mechanisms. Only good customer orders flow in and are accepted. Even in peak pandemic period, bad debt was 1%. Recovered some more. It is 0.7% now.

We have taken new distribution : ota in US and beauty channel in UK. Sometimes product mix also makes a difference. Essentials made web extra elevated last year.

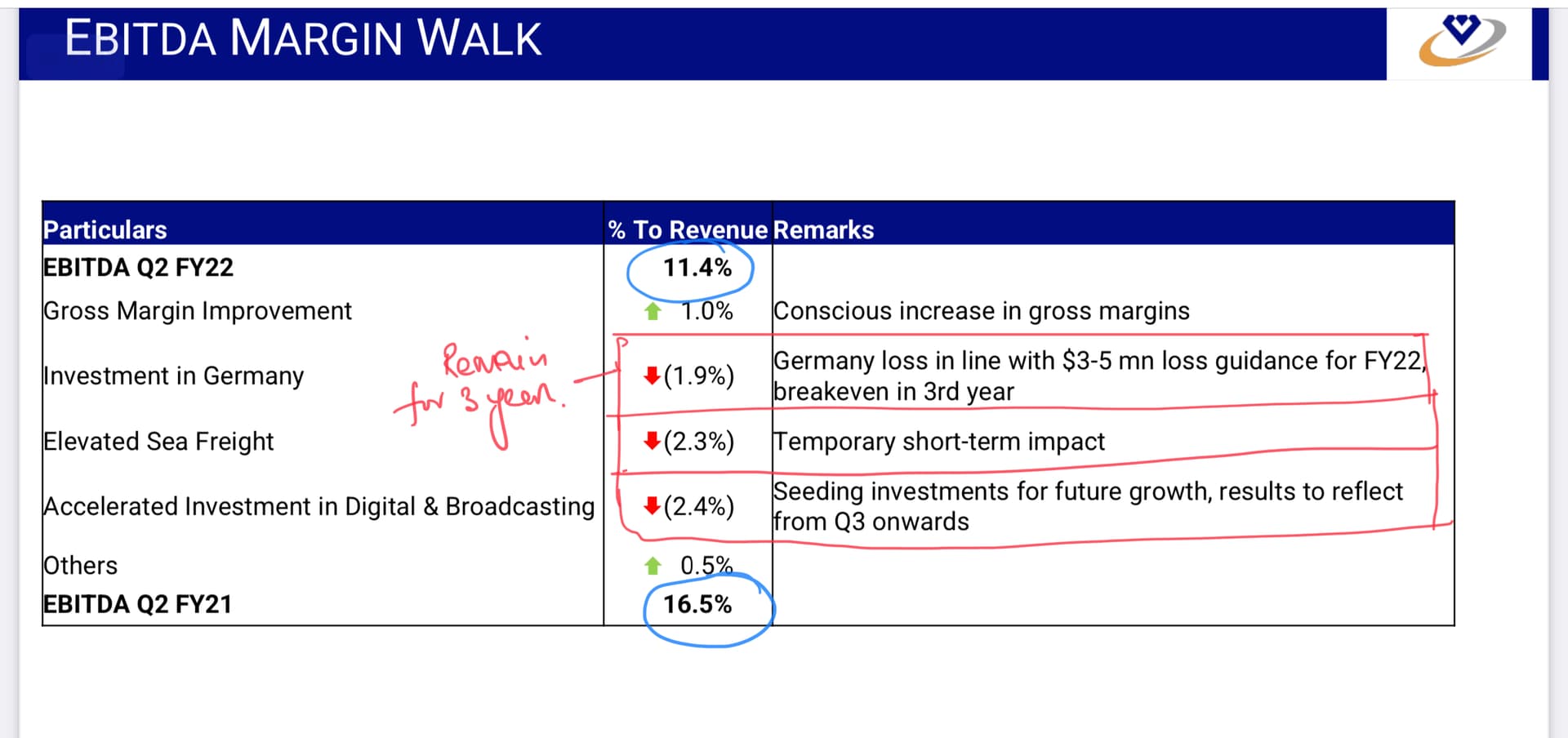

Content & broadcasting expenses has gone up 45% YoY. We took new homes that is one reason. Second: digital marketing. US and UK market will have continued leverage.

ASP tend to go up when jewellery is more. Essentials is more around 10-12$.

Germany is in beta phase. Own studio will be operational in this Q. Will start sales from next Q.

Germany signal goes to Switzerland & Austria too. We are already shipping to Austria.

UK signal goes to Ireland and Scotland too.

QVC is at 60$ per household. We are at 3$ per household. Key difference in strategy is they sell 3P brands. Our strategy is to develop our own brands, like Zara. We dont know what the ceiling is. Noone else has tried this before.

Marketplaces in FY21 was 8M$. In Q1FY22 15cr of marketplace revenues. 21cr in FY21. Sold bunch of essentials in marketplace in Q1FY21.

Social DR 4cr in Q1FY22, 1cr in Q121.

Salaries: We increased wages in US, UK, & also hiring for germany.

Introducing robotics in US and UK warehouses.

Will utilize cash to establish own HQ in US, UK, Germany. After that if cash is left will give an extraordinary dividend.

Want to focus on 20000-25000 items only, not go amazon way with tail of products. Spreading too thin dilutes value for the customer.

Advertising is something they have thought about; Makes more sense for marketplaces like amazon not for VGL. Why would anyone advertise against VGL proprietary products.

Live only 4 hours in beauty channel. It was profitable from variable cost PoV. Right now only 4 hour live.

Dont take any product which gives < 50% margin.

App sales are growing faster than e-commerce sales.

Apparel is having the best growth rate for us.

Investments in IT will only accelerate. Tech is very rapidly evolving. We have to be ahead of the curve.

The stock has been consolidating for almost 3 months now and undergoing time correction. With the good nos. this quarter the seemingly stretched valuation has come down to acceptable levels for the kind of nos. that the business is throwing which IMO is among the best in the history of the company.

It would be interesting to see how the next phase of growth would materialize.

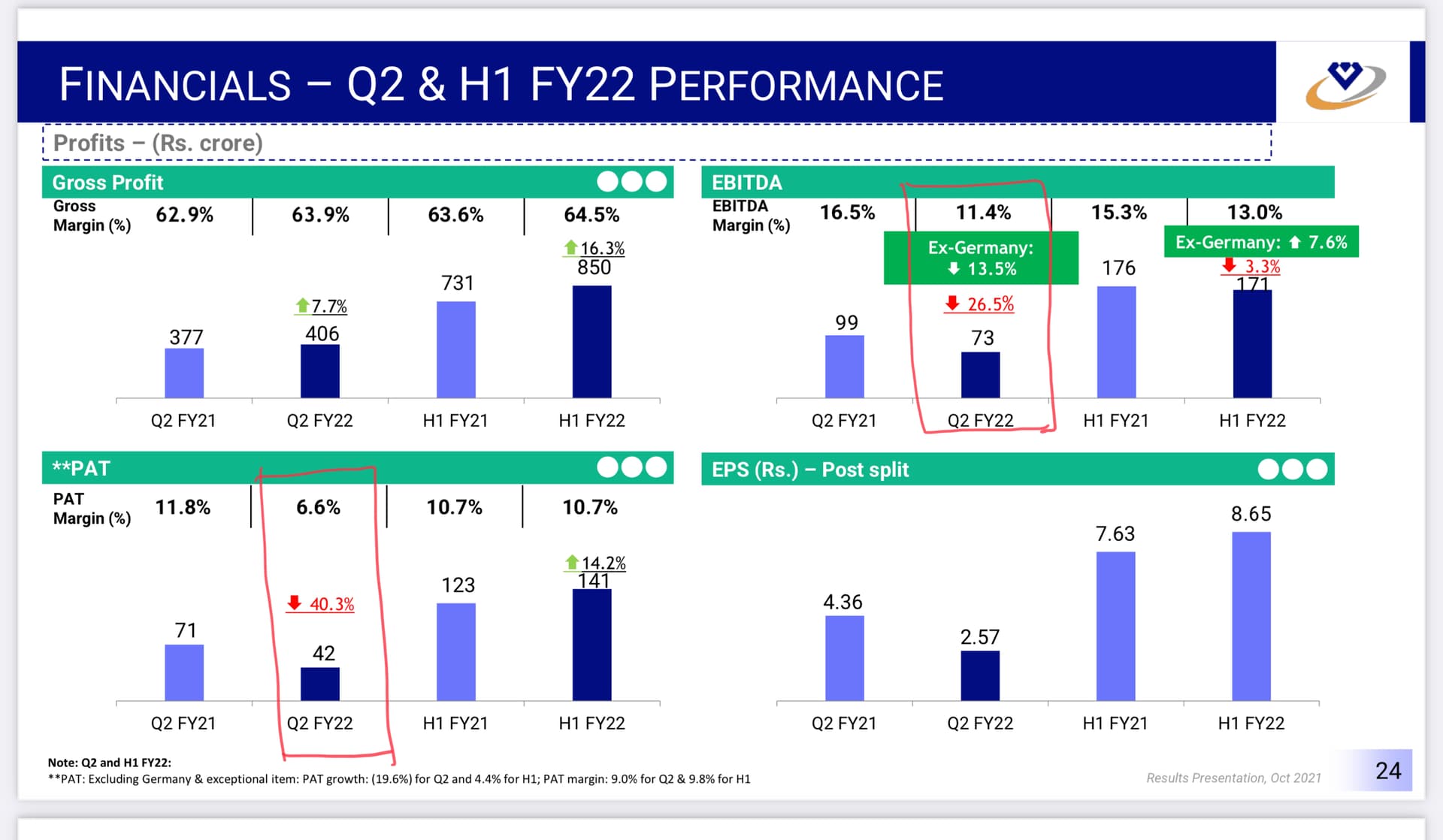

Lackluster results. I was expecting a moderation in revenue growth led by reduction in volumes and reduction in unique customers, however the quantum of it is a bit surprising. Will attend concall for more clarity

Management commentary from press release- In Q2 we have seen our revenues at Rs. 635 crore an increase of 6% Y-o-Y and over Q2 FY20 we have seen a much stronger growth of 30.9%. With the vaccination in both US and UK reaching pivotal levels, severity of threat from Covid has largely reduced. As US and UK economies have more or less fully opened, we have seen consumer behavior moving to something we call revenge outings implying substantial increased in-person shopping in brick-and-mortar stores and people going out on holidays.This has led to lower in-house shopping for home retailers like us. Retail Revenues for us, grew by 3.3% Y-o-Y. After a massive jump last year, overall E-Commerce as a percentage of retail sales has dipped in both US and UK in recent months. We believe that these headwinds are transient and are well placed to continue our growth trajectory in coming years. We are committed to our original guidance of 16-18% constant currency revenue growth for current financial year

Vaibhav Global has been exceptionally good at employing multiple growth lever over the last decade. Lets examine whether those levers can be employed over the next decade as well:

Undercutting Qurate on price to gain volume growth and market share in jewellery -

Vaibhav global now does as much sales and 2x volume as Qurate in US for jewellery while maintaining 60% gross margins. However, now the jewellery business is slowing down for VG. Volume growth in the last few years has been 5% pa. Potential for future growth is low

Geographic expansion to UK and now Germany -

In this respect, Vaibhav Global has been far more effective than Qurate. 26% of Qurate sales in the last year came from all international markets. Whereas Vaibhav global derives 31% of its sales from UK alone with potential to expand to large markets like Germany, Japan, Italy. High potential for contributing to future growth - could double sales in 7-10 years

Internet led growth -

Qurate derives 60% of its sales from the internet and 40% from TV. The numbers are reversed for Vaibhav Global. However, Qurate overall sales have been stagnant so internet has cannibalized TV. Whereas for VG, TV has grown as well albeit at a slower pace than internet. Not sure about this lever for the future

Category expansion -

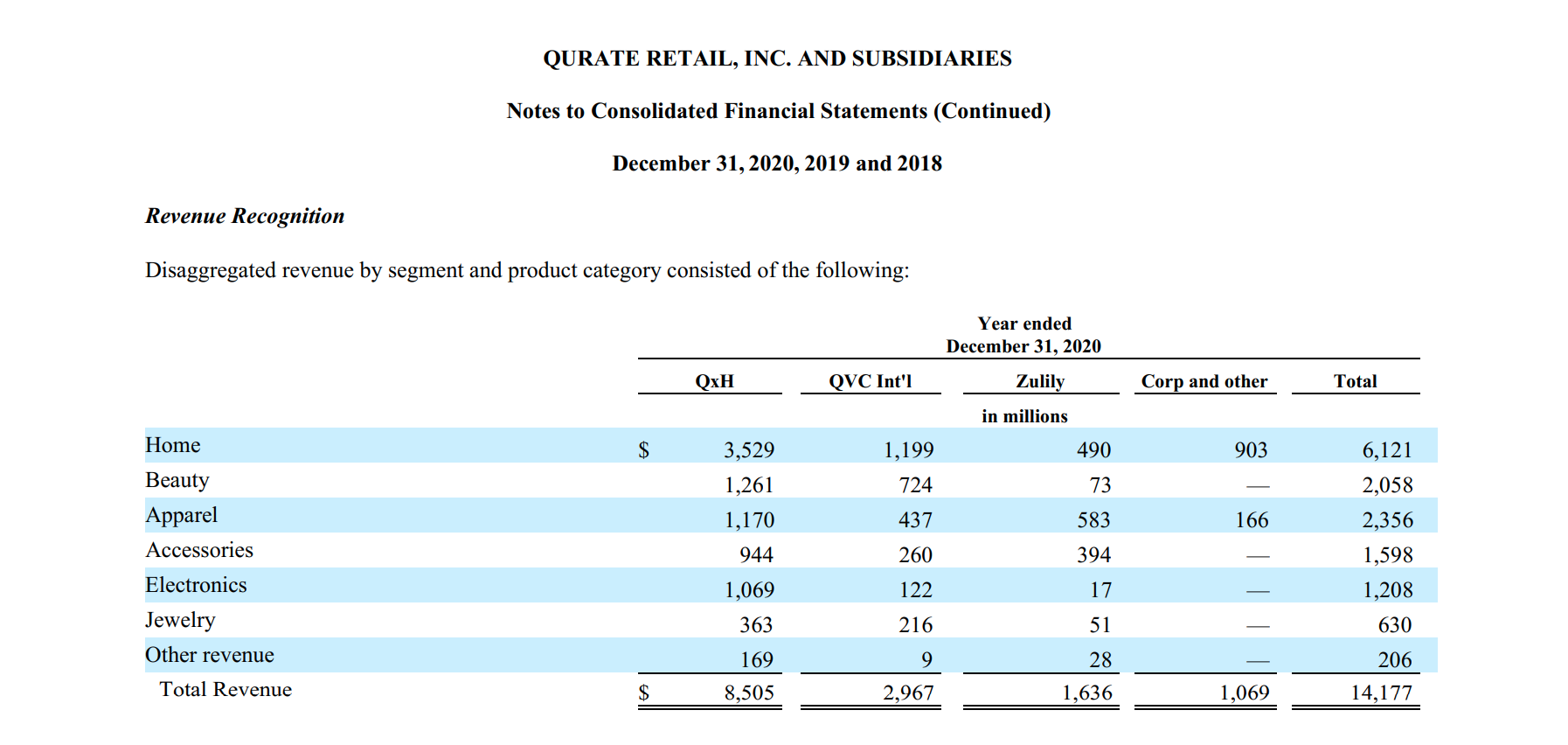

Non-jewellery sales have increased from 17% in FY17 to 31% this year. Qurate non-jewellery sales are 95% of total sales. Huge potential for category expansion still remains but the key question is can it be done in categories like home and electronics while maintaiing such high margins. High future potential for this lever but execution risks abound

ASP increase -

ASP has increased from 24 USD in FY16 to USD 30 today. Management has clearly stated that they will maintain ASP at current levels for the next few years. No help from this in fact as share of internet increases overall ASP could fall

Repeat purchases -

Average annual pieces per customer have increased from 24 in FY16 to 30 in H1FY22. Given that Qurate does average annual pieces per customer of 27 at much larger scale, I dont expect this number to increase further

VGs great advantage is the ability to clone the successes of Qurate at lower cost/with higher efficiency thereby taking market share without too much risk. It seems quite probable to me that VG does 10k cr revenue with 20% EBITDA margins in 7 to 10 years with the same playbook they used for the last 10 years. Would be happy to hear contradictory views.

please share the sources from which you concluded this. This seems incorrect to me.

If you see Qurate presentation (https://d1io3yog0oux5.cloudfront.net/_317a6dac54b46cfeb61c4c2efc26f060/qurateretail/db/880/7988/earnings_presentation/Q3_21_Slide_Deck_Draft+11-4-21.pdf) they did 3B revenue in Q3CY21. Only a small part of this is international sales.

VGL did 600 odd cr for Q2FY21. How are their sales similar?

We know that VGL ASP is half of qurate, so even volume wise they should be worlds apart. as per latest commentary & my estimate, VGL has approx 4-5% market share in US for TV+online retail versus 90% odd for qurate. Nowhere similar.

I think the correct number to look at here is e-retail (TV+online) versus brick & mortar retail. Look at a long enough time horizon and you see qurate sales are also growing. E-retail as % of overall retail is only 18% in US. The market is far from saturated. Of course it does require innovative customer acquisition to switch customer habits from offline (brick & mortar retail shopping) to online/TV retail shopping. I expect this to contribute 5% CAGR over next 10 years to sales.

I expect this to grow down as they enter markets like China + India at some point in the future.

Overall agree with your analysis 90% except the very first point on Qurate sales vs VGL sales. Their main competitive advantage is the vertical integration including incorporating customer feedback & design insights into product development & product lifecycle management. This feedback loop leads to products which are most in demand getting manufactured/sourced much higher than products which fizzle out. The main reason they are able to squeeze out 60% ROCE is because they are not scaling capex/manufacturing, they’re building & scaling brands while outsourcing manufacturing/sourcing. This reminds me of FMCG business models already executed in India.

According to me, VGL has high probability of 15-17% growth and some probability of 17-20% growth with some operating leverage. I Dont expect >25% earnings cagr over long interval of time. The post pandemic growth spurt was in part due to massive e-com tailwinds. e-com went from being 14% of all retail to 18% in a span of 1-1.5 years in US! As a result of that, for this period of time, VGL was able to grow its sales at 25% CAGR. If we see last 1-2 quarters, opening up has resulted in some of retail going back from e-retail to brick & mortar leading to headwinds for e-com players. Valuations had run ahead of fundamentals & thus some correction has been healthy here IMO. I would consider VGL to be fairly valued at current levels given (medium) future growth, high profitability.

I think you need to multiple by 70% twice to account for jewellery revenue in USA.

2500 CR revenue in fy21. 70% of that in usa. 70% of that from jewellery. This gives us 1200cr revenue for Vgl from us Jewellery in fy21. It’s about half of qurate. I would say there is still significant room to grow at 10-15% for long time.

You’re right that jewellery is a slow growing market this is also why they have guided for about 50% non jewellery 50% jewellery mix in next 3-4 years going forward. Non Jewellery growth will out pace jewellery growth.