Why is the market allowing almost 50% arbitrage gains between Ujjivan Holdings and Ujjivan SFB?

Anyone with the bear case on the same.

Thanks.

The obvious answer is that the market is not convinced about the reverse merger. The question is why?

Is the Management not good enough to execute the reverse merger? Samit Ghosh has returned but at his age is it fair to expect Ujjivan to really deliver?

-

This is a merger between holdco and operco. Mgmt. This is a standard merger and mgmt. Has less to do with it.

-

Merger will require approval from SFB Shs who may not be happy with the merger ratio. Merger ratio should have been decided at average of past 6 months price.

-

The sector has gone through a big event in COVID and Ujjivan with Bandhan were the most transparent in reporting the numbers. In Q4 they have the best NNPA, PCR and CE in the industry.

-

Uncertainty stems from 1 year term of Mr. Ittra, but what stands out for me is the organisation functioned and delivered best in industry numbers despite a top and middle management transition during its weakest period.

-

QIP will be around November and should come around 1.5 to 2x PB is my hope. FY23 PAT would cross 550+ cr and would lead to a BVPS of 17-18+ by end of FY23. I expect the SFB to trade at 35 by the same conservatively.

-

Currently investor interest is lacking due to 2 loss years reported and erosion of BVPS from 17+ to 14+. The FY22 low was due to tax loss harvesting and should never be visited again if we get 2-3 years of sustained operation. Once they start reporting +ve PAT and growth in BVPS from Q4FY22 onwards, investors will come back and even UFSL should see interest from arbitragers.

-

It is an easy 2x in FY23 for SFB and probably 3x for UFSL. Even if the merger doesn’t go through, which is highly unlikely, the value of holding in SFB will provide a bottom which will keep increasing.

Sir, I have recently taken a position in Ujjivan FSL because of the reverse merger “work out” opportunity. I have a few questions.

- What are the possible reasons for the deal not going through and what are the odds of it falling through?

- I believe after the deal, the SFB’s outstanding shares will be less than that before the deal as the shares held by holdco will be cancelled so, their shareholders should be happy right?

Anyone who has studied this special situation opportunity, please feel free to reply.

The reverse merger is required to be done because of the regulation of RBI regarding promoter holding and bank holding cos. Understanding this regulation is the key to understanding these 3 cases - IDFC, Ujjivan and Equitas.

Since you are approaching this as a “work-out” play, get an overview of these regulations (consider this as an important analysis step ) , check out the timelines and value arbitrage, calculate the IRR and invest accordingl. Share learnings here for fellow Vpickers, if u like.

u vl hv discovered answers of above questns & probably unearthed the most undervalued situation

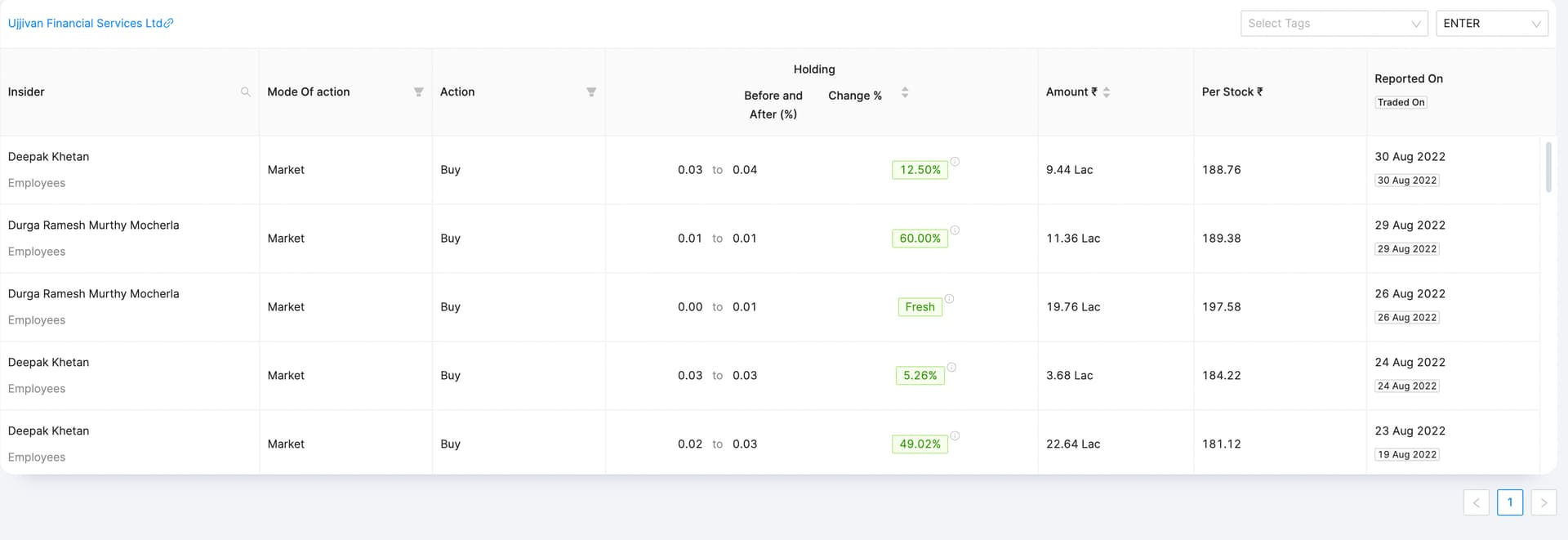

Recently insider trade details in Ujjivan Financial Services Ltd

.

UFSL is a holding company of Ujjivan small finance bank (USFB). Holds more than 83% . RBI reguatory enforced reverse merge unlocks UFSL holding discount.

.

Ujjivan Financials Board of Directors have announced a share swap ratio of 115 shares of Ujjivan SFB for every 10 shares of Ujjivan Financials held by the investor.

.

share swap ratio of 10 shares of UFSL = 115 shares of USFC which is potential upside of 22% from current price ( as of 2nd sep 2022 ).

.

USFB is currently having low NPA ( non performing assets ) among all small finance banks.

.

I have spoke with one of the employees recently that the merger is in-progress and in 6 months period of time it is expected to be completed.

.

Disc : Invested

6 months? First bank needs to do QIP to bring MPS to 25% ,then they need approval from RBI, exchanges, SEBI, NCLT etc which is at least 15 months process.

Agree with you, 6 month timeline is wrong. Maybe the employee has mentioned about QIP.

.

To further confirm your statment.

The is the management has said in conference call

In 3 months they need to meet the criteria ( Jul concall )

by December, we need to meet the

SEBI requirement of minimum public shareholding, so we will meet the SEBI requirement.

( May concall )

.

after we meet the MPS requirement as SEBI has

asked us to meet, we will have to go back to SEBI, exchanges, and RBI to get the NOC’s and

then move to NCLT and shareholder approval. On the timeline, I cannot comment whether it

will be one-and-a-half to two years. It also depends on how quick these regulators respond. So,

there is a parallel process going on with one of our peer who is in a similar process and they

have recently announced that they have got one of the regulator’s NOC and they are moving on

that. With the precedence set on the particular subject, I think that the movement for us can be

faster when we go there. That is just our assumption and we will see how things move when we

go there, when we cross the bridge.

RBI is approved the merger scheme between Ujjivan SFB and Ujjivan Hold co. The share exchange ratio is 11.5:1. With bank trading and 30, Ujjivan holdco derived value stands at 345. CMP 290. There is arbitrage of 20%

Is this understanding right?

regards

Disc: Holding Ujjivan hold co.

@narenarora You are right. There is a ~20% arbitrage available. This will start tapering as company getting a step closer to merger. In case of equitas, arbitrage is very small

Arbitrage is the wrong phrase to describe this - this is because arbitrage means guaranteed profit without risk. Here if the OpCo share falls more than a certain percentage (approx 16.7%) then buying holdco at this level would yield a zero return. Maybe you could call it “swap ratio margin of safety” rather than arbitrage to be technically correct

Yes, this price difference only makes sense only if you are either a existing shareholder of USFB and willing to hold for a year or those who tries to make fresh position in USFB for more than a year.

As mentioned by @arsh13 , if someone who wish to make money out of this, they have to keep in mind they can make money only when UFSL starts moving up and bridges the discount. If USFB starts dropping and USFL holds the price, then this becomes meaning less.

Disc: was invested in USFB, post RBI NoC, switched my holdings to UFSL

Q3FY23 CCT Notes

MISC.

We serve 7.3 million customers through 607 branches and an employee strength of 17,000.

Board will identify next CEO and he will work with me over next year to succeed me,

Growth

This quarter, even post-implementation of the new credit MFI norms, we disbursed INR 4,838 crores and almost another record from the previous quarter. The system took a little while to settle down with the new norms but now all is back to normal.

This quarter, even post-implementation of the new credit MFI norms, we disbursed INR 4,838 crores and almost another record from the previous quarter. The system took a little while to settle down with the new norms but now all is back to normal. In fact, December ’22 was the highest ever monthly disbursement for Ujjivan. Our gross loan books grew 5% sequentially to INR 21,895 crores

Asset Quality

total write-off of INR 179 crores

On the asset quality, our collection efficiency continues to be around 100%, taking our PAR further down to 4.9% from 6.1% as of September ’22. If you look for year-on-year improvement, it is around 1,000 basis points. As of December ’22, our GNPA is at 3.4% and NNPA is just 0.05%. Also, our SMA book, as well as restructured book have shrunk further indicating the reduced stress. The restructured book is now just INR 302 crores with collections, almost in line with the overall book.

Floating provision is governed by RBI norms. So it really depends on when the Reserve Bank of India allows us to take a call on floating provision. We have represented this matter to Reserve Bank of India and we are waiting for a response. So we have to just wait till RBI comes back to us, because this is under a regulatory guideline.

Deposit

Asset growth was outpaced by the growth of our deposits, which grew at 14% sequentially, registering the highest ever quarterly inflows of INR 2,806 crores. Growth in deposits is in line with our guidance of reducing the CD ratio and bringing it closer to 80%, in line with the rest of the banking industry. Our retail deposits grew 15% sequentially and CASA grew 10% sequentially in a market where most banks are witnessing negative CASA growth. I believe this underlines our efforts towards building a granular liability franchise

So we have not taken any TD rate hike after November. The last we took was November and after that market has seen a decent amount of rate hike and we have not been taking rate hikes. We are still seeing very good flow on our liquidity side, our deposit intake, we just mentioned, Mr. Davis mentioned in his speech also, this quarter was very good in terms of overall deposit inflow. In fact, we got INR 2,800 crore of deposit inflow. And in January too, we saw very good amount of deposit inflow. So we haven’t taken rate hike. And as of now, we are feeling — we feel comfortable with that…

Guidance

We expect Q4 ’23 to be similar to Q3 ’23.

Financial year ’24 branch addition would be close to between 50 and 70. Focus is to expand in deposit-rich catchment areas.

Overall, we expect to grow our gross loan book by about 25% in FY ’24

Will focus on CASA to control pressure on NIMs due to COF increase. CI ratio will be kept in control. FY23 exceptionally good in credit cost. Not be repeated. Next year we expect provisions to move up towards 1% on average gross loan book and recoveries though significant, this would be lower than financial year ’23.

Current focus was on quality customers than quantity and thus ATS has increased. Future growth will be through new customer acquisition.

we are developing several of our secured products, which will be launched into the market next year, that will help us. And we are also growing our secured housing and MSE portfolios. There are some system changes, which are taking place right now, which will help us to grow these portfolios faster.

So in the short-run, what has happened is that, post-COVID, we were more prepared with the micro-banking business as an overall to — to come out of COVID. So that is why it has grown faster. But eventually, the other businesses, the secured portfolios will have to catch-up and overtake in terms of rate of growth, but micro-banking will continue to be an important part of our portfolio. And as I said, eventually, in five years or thereabouts, we are looking at a 50-50 breakup between secured and unsecured debts. the micro-banking portfolio is doing much better. We also need to see that the micro-banking portfolio is much more profitable also and giving us that kind of income that is required for the business to invest in all other businesses that we have.

So today, about 26% customers pay us digitally. This not only is convenient for our customers, but at the same time, it reduces your opex as well. As far as long-term numbers are concerned, we are looking at first looking at the milestone of 30%, but the data which is available in the market, that says that close to 40% to 45% customers at this point of time have smartphones, and we are targeting these customers in the next financial year, and this number will gradually increase. So we are looking at gathering more and more customers into a digital repayment so that the entire process of collection becomes much more inexpensive.

In this kind of a business is 2.25% to 2.5% kind of a sustainable ROA is easily manageable. And yes, and with a few years being exceptional like current year was a good year for us as an exception. So we are having that 4% kind of a return. And ROE is largely a factor of your what kind of capital adequacy you are maintaining.

Expect 300 cr in Q4, H2 600 cr, FY23 - 1200 cr PAT.

I mean, definitely the pricing on the secured book is lower than the micro-banking book. But we hope that the credit quality and other aspects will also enhance - the longer-term return on assets will be around the 2%, 2.5%, which is what we expect. And also the return-on-equity will have to be in line with what we are expecting from the market for this sort of thing. But the main thing is that, we build a balanced book and the risk is mitigated through this process.

We are turning around. And this year, we have had fantastic recoveries. Our collection team and our credit team have worked extensively with our customers. And what we are seeing is perhaps second to none in the industry, at least definitely in the small — SFB space. So I think that is helping us. Now, this cannot — this is a very unique situation. And when we come to a more normal environment next financial year and beyond, the things will be different. And we’ll be operating at a normal thing, not at current levels of profitability. It will come more normal profitability. But we expect the business to continue to do well and go back to what we were doing pre-COVID days in terms of how we were operating at that time. Our profitability was good, and the business was doing well. So I think when we get back to normal conditions, that is what we are aiming for.

Maybe the interest rate environment, so far we are not seeing a problem with loan growth. And that, I think, is not just us, the whole industry is continuing to see because we are coming out of COVID and there is a demand for credit. So I think that will continue into next year as well. Now if interest rates continue to remain high throughout next year, then we’ll have to see how to address that situation. But the whole industry is expecting a turnaround or a decline in interest rate to start sometime in the second half of the financial year, definitely. So once that happens, I think the credit demand will continue to be sustained.

Merger

Now an update on the merger with UFSL. As per the update published by SEBI on their website, basis our submission of scheme documents with the exchanges, the NOCs have been received from both the BSE and NSE on January 6th, and SEBI is in the process of seeking clarification from other regulatory bodies. Further, Reserve Bank of India has given us notice to our application, which was uploaded on the exchanges last night. Once we are in receipt of the SEBI clearance, we will proceed to file the application with the NCLT. On submission of our application with the NCLT on receipt of their requisite regulatory and shareholder’s approval, we will positively expect to get the proposal — the proposed merger completed by September this year.

MicroFinance

Micro banking continues to be well backed by strong credit demand, while we did see some hiccups in process due to implementation of the new MFI credit norms, but that is all settled down now and we are seeing good disbursements.

Individual loan is something which is we offer to our customers after completion of one GL cycle, but largely, we have seen that customers opt for individual lending generally after two or three cycles. 90% of our customers in individual loans are the one who graduates from the home loans.

So yes, the entire acquisition process for GL lending. GL lending is something which is very old in Ujjivan. We have been doing GL lending business for last about 12 years. And process is — the product and process is that, as far as Ujjivan is concerned. The entire acquisition process and collection process is separate from group loan business. The customers who graduate to IL, the underwriting mechanism is very, very different which is they are in group loan. And apart from that, we have completely independent credit team right from the field to the top, which is — which has no relation with the business team and a great team besides upon ticket size and customer acquisition of GL lending customers.

We have consciously not taken on board any customers who we or anyone else have written off in the past. They are not in the qualifying list for acquisition.

So about 35% to 40% is disbursements to new customers, the NCA, and between 65% to 70% are existing Ujjivan customers

MSME

You would have noticed a small decline in the MSE book. This is in-line with what we have been mentioning since the last two calls that we are adjusting our strategy there and we’ll see growth once all changes are in place, and systems also upgraded for that.

The micro and small enterprises, we are currently in a transition phase and investing and expanding our product suites and services to be more relevant to the semi-formal and formal segment. Also, we are upgrading our technology platform to serve the customers better.

So on the MSE side, yes, I mean, we did speak about revising our strategy. We will be focusing a lot on the shorter tenure products in the strategy, going-forward and also our customer segment will move towards the semi formal and the formal segment. So this is something that we’re working on. And also we have launched the product called Prime LAP for our customer segments for the longer-term loans. And this would be facilitated also to a large extent through our growth in FinTech partnerships.

Affordable Housing

The other businesses that we have, one is housing. We are pleased to say that we have crossed the INR 3,000 crore OSP this year for housing. Incrementally, we are focusing on semi-formal in Tier 2 and Tier 3 towns. We implemented a state-wise collection collateral policy and ROI metrics and recently — and increased productivity. Consequently, the business has turned profitable. And we have now opened a couple of new asset centers as well, where housing will be operating out of these centers.

Vehicle

Vehicle finance, our IT integration is in place. We look to scale up the business in the coming year, once this is fully operational. Currently, we are doing limited business, majorly with ETB MFI customers. Now we are looking to focus on the new to bank customers as well.

Gold

Among other secured businesses, we are looking to scale up our gold loan business once the test marketing is completed and this will be done commercially across 50+ branches.

First thing is that we have entered into gold loan market. We have launched it in some branches, and we are testing, and we intend to start operation in about close to 50 branches next financial year. You are right that the competition is intense in gold loan, but at the same time, we see that in our micro-banking customers, the overlap is close to 10% to 11%, and that is a huge number. And we see that our customer is in demand of gold loans and because we are giving loan, we are also trying to offer them gold loans.

Apart from micro-banking loan, we have other customers also in the branches, including branch banking, MSE and housing, there also we see demand. And looking at the customer demand with an in-depth survey with the customers and even open market customers, we decided to enter into gold loan market business. And this will allow customers to take a one-stop-shop kind of solution where they can get all kind of loans that they need from us. At the same time, it will also help us increase our secured loan portfolio, which we target to reach 50-50 in the next five years.

And in addition, we will be launching this product in identified geographies, where we believe that it makes sense for us.

FIG

Also our NBFC lending business is doing well with Nil delinquencies

Fee Income

We are focusing on our fee income with the addition of new products like 3 in 1 account, NPS and mutual fund in FY ’24. We are confident that the new initiatives will start materializing in the second half of ’24 one by one and you will see this impact.

Competition

Overall, see, for industry-wide, there is a lot of banks, what we are seeing is there’s a lot of passon that most of the banks are doing in terms of the interest rate hike. In fact, we have not been doing that, for example, in micro-banking, while peers have passed on a lot of rate hike, we have only taken a 50 bps rate hike so far. Even in housing, like Mr. Davis mentioned, it is linked to EBLR, the increased rate that we have done for the new disbursement is around 90 to 100 bps. We have not passed on yet. So we still have that up our sleeve that we will be able to do a little bit of a rate hike, and that’s what he mentioned in his speech also that for whatever cost of fund hike is there, we’ll have to see how we increase our yields going ahead.

Good questions

And this long-term ROA sort of a thing that you’re looking in the range of 2%, 2.5% seems to be pretty low compared to where we are already at 4.5-odd-percent because it would mean essentially that even if you are going to double your asset book in three years, perhaps with 25% growth, you will still be at the same level of profit after tax or something like that. So is that overly conservative guidance? Or what is leading to this sort of a number?

So what we said as a sustainable ROA. The question was the sustainable ROA in this kind of a business. This year, as you are aware, the credit cost is almost negligible and the bad debt recoveries are quite high. That has increased or that has skewed the ROA this year towards on a higher side. But a long-term sustainable with all the changes that you’re talking about, the ROAs sustainable should be around 2.5 percent.

Source:

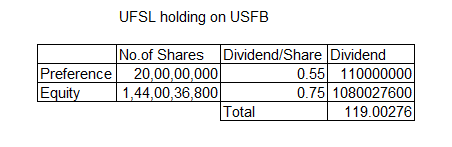

USFB announced 0.75 and 0.55 per share for equity and PNCPS respectively. So UFSL will get 119 crore as dividend, hope same will be passed to shareholders of UFSL.

Hello!

Just wanted to check if new IT rules on debt funds would be a positive for ujjivan since it would be easier for them to get deposits and this might lower cost of funds.

Thanks

CUD U PLZ EXPLAIN IN SIMPLE TERMS ? unable to undertsand specially impact on ujjivan sfb

Move is likely to benefit banks offering higher interest rate on Deposits (including Ujjivan SFB); As HNIs are expected to move some of those funds to bank deposits.