+1. For the same reason I avoided this company.

Disc: Not invested. But tracking since last 6 months.

1 Like

For FY 22-23, the company’s auditors are G.P. Kapadia & Co. It is a very reputable CA firm and we can trust that the financial statements are genuine.

Remember PWC was auditor of Satyam Computers! However strong auditors are, there are limitations. They depend on data provided by company. I’m by nature a bit skeptical about these kind of things ![]()

Look at these these disclaimers by the auditor:

Who audited their subsidiaries??? ![]()

So now whom we depend upon? on management- who are they? I couldn’t find enough on them, their history or on their family/credibility!

The only variable basis which now I can mitigate this risk is “time”. So i’ve to see their performance for next few quarters/years.

1 Like

As far as I know both of them are doctors and are first generation businessmen who are in their mid 30s and started this business originally medical tourism consultant in Africa when they were quite young.

1 Like

H1FY25:

• Revenue growth: 10.5%. EBITDA growth: 20% - EBITDA margins: 37.2%. PAT growth: 23%

Borrowings reduced to 10.23cr vs 15cr in March 24. (Net cash levels similar)

Operating cash flows of 5.76cr (7cr for FY24 full year)

• The Company, via UMC Hospitals Private Limited, intends to add a capacity of 150 to 250 commissioned beds across one or more tertiary care hospitals in India under its operational management in the coming 24-36 months. In line with the Company’s proposed plans to establish a pan-African presence and expand its existing bed capacity across Africa from 200 tertiary care beds to more than 500 commissioned beds in the coming 36 months, the Company had incorporated a wholly owned subsidiary, Unihealth Holdings Limited, in Mauritius. The said subsidiary intends to make investments to acquire as well as invest into setting up of facilities in line with the Company’s vision and growth plans, in key target countries of Africa.

• Looking forward, we’re ambitious about our expansion plans, which include the development of over 1,000 tertiary care hospital beds across Africa and India and the establishment of more than 25 UniHealth Medical and Diagnostic Centres

•

(Consultancy revenues have dipped for current HY)

•

•

CONCALL NOTES:

• EBITDA MARGINS DETAILS AND GUIDANCE: Operational efficiency contributed significantly to the increased EBITDA margin at both the hospitals. On a ground level as the revenues increase, in the hospital industry, the fixed costs to a large extent are capped at a particular break-even point. Beyond that, any growth in revenue usually translates into a higher margin because your cost towards employees, your cost towards the utilities or infrastructure is unlikely to increase in the same proportion.

Going forward, Existing operations might still witness another 1%-1.5% of growth as revenues increase. But on a consolidated basis, as we move towards an expansion mode where we will be adding on significant bed capacity in the coming 6 to 24 months as we inch towards our intended 1,000 beds, all the new addition might be at a lower EBITDA during the first 12 to 18 months while we build on the operations for those facilities. So, on a consolidated level, going forward, either we will be maintaining this EBITDA, or the EBITDA margins are likely to come down by a couple of percentage points while the overall revenues and EBITDA in real absolute numbers will increase considerably as we add on additional beds that we intend to do so.

• NEW FACILITIES/CAPACITY EXPANSION: Company is in advanced discussions for a couple of facilities, which we aim to conclude before the end of this financial year, in a sense that these facilities should be commissioned and operational in the last quarter of the ongoing financial year. We are quite confident of adding another 100 beds to the existing capacity of 200. This is equally positioned in India and Africa. So, for this financial year, we will be adding a 50- bed strength in India and a 50-bed capacity in Africa. Both these are completely new set-ups that we are having for the 50-bed in India. It’s going to be our first facility in India and the other 50-bed that we are looking at is in Tanzania. So, the India one is a pure Greenfield. Tanzania, we have got ongoing discussions with two different facilities. One is a sort of acquisition, and the other one is relatively, I wouldn’t say a clear Greenfield, but it’s midway, where we will be entering, but it does not have an established revenue stream right now. Once we enter, post that, that commissioning phase will happen. So, the turnaround time will be smaller compared to a standard Greenfield, but it does not have an existing top line to contribute to the group on an immediate basis.

We will be increasing the beds in by about 50% by the end of this ongoing fiscal. From the 300 beds that we aim to have before the end of this fiscal, we will be adding another 250 to 300 beds in the next financial year. So, those discussions have also been initiated by the management. Hopefully, very soon we will be in a position to share significant details with all the stakeholders.

INDIA EXPANSION: India is right up there on the management’s focus of the additional capacity that we intend to plan in the coming 3 years. As we grow from a 200-bed strength to a 1,000-bed strength, we will be looking at developing a portfolio of at least 400 to 500 beds in India. The first target for us as we inch towards the 1,000-bed capacity would be to have at least a 400-bed capacity across 4 to 5 facilities in India. So, every single facility that we will be looking at in India is going to be in the range of 50 to 125 beds. That’s the ideal bed strength that we will be looking at as an individual facility in India. So, in the coming 3 years, we will be looking at setting up 5 to 6 facilities with a combined bed strength approximately around 400 beds in India.

NIGERIA EXPANSION: When it comes to Nigeria right now, our presence is in Northern Nigeria in Kano. So, as the first step, we are exploring Lagos, which is the commercial capital of the country and Abuja, which is the political capital of Nigeria. Both those are locations where we can put up a 50 to 75 bed hospitals. We have already started the process to identify the right property for this expansion. That will be step one, which will allow us to provide access to a larger population base of the country to our services.

In Nigeria, we are now looking at expanding our presence by establishing facilities in Lagos and Abuja. So, the bed strength from 80 bed capacity, we are inching towards the 200-bed capacity in the coming 12 to 36 months, as in when the right opportunity comes in.

TANZANIA EXPANSION: The idea is in the coming 2.5, 3 years to have an established bed strength of about 200 to 250 beds in Tanzania across 3 to 4 cities of the country that we are exploring opportunities in. These include the commercial capital that is Dar es Salaam, Mwanza, which is in the Lake region and the second largest and most populated city after Dar es Salaam. Then the other two cities under consideration are the political capital of the country Dodoma and a city called Arusha, which is basically the gateway to all the tourist attractions of the country. So, these four geographies we have earmarked to explore opportunities to set up a bed capacity of about 200 to 250 beds in Tanzania.

• For the next year, there is another 300-bed capacity. For that, you may need a fund, which will call for a fundraising exercise. Akshay Parmar: Quite possibly, it depends upon, so we have got multiple discussions ongoing, both in India and Africa. Some of them may need some additional funding in terms of an acquisition. Some are more on the O&M aspects, where we will be taking those facilities on a long-term lease or come operational contracts. So, out there, the requirement is more so towards the funding of equipment purchase and operational capital, which we have the liberty to access bank debts as well. So, in that case, we may not need to go back to the public for a fund raise for those particular projects. So, it is going to be a mix and the clear idea will be available only by the last quarter of this financial year.

• NAME CHANGE TO UNIHEALTH HOSPITALS LTD: As a management, what the benefit that we foresee in the coming period is that we get better grouped under the healthcare category with the right kind of peers for the public stakeholders. So, there may be a lot of individual stakeholders where that dilemma, whether we are a hospital group or whether we are consultants to the hospitals does arise because of the name. Once we get grouped, typically if we look at the average PE multiple at which the healthcare industry, I mean the hospital industry right now is creating, that average PE is upwards of 50. So, as management, we do feel that by getting it under the right grouping, there is a possibility that the stakeholders will start viewing the company from a different perspective as well.

• MEDICAL TRAVEL DIVISION: We have re-entered the space earlier last year and going forward, the thought process is with hospitals across critical African countries and hospitals in India, it will become something which is going to be purely internal where we are going to achieve way better margins and provide way better services to our patients. So, a patient from a UMC Hospital in Nigeria will have the liberty to undergo treatment at UMC Hospital in India. For the group, it will improvise upon the margins. So, that is one of the arenas that we are looking at. It also helps us with a lot of corporate contracts that we have in these countries, clients like the United Nations, clients like the Ugandan military and defense forces. So, for them, it becomes a seamless experience because then they are not referring to a third party. They are referring to us as UMC Hospitals Group. So, the potential for us to increase that business becomes a reality when it is purely internal. So, from medical value travel, that is one major advantage that we are looking at. Then coming to geographies where UMC Hospitals do not have a presence. Since it has been the oldest vertical for the company, we have the expertise, we have the facilities and capacity with the management, and we have already started sequentially targeting some of those countries also, where traditionally we were receiving a lot of patients from. So, earlier, the margin for such a business would vary between 15% to 20% on a gross basis. But now with UMC Hospitals being one of the front runners for getting that patient base into India, and those patients will effectively be treated at one of the UMC Hospitals facilities in India, that margin will nearly double up. So, then we will be looking at a 40% plus margin on the same business that earlier would fetch us about 15% to 20%.

• Kenya and Ethiopia are two geographies that we are keenly looking at and exploring opportunities

• GROWTH GUIDANCE: What we witnessed in terms of percentage points for the first half, we are going to have a similar pattern for the second half, maybe a slightly better one because there are certain areas in terms of consultancy services where usually the second half of the year does much better than the first half for us on a historic basis. The same goes for the profits as well. The margins are likely to remain the same or witness a small increase in the second half of the year. So, by the end of the year, we will be maintaining the current growth rate or bettering it by a little.

• SYRINGE FACILITY: The construction of the entire structure has been completed. The equipment orders will now be placed with the target that they are all in place on site by the end of the financial year. We are targeting June 2025 for production to begin.

• We are looking at about 8 to 10 medical centers in the coming 18 months in Uganda, in the periphery of Kampala. So, anywhere in the radius of what two to three hours of drivable distance from the hospital that we already have. So, these will allow us a twofold benefit. One, it will allow us to provide services at a lower cost to the underserved population of the country. So, compared to the hospital, these centers will be better priced in terms of the economics. Second, these will also act as feeders or as spokes for the hospital where patients who need surgical intervention, who need intensive care services can then be referred to the main hospital in Kampala. So, that will also allow us to benefit from these kinds of references from within the network itself. So, this is the way forward that we are looking at Uganda.

• Some of these countries have a very good national health insurance already in place, like Tanzania, like Kenya. Countries like Uganda are in the process of establishing a national health insurance scheme. So, the Parliament has already passed the bill. The execution modality is underway, which might take maybe a year or two years more. But once that happens, a much larger population would be under the ambit of healthcare services, access to healthcare. So, from that perspective, being there or having a presence itself will allow us to benefit from the growth that the overall sector is likely to witness.

• MOBILE APP: In the coming six months, we are going to be looking at investing some amount into developing the technological aspect of the company to extend our services to a larger footprint or a larger audience via mobile apps. So, that is something that is a strategic investment that we will be making in the coming two quarters, so that by the time we start commissioning the additional bed capacity that we aim to, we have got this backend absolutely well-defined and ready to roll out.

• We have been tracking the healthcare sector and the industry in Kenya and key geographies in Kenya for us that are on the watch list include Nairobi, which is the capital city, include the port city of Mombasa and smaller places like Kisumu and Kakamega and Eldoret. So, these are the 5 cities and towns in Kenya that we have been tracking for the right opportunity to come to us.

• MANAGEMENT MINDSET ON MANPOWER AND QUALITY OF SERVICE: As a private company we started small, and both the promoters are from the field in terms that both of them are doctors. We have the educational background. So, that allowed us to create very, what you call, robust SOPs, protocols that have been put in place. Dr. Anurag relocated to Uganda from the same perspective that once we had a facility which was our flagship facility way back in 2016-17, we wanted to have some feet on ground which would ensure that all the protocols are implemented, and the quality perspective is well catered too. So, today for us luckily at UniHealth, we have got a very good bench strength of key senior managers and executives who have been trained and who have been working with us since a good number of years in different roles and capabilities and capacities. And they are the ones who will be spearheading the expansion as we take it forward.

Lastly, what is also critically important as we grow is that the manpower that joins the company sticks to it. And I am very happy to share with everyone on the call that for us the attrition rate has been extremely low. We have never had in the last 10 years any senior executive actually leave the company. Whatever attrition that we experience is primarily from our hospitals in Uganda and Nigeria at the entry point level, that is the nurses or the office boys or the technicians. We never really had any senior doctors or management people leave the company over the last 10 to 12 years of our existence. I mean, 14 years, but a lot of them have joined just about 10 years back. So, from that perspective, this also plays an important role in the work culture at UniHealth and will be extremely supportive of the growth that the company undertakes, because that is the time when this will be put to the real test.

So, for our Indian operations, very recently we have had Mr. Saurav Chatterjee join us as the Head of Operations. He has been a veteran in the industry, having worked with Fortis, having worked with Apollo, having worked with Wockhardt and having worked for about a decade or more with Aditya Birla Hospital in Pune in various leadership positions and roles. So, again, out here, the manpower plays a very, very important role.

• OPERTIONAL EFFECIENCY DETAILS: One important aspect was better management of the cost of inventory. So, over a period of time, especially post the tapping into the capital markets and having access to funds, we have been able to plan our exports from India in a much better and a streamlined manner, which has allowed us to reduce procurement locally for a lot of consumables where the pricing parameters are significantly different. So, we have been able to reduce our cost of inventory, which has added to our margins.

The second is that with access to capital, we have been able to plow in a significantly higher working capital in Uganda and tap into a lot of business that we had to earlier forego because of limited access to the funds. Now, what that has done is it has allowed us to increase our top line. And lastly, we have invested into developing certain Centers of Excellence like orthopedics, spine. We are focusing on minimally invasive procedures at laparoscopic surgery, which are higher margin procedures. We have got Indian doctors who are traveling every six to eight weeks to either of our facilities. And that has allowed us to increase our revenues at a much better margin in comparison to the same procedures being done by local doctors. So, that has also added to the increase in the EBITDA and PAT margin.

• RELATIONSHIP WITH LOCAL COMPETITORS AND DOCTORS AND GOVERNMENT: So, all these countries are fairly small in terms of the industry where we have got a very robust mechanisms of interdependency. Because we have very few private players in the industry out there in terms of hospitals. More than being competitors, we are sort of partners in the industry where we do lean on each other. So, there are times when we refer our patients to them when a particular service is down for maintenance in our facility. For example, an MRI machine or CT scan machine for maintenance may be down for a few days, a couple of days or maybe a little more in case any service part needs to be replaced. At that time, we refer patients to them and simultaneously they do and reciprocate the same way when their systems are down. Secondly, what happens is that we are the largest in both the sectors that we are there, in Uganda in the private sector and in Northern Nigeria in the private sector. We also have the largest intensive care facility. We have got modular theaters. So, many times, a lot of these smaller facilities that are there, they refer patients to us so that their patients can get access to the ICUs or their patients can get access to certain minimally invasive procedures that we are undertaking. So, it is a very healthy relationship that we have with a lot of local service providers in terms of the hospitals in these countries.

When it comes to doctors, a lot of local doctors are on an honorary basis. They are honorary consultants. So, they practice at our facility. They also practice at other facilities. So, they are not bound, but once they have been used to our way of functioning, a majority of them end up practicing for 70% to 75% of their time and patient base at our facility because of the infrastructure that we have created and the support system that they have in terms of a lot of facilities and access to a lot of inventory items, which otherwise sometimes are difficult to get in smaller setups in these countries. So, that is the way that we have been liaising and networking and cooperating with the healthcare providers.

When it comes to government, again, we have a very good way of liaising with the government. We are constantly in touch with different departments. We provide our services to a lot of departments, and we are also very forthcoming in sponsoring healthcare services for a lot of events that some of these departments have. For example, when the Sports Ministry undertakes any sports activities in Uganda, we are more than happy to extend our ambulances and a small clinical team to be present on ground on a pro bono basis. Similar activities we undertake in collaboration with the Rotary, where we take part in organized cancer runs to create awareness. Similarly, in Kano also, we extend our services to the airport authorities, to the police force of the city. So, by doing these activities and extending our facilities and services to them, we have been able to create an extremely good rapport with the different government departments out there.

THINGS TO TRACK:

-

ADDITION OF FACILITIES AND THEIR PERFORMANCE

-

PROGRESS IN INDIAN MARKET: Can they replicate their success of African markets in Indian markets as market dynamics are very different between the two? What will be the EBITDA margins of Indian operations?

-

SYRINGE FACILITY PROGRESS

-

CONSULTANCY DIVISION PERFORMANCE

-

CURRENCIES OF NIGERIA AND UGANDA

4 Likes

UMC Hospitals Group announces its First

Multi-Specialty Hospital in India.

https://nsearchives.nseindia.com/corporate/UNIHEALTH_07012025155038_Cvandpressrelease_merged.pdf

Got a couple of questions

1.- They claim many Indian hospital chains tried to enter African markets but were unable to do so. What was the reason? What did the big companies lack that this small company can exploit and use it to its own advantage?

2. They claim they can reduce their costs on inventory and equipment as compared to others by exporting from India. I did not understand this. Why can’t their competitors do the same and exploit the same advantage?

3 Likes

-

Management has significant knowledge of the African markets, also they have tie-up with local partners in all their hospitals which helps them with administrative and other matters.

-

Costs are just mostly a case of sourcing items from lower/lowest supplier which in this case is mostly from India most of which is via trading but they are now in the process of setting up disposable injections facility in Tanzania thus moving up from trading gradually based on market opportunities.

*views expressed are from my limited understanding of the company and whatever little i have researched and read online.

Disclosure: No positions but tracking

2 Likes

Good results

2 Likes

Dear Pranav Ji Appreciate the detailed analysis and follow through. Observed the following

- Entry barriers: Biggest advantage is the country of operation where there are hardly any players (which is also the biggest risk). The business verticals are all part of the value chain which when combined with the location results in an integrated operation with solid moat and makes it even more difficult to be replicated. Therefore full marks for the establishing a moat which can be sustained unless there is any political/administrative risk in the country

- Hence my curiosity to understand why the cash flows are so weak. Even with high TAT for payments over 5 years Operating Cash/Operating Profit: 24% very low. Need to be watchful year as there is a claim that payments are invariably closed but financials tell a different story

- The other question is why they want to expand in India when they know Africa so well. Why there is no plan to expand in other African countries with same set of competitive advantages

- Growth plans of 1200 + beds provides managements desire to expand by 6X. We need to study how much contribution from. Currently the plan is 50:50. Will the India business sustain the EBITDA margins. In this case it is not behaving like Caplin and changing is its business model. Why ? Is there a threat to the Africa growth story. Or are they very aggressive.

- India: Asset Light model. Looking at branded play in 50-125 bed segment (much like lemon tree hotel). What gives them the right to win in this segment. This is a price sensitive segment and only the player with lowest cost structure off course without compromise on service wins

Pls pardon my ignorance to any previous discussion on the points mentioned

3 Likes

H2FY25:

•

•

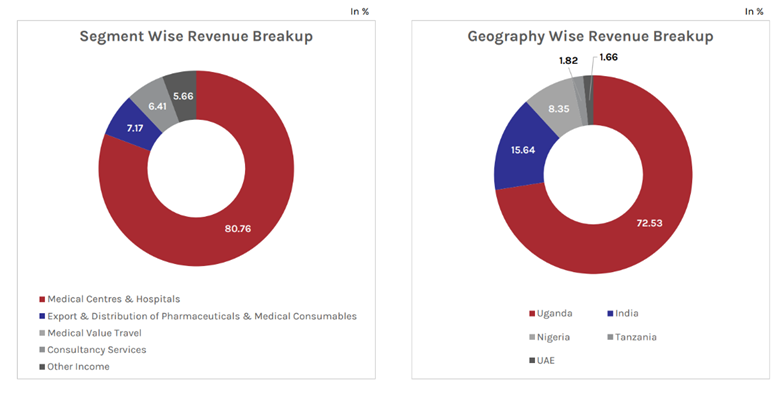

• In FY25, the company reported the following segmental revenue distribution:

Hospitals & Medical Centres: 48.01 Cr (37.9 last year)

Consultancy Services: 2.52 Cr (8.17 last year)

Exports & Distribution: 5.06 Cr (2.69 last year)

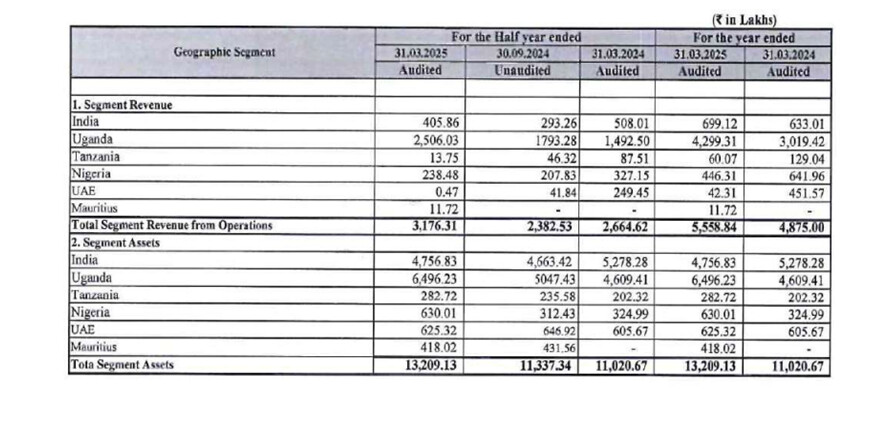

• Geographically, Uganda was the largest contributor with 74.45% of total revenue. India followed with a contribution of 15.81%. Nigeria accounted for 7.71% of the total revenue. Tanzania contributed 1.10%, while UAE and Mauritius contributed 0.73% and 0.20%, respectively.

• Operational Performance:

Average Bed Occupancy Rate: 58%

Annual Procedures Performed: 1,700+ (1250+ last year). Treats 1,31,850+ Patients Annually (110,000+ last year)

Beds Under Consultancy Services: 1,300+ beds across multiple locations (1200+ last year)

• Our multi-specialty tertiary care hospital in Navi Mumbai is progressing well and will be operational soon.

UniHealth - UMC Hospitals Group marks its India foray with a 60-bed tertiary care hospital in Navi Mumbai, set to open by July 2025, as part of its broader plan to establish 5+ hospitals in western India and strengthen India-Africa healthcare collaboration.

Key Facility Highlights:

- Advanced ICU & modular operating rooms

- Cardiac Cath Lab & specialized daycare unit

- Comprehensive lab & radiology diagnostics

• Besides Navi Mumbai, expansions in Nashik and Pune are advancing, expected to add over 500 beds in next two years.

This will result in Strengthening medical value travel between UMC Hospitals in Africa & India

• Our asset-light strategy targets 1,000 new beds over three years.

• To expand our outreach and ensure increased accessibility to quality care, we have also commissioned the first UMC Clinic in Kyanja, Uganda. We aim to expand our network of clinics by adding another 4-5 clinics during this fiscal.

• We will soon commission a 20- bedded secondary care facility in Mwanza, Tanzania.

•

•

(Big decline in EBITDA margins Yoy) (Due to elevated power costs and shortages)

CONCALL NOTES:

• The addition of key super specialties helped the revenues and profitability of our hospitals improve.

• Our broader objective remains clear. To establish a connected network of mid-sized, high performing hospitals that bridge the gap between affordability and clinical excellence.

We continue to see a steady rise in demand for well-structured, mid-sized healthcare facilities, especially in underserved urban and semi-urban areas.

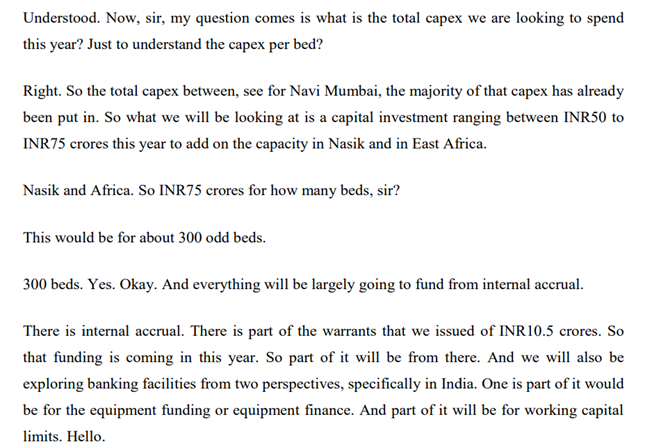

• INDIA BUSINESS:

STRATEGY IN INDIA AND HOW UNIHEALTH PLANS TO DIFFERENTIATE ITSELF AGAINST COMPETITION:

• NASHIK HOSPITAL:

Nashik Hospital to be commissioned by December or January 2025-26

• REVENUE GEOGRAPHICAL DIVERSIFICATION GOING FORWARD:

• Uganda company is likely to go debt free in a couple of months from now, when it comes to banking debt.

• CAPITAL INFUSION GOING FORWARD IF NEEDED: So, the ideal way forward for that would be a mixture of three, which is the promoters infusing their own capital to the best of their ability and capacity, a preferential allotment or going back to the public for a part of that fundraise and maybe looking at some amount of debt as well, since on a consolidated basis, the books are significantly strong when it comes to debt. There’s barely any banking debt that the company has at present. So, it can leverage its strength to raise some amount of that funding via debt as well.

• CONSULTANCY VERTICAL: Now, it is extremely difficult to pinpoint a standard growth pattern for the consultancy division because there might be years where we get a million dollars’ worth of revenue and there might be years where we just do about $300,000, $200,000 because these project cycles can take a long tenure in terms of their planning and execution and revenue realization is also staggered.

Like compared to last year, where we were catering our services to a consolidated bed strength of about 1,250 beds, the project that we are having right now and providing services to exceed 1,300 beds. So, in all the number of projects and the bed capacity have increased, but the revenue realization in this particular financial year has come down significantly. Now we expect that revenue realization to increase in the coming 2 years, because that is how those projects are planned out in terms of the project cycle. And that is where our deliverables are going to be significant and the, invoicing is going to be accordingly to that. So, for consultancy, we always put it across that it is the cream and the cherry on the cake. I do not take that factor into any revenue projections or growth projections that we have.

• DISTRIBUTION VERTICAL: We’ve got another associate entity out there, UniHealth Uganda Limited, which acts as an importer and distributor of a variety of pharmaceutical and medical consumables specifically for the Ugandan market. So, again, that is an entity where we expect the top line and bottom line to grow decently in the coming two years because a lot of products are getting registered at present. We have completed the registration of the manufacturing facility of Reliance Life Sciences of whom we use for Uganda and we are now moving on to the registration of the individual products. Similarly, we are in the same process for few other companies as with that portfolio growing in the coming 12 to 24 months, we do look forward to an incremental revenue and profitability from the distribution division.

• NIGERIA BUSINESS – LOOKING TO MOVE OUT FROM NIGERIA:

There is a direct flight connectivity connecting Mumbai with all these countries in East Africa, whether it’s Ethiopia, Kenya, Tanzania or Uganda, allowing us to ensure that our management team and our doctors can make a quick dash to these countries, perform their procedures, conduct OPDs and come back. And the travel time is still only 5.5 hours.

• TANZANIA BUSINESS:

• AVERAGE REVENUE PER BED AND TARGET FOR THE SAME:

• ASSET LIGHT STRATEGY IN INDIA:

• Consultancy business can generate 50-60% margins depending on revenue increase whereas hospital business would be generating 30-35% EBITDA margins

• BED ADDITION PLAN:

• WHY MARGINS ARE HIGH IN UGANDA BUSINESS:

• GREENFIELD VS BROWNFIELD CAPEX:

• WHY RECIEVABLES ARE HIGH:

• FUNDING THE EXPANSION:

• Pune facility is under discussion. Commissioning will probably happen at the start of the next financial year.

• TOTAL CAPEX THIS YEAR:

THINGS TO TRACK:

• ADDITION OF FACILITIES AND THEIR PERFORMANCE

• PROGRESS IN INDIAN MARKET: Can they replicate their success of African markets in Indian markets as market dynamics are very different between the two? What will be the EBITDA margins of Indian operations?

• CONSULTANCY DIVISION PERFORMANCE

• CURRENCIES OF NIGERIA AND UGANDA

• CASH FLOWS

• UGANDA FACILITY GROWTH RATE: As IVF and other superspecialities have commenced, can it accelerate growth along with better cash flows?

1 Like

The thesis has evolved and changed from what it was originally

Company is now at a inflection point

It’s going to expand in India (targeting 50% sales from india in 3 years)

It’s pulling out of Nigeria (due to constant currency depreciation and power shortage crises)

Expanding in Tanzania

Consultancy division is going well

Distribution to do even better going ahead as more products are Registered

Uganda business is it’s crown jewel. It’s the big moat business. And with IVF and other super speciality services added, it’s going to keep getting better

So, how it does in India, which is a different market than africa and has lots of competition, will make or break the thesis over the medium-long term.

It may not succeed in india (But mature African business will provide cushioning to that failure)

But if it succeeds, then we’ll have entry at the ground floor to a hospital business in india..and that over the long term might prove EXTREMELY LUCRATIVE.

Management is Very intelligent and knowledgeable. So there’s that positive.

Margin of safety is present in terms of earnings going forward. Even if india business doesn’t take off, African (Uganda) business will keep on generating earnings, so earnings degrowth will not happen.Giving us safety net on the downside. If India business doesn’t scale / perform over next 2 years, we can then get out. If it performs, then we can add more shares and hold for a very long time as a compounder

3 Likes

And in terms of cash flows, There hasnt been a single bad debt written off over the last two years and management has also said in a previous concall that there hasn’t been a single time where payment didnt come in Uganda.

They build their pricing of their services such that it accounts for the 9-10 month receivable timeline.

But yes, it will be important to monitor cash flows going forward

2 Likes

I did some research to find that in Kenya Apollo, Narayana, Medanta have established operations and also facilitating medical tourism. Apollo also has operations in Tanzania. These are in partnerships with some other players. If somebody can provide more information then pls share. Though while doing research it also came out that although many players are operating in Kenya they have not expanded in other countries due to Political and Economic Risk, Healthcare affordability, lack of established medical insurance policy, unstable electric power. This leads me to a conclusion that further growth in Africa is limited beyond few countries and therefore Unihealth is expanding in India (Corroborated through their latest concall discussion)

4 Likes

Here is segment data

| Segment | FY21 | FY22 | FY23 | FY24 | FY25 | CAGR 4Y | CAGR 3Y | YOY |

|---|---|---|---|---|---|---|---|---|

| Hospitals | 25.59 | 34.37 | 38.68 | 37.9 | 48.01 | 17% | 12% | 27% |

| Distribution of Pharmaceuticals | 1.38 | 0.29 | 2.69 | 5.06 | 54% | 88% | ||

| Consultancy Services | 0.6167 | 1.08 | 4.97 | 8.17 | 2.52 | 42% | 33% | -69% |

| Other Income | 2.4273 | 1.09 | 2.09 | 1.59 | 2.82 | 4% | 37% | 77% |

I totally exited the stock during curent rise and i shifted my position slowly to NH.

My thesis for exit was

- my high entry point at 155 level. (Valuation was not justifiable)

2.Better opportunity in NH in terms of Valuation, business model,capital light model

3.Too many businesses (hospitals in latin America, consultancy in india,and now planning hospitals in India.

I may be wrong.

4 Likes

ANNUAL REPORT FY25 NOTES:

• 150+ Doctors & Specialists (Same as last FY)

130,000 + Patients Treated Annually (110,000 in FY24)

1,700+ Annual Procedures done (1250+ last FY)

1,300 Beds in Projects under Consultancy (1200+ in FY24)

• The company has exited its operations in Nigeria.

Nigeria accounted for close to 8% of FY25 sales and 7% of PAT

• From our origins as a pioneering medical value travel company, we have evolved into a diversified healthcare platform spanning hospitals, medical centres, consultancy services, and pharmaceutical distribution. Today, our presence extends across East Africa and, with our strategic entry into India, we are well on course to achieve our medium-term target of 1,000 commissioned beds.

• India’s Healthcare Opportunity - In Tier 2 and Tier 3 cities, quality and capacity gaps remain significant. Our strategy is to bridge these gaps with an asset-light, partnership-driven, tech enabled model that blends clinical excellence with operational efficiency.

• Strategic Growth in India: In Phase 1 of our India plan, we are building a robust presence in Maharashtra’s “Golden Triangle” — Mumbai, Pune, and Nashik. Our 50-bed Navi Mumbai hospital is nearing launch, our 200-bed flagship in Nashik is progressing at speed, and we are evaluating a new unit in Pune. Together, these will add 500 beds in India in the coming 24 months, forming the backbone of our domestic network.

• Integrated Model Creating Value:

Our four synergistic verticals create a resilient ecosystem –

» Hospitals anchor our service portfolio and deliver scale

» Medical centres extend our reach into high-demand catchments.

» Consultancy builds market credibility and long-term client ties.

» Pharmaceutical distribution lowers costs and generates high-margin revenue

This model enhances patient referrals, optimises margins, and balances revenues across geographies.

• We have been able to reduce our debt considerably and aim to become debt-free in our existing businesses by the end of FY 2025-26.

This will allow us to further strengthen our balance sheet and explore debt-funding opportunities for our new projects, maintaining fiscal prudence as we move towards a phase of rapid expansion in the coming few years

• Uganda remained our largest market, contributing 74% of total revenue, but with our expansion in India and Tanzania, our geographic mix will become more balanced in the next 24 months.

• We are not building for the short term. Our Africa strategy is focused on expanding by 400–500 new beds through a balanced mix of greenfield projects and strategic partnerships.

• Alongside infrastructure, we are prioritising the development of centres of excellence in orthopedics, ophthalmology, cardiology, oncology, critical care, and diagnostics — specialties where the demand is rising but capacity remains inadequate. Importantly, we are also investing in training programs that nurture local talent, ensuring long-term sustainability and reducing dependence on external expertise.

• Our experience in resource-constrained African settings equips us to scale in India with discipline, while the advanced systems in India bring fresh perspectives to our African network. Together, these reinforce UniHealth’s vision of becoming a truly global, integrated healthcare platform.

•

• The percentage increase in the average remuneration of employees in the financial year: 81.47%

The number of permanent employees on the rolls of Company: 21 (vs 17 last FY)

• Set to commission facilities in Mwanza (Tanzania), Navi Mumbai & Nashik (India) during FY 2025-26, adding nearly 300 beds to its commissioned strength. In addition, addition of another 100 beds in Tanzania is presently under consideration.

• Outlook – Africa: UMC Victoria Hospital in Kampala remains the flagship private tertiary care hospital, with recent upgrades in orthopedics, spine, IVF, and planned ophthalmology services. UniHealth is expanding its presence with 8–10 spoke clinics in Uganda and a 20-bedded secondary facility in Mwanza, Tanzania. Advanced discussions are underway for a 100-bedded tertiary hospital in Dar es Salaam, supported by a 40,000 sq. ft. expansion. By FY25-end, 125–150 new beds are expected to be added across Africa.

• Outlook – India: UniHealth is entering the domestic healthcare delivery space through Maharashtra’s golden triangle (Mumbai–Pune–Nashik). The 50-bedded Navi Mumbai hospital is scheduled to be commissioned in September 2025, followed by a 175–200 bed facility in Nashik in Q4 of the ongoing FY. Two hospitals in Pune, with a combined bed strength of 250–300 beds are being planned for FY 2026-27. By FY28, India is expected to contribute over half of UniHealth’s targeted 1,000-bed capacity, driven by advanced medical technology and patient-centric care.

• Healthcare Consultancy Outlook: The consultancy division is positioned to deliver integrated solutions from concept to commissioning across India and Africa. Current projects include the development of PHRC Health City as a Deemed to-be-University, having a 650-bedded tertiary care hospital along with a medical teaching facility in Pune, India, and multiple African assignments. Long-term Operations & Management contracts are expected to further strengthen recurring revenues.

• Risks and Concerns:

o The Company operates in multiple geographies, exposing it to diverse regulatory regimes across India and Africa, which increases compliance costs and adds to operational complexity.

o A significant dependence on imported consumables and medical equipment also makes operations vulnerable to foreign exchange volatility, supply chain disruptions, and tariff-related risks.

o Fiscal constraints in several African countries, along with declining donor aid and limited healthcare budgets, may further impact patient affordability and demand.

o Additionally, a high revenue concentration in Uganda continues to be a structural risk, as any economic or regulatory disruption in this market could materially affect overall earnings.

o Execution risks also remain relevant for ongoing and upcoming projects across India and Africa, with potential delays, cost overruns, and shortages of skilled manpower posing challenges.

o Dependence on the availability and retention of qualified doctors, nurses, and other healthcare professionals is a critical factor in talent-scarce and highly competitive markets.

o Rising receivables and increasing working capital requirements could exert pressure on liquidity, despite the Company’s low debt-to-equity position.

o Furthermore, global macroeconomic and geopolitical uncertainties—such as inflationary pressures, currency depreciation, and trade disruptions—may affect patient flows, cost structures, and investment sentiment, underscoring the need for prudent financial and operational risk management.

• Asset-light growth strategy under the Design–Build–Operate and leased-hospital model allows for scalable capacity addition with lower upfront capital investment.

• Strategic partnerships with an increasing number of medical consumable and pharmaceutical manufacturers and tie-ups with international airlines enhance supply chain reliability and patient referral networks.

• Balances Written (Back) – 4.95 lacs vs 1.57 lacs written back in FY24 vs 8.9 lacs written back in FY23

• No Bad debts

• ROI – 9 to 9.5%

•

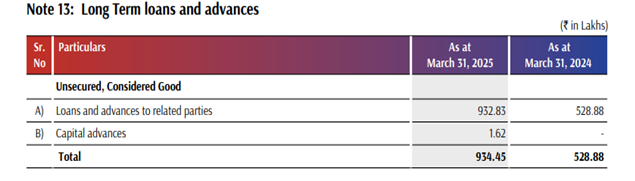

(To subsidiaries and joint ventures)

•

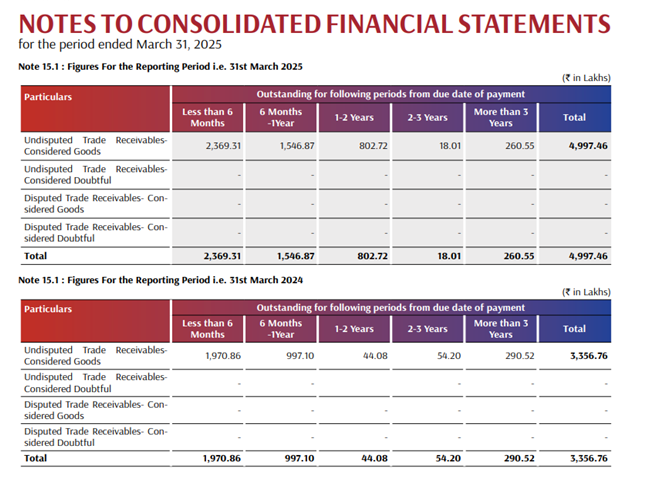

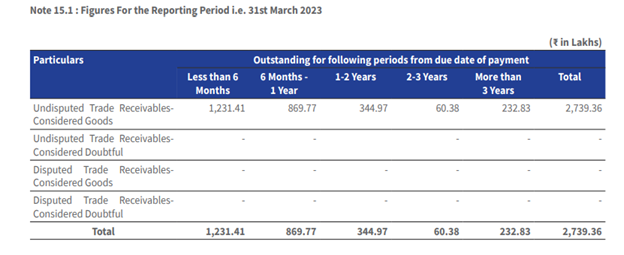

(Deterioration in receivables ageing, though it could be because of increasing sales in Uganda business, as 2023 also had similar 1-2 years duration receivables increase) (Something to keep track of)

•

•

•

•

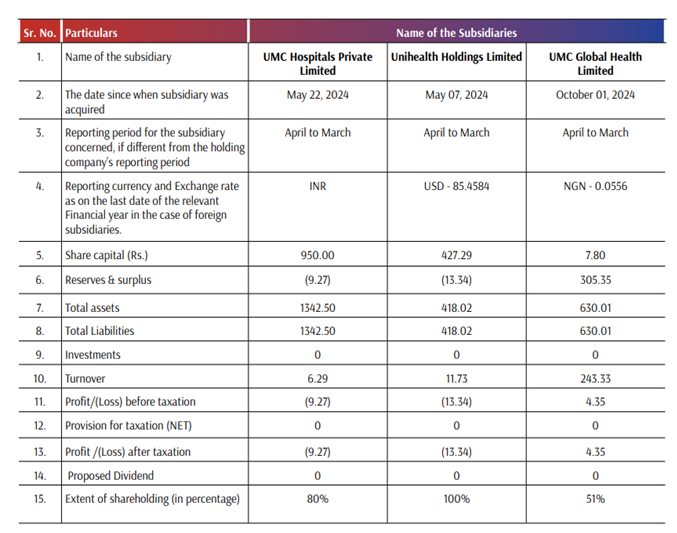

• Dr. Akshay M. Parmar (10% holding) and Dr. Anurag R. Shah (10% holding) in UMC Hospitals Private Limited.

• While Dr. Parmar and Dr. Shah do not hold any shares in UHLM, they collectively hold 10% of the paid-up share capital of UTL.

RED/GREY FLAGS -

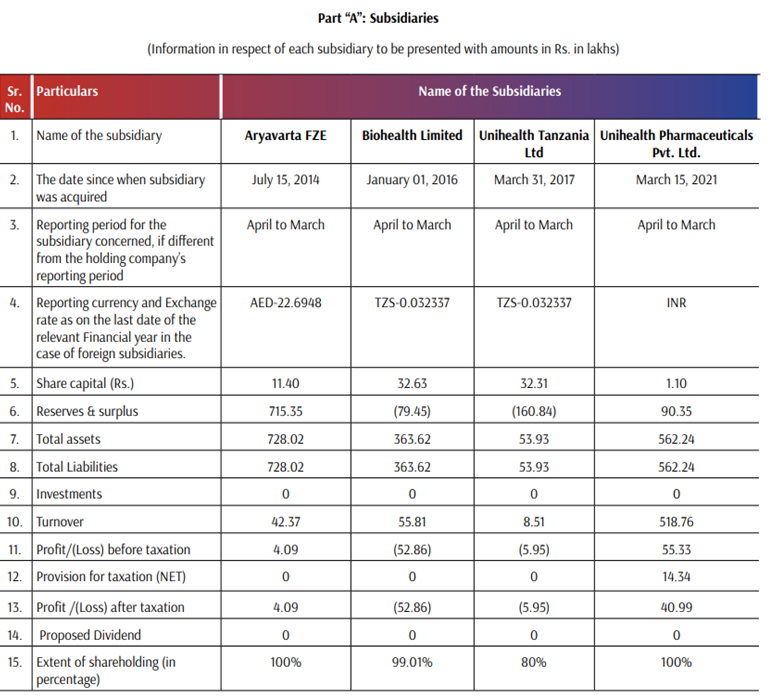

- Promoters are holding 10-10% (total 20%) stake in both Subsidiaries UMC Private hospitals ltd (Where India hospitals would be set) and UMC Tanzania ltd (Where Tanzania hospitals would be set). The parent company is funding their capex through loans and corporate guarantess. So, why not make 100% subsidiaries? Are promoters bringing same amount of capital to subsidiaries?

(The remuneration of management is not much. So, is this the way they pay themselves? or could there be any other reason for it?)

- Deterioration in Receivables ageing. (Though it could be because of increasing sales in Uganda business, as 2023 also had similar 1-2 years duration receivables increase)

There have been no bad debts in last 3 years. On the contrary, there have been balances written back in all 3 years.

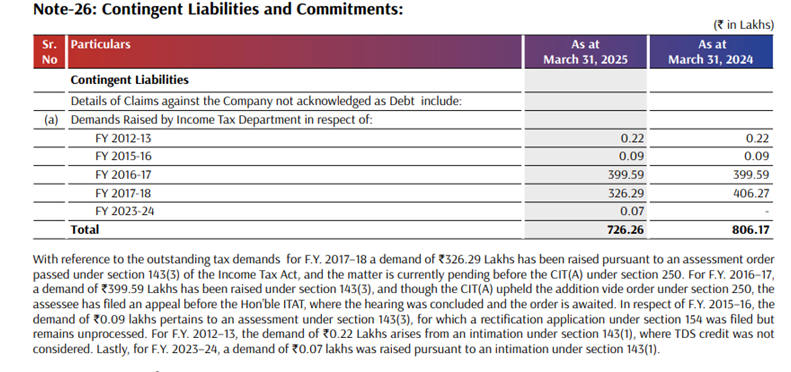

- Contingent tax liabilities

6 Likes

The Unihealth thesis currently stands in a flux. It could be very big or it could be flat/slight degrowth. (Major downside limited due to established mature Uganda Hospital)

They have exited Nigeria operations due to power supply issues and very high currency depreciation.

They’ll now enter India market (which is a very different market in terms of competitive dynamics). How it will pan out, we cannot predict with certainty. Could be a big opportunity if management can execute it.

Tanzania market expansion as well this year.

So, in the near term, there are two opposing factors to earnings

- Uganda business will grow as they’ve commisioned IVF and superspecialities.

- Consultancy vertical will post good numbers at very high margins this year as projects come closer to completion (in FY25, consultancy numbers were subdued)

- Distribution of medicines and consumables will grow as well as product registrations are approved.

whereas

- Newly commissioned Hospitals (beds) in India and Tanzania will take some time to break-even, dragging the earnings down.

Medium to long term trajectory will depend upon how india and Tanzania businesses mature. Could be a huge long term compounder if management is able to execute in India.

Also, receivable situation and promoter taking stakes in subsidiaries needs to be monitored.

Currently trading at 17 pe and 13 EV/EBIT..which i feel captures all these uncertainties.

Balance sheet is also strong currently. (Will have to monitor how they set up funding going ahead for new facilities)

If they scale well, PE re-rating could be substantial as well.

So, will have to evolve the thesis and take any decision on adding/selling shares based on each result going ahead.

Management (from concalls) seem very competent and enterprising and are very young and have scaled the business from 0 to current scale in a matter of 7-8 years. So thats a big positive.

DISCLOSURE- INVESTED

5 Likes

https://nsearchives.nseindia.com/corporate/UNIHEALTH_14112025210943_ilovepdf_merged__1_.pdf

Bumper results , classic case of operating leverage coming into play

3 Likes