Really surprised to see average performance of their HFC book when compared to its peers Aavas, Aptus, Home first, Vastu, Aadhar, AU SFB, Equitas SFB

1 Like

https://twitter.com/OldSchoolFinanc/status/1667426602660278273?s=20

Turned the presentation into a thread.

5 Likes

why does the company have such a low PE?

1 Like

Ujjivan SFB trades at low PE due to higher portion of Microfinance lending and losses due to excess provisioning in FY 2022. Investors are also waiting for reverse merger of Ujjivan FSL with bank which shall increase free float to 100% as against 26% at present for the Bank. This shall open gates for DII, FII to increase allocation to Ujjivan SFB thereby driving PE.

Also bank has not been successful in diversifying into MSME,vehicle loans as compared to Equitas. However Mgmt is trying to fix the policies of lending in these segments. Overall the long term growth story of the bank remains intact.

12 Likes

1st, look at PB and not PE for banking stocks, NBFCs.

2nd, PB is a function of the market’s expectation of how much ROA, growth, and credit cost the business can deliver. Sustainably or cyclically. It will assign lower/higher PB and in turn PE accordingly.

3rd Due to recent events of DEMON, and COVID market over-priced (IMO) risk of default and LGD or risk of ruin to the bank. Now that is getting corrected. In fact, something as big as COVID happened and none of the top 5 MFIs, and SFBs went belly up. Even now the valuations of less than 2x 1yr fwd PB, underestimate (IMO) the length of the good credit + growth cycle due to recency bias. Data from the 2000s suggests longer microfinance cycles if no man-made rare black swans happen.

4th Risk of political interference has significantly reduced as microfinance has been deemed a central subject rather than the state. So local politicians cannot interfere. The market is still not pricing in the recent opening up of Telangana as a market after the 2010s AP crisis. Telangana’s HC ruled that microfinance will be governed by center.

5th IMO, given the ROA, and growth profile when valuations touch 1x 1yr fwd PB, this a very good time to buy. At 2x 1yr fwd PB, these are fairly valued and good to hold. At 3x 1yr fwd PB one should think of reducing position. If any bad news comes one should sell ruthlessly. These are my working, you can build your own DCF model based on PB, BVPS, ROA, ROE and growth to come at a valuation metric.

6th money is made when there are differential expectations between what market prices, what the business delivers and what you can catch before the market prices new expectations.

These are my understanding of the sector and I can be wrong.

Disclosure: Invested in the sector.

20 Likes

Thank you for your insight, much appreciated! I was asking from the assumption that low PE can either demonstrate undervalue, subpar performance or red flags. Haven’t done any looking into the company, but will start doing so. the points you have raised makes it looks like a promising prospect.

I still feel a lot of the traditional ways of thinking (say secured vs unsecured) don’t factor in how much more efficient unsecured lending has become over the years because of multiple layers of India stack & then Account Aggregator.

Today, one can predict the cash flows of a borrower with much more certainty than they could 10 years ago. And this makes a lot of difference in the end NIMs, ROAs, ROEs, etc. etc.

Agreed that Ujjivan, much like other lenders, is focussing on building a secured book, but if NPAs remain fairly within the guided range in the next 2-3 quarters, perhaps a case has to be made for revaluing unsecured lending players in general, factoring in revised risk models.

As for valuations, post the reverse merger, the existing book value will increase by around Rs 2 (guided by the management). Add extra 6 bucks (don’t agree with all research reports out there who are assuming a profit degrowth due to higher provisioning), we get to around Rs 28 as FY24 book value. Assuming a 2xPB exit multiple, we’re looking at 56. Around 30/35% upside from current levels.

Ofcourse, the bank could get further treated depending upon the following key monitorables:- NPA trajectory, diversification into secured lending, reverse merger, and succession of Ittira Davis.

3 Likes

https://www.bseindia.com/xml-data/corpfiling/AttachLive/2cc73014-c3a6-4aba-91e3-69df57e0da65.pdf

Q1 FY 24 results

Highlights:

- Gross loan book at ₹25,326* crore up 30%/5% Y-o-Y/Q-o-Q.

- Deposits at ₹26,660 crore as of Jun’23 up by 45%/4% Y-o-Y/Q-o-Q

-Retail TD grew 71%/8% Q-o-Q/Y-o-Y

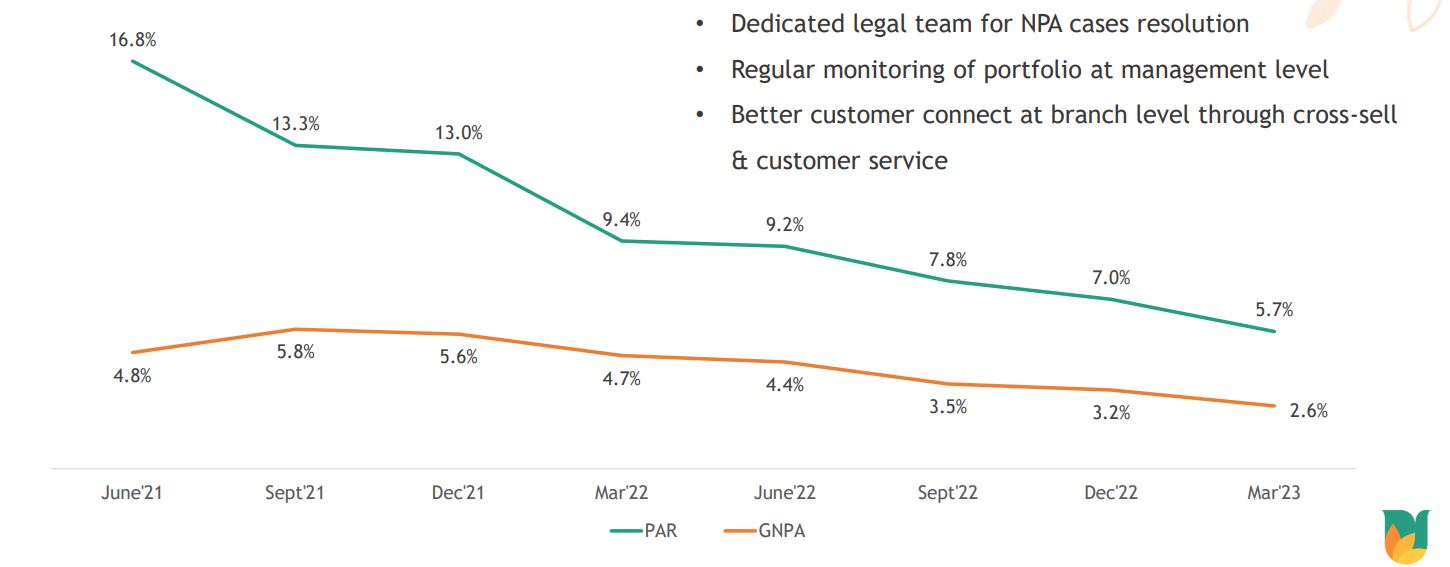

-CASA grew 27% Y-o-Y taking CASA ratio at 24.6% as on Jun’23 - GNPA declined to 2.4% as of Jun’23 vs 2.6% as of Mar’23; NNPA continues to be

negligible at 0.06% as on Jun’23. Provision coverage ratio as on Jun’23 is 97.6%.

Collection efficiency at 99% - Including Floating provisions of INR 250 crore, Total provision on books is INR 845 crore

against GNPA of INR 597 crore. - Cost to Income ratio at 52.8% in Q1FY24 vs 58.5% for Q1FY23.

- Capital adequacy ratio at 26.7% with Tier-1 capital at 23.7%.

- PAT at INR 324 crore against INR 203 crore in June 22.

- ROA at 3.80% and ROE at 29.80%

- Reverse merger - On the merger with our promoter, the hearing of our application with the

NCLT was completed on June 28, 2023 and we positively expect to receive the order

soon. - Loan book breakup: 73% microfinance; 14% Affordable housing; 6% MSME, 5% FIG lending.

- Avg Portfolio yield at 19.10% increased from 18.90% in march quarter. Microfinance

Yield at 21.80%. - NIM at 9.2% against 9.10% in march quarter. Cost of Funds at 7.2% against 6.90% in

march quarter. - Total Branches at 661. Opened 32 new branches during the quarter.

Disclosure: Invested.

9 Likes

At this juncture arbitrage opportunity of buying USF has narrowed down to 5%. Is there any development here other than the details shared by the management of USFB in the last con call? Please share.

Disclosure: Invested at lower levels a few months back and waiting for right time to exit.

You can check the NCLT website to see the case status. The next date of hearing is in November. Most likely NCLT will give the approval in that hearing.

There’s no hearing in November. Status is that the matter is reserved for orders and the order can come anytime now.

1 Like

at this stage, the NCLT order will be on convening meetings of shareholders and creditors only.

Ujjivan twins voting for reverse merger is approved by NCLT. Date of voting is 3rd November.

7 Likes

Ujjivan put its investor presentation out recently. The growth in IL and MGL is impressive, however the NIMs are down. Now I do understand that the cost of funds is increasing, people are locking in term deposits at higher rates, etc. However to what grade will the NIMs and the RoA get affected by the managements focus on these new, secured products? Ujjivan aims at achieving a higher %of secure loans. Do you think that this might be the start of a phase where the BVPS is increasing but the risk premium keeps decreasing? (Sorry if the question is too trivial, I am very new to the MFI space)

Good question, one whose answer we will only get to know when the transformation is complete.

This is because the valuations are a factor of full cycle ROE/ROA and growth.

As the book becomes more secured, book yield will reduce, subsequently, NIMs will also contract, but across a full cycle credit cost, provisioning and LGD can also potentially reduce.

I write potentially because if one is doing risky lending in the secured segment the credit costs can still be high.

Modelling the above with incomplete information at the current juncture will not be right. There are a lot of moving parts.

The CEO is due to change, and while they may follow the direction of the old management which will be guiding from the BoD, the CEO could have their own direction as well.

If the “small” tag is removed, because they get a universal bank license, the OPEX, funding costs, and CAR, could change substantially.

Currently, the PAT, ROA, and ROE is at a cyclical high due to outlier credit costs. As the credit costs normalize next year the PAT may stagnate for that year (I use may because growth from the book will still be there, and higher NII will balance against higher provisioning costs), ROA, and ROE will reduce to cycle average, BVPS will keep growing.

How the market will react to the above is anyone’s guess, will it punish the valuations by focusing on PAT, or will the sector be in euphoria due to the growth potential, and bad memory of new market participants about COVID, and DEMON losses? Who knows?

Lastly, there is always the risk of the cycle turning bad and credit costs being elevated. That can happen anytime and needs to be watched like a hawk always. But if the cycle doesn’t turn for a 5-year period, it could be a golden period from an investment return perspective.

Many fingurus, have a recency bias and have been calling a credit cycle top for the past year. They have even taken a small data point for DEMON, and COVID which were man-made outlier events and modelled that such shocks come every 3 years. Go figure. They forget to look at the cycles from the 2000s.

To conclude, I am not saying something bad can’t happen, it can at any time. But if they don’t you will miss the opportunity of a lifetime.

Valuation premium you need to judge what is being priced in. Post-COVID at 0.7 PB the market was overpricing risk, IMO at 3x 1yr FWD PB the market will be underpricing risk for a 25% growth CAGR.

2x 1yr FWD PB may be fair valuations for a well-run MFI, SFB IMO. Well-run means they are transparent in reporting, aggressive in recognising NPAs, and write-offs and quick to turn around as the collection efficiency bounces back. All of which Ujjivan has displayed since its inception in 2006.

11 Likes

RIght, I understand the conjecture when it comes to how the market reacts to the banks performance in the future.

In contrast to Equitas, which has its fixed book at ~85%, is there any information about what % of Ujjivans book is at fixed rate? I ask this as yield on current disbursements would be higher for Equitas than Ujjivan if the later has a lower fixed rate book, maybe? This could probably be a cause for the RoA to enter a cyclical downtrend till the cycle of normalizing the RFRs continues.

Thanks @hack2abi for sharing your thoughts, some great insights. Do you think the unfavourable credit cost base from last year along with higher funding cost are likely to result in depressed PAT growth at least in the short term (Q3-Q4 24)?

They should be able to do 1300+ cr PAT in FY24 if the status quo is maintained w.r.t. credit costs. H2 sees higher growth relative to H1. I expected a bigger reduction in the off-roll collections team this year, but that lever is yet to play in decreasing the OPEX. The management guided this, but the quantum of the reduction was never mentioned IIRC. Cost to income has already reduced even without this lever.

Honestly, I expected the PAT to normalize, and stagnate in FY24 itself, but the credit cost cycle had a mind of its own. I doubt anyone can predict when the normal will return. All we know is it will.

So, while it can happen, but H2 is not when the credit costs looks to normalize. If you go through the con calls of all MFIs, SFBs, they are all guiding 1-1.5% credit cost this year. Some are foolish to guide for next year as well, they can be ignored.

4 Likes

I feel it is more procedural and matter of few more weeks now ( Mgmt wanted to complete it before end of Q3 ) . Even if we account for another three months and make it end of Q4 , a 20% discount at current valuations looks attractive .

I feel that Ujjivan Bank itself would be a strong buy with yesterday’s election results . Considering it has one of the largest MFI books in Small Finance banks , unless we see signs of stress in portfolio . Considering their Provisioning levels , they seems to have create sufficient buffers for any stresses .

7 Likes

NCLT’s next hearing date is 30/1/2024. So we are still some time away from the reverse merger process approval.