It’s bad for Diageo but positive for USL.

Infact an opportunity to manufacture those Diageo brands in India?

It’s bad for Diageo but positive for USL.

Infact an opportunity to manufacture those Diageo brands in India?

I am thinking is it possible to manufacture say a Black label in India? The main USP for these brands is “made in scotland” and hence called “scotch”. The processes used, the water, weather, ingredients and even the barrels add up to the unique profile of these spirits. While I agree Indian made single malt can also be equally good but I doubt if they can be a substitute to the heritage and unique profile of these age old legends…

Not possible . Scotch can’t be reproduced anywhere else.

Interesting Pioneer Distilleries has got few NOCs merger this month… Discount of 5-7% still if you buy Pioneer Distilleries

A bit long at around 45 mins but reveals a lot about the man at helm of the ship. Increases my conviction even further

Disc : Invested, one of my top holdings.

United spirits Q2 concall was on 5th Nov as per bse. But nowhere transcript or audio is available. Does anyone have any idea?

check stockadda, it is there.

New CEO at the helm from July 2021

Have started tracking the business very recently.

I understand that the company has tried to increase margins by debt reduction and cost cutting and has been able to do so quite successfully. There is still some scope for margin improvement - as the management suggests.

My questions to all those who are consistently tracking the business:

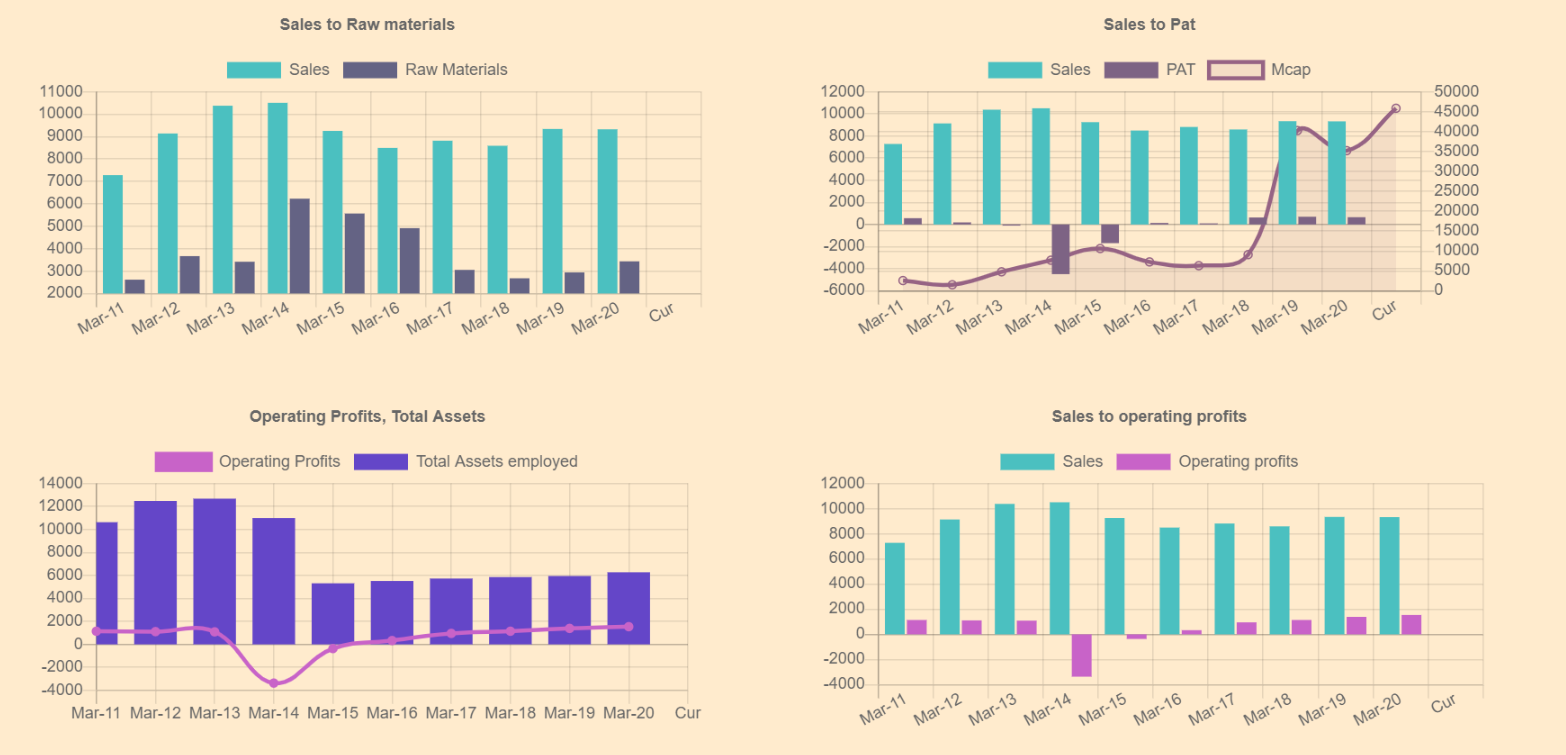

Other than that the company has steadily franchised out lower margin popular segment business and increased sales contribution of Prestige and Above segment in total sales. As you would be aware that sales growth is higher in Prestige and Above, also margin is higher in that segment. Hence there is a shift from low margin Popular segment to high margin Prestive and Above segment. Due to this sales remain constant, but see the growth in PAT. EPS 5 times from 2016 to 2020.

| Year | Sales Volume Total (in Million cases) | P&A Volume % | P&A Value % | Growth in P&A (Volume) | Growth in P&A (Value) |

|---|---|---|---|---|---|

| 2016 | 93 | 37% | 51% | 10% | 26% |

| 2017 | 90 | 41% | 58% | 7.7% | 13% |

| 2018 | 78.5 | 47% | 63% | 1% | 3% |

| 2019 | 81.6 | 50.9% | 71% | 11.8% | 15.2% |

| 2020 | 79.7 | 51.3% | 65.2% | -1.5% | 0.4% |

Growth in sales would start to appear once P&A value becomes dominant (>80%) and franchising operation of popular brand is stable. So the answer to “Is the cost-cutting sustainable in the long-run?”, yes it is sustainable, because other than immediate cost cutting, premiumization trend is helping the company. With globally established brands and significant experience in route to market, USL would do better and better with time.

Time correction in the quality name. That is the risk of overpaying.

Thanks Suraj for this lucid explanation! Really helpful!

I was reading few concalls and have deduced that:

IMO, this can turn out to be a really long term play.

Havn’t gone through the annual reports yet. Reading the concall trascripts currently.

Disc: Tracking

Tern Distilleries being sold to NCL Industries Limited for consideration of INR 30 crore.

For the financial year ended March 2020, Tern Distilleries was a non-operative company and consequently did not have any turnover or revenue or income. It had a net worth of approximately INR 134 million representing 0.36% of USL’s consolidated net-worth.

This was acquired in 2013 for 13.4 Crs. Good to see some operational optimization & cleanup of non-essential assets. The sale will be completed in 30 Days.

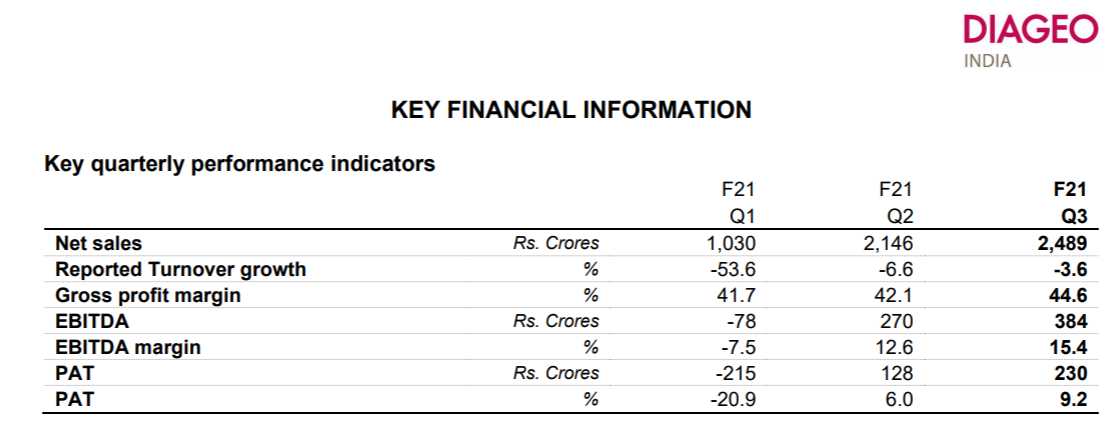

The Q3 results seem good to me as QoQ recovery looks better than expectation.

However, I am unable to understand huge different in Revenue and Profits by different websites.

Below article puts revenues in range of 7000+ cr and Profit as 280 cr

This one puts revenue as 2489 cr and profits as 230 cr

One thing is clear - One is consolidated and other is standalone figures. But why is such a huge difference. Consolidated revenues is almost four times of standalone revenues. Seems like there are three other United Spirits running within the Consolidated United Spirits? What am I missing here? Thanks

Gross Sales vs Net Sales

Difference is the excise duties.

We should Refer to the official statement on BSE for clarity on numbers.

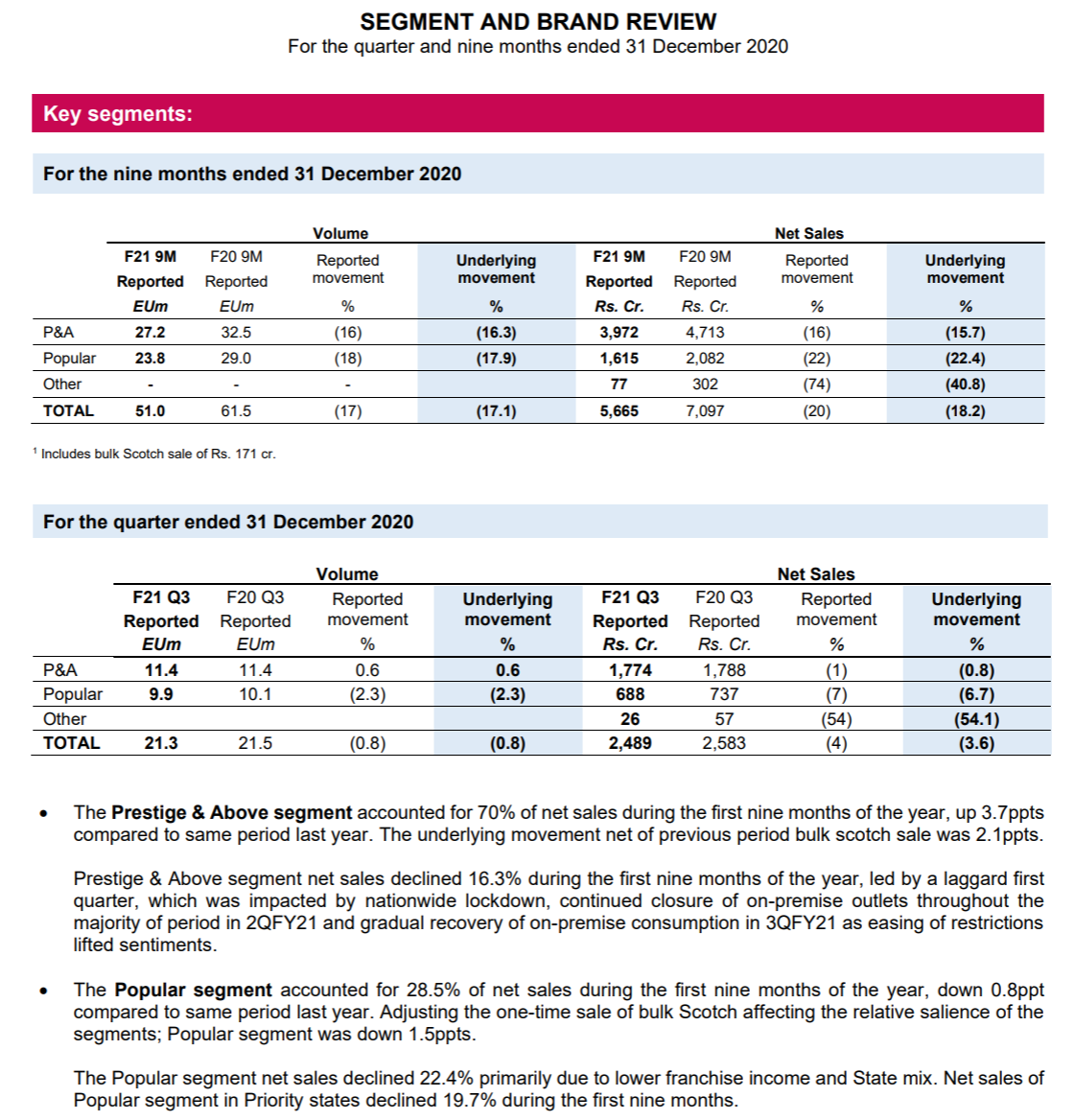

The growth in P&A segment continues & should do so in future as well. This will aid in increasing GM & bottom-line. Q3 was a good recovery for this year & the Q4 should be on the same lines. With the appointment of Hina Nagarajan the change in growth orbits for the next phase is apparent & valuation should also inch higher in line with a MNC consumption company as we go forward in next few quarters.

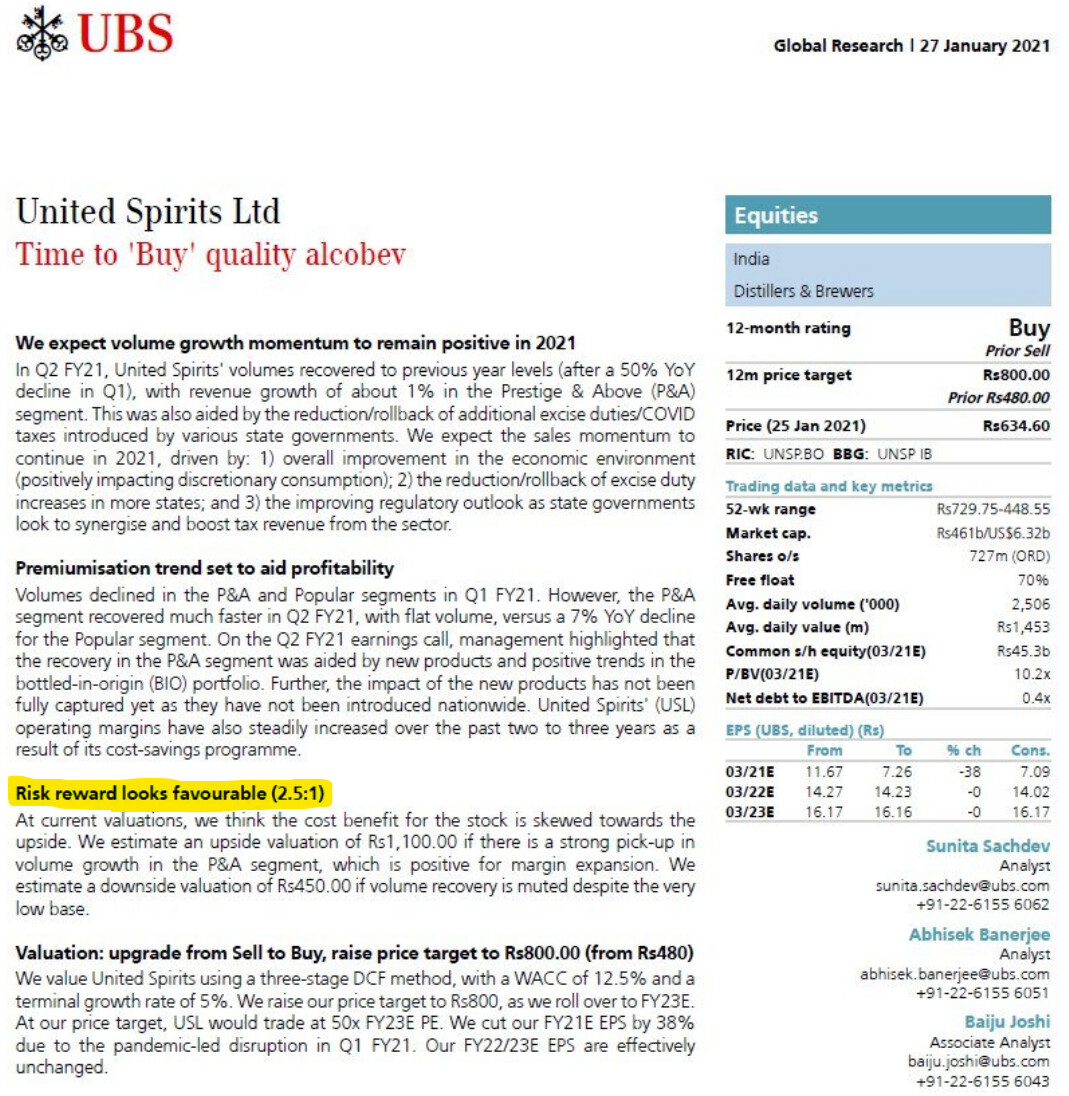

As per a recent UBS report on USL - the risk reward is quite favorable for the upside from here.

Disc: Invested from lower level & Part of core PF.

Does anyone have the full report from UBS?

Seems quite high conviction given the target price.

I understand that we do not discuss price movements and that is not the intention of my this post, however, I am unable to understand the market reaction after better than expected results from United Spirits. The stock was hammered last two days.

Intention of this post is to understand if there was anything fundamentally not good in the results and business recovery that I missed, as markets know better and I think I must have missed something. United Breweries also reported similar yoy and qoq volume trajectory but still its result was respected and its valuation is way higher than United Spirits. I am aware we cannot directly compare the two but the difference is too huge. Thoughts welcome

Your concern is genuine. But here important point is - Better Than Expected. This is by whom is more important.

These are my thoughts on this.

Market simply LOVES growth and hates de-growth. Its may accept the de-growth in net profit but won’t accept any degrowth in sales. And mind you alcohol shops were one of the first to be opened by almost all states for the Tax Revenue generation. So probably market was expecting better net sales.

Other obvious reason is the high PE ratio. And with such results market will think twice before giving it say PE of above 100 ( I am guessing a number here)

Other much more personal thinking is WHY give such a high PE of such a low margin and tax burdened business when there are plenty of better opportunities are available in the market.

Regards,

Vikas