Vadivarhe ( VSCL) was incorporated in 2009, is a globally active, Indian chemical producer, focused on organic chemicals and custom synthesis and primarily engaged in manufacturing of Specialty chemicals, Active Pharmaceutical ingredients, intermediate and personal care ingredients. VSCL is also ISO 9001:2015 certified company by Quality Systems Zurich and has also received WHO- GMP Certificate for their Manufacturing, Marketing & Supply of Active Pharma Ingredients i.e. API’s and intermediates. The manufacturing facility is located at Vadivarhe, Nashik which is about 20 Km from Nashik towards Mumbai and around 150 Km from Mumbai.

Fem Care Pharma Ltd was promoted by Mr. Sunil Haripant Pophale which was later taken over by Dabur India Ltd in the year 2009. Mr. Sunil Haripant Pophale sold his stake in Fem Care Pharma Ltd to Dabur India Ltd and as per the terms and condition of the Division Transfer Agreement dated May 07, 2009 the Speciality chemical division of Fem Care Pharma Limited was transferred to Vadivarhe Speciality Chemicals Limited. The IPO of Fem Care was at Rs.40/- in the year 1996 and the sale to Dabur was done at Rs.800/- per share.

Some of VSCL’s major clients are Glaxo Smithkline Pharmaceuticals Ltd, Fine Organics Ltd UK, Chem-Impex International INC, D C Fine Chemicals, USV Ltd, Lupin Ltd, Mankind Pharma Limited, Himedia Laboratories Pvt. Ltd., Hetero Labs Ltd & many others in the Domestic and International sector.

Shares of VSCL will be listed on NSE EMEGE platform on 2nd June after its successful IPO at Rs. 42/- which closed on 25th May and was oversubscribed by 40 times. The issue was for 34,44,000 shares out of which 27,55,000 shares was an offer for sale by the promoters. Post issue, the Equity capital will be Rs. 12.78 Crs and the promoters shareholding post issue would be 74%

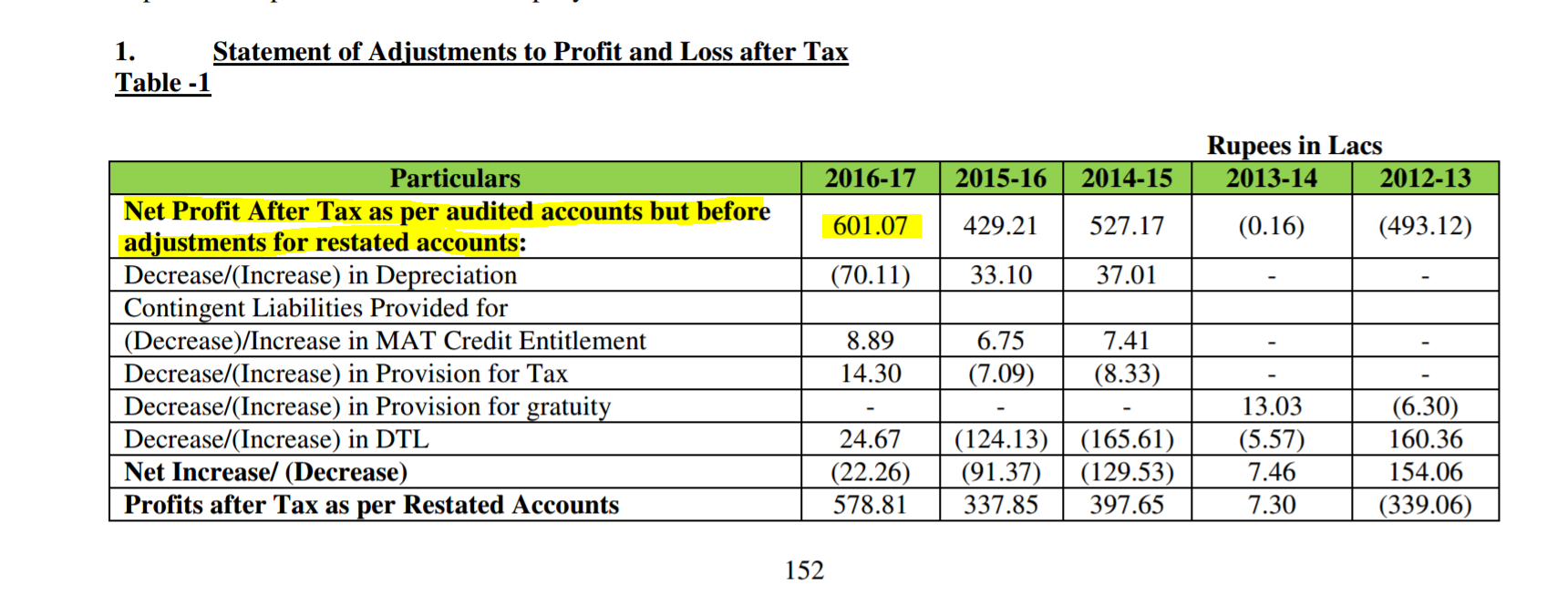

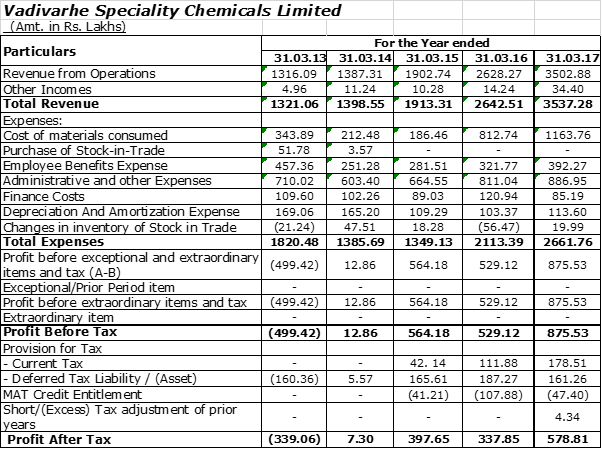

For FY 17 VSCL has reported profit after tax of Rs.601 lakh which works out to an EPS of Rs. 4.70 on the expanded equity. The Return on Equity was a healthy 24.43% For FY 18 the company is confident to increase its turnover from Rs.35 crs to Rs.51 crs and have a PBT of Rs.14 crs and PAT of Rs.10 crs. The vision is to achieve a turnover of Rs.100 crs by 2021.

Present plant capacity is sufficient to support a turnover of around Rs.60 crores. With additional capex of Rs.5 crs additional capacity to achieve Rs.20 crs turnover is possible.

Looking at the growth prospects and March 18 eps of Rs. 7.75 and with companies in this sector commanding PEs between 20 times to 30 times earnings we have a potential multibagger over next 2-3 years.

Link of Prospectus: https://www.nseindia.com/emerge/corporates/content/VSCL_PROSP.pdf

Today Specialty chemical companies are trading at PE multiple of pharma company of 2014 and pharma companies are trading at PE multiple of chemical companies of 2014.

I was involved in a conversation with a I-banker in the Oct/ Nov 2016 where he had come representing a company for sale. I checked the location, financial numbers, history with Dabur as well as Mr. Pophale’s profile and it all falls in place. Then, the I-banker said the owner wanted to leave the manufacturing business and focus on other interests.

I’m not sure if Mr. Pophale/ the promoters have changed their mind about continuing the business, but I think they will spend time in the future scouting for a seller rather than actually investing time in the business. This business should be valued, at best, at its resale value before the current bull market in specialty chemicals ends.

RONW of 24%,OPM of 20 odd % n NPM of high teens,low PE & DE under an IITian Technocrat promoter of good track record makes this a interesting stock.Opp size seems good.

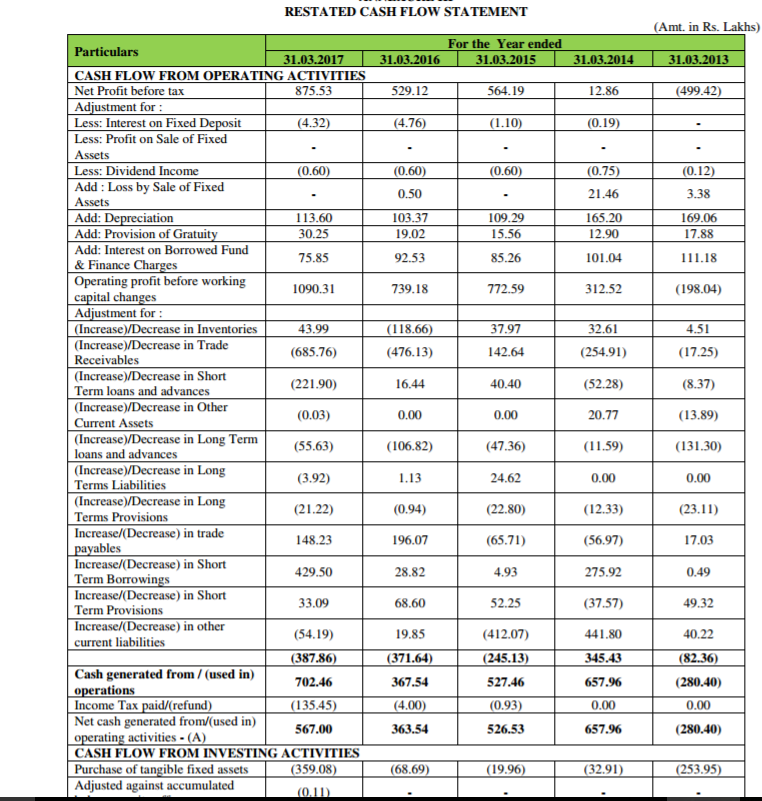

What happened in FY2015 that turnover jumped 600 lakhs on the same cost base? The inventories don’t seem out of place either?

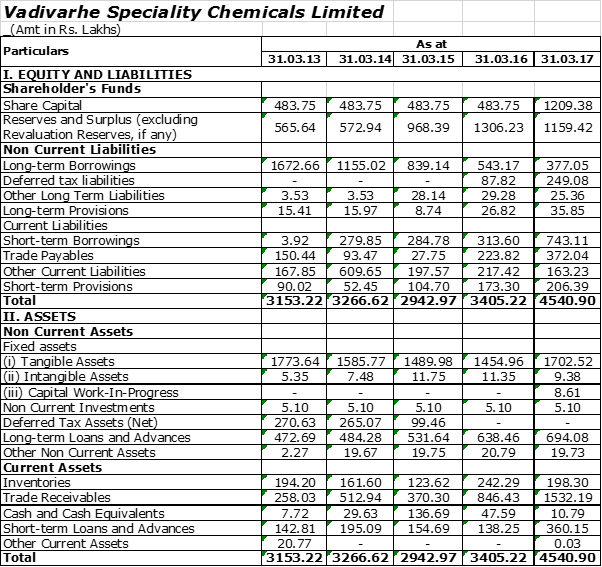

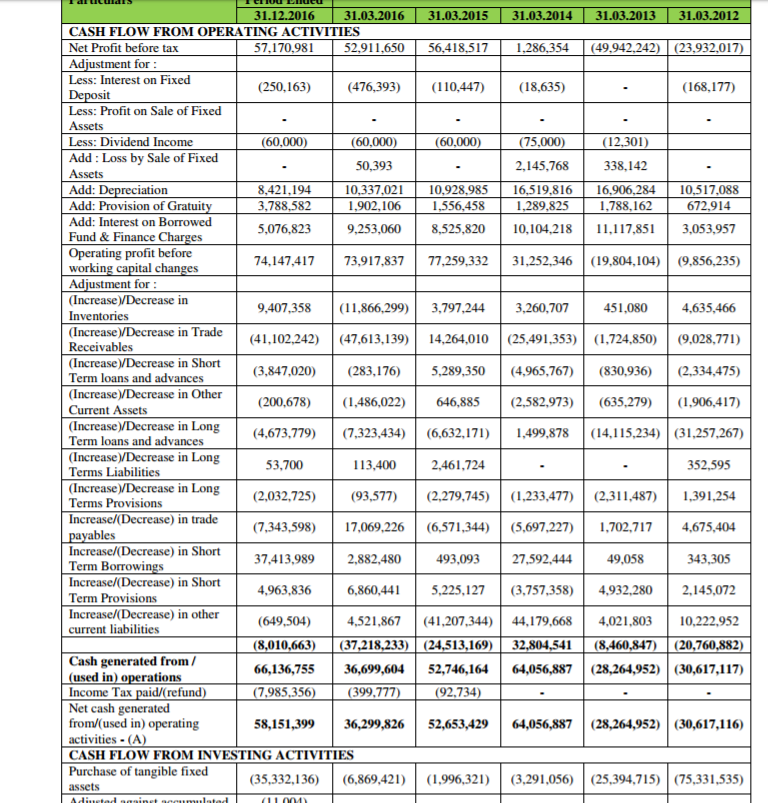

Also, from FY13 to FY17, the Company repaid 1300 lakhs of borrowings on a book profit of 1480 lakhs, but at the same time receivables swell 1300 lakhs too. Do we have cash flow statements to analyse sources of cash?

It is a “H.O.S.” - this was a discussion in a whatsapp group I was part of yesterday by someone based in Kolkata and who claims to know the person. Needless to state this is heresay, however pertinent to put on the board since the assumption that the “High quality Mega Investor” is invested may be flawed and should be verified by anyone who considers this an important aspect.

Seems VSCL MD came on CNBC today. Can anyone provide the link to the interview or what was he saying?

CNBC confirmed that famous ramesh s Damani has bought nearly 3 lacs of VSCL.

Hope VPers who track this thread would have made good money as today again its locked at UC at 95.7 with 6 lacs buyers pending.

Valn still ok imho on FY 19 basis( cud touch 10 EPS) as base is small,investment phase over & now returns should come. PE cud increase as growth would be in range of 25-30%,ethical promoter,debt reduction,marquee investors investing,mktcap vs opp size low.