• ABOUT:

Unihealth Consultancy Limited is a healthcare service provider with a global presence, particularly in Africa. The Company is having its presence in diverse business segments, that include medical centers, hospitals, consultancy services, distribution of pharmaceutical and medical consumable products and medical value travel.

BUSINESS SEGMENTS:

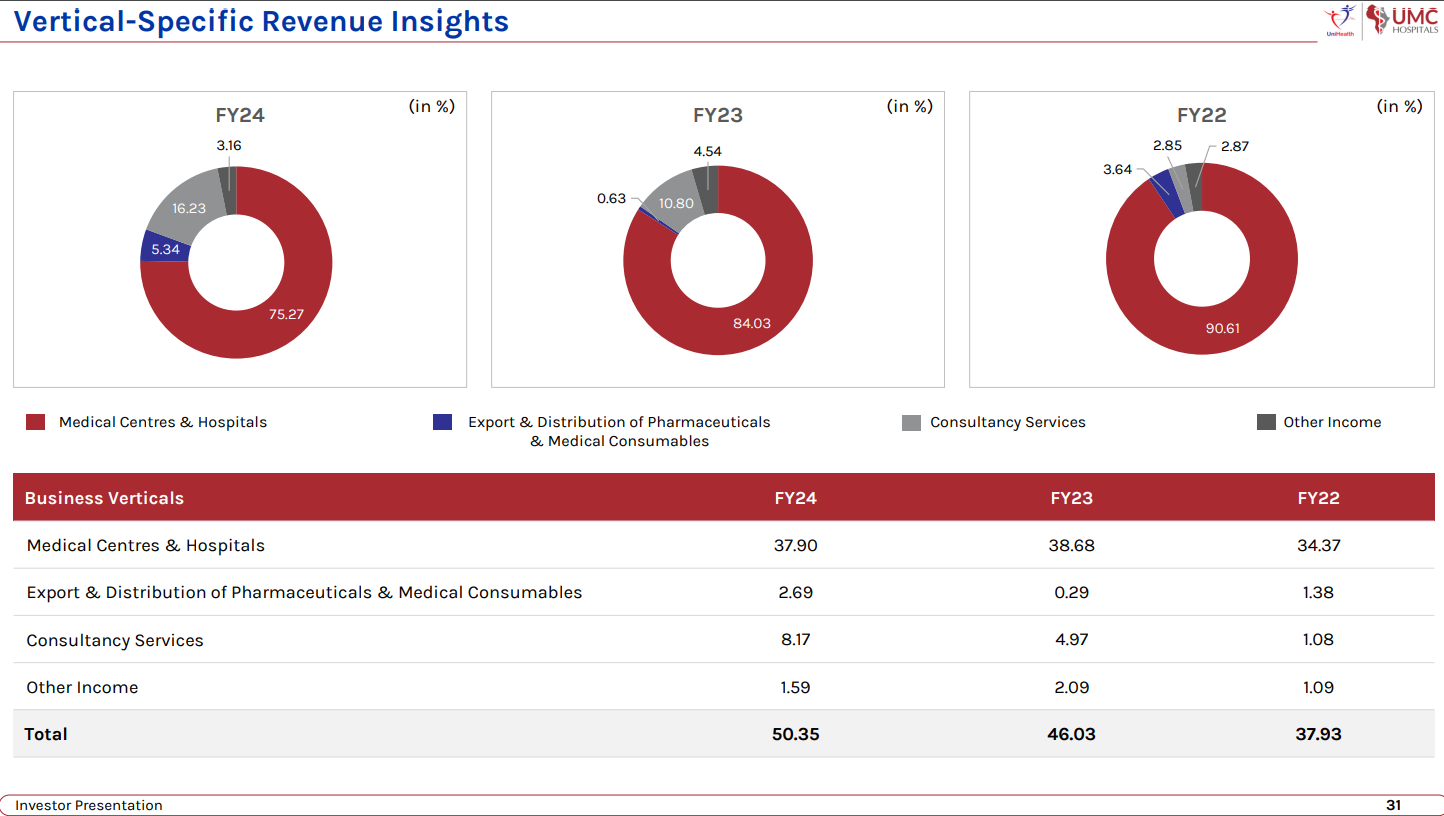

Medical centers and hospitals: Under the ‘UMC Hospitals’ brand, the company manages two multi-specialty facilities: UMC Victoria Hospital in Kampala, Uganda, and UMC Zhahir Hospital in Kano (Nigeria), collectively operating a cumulative bed strength of 200 operational beds. Unihealth also operates ‘Unihealth Medical Centre,’ a dedicated dialysis facility in Mwanza, Tanzania.

In Uganda, we are the only UN accredited hospital in the country. So, we’ve got the entire United Nations as our patient base. We are also the preferred hospital of choice for the Ugandan military.

Healthcare Consultancy services: UniHealth offers end-to-end solutions following global standards and practices. The Group has become a one-stop service provider, assisting clients from pre-development stages to successful project commissioning of healthcare centres.

Services: Project Report & Feasibility Study Architectural Planning & Designing Medical Planning & Procurement Management Consultancy Quality Management & Accreditation Business Process Restructuring Operations & Management Project Management Consultancy

1,000+ Beds in projects under consultancy

Distribution of Pharma products and medical consumables: The company exports and distributes pharmaceutical and medical consumable products to Uganda, Tanzania, and Nigeria, serving as reputable distributors for several Indian manufacturing companies across these African nations.

Medical travel: UniHealth is a leading provider of medical travel facilitation services, assisting international patients seeking specialized treatments in India. With a network of over 50 tertiary care hospitals, the Group prioritizes patient care and comfort.

INVESTMENT THESIS

• LONG RUNWAY FOR COMPOUNDING GROWTH:

o PRESENCE IN THE SECULAR HEALTHCARE INDUSTRY: Demand for hospitals, consultancy services is going to consistently increase at a good pace for a long time, offering the company a long runway to achieve compounding growth.

o BIG DEMAND-SUPPLY IMBALANCE FOR HEALTHCARE SERVICES IN AFRICA:

As per the last available data, as per World Bank Databank, the number of hospital beds available per 1,000 people in Uganda in 2010 and in Nigeria in 2004 was 0.5 compared to the WHO recommended standard of having 3 hospital beds per 1,000 people. The number of physicians per 1,000 people in Uganda in 2017 was 0.2 and in Nigeria in 2016 was 0.4 124 compared to the WHO recommended standard of having 1 physician per 1,000 people. These statistics indicate the supply-demand gap in the countries where the Company has invested in to set up advanced tertiary care facilities, thereby underlining the available opportunities for growth in the coming years.

o INCREASING OPPORTUNITIES FOR CONSULTANCY SERVICES:

• UNIQUE BUSINESS MODEL (A bit like Mini-caplin/ Caplin of Hospital chains):

The Company has established medical centres and hospitals in countries having a skewed supply demand gap, allowing it to cater to an under-served population and make an impact on the healthcare services sector of the country.

The company ventured into countries where no other branded player went and through on-ground knowledge and experience, has established a healthy, profitable and a growing business model. Just like what Caplin did for medicines in unknown LatAm markets.

There have been many Indian players or Indian hospital groups which have gone into these countries but have not been able to actually commission a facility. So that, since we have commissioned facilities, it gives us a massive trust benefit from the local market.

The presence is relatively unknown and “risky” geographies adds an additional entry barrier for new international companies: For example, in Nigeria, you would have heard or read about Boko Haram. Boko Haram, Nigeria is a big country with almost 200 million people. Boko Haram is cantered in a small pocket, similar to say our issue in northeast or central India with the Naxalites. It’s similar. It’s there in a particular part of a particular state. It does not equate to the entire country. So, the remaining country is open for businesses, absolutely safe to move around. But what comes to India in terms of the international media is the risk profile of Nigeria. So socio-political or geopolitical risk is not something on ground that we have ever experienced. But it adds to our benefit, in terms that the overall entry barrier for any international investor in terms of coming, investing into that particular country becomes relatively higher.

If I have taken the risk of actually going there on ground, despite all these issues in the media and setting up a facility, the chances of a competitor actually coming in are fairly low because people are concerned about it. For us, the advantage has been that we have been present on ground since long before we started investing into it. Like I mentioned earlier, we started with medical travel as our initial business, because of which we had actively travelled to all these countries for a very long number, a good number of years, five or six years before we started investing in them.

• PRESENCE OF MULTIPLE GROWTH DRIVERS ACROSS MULTIPLE SEGMENTS:

o MARGIN-ACCRETIVE ADDITION OF SUPERSPECIALITY SERVICES IN EXISTING HOSPITALS: The addition of super-specialty services at its hospitals in Uganda and Nigeria will allow the Company to add high-revenue generating departments by investing only in the required equipment and working capital. The Company will benefit from available space within its hospitals as well as the existing administrative manpower to oversee these departments. Furthermore, these departments will be able to generate revenue on an immediate basis post commissioning in view of the existing patient-base of the hospitals.

There’s a great demand for super specialty services like ophthalmology, infertility, cardiac care in these geographies. So, we are going to be targeting making investments into the required equipment. Since the infrastructure is already in place, since the senior manpower is already there, since the utility staff is already there, these investments are, you know, critical from the perspective that they will allow us to generate higher revenues at much higher EBITDA. Because the cost of the investment or the operating cost both is only in the equipment and the specialized manpower to operate that particular equipment. All the remaining expenses are already being taken care of since it’s an existing infrastructure.

o NEW HOSPITAL IN TANZANIA: The company already has a medical centre in Mwanza, Tanzania and its looking graduate from a medical centre to a hospital by adding a bed capacity of 50 in-patient beds and equipping the operating theatre with the necessary equipment to extend surgical services to its patients, in addition to strengthening its radiology diagnostic services. The medical centre, owing to its location and registration with the National Health Insurance Fund (NHIF) is well positioned to benefit from expanding the scope of services being provided at its facility.

The company is also looking at inorganic acquisition or Operations and maintenance collaboration in Tanzania

o NEW SYRINGE MANUFACTURING PLANT IN TANZANIA: The company is putting up a syringe manufacturing unit in Tanzania. The facility is presently in the process of getting constructed. Expect the commissioning of that facility somewhere around June 2024. Total investment will be roughly about INR8 crores.

The idea is to start with syringe manufacturing, disposable syringes, and then add a variety of other similar lined products, medical consumable products for that. These countries like Tanzania are heavily dependent on importation of all these medical consumables. So, the government is very, very keen to locally indigenize the entire product profile for local manufacturing and is supporting the entire initiative.

The procurement is mainly going to be by the government itself. So that gives us a very strong standing in terms of ensuring that our 100% manufactured product is getting sold within a shorter period as compared to a competitive market like India.

We are initially putting up a plant of the capacity of about 2,00,000 syringes per day. So, we will be targeting about 5 million to 6 million syringes every month. Revenue potential, additional details will be shared by management in due course.

o INCREASING REGISTRATIONS FOR EXPORT OF PHARMA PRODCUTS:

Pharmaceutical distribution and export is something which the company recently started. In all these countries, you need registration of the manufacturing facility, the plant, as well as all the drugs. And that process can take about 18-odd months. The company has initiated that process in certain countries with certain companies, and is expecting all these approvals to be there in the next 9 to 15 months, different products at different levels. So, in the fiscal year, somewhere around 2025-26, the contribution from that division will increase considerably once all these products are registered.

Unihealth Uganda Limited (UUL) UUL has recently procured the wholesale pharmacy license from the National Drug Authority of Uganda to trade and distribute pharmaceutical and medical consumable products in Uganda. The company has submitted applications to register its partner Indian manufacturers in Uganda with the intent to expand its distribution business in the country

The company is planning to develop its distribution network and collaborate with an increasing number of manufacturers / brands for exclusive distribution. The Company, by capitalising and leveraging on its inherent requirements and infrastructural advantage, intends to expand its distribution network in the region of its presence by creating a dedicated team of medical and marketing representatives and participating in tenders floated by the government agencies as well as nongovernmental organisations for procurement of the products being distributed by our Company. Simultaneously, our Company also plans to increase the number of portfolio companies with which it is associated to increase the number of inter-linked products that it can offer its target clientele by using the same distribution network and field workforce.

o INCREASING PROJECTS IN CONSULTANCY VERTICAL:

Pune project: The appointment of the Company as the Project Management Consultant for the proposed 300+ bedded PHRC Health City in Pune reflects the Company’s ability to secure and work upon projects of size, in-effect, acting as a proof of concept for probable projects that the Company bids in the future.

Myanmar project: MoU signed for a 300-bed Health City in Yangon, Myanmar with Maykhalar Group.

The state of the project is that we’re looking at a 300-bed hospital in two phases. The building structure, the superstructure is already there. So, that construction has already been completed by the local partner. Now, the expertise required to actually convert that building into a hospital is where UniHealth comes in. So, this project again we are doing on the DBO model that we have, Design, Build and Operate. But we are first going to help them design it, then execute the entire aspect other than the construction. So, when I say execution, we’ll help them plan the equipment, the processes and everything, to take it to the commissioning phase and eventually look at operating it. Right now, the project is at an MOU level. The agreement level will be in a cross-over in another quarter or so, following which that project will move ahead. On ground, whatever local formalities are needed to actually take this forward, including a financial closure at the partner’s end, at the client’s end, that is an ongoing process right now. So, hopefully, in tandem with the timeline for the agreement, that particular process will also get completed with.

Kenya project: UniHealth Expands Global Footprint through Key Healthcare Consultancy Partnership in Kenya. UniHealth has entered a service agreement with North Coast Healthcare Solutions Limited in Kenya. The collaboration focuses on providing detailed design consultancy for Links Hospital, a visionary 200-bed tertiary care multi-specialty hospital in Mombasa, Kenya. Planned on a land parcel spanning 43,000 square feet, Links Hospital aims to be a healthcare landmark with a proposed built-up area exceeding 2 lac square feet.

As the company keeps on doing more and more projects, its reputation and experience will increase and thus, allowing it to bid on more and more projects. This can be long term growth driver.

The Consultancy Services vertical of the Company allows it to explore opportunities to forge partnerships to set-up and expand our network of hospitals under the ‘UMC Hospitals’ brand, either by way of equity partnerships or operations and management agreements, thereby supporting the growth avenues for the Company in addition to generating revenues and profits as a standalone business unit.

o PARTNERSHIPS IN MEDICAL TRAVEL:

Recently announced Collaboration with Myanmar airlines for medical travel. UniHealth - MAI Medical Travel Program. Discussions going on with Air Tanzania.

o LOOKING TO EXPAND HOSPITALS IN INDIA AND OTHER COUNTRIES:

Going forward, by 2025-26, we target a 1,000-bed capacity. Of that, we are also targeting to have about 300 to 350 beds on an O&M, as an operating and management contract basis within India. Target markets right now are mainly Western India. So that will also significantly contribute to the top line and bottom line as we move forward in the next two fiscals.

The second part of expansion in terms of the geography that we are looking at, outside the existing facilities, we are actively looking at Tanzania, where we have presence in terms of a medical and a dialysis center to put up a hospital and, you know, explore both acquisition opportunities as well as organic growth. Other geography of, you know, in terms of target geographies, which we are very keenly looking at is Kenya. So Kenyan healthcare is also booming.

o DEVELOPING NEW HEALTHCARE PLATFORM: The Company has embarked on a project to develop a comprehensive health-tech platform to extend a variety of tech-enabled services to its patients across the geographies of its presence. With an existing patient inflow of more than 1,00,000 patients annually, the Company intends to capitalise on the available target clientele to offer its services. The tech-platform being considered by the Company will provide e-health services like online consultations, electronic health records, scheduling of appointments and lab collections as well as e-pharmacy solutions. The data collected will allow the Company to analyse trends and plan its marketing strategies and investments in key specialties in accordance with the expected inflow of patients, their spending patterns and provide our Company with accelerated benefits.

o UHS Oncology Private Limited (UOPL) UOPL has been recently incorporated by UCL to set-up dedicated radiation oncology units and cancer care centres in key target geographies in Africa. The company aims to carry on the business of developing, promoting, marketing or supplying radiation therapy services, chemotherapy services in any manner whatsoever in India or elsewhere and bridge the wide supply-demand gap in the critical area of cancer care.

• COMPETITIVE ADVANTAGES:

o SCALE ECONOMICS: UMC Victoria Hospital, the Company’s flagship facility in Uganda is the largest private sector hospital of the country while UMC Zhahir Hospital, the Company’s facility in Nigeria is the largest private sector hospital of the Northern Nigerian region. These ensure that the Company is able to derive maximum benefit from economies of scale relevant to the said geographies. Scale economics is particularly relevant to hospitals which have a high fixed cost and thus can benefit immensely with increasing scale and market leadership.

o COST ADVANTAGES BECAUSE OF INTERLINKED BUSINESS VERTICALS:

Now, the entire business model over the years, from 2010 that we started till today, has evolved into an interlinked business model.

In terms of hospitals, we’ve got our consultancy services which can help the client or the target principal, help design the facility, and we come in as operators. We follow it up even with consumable exports and pharmaceutical exports from India. So that effectively is allowing all our functioning units to bring down our cost of inventory, which in a hospital is a major, major cost.

So, the two major cost centers for our hospitals are the cost of manpower and the cost of inventory. Being an in-house supply chain, the cost of inventory for us reduces considerably, right from the time that we are making capital investment. So even in terms of the initial equipment, compared to a competitor which is locally present in Africa, who’s going to be sourcing equipment globally or locally from within the continent, we are able to source the equipment at a much, much lower cost. Now what that allows us to do is bring down the capex considerably compared to our peers, and typically we can see that half of our battle is won at that level itself.

This we follow up with a reduction in the cost of inventory when we talk about the operational expenses. So that allows us to increase our EBITDA margin considerably compared to our peers, reinvest significantly in newer equipment, newer technology, and stay ahead of competition.

The existing facilities provide great opportunity for the Company to add inter-linked verticals like distribution of medical consumables and pharmaceuticals and health-tech solutions. The captive consumption and access to the existing patient-base as the target clientele provide financial viability to the Company to invest into these newer verticals which, in due course, provide the Company with incremental opportunities of growth outside the captive requirements. This unique proposition allows the Company to widen its service segments and provide comprehensive solutions to its consultancy services clients in India and overseas, thereby positioning it better to attract interest and secure projects from its clients.

Every vertical of business has been categorized operationally as a standalone business unit with a management and reporting structure in place to ensure that it achieves financial viability and profitability on an individual basis. The day-to-day operational governance of these verticals is overseen by the Head of Operations of the given vertical with pre-defined reporting structure and timelines in place for the Management to review the same.

• LACK OF REAL COMPETITION IN HOSPITAL SEGMENT:

So, competitors are there, government-run hospitals definitely are there, but government-run hospitals are somewhere where the paying patient would not really want to go. So, that is the Swahili state of the region itself. So, those are not really our competitors. Then in the private sector, so there are few local hospitals, no international chain is there per se, which is there present in these countries. So, competition is not there from local, it’s not there from international players, it’s mainly from local hospital groups. So, some doctors would have founded a hospital or an older hospital, which was already there over the years

The benefit that we have is two-fold. One, we focus highly on specialized and super specialized care. So, that allows us to fill the supply-demand gap. A lot of the local hospitals which are there, their main focus has been basic surgeries till now.

Second, when they are looking at expanding into specialized and super-specialized care. The challenge that they are facing is two-fold. One, the cost of equipment for them is way higher because they are procuring locally from the local distributor of GE or Siemens or Philips or whosoever it is, versus us where we have the ability to procure from India and export it at a marginal cost. So, in terms of the cost of investment becomes low, automatically we have that added advantage out there.

Second benefit that we get is in terms of manpower. We have to be dependent only on local manpower because when it comes to Indian manpower, whether it’s technicians or paramedical nurses or even doctors, for them it is relatively difficult to source them and to develop trust. Vis-a-vis, giving help, we are able to do it in a much easier manner. So, from these two-folds, we have that advantage over these local existing facilities when it comes to the overall business potential.

So, currently competition is very low. Even if competition were to increase in the future, the demand supply gap is so wide, that it can easily accommodate new players and not hurt the growth of the company.

• YOUNG AND ENTERPRISING MANAGEMENT:

The promoters Dr. Akshay Parmar and Dr. Anurag Shah are 36 and 38 years old. They started the company in their mid-twenties and have evolved the company from a single vertical of medical travel to the interlinked, profitable business which it is currently. This shows their capability and enterprising thinking. Dr. Anurag Shah lives in Uganda. So, he has on ground information and knowledge directly.

Extremely clear and good answers on all questions of concall and interview.

From DHRP: There is no outstanding litigation against our Promoters

• GOOD FINANCIALS:

High Ebitda margins: 32%

High ROCE: 20%

Net debt free (Because of IPO proceeds)

Strong sales growth for last 4 years

Positive Free cashflow

RISKS

• CURRENCY FLUCTUATIONS: The only major risk factor that we can look at is the currency depreciation. So, in Africa, the currency risk is fairly high compared to a lot of other countries. So that is something that is a fairly higher risk factor which we prefer factoring in when it comes to Africa compared to geopolitical issues.

• GEOPOLITICAL RISKS: But on the ground, over the years, over the last seven, eight years of our presence in terms of our own investments on the ground, we have not encountered any specific security issue or geopolitical issue.

For example, in Nigeria, you would have heard or read about Boko Haram. Boko Haram, Nigeria is a big country with almost 200 million people. Boko Haram is cantered in a small pocket, similar to say our issue in northeast or central India with the Naxalites. It’s similar. It’s there in a particular part of a particular state. It does not equate to the entire country. So, the remaining country is open for businesses, absolutely safe to move around.

Like I mentioned earlier, we started with medical travel as our initial business, because of which we had actively travelled to all these countries for a very long number, a good number of years, five or six years before we started investing in them.

Second part is that healthcare is the need of the hour out there. So, it is something which is needed by the ruling government. It is something that is needed by the opposition. It is something that is needed by the police force. It is something that is needed by the military. So almost everything or every agency or political collaboration in these countries need quality healthcare. So, healthcare from that perspective is fairly well protected because of the patient base that we have. So, in Uganda, for example, we are the only UN accredited hospital in the country. So, we’ve got the entire United Nations as our patient base. We are also the preferred hospital of choice for the Ugandan military. Similar goes for the parliamentarians, the cabinet ministers. So overall, the patient profile is also such that as a hospital, as a healthcare company, we are fairly well protected and cushioned from a lot of these kind of issues that from perception may arise.

• VALUATION SLIGHTLY HIGH:

Company trading at 15x EV/EBIT. So slightly above fair value. Would have liked to have at 10-12x EV/EBIT. But given the immense potential of the company and more importantly, the long-term runway for growth, paying slightly high valuation is okay. If the growth comes as expected, then valuations will take care of themselves.

Only thing the slightly high valuations exposes us is to temporary downturns, both because of overall market or because of company specific/execution issues.

• HIGH WORKING CAPITAL REQUIREMENTS: Working capital days high at 170 days. Because of long payment cycle by the Uganda Government. But it’s not a concern as explained below.

So, in Uganda, the payment cycle from the government extends quite significantly and go in between nine months to 10 months of actually submitting the bill. But the benefit is two-fold in that one, the overall treatment charges that the contractual rates with the government agencies are higher than your cash patients. So, basically, the cost of funding incurred by the company is already taken care of in the margin which is there for these patients.

Second, in the history of Uganda over the last 25 years, 30 years, and in our discussion with a lot of bankers out there, what has been established and what we’ve also seen in the last five years of our association with them is that one, there is never been a default in the payment, so it has never so happened with any company that it has been default because eventually it is the government which is paying.

And second, there has never been a deduction. So, when it comes to private company, private insurance, we have to factor in a margin of about 2% to 5% which may get deducted based on rejection of certain bills that the insurance has, similar to the private insurances in India. But when it comes to the government, if your bill is $100, you will receive $100 payment, even if it comes up to nine months, it’s not going to be $99 or $98, it is going to be a full $100. So, that is another benefit that the rejection ratio for these payments is zero.

When we go to Nigeria, the ratio changes majorly, it becomes about 70%, 75% as cash patients, and only 25% as credit patients, getting corporate out there or certain medical insurance companies out there. In Tanzania, the government itself has a National Health Insurance Scheme. They call it the NHIF, National Health Insurance Fund. So, the payment comes from that particular scheme. So, the patients, almost 70% or 75% of the patient base, it is from NHIF and paid for by NHIS. Those payments normally are able to receive anywhere between 90 to 100 days.

• Contingent liability of 8cr: Income tax demand raised

• Our revenue and profitability are inherently influenced by the project-based nature of our consultancy services.

WHAT TO DO

BUY. It’s a very unique opportunity. Like getting on the ground floor of the next caplin. Buy Half quantity @cmp and more as / if correction comes or as results come in the future.

THINGS TO MONITER

• SUPERSPECIALITY SERVICES AND ITS IMPACT ON MARGINS

• CAPEX PLAN OF 1000 BEDS AND NEW HOSPITALS UNDER OPERATIONS AND MANGEMENT MODEL (can they replicate their previous successes?)

• TANZANIA PLANT AND ITS EXECUTION AND SALES

• EXECUTION OF CURRENT CONSULTANCY DEALS AND NEW DEAL WINS

• TANZANIA HOSPITAL CAPEX AND SUBSEQUENT SALES

• PHARMA DISTRIBUTION SALES, TIE-UPS AND REGISTRATIONS UPDATES

• CURRENCY FLUCTUATIONS

• RECEIVABLES AND WORKING CAPITAL

• GEOPOLITICAL NEWS AND DEVELOPMENT.

• DEVELOPING NEW SALES GEOGRAPHIES, PARTICULARLY INDIA.

• MEDICAL TRAVEL PARTNERSHIPS AND HEALTHCARE PLATFORM

• ANY CHANGE IN COMPETITIVE LANDSCAPE (Highly highly unlikely)

MISCELLANEOUS/BUSINESS INFORMATION

• CAPEX: At present, we have a capex plan of more than INR 2,500 lakhs for the next two years. Our mission is to increase our bed capacity to roughly around 1,000 beds from our current 200-bed capacity. This is targeted by the end of fiscal year 2025-26. Part of it may be acquisition also. And we are going to be acquiring, we will be looking at a 50 bed to 100 bed facility. That is going to be the model for our acquisition plan.

• ASSET LIGHT MODEL GOING FORWARD: Going forward, the capex plan is typically aimed at investing in equipment. We are not looking at investing in infrastructure. We are planning to work on an asset light model. Because of our existing hospitals, which act as proof of concept in these geographies, we’ve got a good number of opportunities where we have infrastructure ready for us, where they are open to the infrastructure, either on a revenue share model or a long-term lease model, which works very well for us because then we are reducing our capital investment in land and building. And we focus mainly on the high-end equipment that is required to run specialized hospitals. So, the focus going forward, as we expand from our 200 beds to targeted 1000 beds, is going to be more on operations and management of these facilities and investing in the equipment, not in the real estate, so more of an asset-light model.

So, because of our existing hospitals, the trust that the brand has in these geographies is very high. There have been many Indian players or Indian hospital groups which have gone into these countries but have not been able to actually commission a facility. So that, since we have commissioned facilities, it gives us a massive trust benefit from the local market. And that is where we are well positioned even to consider acquisition or partnerships with players who are keen to invest in the infrastructure aspect of the hospital.

• So I am saying in certain countries, we have got our local partners already, like in the countries of our presence, Uganda, Nigeria, we got local partners. So as and when we are expanding our footprint in those countries, the entire capital investment that is going to be made, is going to be made by us in equal proportion by our local partner. And we are also open to funding from the local banks out there. So whatever capex outline that we have outlined at this moment, whatever I have mentioned in terms of the INR25 crores of capex, that is the contribution that UniHealth Consultancy will be making towards achieving the commissioning or realizing the projects that are presently formalized to a large extent. In terms of the strategy, the location and everything, definitely there is going to be investment from our local partners also. And there is going to be a certain amount of funding that we may look at from the local banks, maybe in terms of the working capital, equipment funding, in this manner. So the overall capital investment that will eventually be made to roll out the project is going to be higher. It is going to be more than double of what I have mentioned. What I have mentioned is only the contribution you will not by UniHealth at this moment.

• setting up super specialized centers, mainly looking at ophthalmology, infertility, there is IVF and cardiology to begin with. At a later stage, we will also explore, you know, cancer care in a much bigger footprint. But that may come only after one more fiscal going forward.

• We follow something which is a DBO model of business, which is design, build, and operate when it comes to medical centers and hospitals. So, we have a solution right from the beginning, that is, from the time that we have land available with us or basic infrastructure available with us, and we specialize in converting that existing infrastructure all the way into an operational facility, going forward and operating it as well.

So, when it comes to geographies like Africa, where we are present or where we intend to expand, getting the right mix of consultants to actually help you put up a hospital and then getting the right operator in these markets is quite a challenging task from the local perspective. With UniHealth, they’re able to get all of this at the same level, within the same company. We have got specialized teams which are taking care of the initial planning, conceptualization, designing, architecturally, as well as interior equipment planning. So that is one team of the company, which works as a standalone business unit, which caters to that requirement.

• In our understanding, especially in terms of the African market, any specific unknown unit, a single hospital is rightly positioned if it is between 70 beds to about 120-130 beds. Anything beyond that in terms of a single site may not be able to generate profitability in the same proportion. So, the highest profitability in terms of the overall revenue structure and expenses is best in this particular segment. So, like in Uganda, we already have 120 beds. We don’t foresee an increase in the same facility. So, the same goes with Nigeria. We have got an 80-bed facility in Kano. We will not expand that facility in further. We would rather put up a smaller facility in some other city which is equally lucrative.

So, with 120 beds in Uganda, we are also amongst the largest facilities in the country already. So anything beyond that, because the patient profiling is such that you will not be able to attract quality patients and bring quality services, because our focus is again on superficiality specialty services. We are not looking at something which is treating malaria or typhoid or just mother and child care. So, when you look at higher revenue generating specialties, then the bed span becomes ideal at about 100 plus minus.

• So, revenue, ideal revenue per bed by the per year of any facility is about $100,000, which in Indian terms would be ranging INR80-odd lakhs per operational bed. So, the average revenue per operational bed that we would target would be in Indian terms about INR80 lakh, INR85 lakh. At present, definitely as we move forward, that number is likely to change based on inflationary requirements and a lot of other factors. But yes, right now it is the ideal average revenue per operational bed that we target anywhere between 18 months to 36 months of commissioning a facility

• So, the medical travel was something that we started with in 2010. So that was the first vertical of the company. There are multiple companies in this field today, as we speak. In 2010, there was barely any competition or there were fewer number of companies. But today, if you look at it, it is a very competitive market. There are multiple companies which facilitate and every single major hospital chain itself is also directly present.

But the unique advantage that we have is twofold. One, we’ve got physical presence in a lot of the countries from which we are targeting patients. So, basically, I’ve got my hospitals where patients come. If you are unable to serve them within the hospital for particular treatment, we have the advantage of referring that patient to India. So that is one major first advantage that we have. And second is the unique model that we have been pursuing since the beginning. So, we have had a very unique collaboration with Ethiopian Air in 2013, under which we had launched a program called Ethiopian Air Medical Travel Program. We were accessing all physical offices of Ethiopian Air across Africa to provide medical travel services, to promote and market these services. We also gave massive discounts on the air tickets for air travel, which would attract these patients. Now we are pursuing similar discussions like I mentioned with Air Tanzania, with Myanmar Airways. So, we’ve got certain unique product profiles that we are venturing into, which give us a slight advantage over the peers that we have and even over the hospitals that are competing. But yes, it is a fairly competitive market in terms of medical travel.

No, so I wouldn’t say that the margins are comparatively better than the other verticals, but it helps us complete the service profile of the entire group.

• MANPOWER: So the medical manpower in terms of doctors is available, they are very skilled. The challenge till now was that they did not have access to infrastructure to actually go and operate, the patients using the right kind of equipment. With us doing and putting the infrastructure, these doctors are more than happy to actually come and operate at our facilities. So, in terms of medical doctors, it’s not a challenge.

Nursing and paramedical, technicians or in terms of dialysis or radiology, that is a challenge to some extent. And for that, we have Indians who are positioned in these departments out there. In these particular departments, it’s not a very big challenge, because when the piece is way better than what they’re making in India, you’re able to, get these people to relocate.

So, local manpower, whatever my cost is, eventually if I’m to take an Indian manpower, it’s going to cost me upwards of twice that particular expenditure and that is one reason why over the years, after the first three years, we focus a lot on skill development and shift these from having expatriates to having locals. So, we’ve created that entire bunch of local manpower also, but it cannot be 100% because there are certain technical aspects which we cannot rely upon when it comes to local manpower as yet. Certain high investment related equipment like CT scan and MRI, I will need a technician from India. As a company, we are more safe and secure in terms of the overall handling of that equipment. So, yes, I mean, both we have observed – both aspects of the question now.

• For example, in Uganda, like you rightly mentioned, the insurance coverage is very minimum. So, you do not have a lot of people on insurance, the government itself does not have a National Health Insurance Scheme like a lot of other countries. So, the, the patient profile shifts from insurance to a lot of corporate. When I say corporate, it is like, for example, the Ugandan military, the entire payment is made by the Ministry of Defence, the United Nations beneficiaries that those patients are paid for by either UN directly or by the international insurance that the United Nations have taken, like, for example, Cigna. And there is a small proportion of private insurance companies or regional insurance companies, which make payments.

So, for us at our hospital, it is a mix of all of this. 25% to 30% of the contribution is from cash patients, about 70% of the contribution is from credit patients or these kinds of corporate clients, of which some of them are backed by the government, for example, the Ugandan military, eventually it’s the Ministry of Defence, which is part of the government.

• VHL commissioned its operations as UMC Victoria Hospital in January 2017 and achieved operational breakeven in FY 2018-19, within 24 months of commissioning services of the hospital facility.

•

DISCLOSURE: Invested @159