Any idea why the results not good?

I had 2 questions on VSCL.

- Intermediates seem to be a product where great skill and complexity is not required. Then how does this company make operating margins of ~30%? It appears that company does not have to account for raw material expenses for jobwork. Is that leading to higher operating margins? In that case, would the margin reduce rather than increase when the company moves away from jobwork to manufacturing on its own?

- Why would the promoter sell 25% of his equity at a cheap price in the IPO at an early stage when the company does not need any cash for its business? An Ipo after a couple of years would have provided him with a much better price for his shares.

We have discussed the answers proposing that the promoter may be a benevolent person. Does anyone have a different take on this?

~Thanks!

1 Like

HI

Your observation on jobwork seems fairly accurate wherein the company would have to just incur the cost of conversion RM into API’s and not procure the actual materials itself which would be provided by enaltec.

On dilution of equity while main reason stated in rhp was for working capital purpose, my own sense is you would need considerable amount of capital scaling up from just an intermediary to a niche manufacturer

1 Like

True.

But on the IPO front, ~80% of the shares offered in the IPO were sold by the Promoter and only ~20% were for infusion of funds in the company. 3 crs of funds that were raised form the IPO could have been generated in the form of internal accruals by the company in 6 months.

Why bring an IPO so early and sell your shares so cheap. Unless, you did not sell that many shares and bought them back in the IPO through your friends, relatives, sub-accounts, etc.

Huge volume + Upper circuit!

Any reason?

Any negative news on VSCL? Stock has fallen close to 30% in the past month

It was trading above the valuation & correction was quite obvious

There are overwhelming sellers. I am unable to see any developement from NSE Emerge website. Anybody in the know of things, Pls share.

I spoke to Company Secretary. He catagorically informed there is no adverse developement , whatsoever , in the company that triggered the sell off. It is purely market dynamics at play. Company is peforming as per projections.

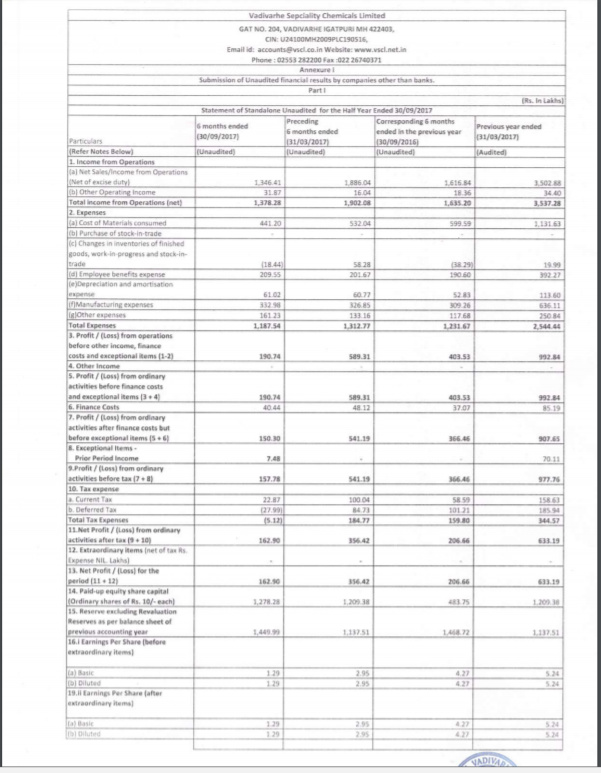

Fine Organics UK which contributed nearly 13 odd crore (nearly 35 to 40%) to VSCL turnover has been taken over by a Chinese co and as a result they have stopped buying from VSCL. So the turnover and profitability has taken a hit. Pl see the half yearly results ended Sept 2017:

1 Like

IMHO, half yearly results were published during mid Nov 17 and it was already discounted by market.

Hope there is no further adverse developement .

.

The expected growth envisaged during ipo has turned into degrowth with the loss of Fine Organic orders. Second half too will be dismal.

I never understood the great enthusiasm about this company. If I look at its products, almost all of them are commodity chemicals. The company hardly supplies anything to big names like GSK but prominently advertises them as key customers. If I look at the kind of work done by the company, it is mostly job work. It looks to me that the profit margins on job work and exports were almost the same. So, the nature of exports was closer to job work than manufacturing of specialty chemicals. The company needed to export its products to meet its export obligations created while importing machinery. If these obligations are not met, then the company will have to pay import duty on its machinery. Probably, this is why even the job work / commodity chemical was being exported.

For the type of work that the company does, it generates high profit margins, even higher than that of the pharma majors. I don’t understand the reason behind such high profit margins and whether they would be sustainable. This makes me uncomfortable. Plus, substantial Capex was required to increase the revenues above 55 crs.

Now, Capex seems like a long drawn out story.

1 Like

Quite an interesting case. It looks like the promoter knew that he was losing Fine Organics as a Customer. Considering this company only had 2 big clients (Fine Organics & Enaltec), losing one was going to be near fatal.

This is from March 13, 2017 when a Chinese buyer bought Fine Organics UK

https://cen.acs.org/articles/95/i11/Fine-Industries-sold-Chinese-buyer.html

Vadivarhe IPO in May 2017 - By this time in Q1 FY18, the company must have lost Fine Organics as a Customer. It made the most of the bull market and sold a part of the company based on 2017 financials when things were great.

Now EPS for FY18 could actually be around Rs.3 or even Rs.2.50 which means that at around 80 levels, we could be at around 30 P/E which certainly is very expensive considering all hopes hang on a single big client now. IMHO, this should get down to earth around Rs.50 levels sometime in the future when the market realises that the promoter pulled a fast one on them.

4 Likes

Someone should file a criminal case under section 420 of IPC against the the promoters, lead managers and NSE for fraud and cheating. Also should take up the matter with SEBI.

1 Like

Do we have to believe that the management want to kill themselves, by not taking an effort to add more customers.

Seriously, I don’t think we need to build up a story where there is none. If the promoter really wanted to cash out on the valuation, he wouldn’t have maintained a 74% stake with lock in and would have diluted much more.

People should deal with SME companies companies only if they are able to accept such risks. I have full confidence in the promoter and the management’s ability to diversify and get back on the growth track.

Disc - Invested from lower levels and continue to add during corrections.

1 Like

They may very well add one more, two more or many more but what we are dealing with here in the present is that the promoter knew that they had lost a key Customer but deluded the market. Also, to know how bad dependency on one or clients can end up, take a look at RS Software when it lost Visa as a client in 2014.

The lock-in period for promoter shares is a requirement of listing and it is only for 20% of shares held by promoter post-listing if I am not mistaken. Also, selling more than 25% would have raised eyebrows as the company had no real need for cash more than that and wouldn’t have been able to justify it. In retrospect, the relatively cheap IPO valuation makes a bit of sense now.

2 Likes

Fine Organics assured about future supply, expect from Jun-18 onwards

Still promoter holding is 74%

Good to know. What is the source of this info?