@sanpat,

Hi,

I spoke to ICICI DIRECT call center yesterday. Due to SME segment, they don’t allow trading as per their compliance guidelines during Market hours but order can be placed by calling their call center before 9 am… found respondent less knowledgeable but surely transaction cannot be done. They don’t have Stock code as well.

Thanks for the update Vivek…looks like the real Damani did pick up 99,000 shares…

The growth from here on seems to be slowing down…the sales were increasing @35%CAGR from 2014-2017 …mainly due to addition in capacities about 35% every year from now on they will be adding capacities @15% EVERY YEAR TILL 2021.

Still if they will be able to increase their exports and market their product they can still grow @35% CAGR which is way above then industry average.

1 Like

Could you please elaborate as to how you are calculating that the capacity has been increasing by 35% from 2014-17? Moreover, the capacity increase has been mainly due to increase in capacity utilization. That means even if exports improve, the maximum the revenues can increase is 10-11% by 2019-20.

My apologies for the mistake, the production was getting increased by 35% but not the capacities.Thanks @mrialayush for pointing it out.

But as far are as exports are concerned they seems to be focused on increasing its share in total revenue and moreover they also wants to reduce their dependence on their top 5 clients .

As you can see the growth in export no.s has been fairly strong in the past and expansion is no problem for them even with capex of Rs.5cr they can generate revenues of about 20cr which can help them in in increasing revenues as stated in initial post by Manoj Agarwal.

So, even if we say that the goal of the management is to increase their turnover from present 35cr to 100cr in coming years it still seems to be realistic.

Hi

I had some questions.

Why is the company coming with ipo

why should the money gathered by ipo needed for working capital. I thought the cash flow was good

What was the reason for loss in 2013

What was the reason of astounding results in 2015

Profit is a little erratic. Why

Why was this segment of fem not growing that rapidly when part of fem

What products does the company have

Why was the ipo so under priced in this bull market of speciality chemicals

Thanks

VSCL started from scratch after selling out cosmettic business to dabur & co went thru investment phase for first few years. Sarting as contract manfr of Enaltech a co founded by ex Glenmark professionals n funded from abroad they acquired more clients & Enaltech is only 30% of business & will further reduce in coming years.

Some SME IPOs are priced cheaply as promoter at times owns 75% & is ethical n generous enough to leave something on table for other investors. This happened in case of VSCL,Focus Lighting,MRSS etc. we need to find such co & then bet big on them.

Promoter is ethical with good reputation & opp size for pharma & agrochem increasing. exports too rising.Margins are really good at 30%.RONW & CAGR too good. Mktcap vs opp size is good.

Risk is of client conc ,high receivables & small size of co,SME Listing which leads to low liquidity n price sway.

7 Likes

Vscl ckt now open. Story remains intact. Aries stock trade a co of Saurabh jain had again bought at 116 in bulk deal a few days back.Anyone having any idea about this co n their promoter & their track record?

1 Like

Hi Vivek

Thanks for the find - I have entered VSCL at 110 arnd 15 days ago - purely based on promoter’s track record and also the fact that you and some other veterans are positive on it. I did try to find about Aries Stock trade. I found something from Saurabh Jain’s linkedin profile which lists him as Director of Astute Investment which is the erstwhile Aries Stock Broking

http://astuteinvestment.in/#about

Looking to average up on VSCL depending on how things pan out

1 Like

Key takeaways of my conversation with mgmt :-

-

VSCL have major turnover by manufacturing loan license product (Job work) but from last 2 to 3 years focusing on developing new products, new customers. New customers were developed in last 2 years which resulted in increasing turnover & profits also. Company has now focusing on development of new products to increase sales & for the same company has also appointed higly qualified & experienced peoples in R&D.

-

Regarding Capacity- To increase capacity company will install higher capacity reactors & equipment & also will do job work in other companies

-

Earlier company has focused only on job work manufacturing after separation from fem care pharma ltd. Now from last 2 to 3 years, focusing on marketing, new produts range,etc. In last 2 to 3 years new customers were joined. Also, new customers development is in process for new products & MOU have been signed.

-

Regarding the rumors of selling the business

He said there were no such mindsets. Also, promoter has kept his shares lockin for 3years.

5 Likes

UPDATE - Updated my comments on borrowing and cashflow from financing.

Few quick observations from IPO prospectus

-

Sharp increase in receivables but not inventories

-

Without an equivalent jump in sales

-

Resulting in increase in days sales outstanding from 70 to 160 which is way over my comfort limit.

-

Perhaps the only bright point is company is paying down the debt but not making capex.

- There is no increase in fixed assets (plant and machinery)

In fact the only capex company has done is solar power and water heater. A small comany should invest in revenue generating capex not cost saving capex like a solar power. I couldn’t even find how much money they spent on energy cost to justify spending 3 cr on a solar heater.

- There is an advance to related to party of 2.5 cr.

Which may be another venture of the promoter

these are just quick notes. I didn’t even dig deeper as these are major warning signs that I will not consider this as an investment.

18 Likes

Concerns on debtors and related party are addressed in above snapshot:

The increase in receivables and not inventory maybe perhaps partly explained by the nature of jobwork sales provided to their key customer Enaltec which probably explains their lumpy nature of business. (Additionally, there are no debtors from business which exceeds > 6 months as per the AR)

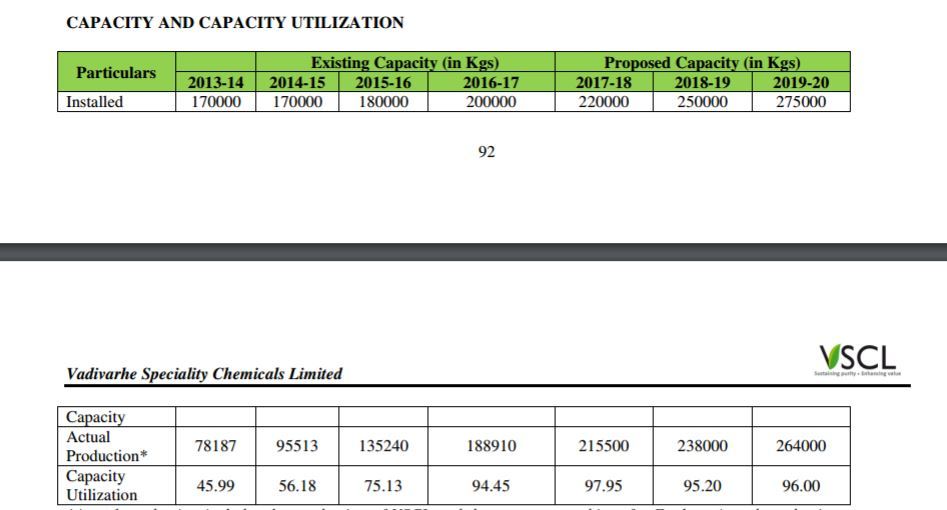

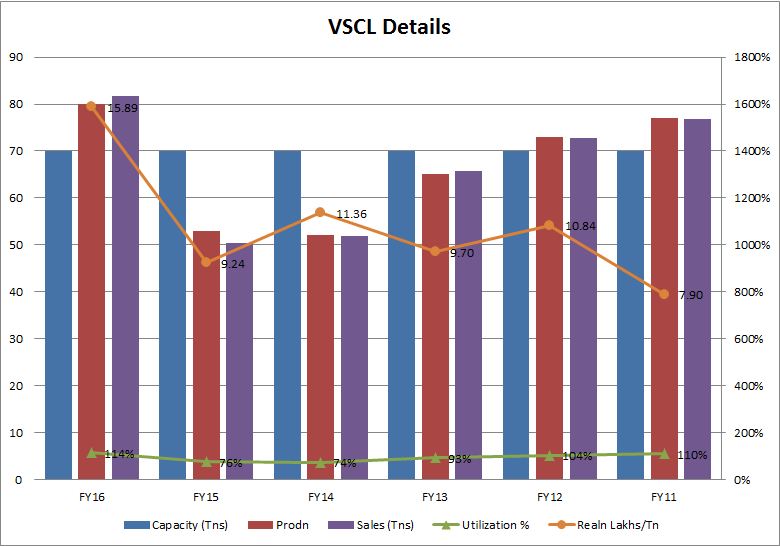

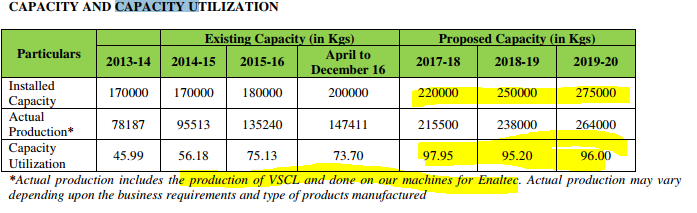

Attaching the production details and utilization details from their past AR:

Except for 2011 and 2016, they have never utilized their idle capacities for production (partly explained by the realization data shared which has been quite volatile in the past! partly due to crude movements). So in all practical sense there was really no necessity for expansion of plants;

Now on Cost saving capex surely we would agree that cost-saved equals to EBITDA gained (consequently EPS ![]() )

)

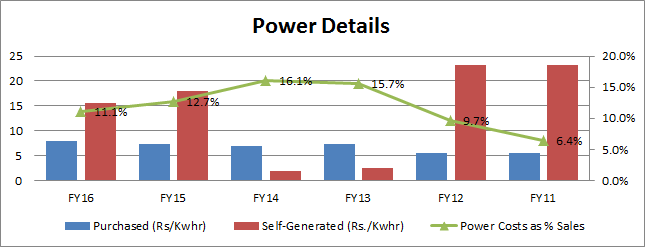

When your Power costs varies from 6-16% of sales it makes more sense to ensure a steady and low cost source of power which becomes all the more essential for a specialty chemical company. The costs invested in solar power could be partly offset by the tax benefits gained so I would really not be concerned on the cost front.

Also:

Given their largely job-work/contract manufacturing nature of work, my view is that they really do not require much capex addition (ie revenue generating) as they have ample of idle capacities.

While I agree it is essential to be cautious on our hard earned money and investments, we should also have a holistic view on the business.

My own sense on the promoters is that they do have a reputation in this industry: they have sold their earlier Fem Care Pharma to Dabur (Indian FMCG giant). So some credibility should be attached (again not saying one should put a blind faith on them!).

http://www.business-standard.com/article/companies/dabur-buys-72-15-in-fem-care-108112201045_1.html

Regards

Sreekanth

Disclosure: Invested during IPO, exited recently after run-up. These are purely my investment strategies and not a general recommendation of buy or sell. Please do your research before investing.

9 Likes

Guys,

The stock suddenly started rallying in the last three days. I have been scouring the internet to find out what triggered this. Does anybody know whats causing this?

Annual report 2016-17

http://www.vscl.net.in/uploads/pdf/VSCL%20Annual%20Report%202016-2017.pdf

Who all own & track this high margin,co strong in its niche promoted by a technocrat IITian first gen entrepreneur ? When are its results due?

Is there any provison that SME company have to announce the results Halfyearly?

Result is due tomorrow.

Smart and informed money seems to have left this company driving the stock price down!!!

1 Like