My highlevel notes and calculations based on Management guidance and some baseline assumptions post the H1 con-call is as below,

Management gave these guidance numbers,

• Uganda: 40% ( margin stable ±2%)

• India (Navi + Nashik): 17.5% midpoint of guided 15–20% for first-year operations

• Uganda target ARPOB = ₹55k–₹60k

• India initial ARPOB = ₹27k–₹28k for Navi Mumbai

• Nashik similar ARPOB ₹25k–₹28k

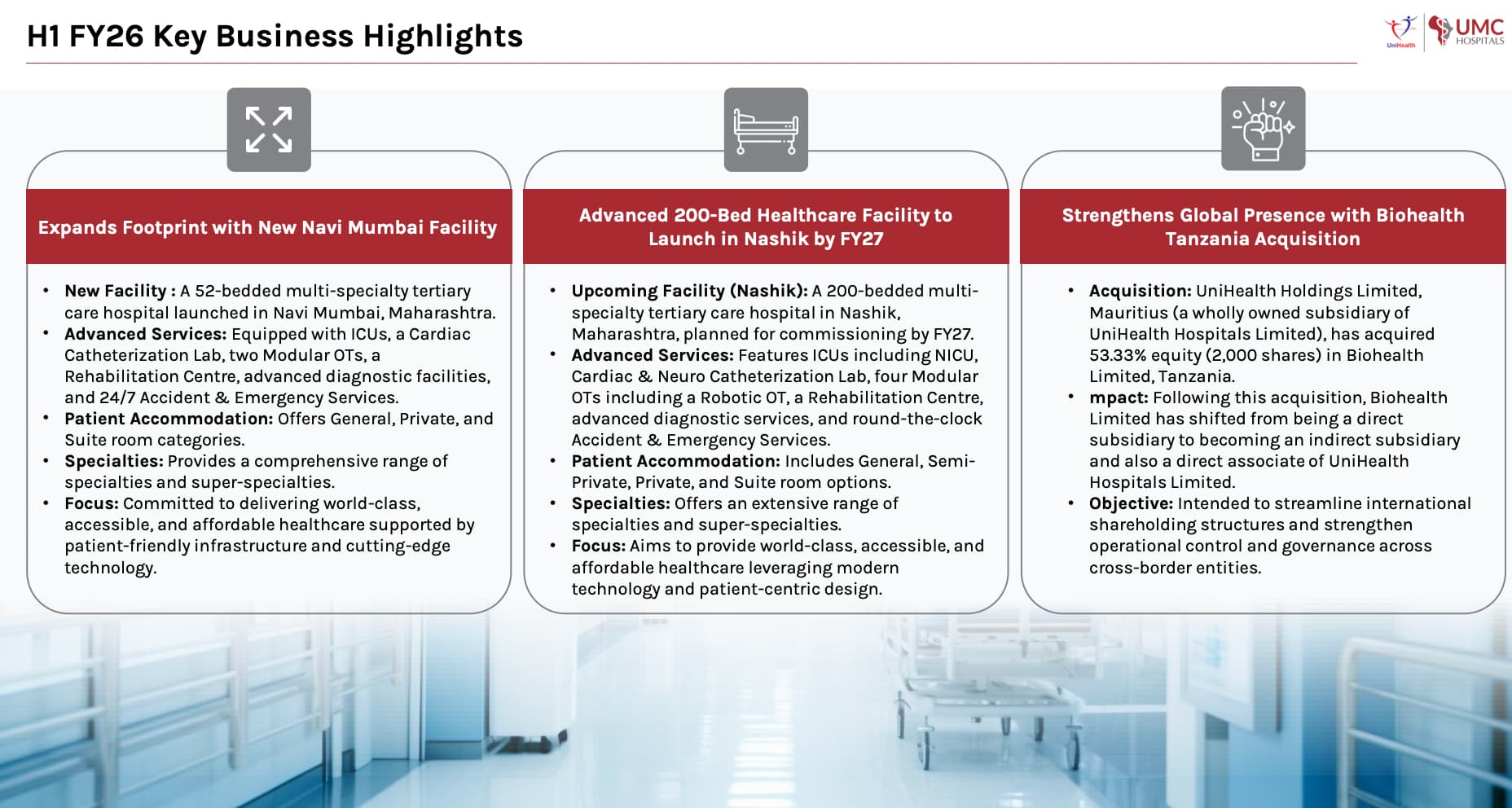

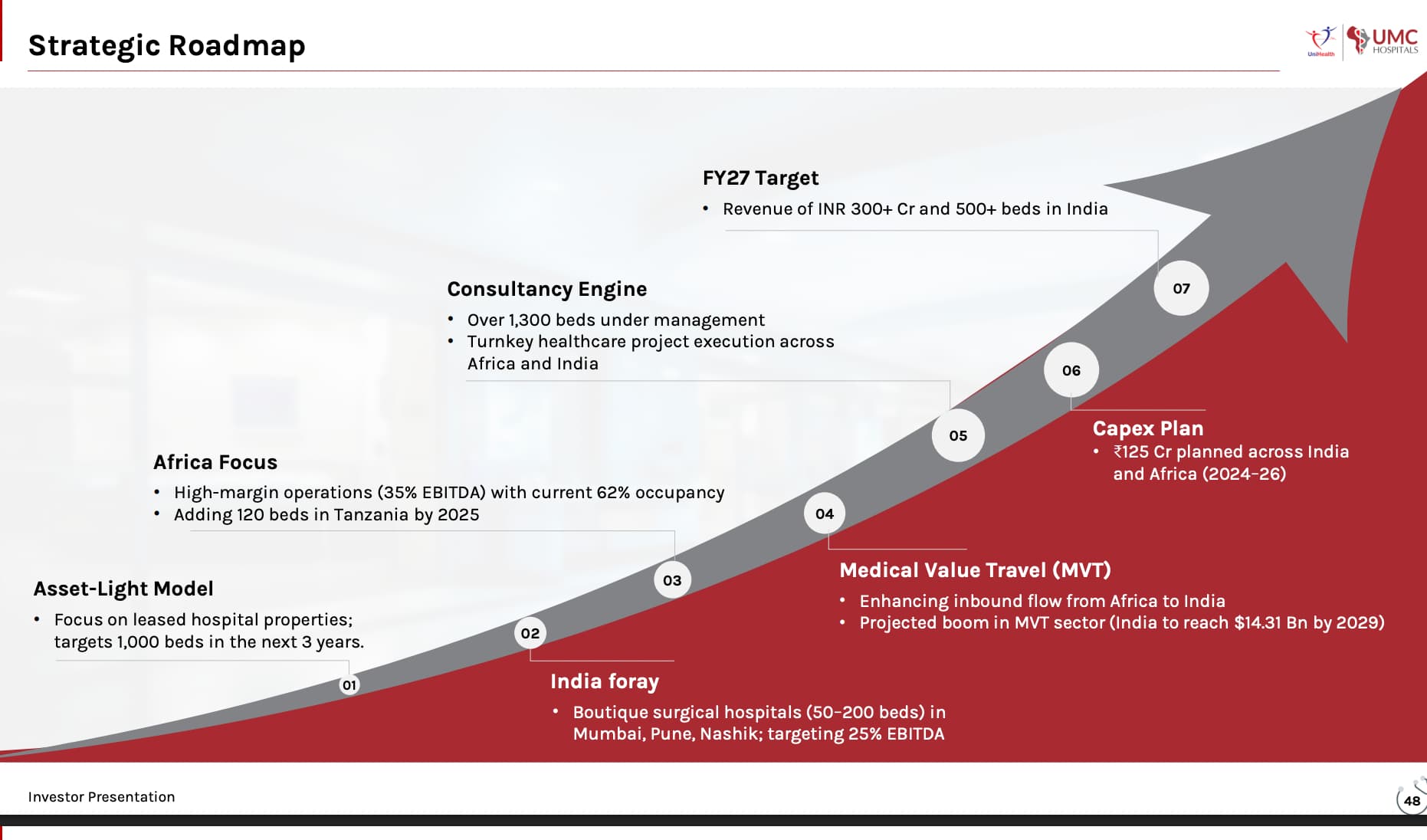

• Uganda = 120 beds

• Navi Mumbai = 52 beds

• Nashik = 200 beds

Not considered for working out the numbers ,

• Tanzania 20-bed centre

• Tanzania 100-bed tertiary acquisition

• Consultancy vertical beds/revenues

All revenues in Cr.

| Region | Hospital | Beds | ARPOB (₹/day) | Revenue FY26 | Revenue FY27 | Revenue FY28 | EBITDA FY26 | EBITDA FY27 | EBITDA FY28 |

|---|---|---|---|---|---|---|---|---|---|

| Africa | Uganda – UMC | 120 | 55,000–60,000 | 126 | 126 | 132 | 50.4 (40%) | 50.4 (40%) | 52.8 (40%) |

| India | Navi Mumbai | 52 | 27,000–28,000 | — | 30 | 33 | — | 5.25 (17.5%) | 5.7 (17.5%) |

| India | Nashik | 200 | 25,000–28,000 | — | 100 | 110 | — | 17.5 (17.5%) | 19.25 (17.5%) |

| TOTAL | — | 372 | — | 140 | 251 | 275 | 50.4 | 73.15 | 77.75 |

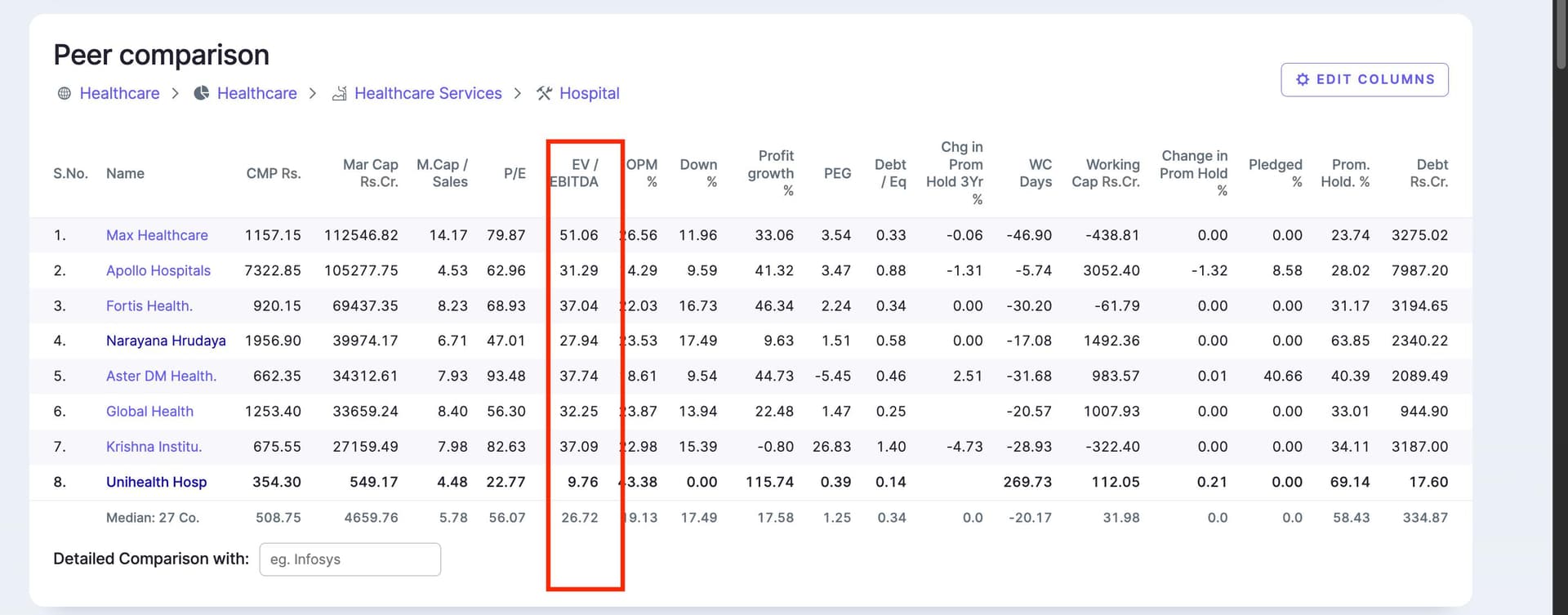

The Sector trades at 30-40 EV/EBIDTA.

At 20 X EV EBIDTA FY28 it works out to around 1400 Cr EV (market cap +debt) at 70Cr edbidta.

Need to see future fund raise and debt plan. Looks undervalued to me at this price too post the run up.

PS: Invested with a small allocation recently. Contemplating adding more on dips.