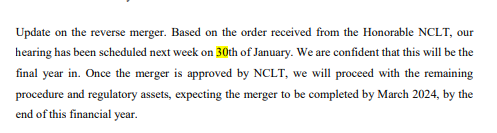

I assume NCLT has already approved it . What is this date for ?

NCLT had directed the shareholders of both entities to vote on the merger. Now that the shareholders have approved the merger, NCLT should give its final approval. But we have to wait till the hearing. Hopefully it should end in one hearing.

1 Like

Hello @hack2abi

Have loved your detailed posts in this thread.

Now that there is more clarity on the reverse merger, and valuation of the bank has improved quite a bit, how do you plan to play this.

Thanks for your time ![]()

1 Like

- Invested for the long term as long as the growth story keeps delivering.

- Keep following the credit cycle to play the bottoms, recovery, and euphoria.

- Key monitorable right now is who will be the next CEO and what direction they will take. Another one is the application for a universal bank. Probably Equitas will apply before them. If the application is accepted by RBI it may lead to higher valuations given the better return metrics it will unlock, if RBI rejects then it could lead to some near-term pain.

- Valuation rerating is mostly done—probably fair valuations at 2-2.5x current PB. The market can take the sector to euphoric valuations of 3-4x current PB but I won’t base an investment thesis on this.

- I would start trimming if valuations cross 3x 1yr fwd PB. At those valuations, the market will be underpricing risks just as it had overpriced risks by giving 0.7x PB valuation post-COVID. The market does overreact in extremes.

- FY24 should end at a BVPS of 28. Apply whatever PB multiple you think is fair on it. FY25 can end at 34 BVPS.

- Talking of absolute downside for an investor. Taking COVID as an example, such a black swan could wipe out 25% of net worth. So 28 could become 21 BVPS. The worst valuation during COVID was 0.7 PB maybe. So the stock could potentially go down to 14.7. This is a floor set as an investor on their downside. As the BVPS grows at 25% CAGR this floor will also keep rising. For someone who invested at 20, their investment will be above this floor in 2 years. Post that theoretically even a COVID-type event could happen again, and they won’t be in absolute loss ever.

- To conclude, stay vigilant at both pessimistic and euphoric times for wealth creation & preservation opportunities. Play the cycle and earnings the best you can. No one will be able to play it perfectly. You will be rewarded for the work put in and the risk you take on/off at the appropriate time but if you cannot take the stress of ups and downs in this sector, better avoid this sector.

14 Likes

2 Likes

Ujjivan will have its best ever quarter in terms of disbursement in Q4. The loan book will be record high, probably around ₹30000cr. NIMs will improve further from the low of September quarter. Inspite of normalised credit cost, the PAT will be highest ever and most probably reverse merger will also be done with by March end taking book value to around ₹29 per share.

It was a decent result according to me. This much stock price fall doesn’t make sense to me. What does everyone else think?

1 Like

Yes, it was an acceptable result. Last year was supernormal with very low credit costs. This continued till H1. It was only a matter of time. Even now 100 bps guided credit cost is below Pre COVID normal. For next year they have somewhat reluctantly guided 125-130 bps credit cost. A more firm number will be given after Q4.

Then there was the added OPEX from ESOPs, branch expansion, and possible attrition-arresting measures. Even NIMs are at a cyclical trough given in the rate cycle we are in. What I liked was the CASA growth given the tough environment. Much better than anyone in the industry.

Even with credit costs normalizing, NIMs muting, rate tightening, and branch expansion they will still deliver a mid-teen growth in PAT for the full FY24 YoY. They should manage to do 1250 cr PAT in FY24.

The good part is in the con call they said the merger will add 2-2.5 to BVPS. This will comfortably make FY24 end BVPS at 28+.

Now in FY25 even if they deliver a no-growth PAT of 1250 cr, the BVPS by FY25 end will be 34+ easily. If inflation eases and gives central banks room for easing rates, NIMs will expand for the entire industry. PAT should certainly be higher than 1250 cr in the next FY.

PB multiples are up to the market to give, unless some catastrophe strikes 2x looks like the norm given by the market. Could expand to 2.5 or even 3x if the market wishes so.

Now, the only thing I do not like and should be monitored is their secured book expansion. Throughout COVID and now the unsecured micro book has better collection efficiency than affordable housing and MSME. And they do not provide any further segmentation on how much of AH and MSME is micro-LAP. I like the unsecured better but they are not growing that as fast as someone like CAGL is. Yes, unsecured has 0 LGD, while secured could have 50% LGD. But for now, CE, credit costs, and NPAs for secured book are not providing comfort.

Then there is the issue of CEO change. By Jan-25 they need to pick a new CEO. The last outsider pick ended up in a disaster. I hope they pick some insider this time who understands their culture and values better.

Post the merger we should see some selling as the opportunistic arbitrageurs who are not in it for the long term will exit. If they apply and get a universal banking license, the stock PB can get rerated as the operating cost burden should be reduced. Equitas will probably apply 1st for this process to RBI so whatever outcome RBI decides should rub off on this bank as well. RBI can reject the application as well so this is both a risk and opportunity.

Overall, the medium-term future is the same as any other stock, many knowns, unknowns, risks, uncertainty, opportunities, growth and quality. What gives me comfort is the management quality, competence, discipline and transparency. Investors are rewarded for the uncertainty they take on, no stock ride is easy for the long term.

13 Likes

As I heard. Merger will add 2-2.5**%** to BVPS, not absolute 2-2.5 rupees.

Thanks & Regards,

Bharat Kothari

Phone 7685806922

Merger will add the cash of Rs. 211 cr in HoldCo to the SFB and also there will be share cancellation. In overall the BVPS will increase by more than 2.5 per share

2 Likes

4.07 cr shares are being cancelled and assuming 211 cr cash on books comes in with merger the book value would rise by Rs. 1.65 per share due to merger.

Net worth as on 31.12.23 = 5083 cr + 211 cr = 5294 cr / (191.58 cr shares).

2 Likes

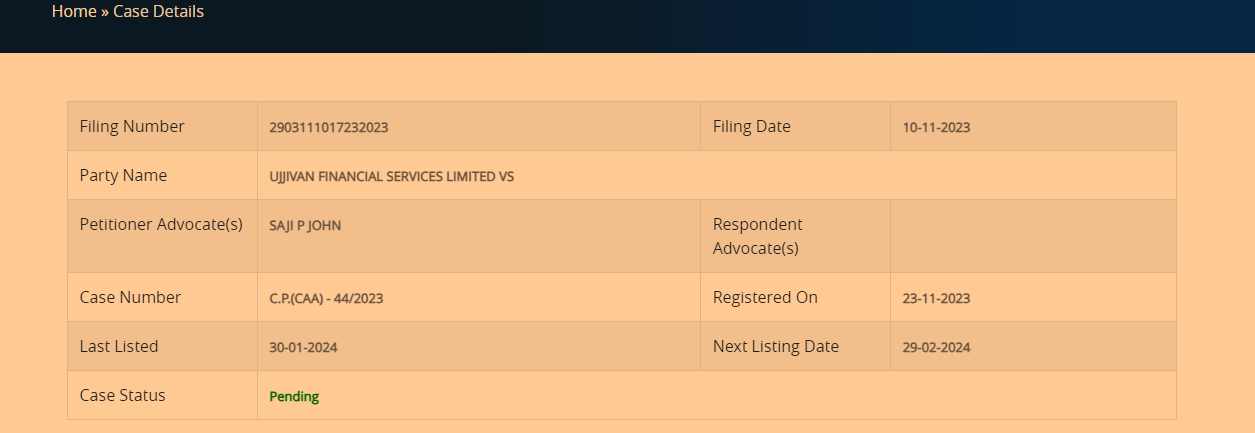

Any update on the NCLT hearing today?

Investor call transcript

Ujjivan’ note to Exchanges

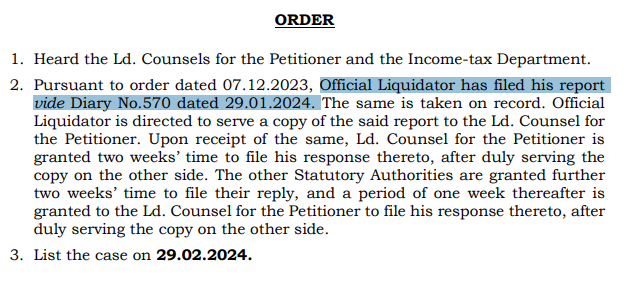

NCLT’ 30th Jan order

Looking as above this is not just simple adjournment of the case. There is liquidator’ report which has to be replied to. In earlier meeting of 7 December 23, company was asked to serve the notice of the Petition to (c) the office of the Official Liquidator along with other 6-7 authorities. among them probably one responded. NCLT must have considered it worth seeking a reply from the bank (petitioners), that’ why this new date, unlike what Ujjivan seems to portray.

Disclosure: Invested

2 Likes

With same management of both the entities what are the reasons for your concern

2 Likes

Earlier merger was supposed to get over by November 23, now it is already shifted to April 24.

There is no major concern, as you mentioned both the entities are under same management, but some irritation as management commentary and timeline does not match the actual notices narration and timeline.

3 Likes

In Feb 2020, the share price of ujjivan small finance Bank was around 56. After 4 years and 3 fold growth in revenue and profit the share price is still the same at 56. What should be it’s fair value in these market conditions, given that PSU banks have much higher P/E ratio?

Short explanation:

It was overvalued then at a PB of 2.4. It is fairly valued now at a PB of 1.84 considering the growth rate & future prospects.

P.S Valuations are subjective and this is just one way to look at it.

3 Likes

When it was listed the BVPS was ~18 IIRC. At the price you mentioned, the PB was ~3x.

Before the market realised that UFSL should get a hold co. discount, the market used to value it at a higher PB multiple as well. Then the weakness of the business model came to light once with DEMON and then COVID.

During COVID, the PB compressed dramatically as the market overvalued risk and 1 yr fwd PB was less than 1x. Those who understood the quantum of risk materializing and the discrepancy in the market’s valuation reaped the rewards of the subsequent rerating.

Now, one must run a reverse DCF with growth, ROE, and COE parameters to judge a fair multiple. Full cycle credit costs and resultant average multi-year ROE is needed as inputs. Since the loan book itself is changing it is very difficult to accurately estimate this.

As I have discussed here before, a broad range of fair PB for a financial company growth at 20+% and 15-18% ROE is 2-2.5x. During periods of fear, the market will overvalue risk and PB can go below 1x during euphoric times when risk is undervalued the market can even assign a PB of 3-4x.

One must recognize where we are in the business, valuation and market cycle and try to play it accordingly without getting affected by the stories floating in the market. Going against the crowd is tough intellectually and emotionally.

If we buy or sell at the wrong time one of the outcomes is as you mentioned, the other can be of a famous Pune-based PMS which exited at a big loss at the bottom in Apr-22 and missed a subsequent 4x opportunity.

12 Likes

Hello,

Any clarity on the reverse merger? Thanks