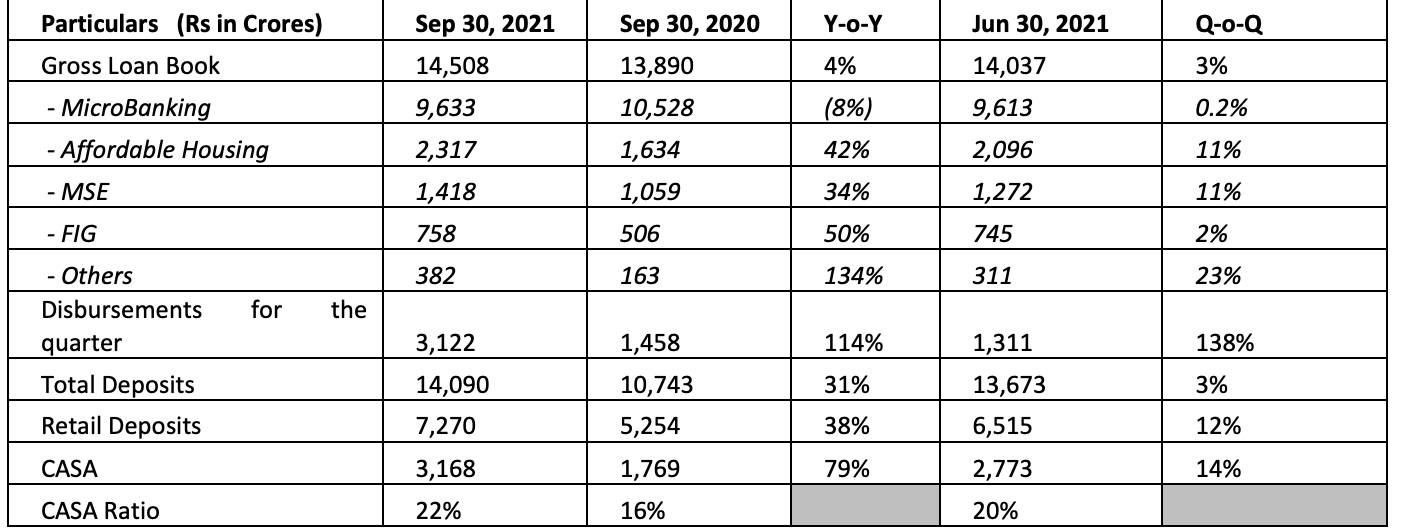

Hi

Greetings!!

Any idea why Ujjivan financial services posted huge loss in current quarter…NPA provisions? hit the bottom line?

Hi

Greetings!!

Any idea why Ujjivan financial services posted huge loss in current quarter…NPA provisions? hit the bottom line?

They have taken impairment on their financial assets, which means they expect it will go bad in the future. How good or bad this practice is I am not sure.

Hi,

This depends on how aggressive provisioning strategy a bank has adopted (whether you provision now vs lesser provision now and declare later as bad). Ujjivan and Bandhan have been more aggressive in provisioning. Covid provision / loans for Ujjivan in Q3 (5.50 %) and Bandhan (3.57%) . Bandhan has provisioned 1000 Cr in Q3.

Here’s an extract from the earnings call. They have front ended everything w.r.t provisions. No provisions expected from Q4 onwards

There is a huge difference in P/B Ratio of Ujjivan Financial Services (at around 1) and Ujjivan Small Finance Bank(Around 1.9). Ujjivan Financial Services is the holding company of Ujjivan Small Finance Bank.

Request some seniors on the forum to explain why so much of difference in P/B Ratio.

holding company discount of 50%

Deposits growth at 31% YOY. – I think, due to 7% interest rate offering in saving accounts

Minor growth of loan book - 4% YOY – conservative approach

Similar to IDFCF bank, they can also grow CASA very easily.

Asset quality remains to be seen in this quarterly results.

With the appointment of new CEO and improving asset quality, it can easily re-rate to above 2 P/B, (hence giving 100% returns) in next 1 year.

Thoughts ?

Disclosure: Invested

Any update on the merger date, approval, specs etc…

What is impact of fund raising by Ujjivan Small Finance Bank on the Ujjivan Financial Services.

Attached the announcement by the Ujjivan Small Finance bank for fund raising.

69132c5c-f381-4260-affe-56e528e86744.pdf (266.6 KB)

Its a regulatory requirement for listed entities to have 25% public holding, within 3 years of IPO. So they need to increase public holding from 17% to 25%. This will precede the reverse merger of the holding entity with the bank. Besides meeting regulatory requirement, fresh capital will also help drive growth in next year or so.

600 cr equity infusion is for sale of 8% stake in usfb? As of today’s mcap 8% stake would fetch 256cr so looks like dilution will be close to 16-18% to raise 600 cr thru equity

Board resolution is for up to 600 cr. They may not go for the full amount.

If the qip goes through it will bring down the holding to 75% . Does this will have change in holdco discounting and other valuation. I saw one report from hdfc securities that gives almost 60% upside to ujjivan financial

Any red flags recently after 3rd results and concall? Stock is tanking in a way which feels like some negative news being factored into

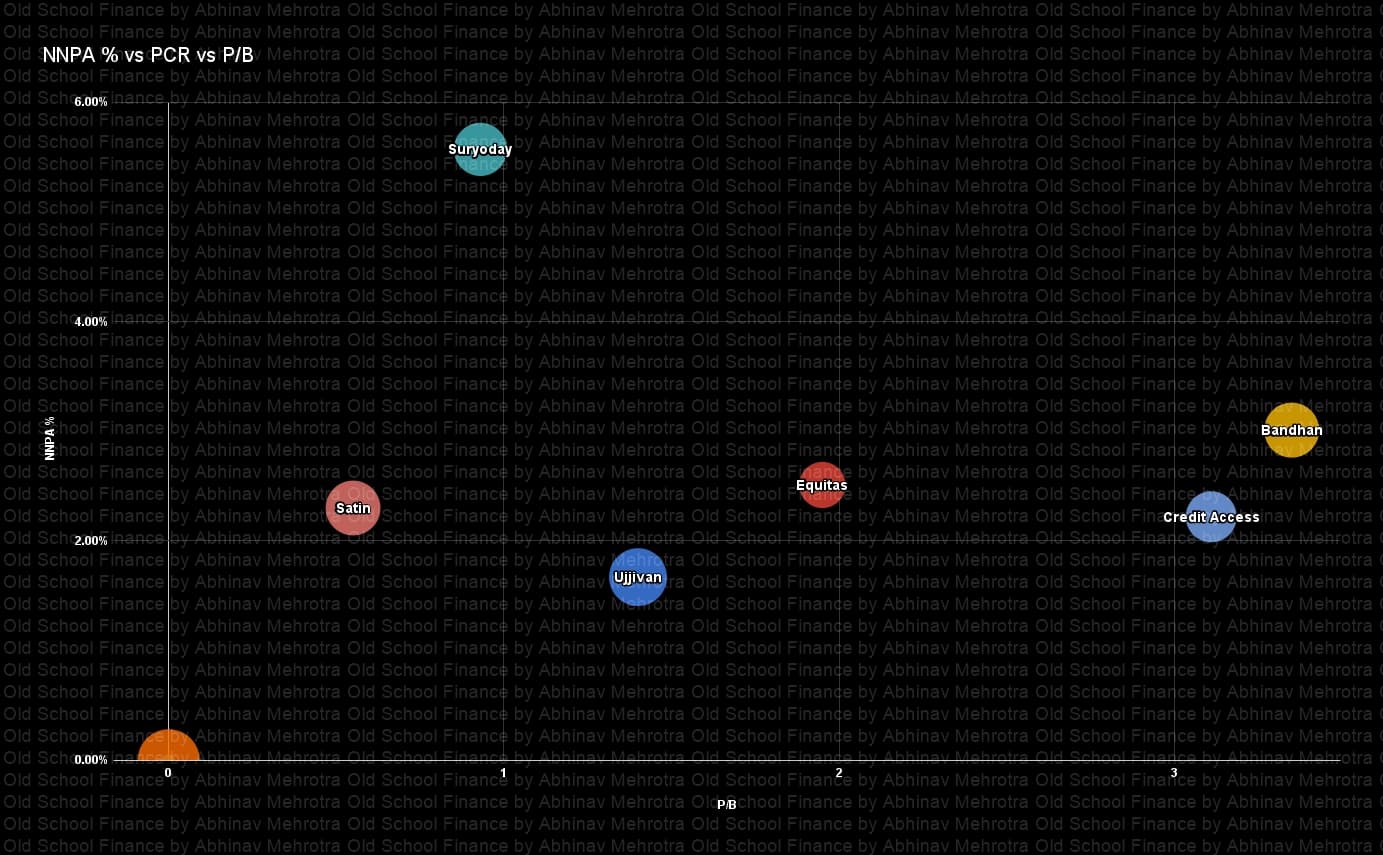

Bubble size representative of PCR

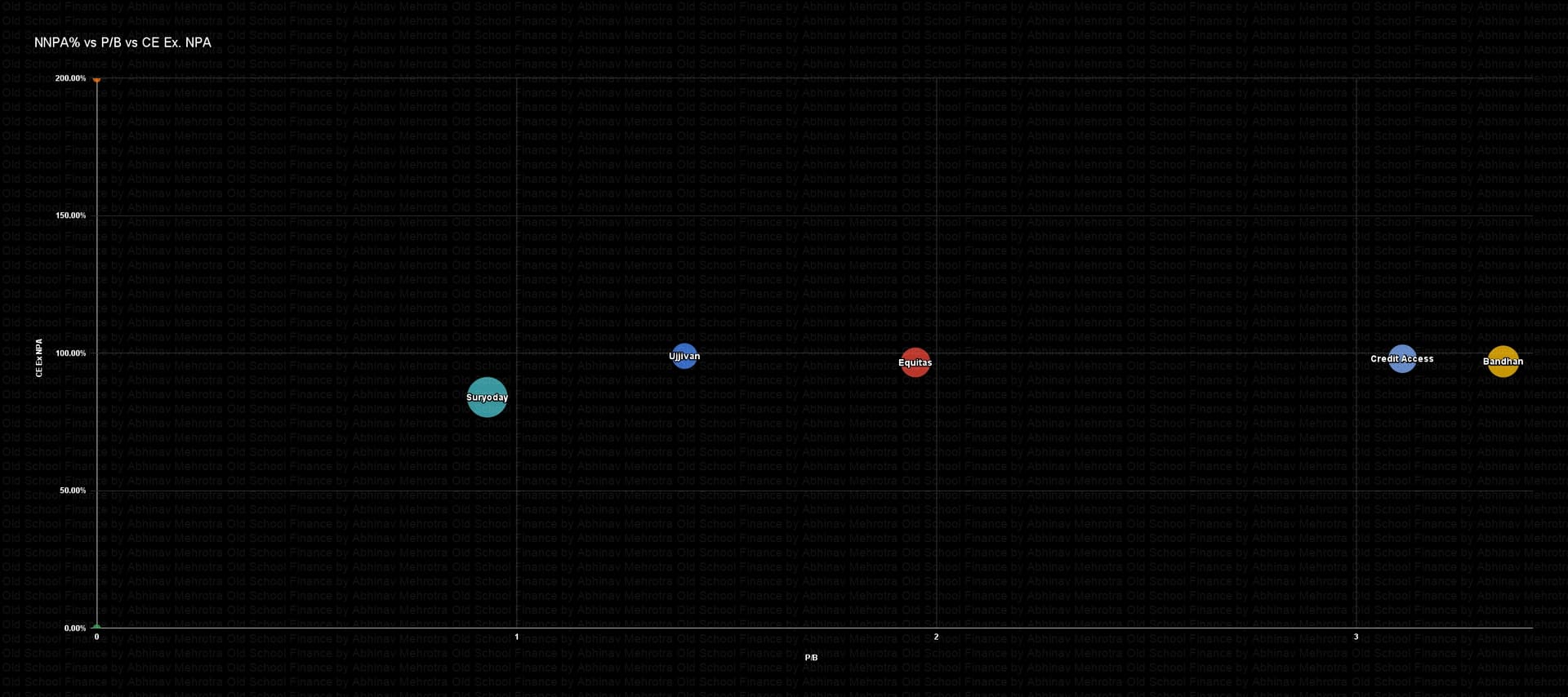

Bubble size representative of NNPA %

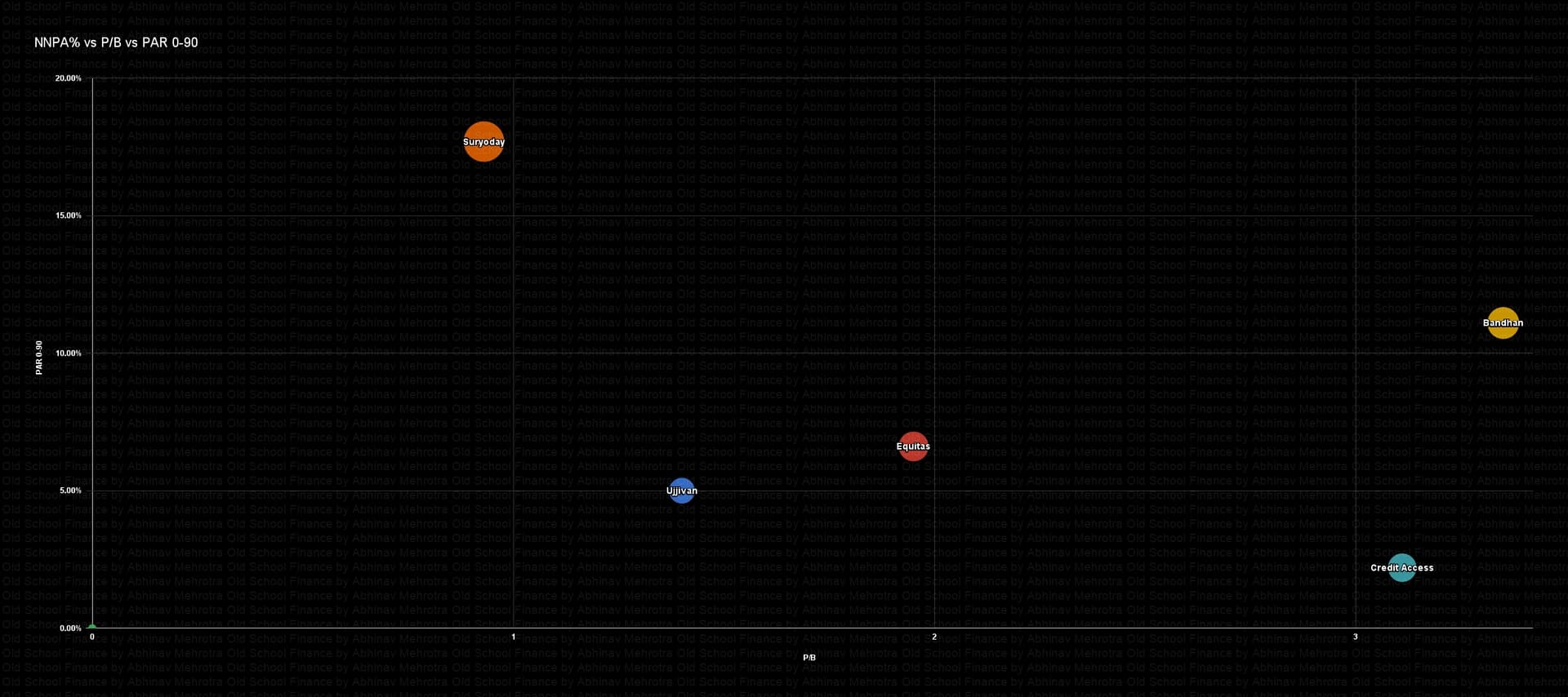

Bubble size representative of NNPA %

I tried to understand the graphs but couldn’t.

Could you also add textual comment on which banks / SFBs are doing good / bad wrt each parameter?

X-Axis is Price/Book ratio.

Y-Axises are NNPA %, Collection Efficiency Excluding NPA and PAR 0-90

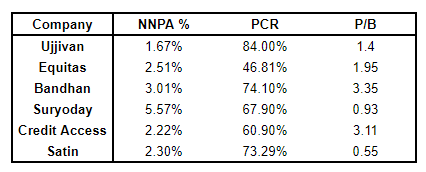

Ujjivan amongst all microfinance lenders has the lowest Net NPA % which means all current stress from COVID waves has been provided for.

Ujjivan has the best PCR, PAR 0-90 and collection efficiency in the industry as well. So additional stress should be the lowest in the industry.

Equitas has the least information in their IPs. Equitas PAR numbers are 31 to 90 while all others are 0 to 90. Bandhan CE numbers are for EEB segment.

Just for clarification here, Equitas isn’t purely a Microfinance institution. 15% types of the book unlike others with 80%+ exposure to microfin.

Disc:- invested in Equitas.