These are businesses to be held for years for story to play out.

But Covid has brought structural changes which is likely to unfold over next few years - Home consumption, home delivery, some retailers allowed to sell alcohol like west, government’s recognition of sector as important revenue generator.

Current environment when there is such quick sector/stock rotation, on needs to be prepared for periodic drawdowns based on slightest mismatch with streets expectations.

To add in above points-

I think the major reason of current drawdown is due to excise cycle. People are expecting more taxes on liquors.

second point, I feel, is degrowth in WB and AP. And reason for low volume in west bengal is increase in excise.

Have mixed thoughts on this point. A low margin today compared to the leader is an opportunity to improve and positively suprise in long term. Also, I see net profit margin of US around 9% back in 2019 and currently around 5%…anyone tracking this business since long, what should be a realistic long term profit margin for a business such as US? This brings me to a important point I wanted to dig deeper… what’s the margin difference when US sells it’s own Indian premium brand vs the Scotch it imports from its parent? Does it make reasonable cut in selling for its parent brands or the parent enjoys the benefits leaving very little on table for US? Thanks

Pernod Ricard generated a net profit of Rs.1612 crore on a gross revenue of Rs.21424 crore for FY20.

United Spirits had a net revenue of Rs.9325 crore while a gross revenue of Rs.28823 crore, implying excise of ~67%.

Putting the same excise on Pernod Ricard gives their net revenue at ~7k crore -> PAT margins are more than 20% whereas the same are around 7% for USL for FY20.

Shows huge opportunity to improve margins. Although Pernod has higher contribution from premium brands than USL.

It’s (prestige and above part of Indian whisky market) also the one where you have the best margins, versus the lower end where we’ve never been present and have no intention to be.

I’d only welcome other industry players investing in that segment. There is huge potential to increase demand in that segment”

Pernod, just like USL, has many global brands like its scotch range etc selling in India. How does the margins for imported brands of Pernod compares to USL?

The long term strength of these two companies lies in their parentage and global brands. It is very important to know if USL makes decent profits in introducing new brands of their parent or would make more if they create India specific Prestige brands?

• Off-trade channel completely operational now. On-trade channel (pubs, restaurants, bars) 85% operational but with low occupancy.

• P&A (Prestige and above) category doing much better than the popular category [Company’s focus area is P&A]. Excluding Andhra Pradesh, P&A sales grew by 4.5%. This is very positive for the company.

• Company (and industry) facing few challenges with surrogate advertisement in a couple of states

• UP has been one of the most progressive states in terms of regulations. Company on the anvil of a huge breakthrough in Delhi where the legal drinking age is coming down ( and also reducing the number of govt stores and increasing pvt stores, simplifying the rates and also making label registrations more transparent)

• Home Delivery will be a huge inflection point for the industry – specially the premium category liquor. Home delivery will also help the company because the population will shift from beer to premium liquor (behavioural change). Home delivery will also remove the accessibility barrier

• West Bengal has imposed high taxes on all segments. Business is suffering in the state.

• Red-Label is doing remarkably well. BIO (Bottled-in-origin) is doing really well as a category

• Travelling is restricted and it will come down in the future as compared to previous levels. This means the high end liquor (which people bought from duty-free) shops and foreign shops will suffer.

• Andhra Pradesh impact will be out to a large extent in Q4

• RCB profits about 100 crores per season. Largely depends on how well the team is performing in the league.

While the net sales per case is 2x for Prestige, the Gross profit per case is 4x and EBIT per case becomes almost 10x.

Thus, in my estimate, currently the popular segment contributes <10% of profits for UNSP despite making 30% of sales and 50% of volumes.

Given volumes are split evenly, one can safely assume that ~35% of the current capital deployed sits in the popular business translating into a poor ROCE of 8%.

UNSP’s Prestige business makes a health pre tax ROCE of 46% which is very healthy although still below Pernod Ricard.

Divesting the popular business will thus release 40% of the capital which currently does not add any value (assuming 10% is the cost of capital)

Hence the popular business being divested will be a major ROCE and FCF booster for UNSP – no wonder the mgmt. wants to do it.

In my view, the EPS impact of this will be ‘nil’ due to the following reasons

Currently UNSP makes Rs1650mn franchise income on 50mn franchised volumes (Rs33 per case). Thus they will likely make Rs1350mn if the franchise the current 40mn cases which will offset the outgoing EBIT contribution of Rs980mn.

Lets assume the sell the business @10xEV/EBIT versus 30x at which UNSP currently trades. That should generate cash proceeds of Rs10bn which will bring in annual interest of Rs800mn again almost the outgoing EBIT contribution of Rs980mn.

Although I think they will do a mix of the above two.

Thus given negligible earnings risk from divestiture/ franchising of the remaining popular business and substantially better utilization of resources (both capital and mgmt. bandwidth), stock can definitely hold multiples if not further re-rate.

Not too hard to triangulate. Net sales per case is 2x a fact known from the company (its reported). We have known from mgmt over the years that P&A gross margin tends to be ~50%+ (Pernod does that much and is a pure P&A co). UNSP overall GM is around 45%, so popular implied should be around 30%. All spirits use the same RM - ENA and glass. While P&A uses better quality RM, the RM cost is not double of popular as is the case for the net sales per case. That gives you 4x GP math.

On opex per case, even if you assume P&A is higher by 2.5x due to higher investments in trade channel and A&P spends, EBITDA is about 6x and then assuming same dep per case, you get EBIT per case of 7-8x.

Good analysis Rohit. I just scratched the surface and prime facie it does look like that further PE de-rating is unlikely looking at the business potential, substantial mkt share, strong parentage, possible creeping acquisition by Diageo. The question does remain about the strength of recovery, which could track 20% cagr given the low base.

Can you pls elaborate on this? It is already acquired by Diageo and is infact Diageo India with Diageo having majority 50% plus shareholding and it’s promoters

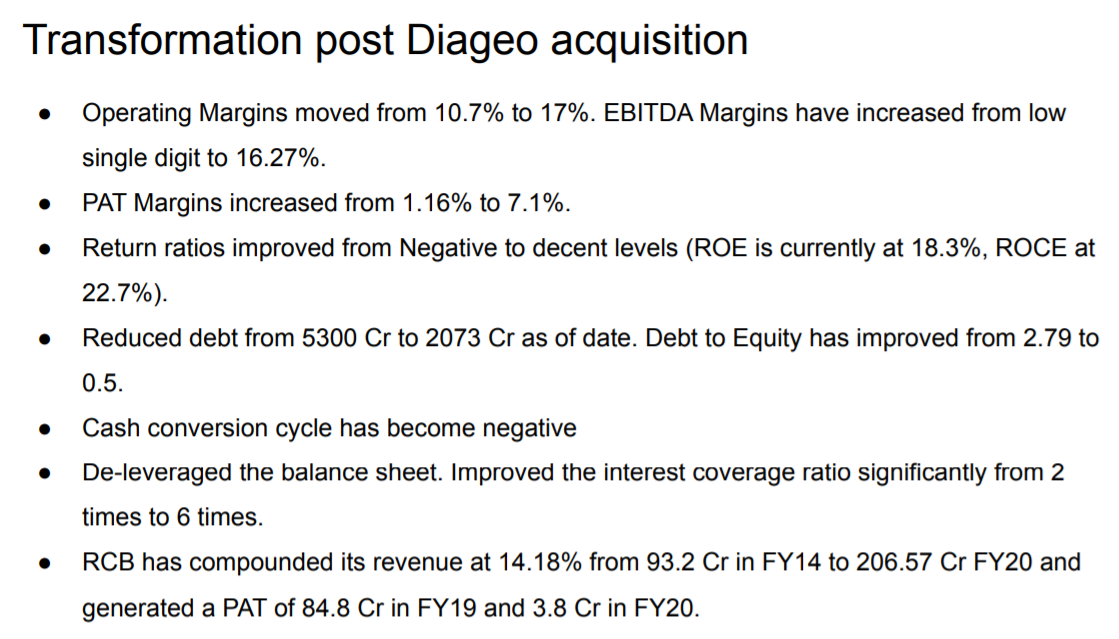

Debt has been reduced considerably and there is a possiblity that US will start paying dividends.

See slides below from PPFAS presentation on Alcohol-Bev Industry.