Was surprised to see that one of most well-known company does not have a thread and thought to create a thread for the same. However, going through researching this script has been one of complex experiences though exciting.

So, let us start from the start. United Spirits Limited, abbreviated to USL, is an Indian alcoholic beverages company, and the world’s second-largest spirits company by volume. It is a subsidiary of Diageo PLC.

Background:

The company originated as a trading company called McDowell and Company (also known as McDowell & Co, McDowell or McDowell’s), founded in India in 1826 by Angus McDowell, a Scot.

In 1959, Mallya established the company’s first distillery at Cherthala. McDowell’s began bottling Bisquit Brandy and Dorville French Brandy, from imported, becoming the first company to manufacture Indian Made Foreign Liquor(IMFL). The company opened India’s first distillation plant to manufacture extra neutral alcohol (ENA) at Cherthala in 1961.

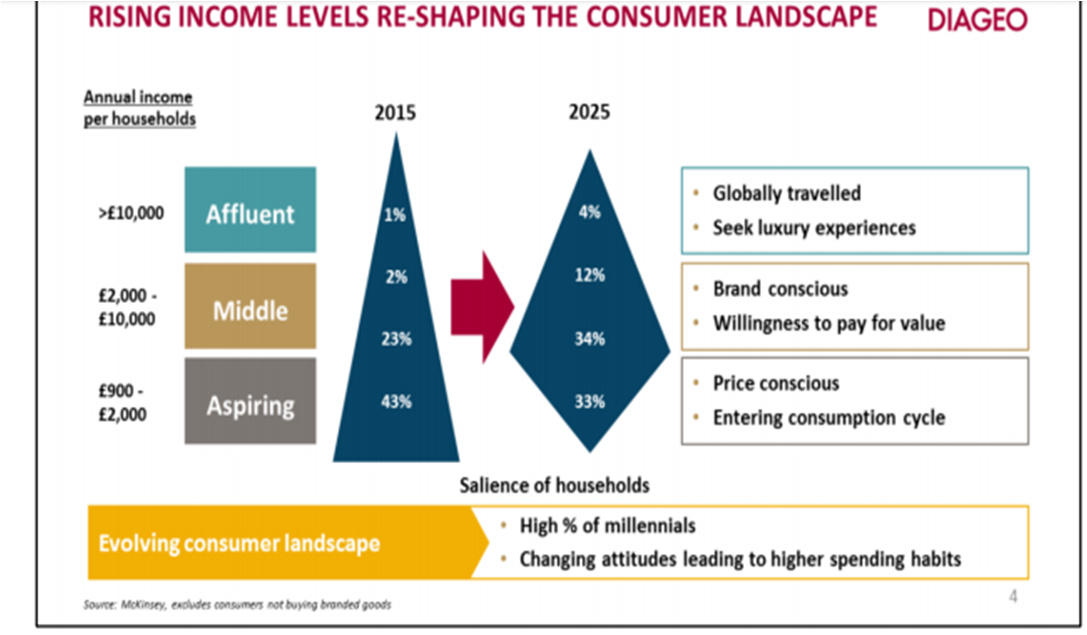

Fast forward to 2013, On 27 May 2013, Diageo PLC acquired a 10% stake in United Spirits at a cost of ₹20,927,196,000 (US$300 million). It also separately acquired an additional 58,668 shares for ₹ 85,778,082. On 4 July 2013, Diageo bought an additional 14.98% of the company for ₹31.35 billion (US$450 million). Diageo acquired an additional 21.77 million shares at a cost of ₹1,440 (US$21) per share in an off-market-deal from United Spirits’ promoters, raising its holdings to 25.02 per cent of the company. Following that purchase, Diageo held 36.3 million shares in USL, acquired at a cost of ₹52,358.5 million (US$760 million), making it the largest shareholder. Under pressure from Diageo, some substantial changes to the management structure of the firm began to take place in 2013. In 2014, Diageo’s share holdings rose to 54.8% of USL.

There are many informative articles how the overall story unfolded and one can read:

Even though Mallya is out and Diageo PLC is done lot of clean up, still, there are some old wounds which continue to haunt USL and present in various annual reports and we will discuss further. However, below links can give a feel of kinds of tussle which went even post Diageo PLC taking over control.

Current Business and Product Portfolio

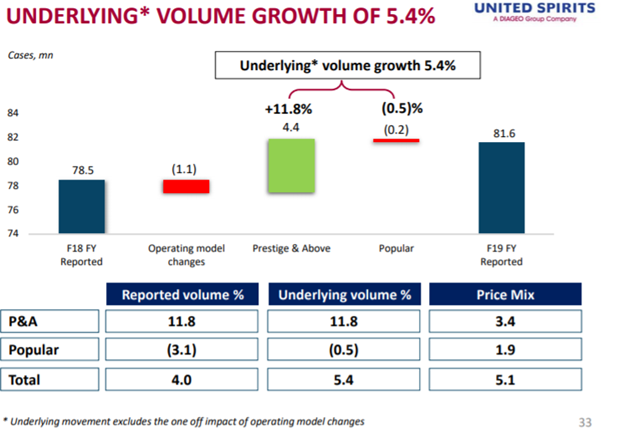

Company has 80 brands of scotch, whisky, IMFL whisky, brandy, rum, vodka, gin and wine. In FY 19 company sold over 81.6 million cases, second highest in the world. Company works through 19 manufacturing facilities spread across India.

The Transition from 2013 till now:

Now, let us see, what Diageo PLC has done in last 5-6 years post take over though it is evident from above links that lot of time went in fixing corporate structure itself to create the basic foundation to start any kind of financial and operational clean up

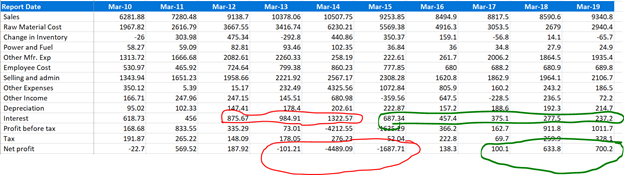

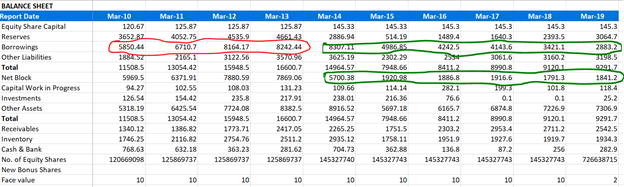

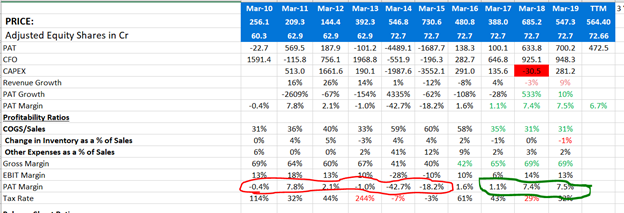

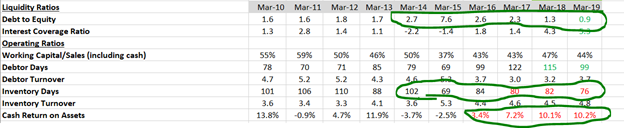

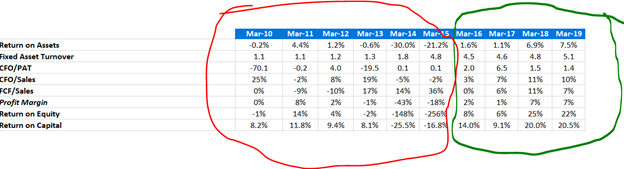

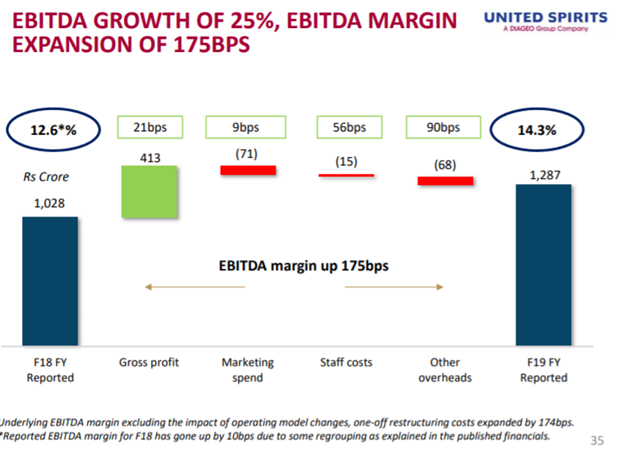

As it is evident from above tables that new management has been able to do the herculean task of bringing house in order from one of the worst-case scenarios to a respectable state by fixing balance sheet, cash flows as well as profitability. This has been achieved by:

- Overall organization level clean up by getting a new leadership team

- Fixing balance sheet by getting rid of non-core assets

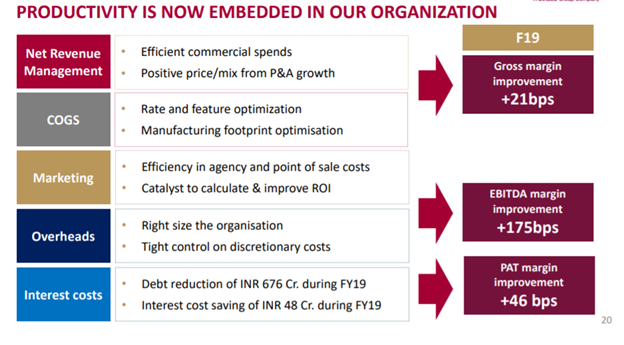

- Controlling operations and supply chain by improving efficiencies and improving margin

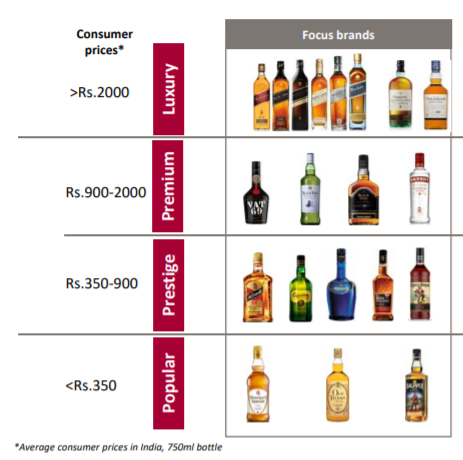

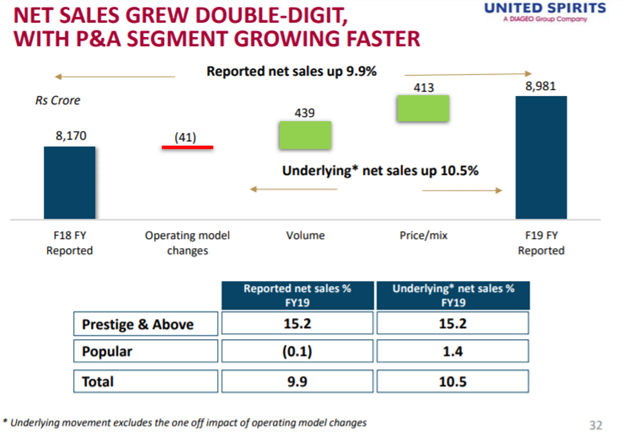

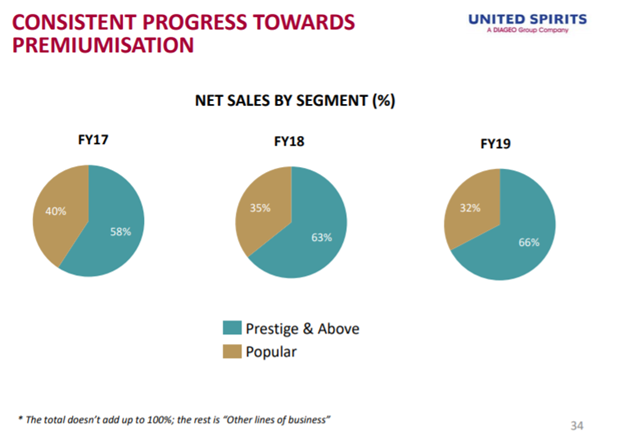

- Deep focus on premiumization and improving share of premium segment from 53% of revenue to 66% of revenue in last 3 years through both double-digit volume as well as value growth rate and hence bringing profitability back on track

- Improving route to customer strategy across states considering regulatory constraints

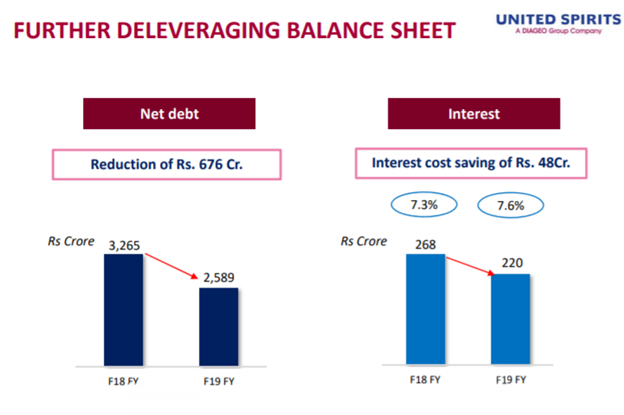

- Leveraging improving profitability to strengthen balance sheet by improving credit rating and reducing interest cost further and deleveraging debt further

- Strengthening and investing in core brands and marketing

- Bringing best practices from parent company like technology and data driven marketing and business planning through salesforce automation, MDM and advance analytics

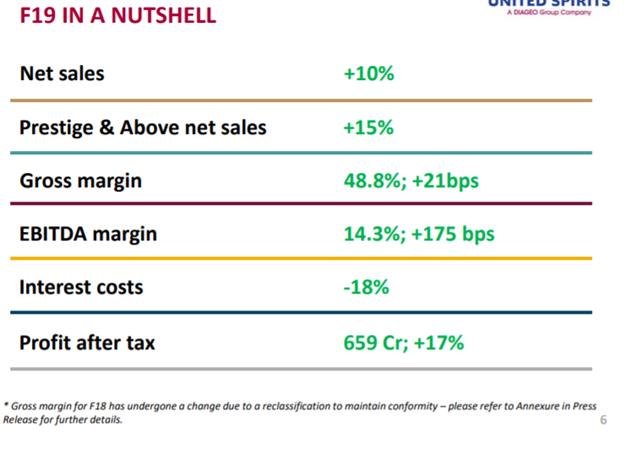

How has company performed recently:

Opportunity:

-

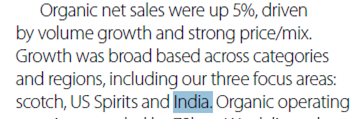

Urbanization, Growth in per capita income and young population would provide enough scope for growth

-

Premiumization is phenomenon playing out and should benefit companies like USL

-

Very low chances of disruption

Risks:

-

Highly regulated business with many regulatory issues occurring every 2-3 years like election driven state mandates, highway ban on liquor, non-ending tax hikes, price controls, state level complexities etc.

-

Raw material price fluctuation of ENA making gross margins cyclic to some extent (depending on pricing power of brand and products)

-

Raw material price fluctuation in terms of glass prices for bottling

-

Highly working capital-intensive business with working capital to sales ratio around 40%

-

Legacy legal issues related with banks and state governments

-

Non-core legacy investments like IPL Bangalore

Sources:

- Google Search

- Annual Reports

- Company Presentation

- Screener.in

- Wikipedia

Disc: Hold a tracking position. Please do your own research. This is not a recommendation by any means

Note: There is much more to cover in terms of industry analysis, financial analysis and legacy and financial issues and will cover slowly in next set of posts. This is just a start.