1 Like

This news and the latest stimulus package in the US could really be a big boost for the stock as the Economy gets back on track over there the latest stimulus package could really increase consumer spending

Another step towards starting business in a new country - Germany. Awaiting more details.

Rgds

RR

1 Like

Stock split on cards.

Details:

Split Ratio : 1:5

Split of equity shares shall be decided after obtaining approval for sub-division/split from the members through postal ballot and will be intimated accordingly.

2031 Volume Targets

Very interesting goal set by VGL:

VGL is aiming to feed 1 million children per day by 2030. Currently they are feeding 53000 children per day through their 1 for 1 program wherein every time a user buys 1 item they promise to feed 1 child 1 meal. Assuming even a constant ASP, this would imply an almost 19x jump in revenues in 10 years. I don’t know how they would be able to achieve this, but would imply a 34% CAGR. If the ASP drops by 66% to 6.7$ (assuming entry into markets like India eventually, and PPP of 3 between india and US) the topline would still grow by 6.33x times resulting in 20% CAGR for topline. It would be safe to assume that VGL is planning to grow topline between 20-34% in next 10 years. We already know how much operating leverage they have looking at last many quarters of 25% topline and 50% bottomline growth. Whether they can execute well on this mission would decide whether and how much wealth would be created.

Q4FY21 Volume growth Estimation

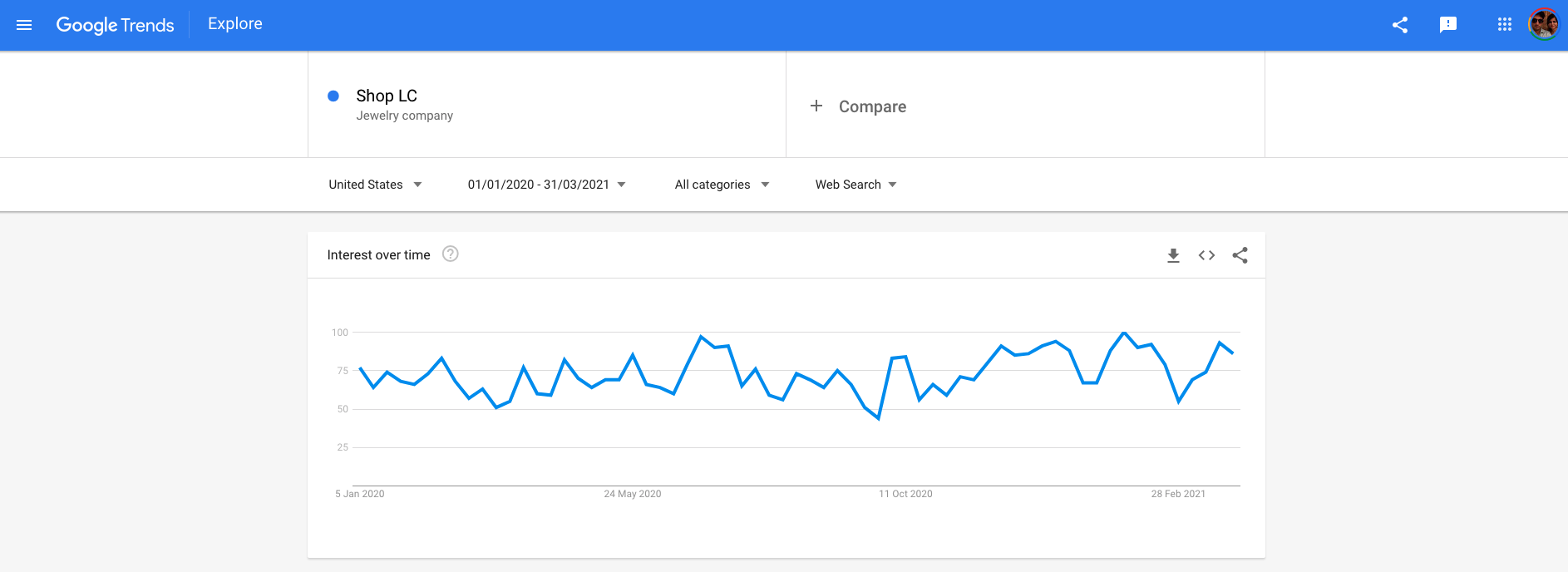

One interesting way I have found to track/estimate VGL’s upcoming quarter topline growth is to track the google trends for Shop LC. This forms majority of their revenues. Since VGL only retains about 52% of their customers, so about half of them are new customers. Many of them would be coming through Google Search. So assuming some constant search to purchase conversion, a bump in search volume should translate (to some degree) to a bump in revenues as well. Have found this to work well in the past (upto some degree of error of course).

Here is my custom Google trends query:

https://trends.google.com/trends/explore?date=2020-01-01%202021-03-31&geo=US&q=%2Fm%2F04zzd1j

Raw data can be downloaded. In Q4FY20 the interest in ShopLC was 67.3 and in Q4FY21 the interest is 81.6. This implies a rough estimated 21% topline growth YoY.

Disc: Invested. This is not an investment advice.

11 Likes

Company shares views on developments post the last results.

- Continues to see robust high growth seen in previous quarters.

- Launched/aquired 2 new channels : one in Germany and another in UK (TKC beauty).

Disc: invested. This is not investment advice

4 Likes

Has anyone received the split shares yet ? If i have sold shares on the ex-date on which price was approx Rs 4000 lower then am i eligible for split shares ? Thanks

Yes you still will be eligible for the split shares if you were holding them a day before the ex-date. So e.g if you were holding 100 shares before ex-date when price was 5000 and sold them on ex-date when price was 1000, then you will still get 400 shares. These shares would be in broker’s account who will transfer them to your demat acct. If you don’t see them in your demat acct, contact your broker.

Rgds

RR

1 Like

3cd97d07-32a8-44d3-9619-c93b07a78ae1 (1).pdf (4.9 MB)

Results are out and growth YoY continues

Pat has increased from 39cr to 56 cr YOY

Healthy top line and bottomline growth YoY

Dividend of 1.50 Rs.

Concall tmrw at 4.30 pm

Investor presentation:

3e5f2e88-d590-4593-9230-759971eacbe0.pdf (4.3 MB)

Key highlights(from investor presentation)

Robust 33% Y-o-Y growth in retail revenues (FY21 31% Y-o-Y )

EBITDA grew by a strong 41% Y-o-Y, margin expanded 70 bps to 12.8%. (FY21 40% Y-o-Y)

Further improvement in return ratios with ROCE expanded to 61%(TTM basis)

FY21 Free Cash Flows enhanced to Rs. 268 crore

Significant Y-o-Y jump of 38% in Unique Customers (TTM basis) to 501,169

Edit:

Concall details:

9511cfd8-6c59-4e55-98c5-b4c1d02e55e2 (1).pdf (414.7 KB)

1 Like

Hi…Couldn’t find the concall details. Would you be kind enough to post it here. Thanks.

One can register through below link:

https://services.choruscall.in/DiamondPassRegistration/register?confirmationNumber=2580885&linkSecurityString=8d1576eba

1 Like

Wanted to share a short summary of the company:

Core Business

Vaibhav Global is a vertically integrated company that sells fashion jewellery and lifestyle products, manufacturing them at their India and China factories and also sourcing them from over 20+ countries. Their primary business modelis to manufacture or outsource many deep discounted products, launch them as “experiments” on their several sales/marketing media (their own websites, Apps, TV channels, OTT channels (TV channel on the web), Other web platforms (Amazon, eBay). Those products which have highest demand are scaled up in production and sold in larger quantities. When production moves beyond a certain threshold, they move production in-house, thus leading to larger vertical integration. At Each product category and also overall business level, they maintain 60% gross profit margins. For this reason, they do not sell other brands’ items on their platforms. They have an interesting inventory (including returns that they cannot resell) clearing mechanism known as ‘Rising Auction’.Rising auction has a mechanism of starting everything at $1, and at whatever price it clears, it clears. Their Web business is growing much faster than the TV business. They still retain the TV business because they follow an Omnichannel sales strategy.They have also observed that the lifetime value of a customer (defined as total purchases they make over their life of being a customer at Vaibhav) is x when it is a web-only customer, 3x when it is a TV-only customer, and 9x when the customer makes purchases on web and TV platforms.

Size of opportunity

Vaibhav global works to identify trends in what customers want and then work to either outsource or manufacture those products (50% each in FY20 revenues). Understanding customers is a key part of the business model. For this reason, they do not scale mindlessly to all markets or all countries. Right now, they only operate in US and UK. In fact in an earlier avatar they did try to scale to multiple countries simultaneously, Realized it is not possible to do so, profitably, and hence scaled down (during 2008-2010) to only these 2 markets. They are open to scaling to new markets as and when the size of operations grows more and they see slowdown of growth in their key markets (US, UK.

In the US, their key competitor is QVC which has a market share of 93%. In the last 3 years, VGL has grown their market share from 1.5% to 3% (counting only television/e-commerce and not counting brick and mortar). As we can see, they have a huge runway, if they do manage to bring some of these customers over to VGL. We can see this in revenue growth as well. While VGL revenue growth has been ~11-12% in the last 3 years, QVC’s has been flat, meaning that VGL is gaining market share from QVC. VGL’s revenue per household in the US is 3$ while QVC’s revenue per household is 60$. This is another way to understand opportunity size.

Why now?

There are a few tail-winds working for Vaibhav Global. These have been sped up due to Covid19 Pandemic. To what extent they prove to be secular tailwinds, only time will tell. Latest Q4FY21 concall management has revealed that they are continuing to see elevated levels of revenue growth in the 6W of Q1FY22 even over the higher base of Q1FY21.

VGL’s unique customers per year have been growing at around 4-5% per year in the last few years. Due to Covid19, a lot of offline retail buyers migrated to online retail and thus to VGL. on a TTM basis, VGL’s unique customers were 342000 in FY19, 363000 in FY20 and 425000 in Q1-FY21 TTM and 5,00,000 in FY21.

All these tailwinds are visible in FY21 results: Revenues increased by a strong 28% year-on-year to INR 550 crores. Gross margin came in at 62.3%, even as they expanded portfolio of products to essential items. FY21 EBITDA margin expanded by 1.4% year-on-year to 15.3%. And profit after tax grew by 46% year-on-year to 344cr. Due to good growth, management has guided for 16-18% constant currency growth in US and UK geographies. Management is generally very conservative

The business model has proven to be antifragile against the covid-19 pandemic. When there were total lockdowns in China, they were able to ramp up production in India and sourcing from Thailand and other countries, and when there was a Lockdown in India, China production went up along with sourcing from Thailand.

In the latest Q4FY21 concall, company has also declared intention to expand into the Germany markets in H1FY22 and will do 2M$ capex in FY22 with opex losses in first year. This will open up an additional avenue for growth and expand the opportunity size even larger since germany is largest home shopping european market. Germany has similar competitive landscape like US and UK geographies with QVC and HVC each doing 1B$ revenues.

Financials

VGL has significant operating leverage due to relatively lower fixed costs versus variable costs. This is visible in their Sales, EBITDA and PAT CAGR in last 4 years. I take this screenshot from FY20 Annual Report for making the point:

Sales became 1.5x, EBITDA became 3.7x and PAT became 4.8x in 4 years.

Their gross margins are fairly stable at ~60%. This is a core part of the business model. They discontinue products/SKUs where gross margins are significantly below 60%. In fact in Q1FY21 they introduced some essentials on their website like masks, rice, pasta. Even in Essentials as a category, their Gross margins were 60%. Due to very high ROCEs of 61% they do not need much incremental capex. This is a very asset light business. Hence, they have very healthy Free Cash Flows and also have a stated policy of giving back 20-30% of FCF to shareholders via Dividends + BuyBacks.

Accounting

This is probably my weakest part in analysis. I could not find many red flags. A couple of observations I made is that their internal auditors are Deloitte and their Auditors are KPMG (for 5 years since 2017-18). This leads some credence to their accounting books.

Valuation

Given the growth metrics, I do think they are fairly to overvalued right now (EV/Sales and P/E). However, given the size of the opportunity, I have a decent investment in VGL. If the growth rates revert back to 17% topline 25-30% bottomline, then current valuations could potentially crash. However, for now, the valuations seem justified given the current growth trajectory.

Q4FY21 Concall Notes

- Unique customers grow 38%. Crossed 0.5M mark. Business model is integrated vertically, flexibility in the supply chain.

- Introduced adjacent product categories. Our products earn gross margins higher than largest peers.

- Will expand to the German market. Largest home shopping market in Europe. In FY22, 2M$ capex. Operating loss of 3-5M$ in germany operations in FY22. Expect it to become profitable in 3 years.

- For 2-4 years we expect 15-17% topline growth from older geographies.

- 28% growth for ShopLC and 34% growth for TJC.

- Retail revenues grew by 31%.

- TV revenues 28% growth. Web revenues 43% growth.

- TV contributes 64% and 36% from Web channels.

- Non jewellery products 31% contribution

- Operating leverage lower than before due to investments into germany. 13.1% EBITDA margins if we exclude the expenditure done for Germany expansion.

- Separate channel will be launched for beauty products. Separate channel to give us additional screen time with our customers. Will only live for 4 hours a day. We will expand the channel airtime only if we see traction.

- Germany Updates: We expect to invest 3M$ in capex. We already launched digitally. On TV side, we will launch on H1FY22. Sales revenue point, 16-18% for older geographies. We have launched in Germany already through our own website.

- We have made some investments in social commerce in last Q and will continue to do so. Do not want to dilute our operating leverage too much.

- UK we have significantly reduce delivery in UK with TJC+ it is 24 hours. It is like Amazon prime. Bottlenecks in US with covid pandemic. Aim to bring it down from 4.8 days to 3.4 days in FY22. In texas and oklahoma it is 1.5 days down from 5 days due to better logistics.

- Continuing to see elevated growth in 6 weeks of Q1 on the elevated base in Q1FY21.

- Competitive space in Germany is similar to the US and UK. 2 major players of 1B$ each QVC and HVC. Market size is at least 2B$.

- In Japan we are already showing in the local markets. We are still trying to understand the market. We don’t want to grow in Japan until Germany fully stabilizes.

- 1 for 1 (VGL’s CSR program to feed hungry children 1 meal for each purchase) run rate is 54000. meals per day We want to grow to 1M meals per day by 2031. We have to grow 22% (was a bit inaudible) YoY every year for a very long time. We take this goal with lot of courage and ambition.

- Lifestyle will be 50% of our mix in 2-3 years.

- We have experience in Germany since 2007. Have transferred a UK manager who has lived in germany to germany business. Our success probability is much higher this time around due to our success in US and UK.

- Want to bring TJC+ to US when we have our shipping under control (shipping costs and delivery time) then we will launch TJC+

- 12M$ from marketplace (Amazon etc) in FY21. We did 3.5M$ in FY20. So we have huge growth despite large competition. We expect to grow higher next year though no guidance.

- In FY21, 501k unique customers. 321k in US , 179k costumers in UK. Last year 362k total, 225k in US, 136k in UK.

- 65L opex gone for Germany in Q4FY21.

Disc: Have a large investment here. Full PF here. This is not investment advice.

22 Likes

Thank you for wonderful write ups. One more interesting thing for Vaibhav Global could be that it’s biggest competitor, QVC is highly leveraged.

2 Likes

Industry Tailwinds

One of the key tailwinds for VGL and the e-retail industry is the shift from Brick & Mortar stores to e-commerce.

Here are a couple of articles that track the acceleration of this trend post covid:

The Discount e-retailing market in USA has QVC (Qurate) as the market leader with 93% market share. In this post, I’m adding commentary by Qurate management as a proxy for how the industry can be expected to grow in medium term. For context, QVC revenues have been largely flat since 2018 (pre covid) However, they have started increasing at ~10% per annum again since Covid-19 pandemic (Source:TIKR). In a recent (20 Nov 2020) Analyst day Concall (Source:TiKR) done by Qurate (QVC), they have claimed that the increase in revenues and new customer acquisition is sustainable (I do not yet know how reliable Qurate management are and hence would request investors to not over index on the management commentary). Here are my notes regarding the e-retail business:

- [Customer Additions]: The customer response has been quite remarkable. It’s enabled us to drive outsized growth in revenue and OIBDA and free cash flow, all buoyed by these record levels of new customers we’re adding across the business. And we recognize this is a significant change in trend. And it begs the question all of you are asking, which is what do these results tell us about the long-term growth potential of our business post-pandemic.

- [Covid accelerated existing value migration]: The pandemic has largely accelerated pre-existing trends towards a more digitally driven lifestyle.

- [Qurate growth prospects]: We’re confident in our ability to drive long-term healthy growth in revenue and profits and in cash flow, and we’re committed to attractive shareholder friendly ways of returning that capital.

- [Digital lifestyle]: This digital lifestyle is here to stay, whether it’s the dramatic increase in usage of streaming services or the fact that shopping journeys are increasingly digitally driven with the physical store just being one touch point, among many other more digital interactions. And this explosion of interest recently in live stream shopping speaks to the consumer’s hunger. They have more engaging, more immersive digital experiences that can begin to replace the energy of the physical environment.

- [Adoption across generations]: . Even today’s millennial consumer, when she hits her mid-30s, is adopting our platform at about the same rate as her Gen X and baby boomer forbearers did in past years.

- [Best customers]: Look at the super users that we attract to our business. These best customers, who we define as those making 20 purchases or more a year, represent almost 70% of our sales. They visit our websites 33x, they – a month. They view our TV programming 19 days a month. And they make, on average, 69 purchases. We also know that it raises concern. There’s a fear that some have that these super users must have joined decades ago and built up this habit, and they’re going to fade away to be replaced by today’s low loyalty transactional price-driven e-commerce consumer. We retain 99% of best customers every year, year after year after year. We are bringing in new best customers at about the same rate as we have always brought them in. And far from taking years to become a best customer, new customers who become best customers typically do so in the very first year they join.

- [Quality of new customers]: Your likelihood of making a repeat purchase within 60 days is a very consistently predictive dimension of becoming a good lifetime customer. That metric is stable across classes at 22% to 23%. Of course, the ultimate measure of the quality of a new customer class is how many go on to be best customers, and you need a year to see that behavior. But let’s look at just how many new customers became best customers and then they hit that 20 purchase threshold in just their first 60 days as a customer. That metric is amazingly stable over time.

To conclude, here is a graph from statistica with past and predicted global e-retail penetration:

https://www.statista.com/statistics/534123/e-commerce-share-of-retail-sales-worldwide/

Trends are very similar in USA & UK (both key markets for VGL).

https://www.statista.com/statistics/272391/us-retail-e-commerce-sales-forecast/

Here is a report by US department of Commerce on e-retail sales in USA. The bump due to Covid-19 is fairly visible:

Latest update is that as one can see from Qurate (QVC)'s financial results, their sales growth has actually accelerated in Q1CY21 (14% YOY revenue growth).

Disc: same as before

9 Likes

Some great CSR initiatives being done by VGL here in India:

The world is fighting together against the coronavirus pandemic. Vaibhav

Global Limited, (VGL) remains focused in helping its employees, customers, and communities. In

the midst of lockdown in India, VGL donates an Oxygen Plant to 550 bed SDMH hospital in Jaipur.

With oxygen supply at a critical point, the team at VGL leveraged its supply chain to procure,

install and donate an Oxygen Generator Plant with capacity to supply 150 beds at the Santokba

Durlabhji Memorial Hospital, Jaipur, India. The entire process from ordering to installation was

completed in just 15 days. The third‐party purity testing of Oxygen Generator Plant has been

carried out with oxygen purity of above 95% and observed on‐flow rate of 30 NM/hour. This

indicates that the oxygen generated is of medical grade and can be utilized in patient care.

In addition to the Oxygen Generator Plant, the team secured and donated 110 oxygen

concentrators, 30 BiPap machines and two Ventilatorsto several local hospitals and Associations.

“Supporting our communities is very important to us at VGL. During this stressful time, we want

to bring hope to those in need by providing much needed resources. I am proud of the team for

their ability to accomplish this in such a short time.” shares Mr. Sunil Agrawal, Managing

Director, Vaibhav Global Limited.

Since March 2020, the VGL team has provided support in many different ways to both the

community and employees by developing a line of essentials, distributing masks, ration packets,

fruits and vegetables, groceries, medicines, providing online consultation, and access to

vaccinations

Taken from a BSE disclosure:

Disc: Same as before

3 Likes

whats the TAM and how much is the runway for this? I see QVC does almost 15B USD.But QVC is values at only 5,5B USD… however VGL has a vey high valuations…whats the rationale?

With Shopify and likes, can VGL continue to grow?

Doesnt free to air television marketing have a lowcost /fake kind of image among larger public ? Is ecommerce(including shop LC web portal) like Amazon/Etsy /walmart a better platform for VGL products and can they manage to grow profitably without TV?

Does it have sustainable higher 20% growth for a foreseeable future to justify its valuations?

3 Likes

E-Commerce customers on third-party portals are not VGL’s customers. they are customers of respective websites. they just buy on those platforms (Amazon. Shopify etc.) and VGL is just another vendor.

To acquire customers, VGL must focus on its own exclusive channels. Customer profiles of VGL customers are different and region-wise, customers prefer different platforms for shopping. while in the US, it is the internet, in the UK it is Television shopping networks.

I think 15-20% topline growth is possible with the right product mix.

2 Likes

I had asked a couple of questions to the management/investor relations. Pleasantly surprised to see that they answered it. I had planned to ask them in the concall but could not, but good to see that they were answered on email.

*The link was added by me.

Disc:invested, biased

9 Likes

IMHO VGL’s positives are:

^ highest quality of business one can imagine, low on fixed assets and low to moderate on WC. A very very rare species to locate.

^ massive runway ahead

^ low profile management; not much media interactions; under promise nd over deliver type

^ good dividend policy

look at Germany foray: very less capex required nd apex will be flushed in P&L. even if they dont succeed, they can simply abandon without losing much, its not like they are stuck and creates identity crisis. So, this kind of company can do a lot of experiments, if required, and CAN AFFORD TO FAIL TILL SUCCEEDS.

^consistent and predictable growth

Negatives:

^sometimes it looks too good to be true but no evidence against coy till now.

^tax payment is less, complicated, dont understand, so no comment

Analysis:

^ Fairly valued, so what, it might deserve even higher valuations considering business quality and FCF generation, may get overpriced further

^ Germany foray, if successful, then after 3-4 years, it will be in different orbit altogether and will provide confidence of moving to other markets also. If not succeeds then life does not end.

not much to lose but lot to gain kind of scenario. HEAD I DONT LOSE MUCH, TAIL I WIN A LOT.

Disc: invested from very low levels for 5 years…

4 Likes